University of Sunderland - APC308 Financial Management Assignment

VerifiedAdded on 2023/01/23

|8

|1328

|55

Homework Assignment

AI Summary

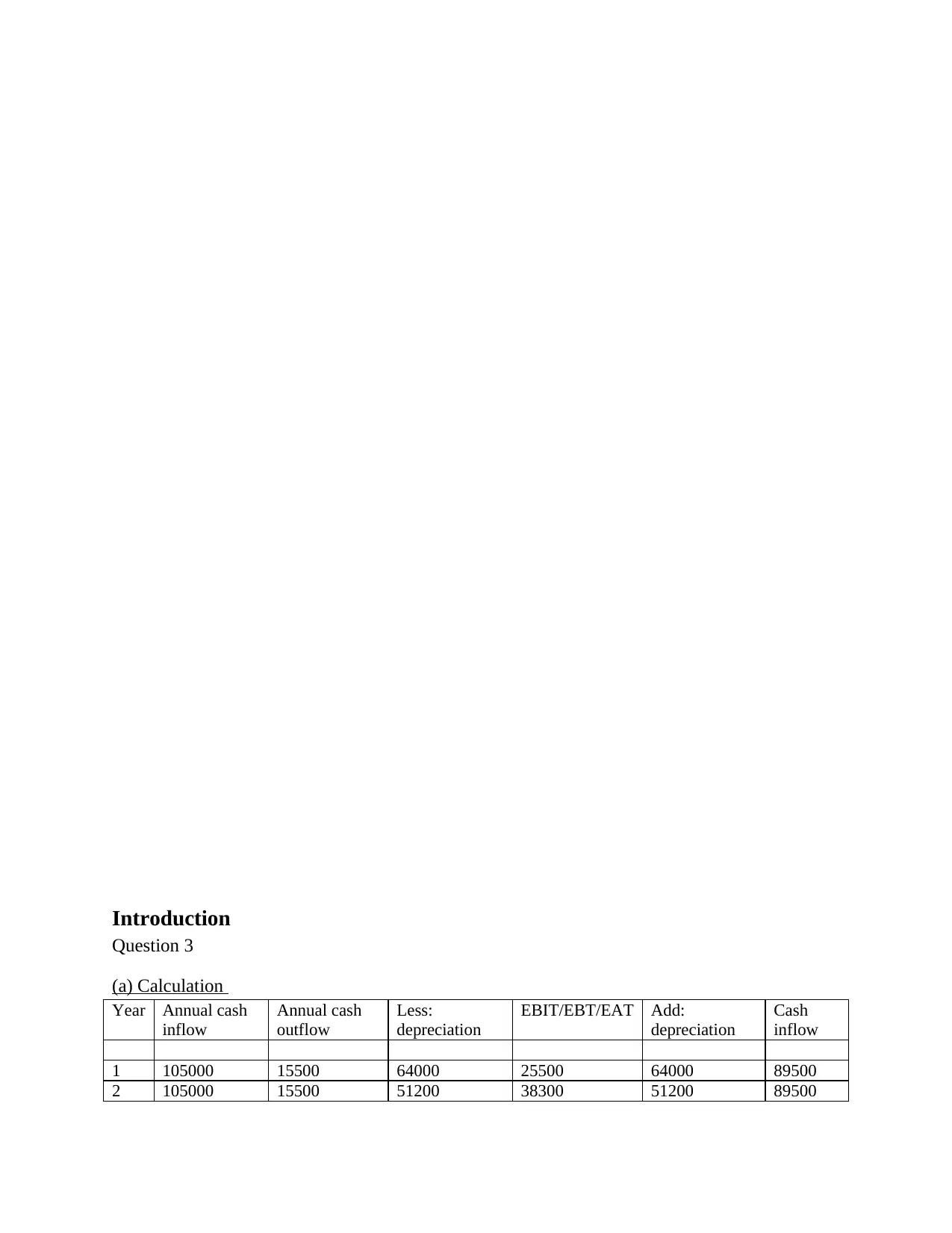

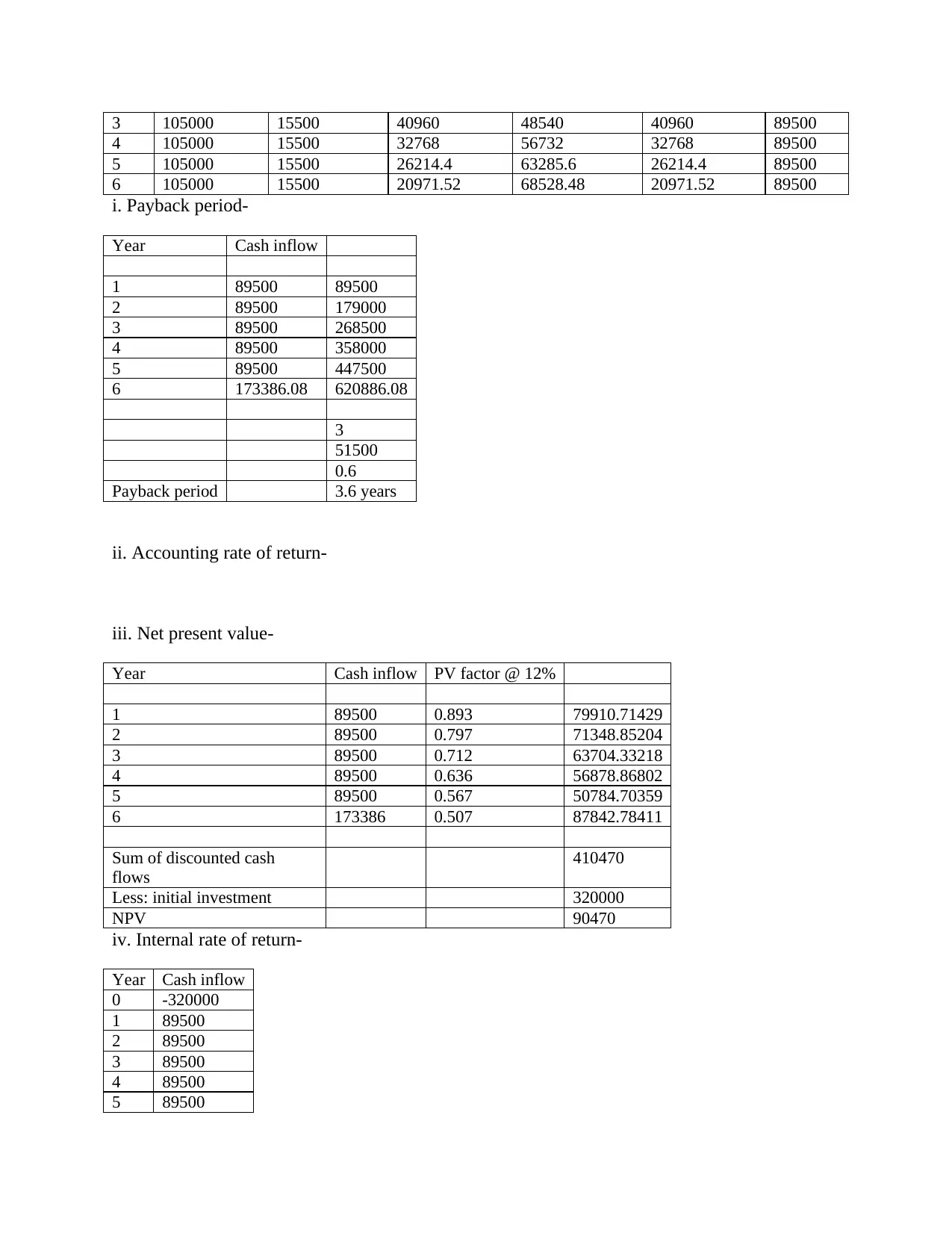

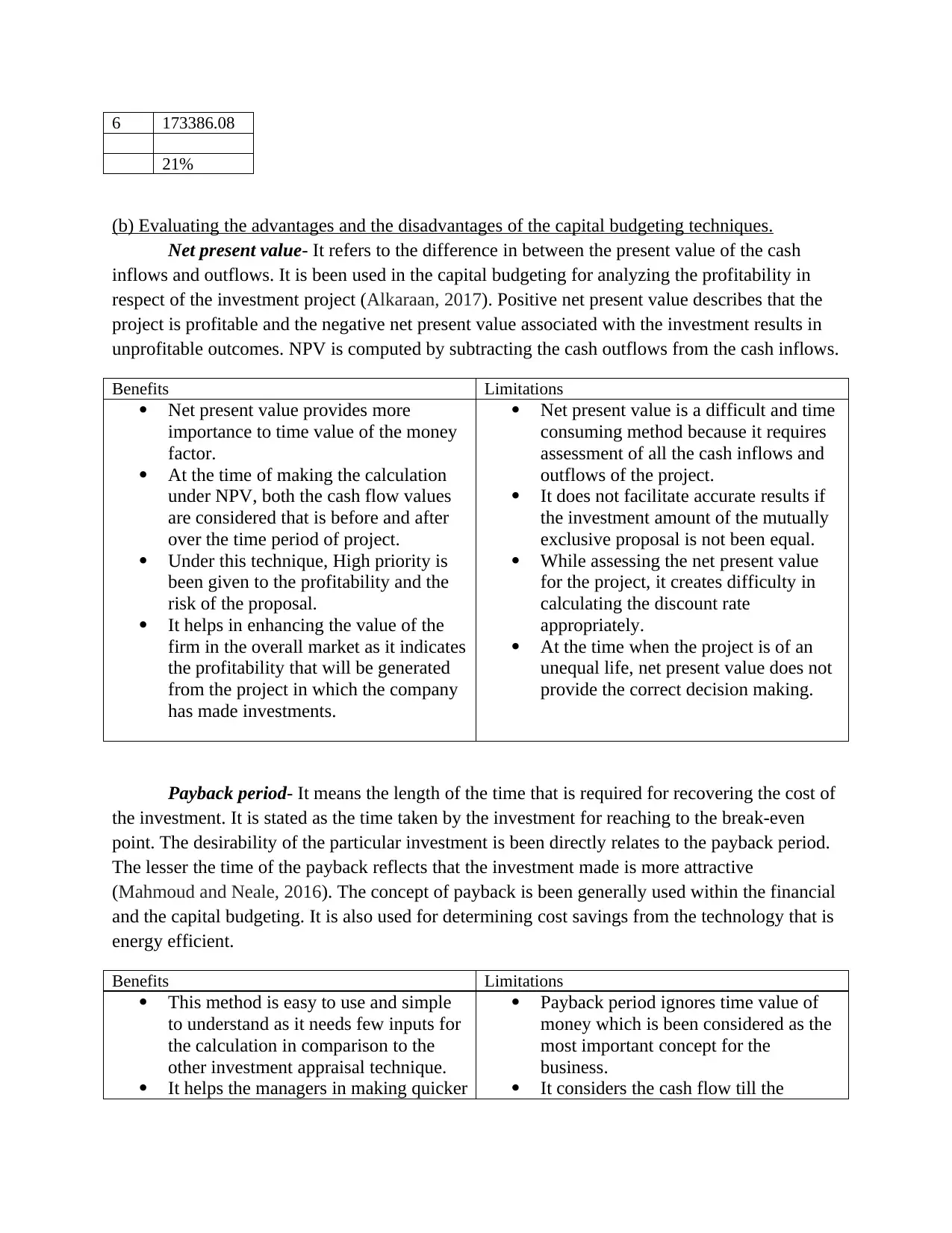

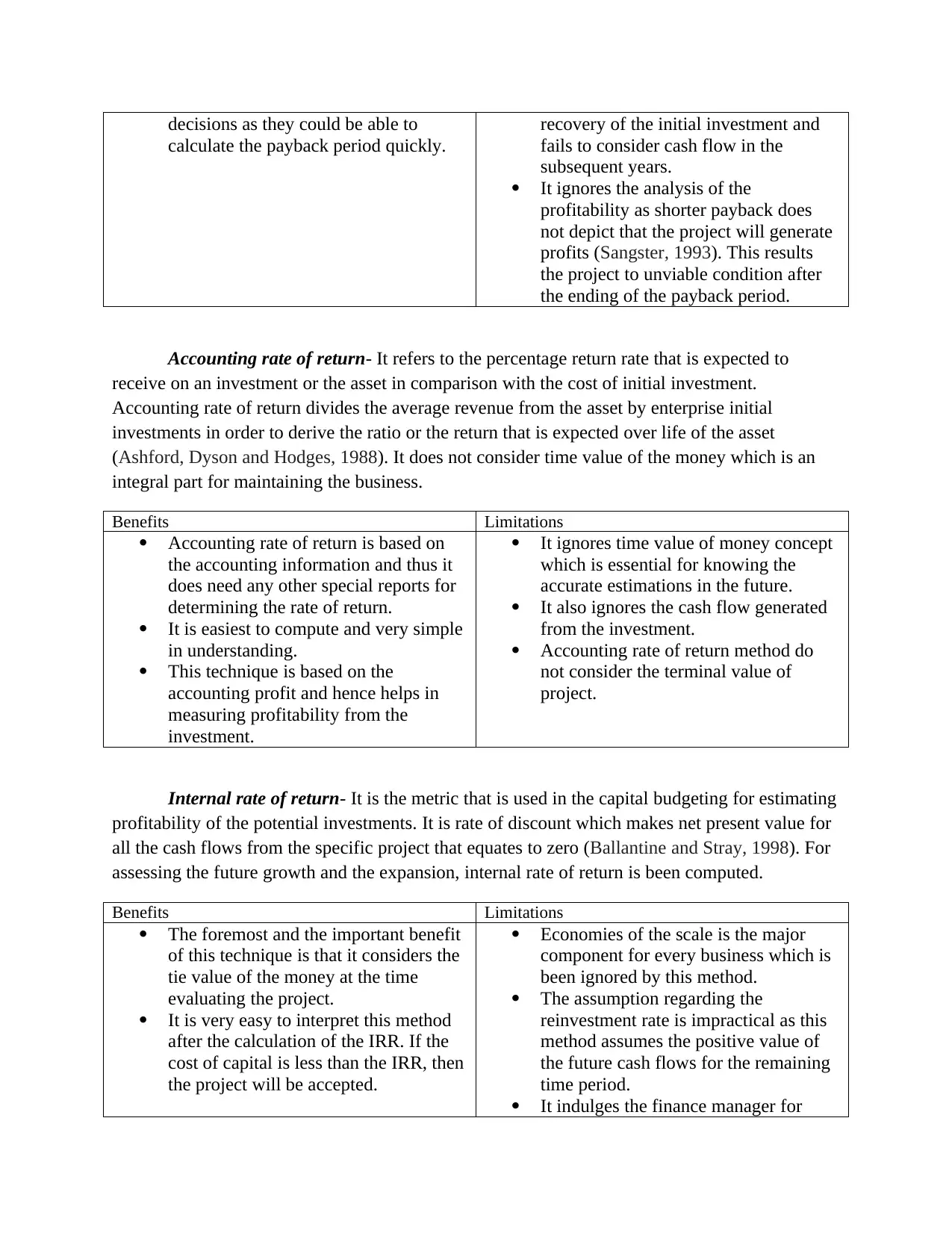

This assignment solution delves into the core concepts of financial management, specifically focusing on capital budgeting techniques. The solution provides detailed calculations and analysis of various methods, including payback period, accounting rate of return, net present value (NPV), and internal rate of return (IRR). The assignment includes the calculation of cash inflows and outflows, depreciation, and earnings before interest and taxes (EBIT). Furthermore, the assignment evaluates the advantages and disadvantages of each capital budgeting technique, providing a comprehensive understanding of their practical applications and limitations. The solution references relevant books and journals to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.