ACCT20080 Case Study: Ethical Analysis of From Bad to Worse Scenario

VerifiedAdded on 2022/09/28

|14

|3992

|18

Case Study

AI Summary

This report presents an analysis of the case study "From Bad to Worse," examining the ethical dilemmas faced by a company's management. The analysis begins by applying ethical theories, including egoism, utilitarianism, and deontological ethics, to the actions of key characters such as Mr. Goodrich and Mr. Arnold. The report then utilizes the AAA ethical decision-making model to evaluate the choices made by Mr. Goodrich. Finally, it explores the application of the APES 110 code of conduct for professional accountants, discussing the relevant principles, potential threats, and necessary safeguards within the context of the case. The report aims to provide a comprehensive understanding of the ethical considerations and decision-making processes involved in the scenario.

Running Head: ETHICS AND GOVERNANCE 0

FROM BAD TO WORSE

FROM BAD TO WORSE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ETHICS AND GOVERNANCE 2

Executive summary

The Report is prepared on the Case Study” From Bad to Worse”. The report is about solving the

case study from an ethical perspective. In the first part of the report the ethical theories such as

deontological and utilitarianism is applied to the behaviors of the characters. In the second part,

the AAA model of ethical decision-making is used and in the last part the APES 110 code of

conduct, which includes principals, threats and safeguards for the professional accountant are

discussed.

Executive summary

The Report is prepared on the Case Study” From Bad to Worse”. The report is about solving the

case study from an ethical perspective. In the first part of the report the ethical theories such as

deontological and utilitarianism is applied to the behaviors of the characters. In the second part,

the AAA model of ethical decision-making is used and in the last part the APES 110 code of

conduct, which includes principals, threats and safeguards for the professional accountant are

discussed.

ETHICS AND GOVERNANCE 3

Contents

Introduction.................................................................................................................................................4

CASE STUDY: FROM BAD TO WORSE.................................................................................................4

Part A: Application of ethical theories....................................................................................................4

Mr. Goodrich’s Behavior according to the theory of Egoism..............................................................4

Mr. Goodrich’s Behavior according to the theory of Utilitarianism....................................................5

Mr. Arnold’s Behavior according to the theory of Utilitarianism........................................................5

Mr. Arnold’s Behavior according to the Deontological theory............................................................6

Part B: AAA Ethical Decision making Model used by Mr. Goodrich....................................................6

Part C: Application of APES 110...........................................................................................................8

Conclusion.................................................................................................................................................10

Bibliography..............................................................................................................................................11

Contents

Introduction.................................................................................................................................................4

CASE STUDY: FROM BAD TO WORSE.................................................................................................4

Part A: Application of ethical theories....................................................................................................4

Mr. Goodrich’s Behavior according to the theory of Egoism..............................................................4

Mr. Goodrich’s Behavior according to the theory of Utilitarianism....................................................5

Mr. Arnold’s Behavior according to the theory of Utilitarianism........................................................5

Mr. Arnold’s Behavior according to the Deontological theory............................................................6

Part B: AAA Ethical Decision making Model used by Mr. Goodrich....................................................6

Part C: Application of APES 110...........................................................................................................8

Conclusion.................................................................................................................................................10

Bibliography..............................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ETHICS AND GOVERNANCE 4

Introduction

A company faces various ethical dilemmas in its workings. These ethical issues arise due

to the lack of knowledge of ethics or the insincerity of the employee for its applications. The

ethical issues, which arise, are inevitable from the organization. The most important thing that

matters is how the management takes the decision when such unethical issues arise. In the case

study, Mr. Goodrich who is the CEO of the company is faced with the dilemma to take the

ethical decision regarding the exploitation of labor union. The following report will be discussing

the application of ethical theories to the case study in its first section and the usage of AAA

model of ethical decision making in the organization in the section B. It also discusses about

APES 110 Code of ethics for professional accountants and its application according to the case-

study in section C.

CASE STUDY: FROM BAD TO WORSE

Part A: Application of ethical theories

Mr. Goodrich’s Behavior according to the theory of Egoism

The theory of egoism is concerned with an individual whose primary motive is

satisfaction of his wants and desires (Gates, 2013). The theory has two aspects, which are

descriptive and normative. The descriptive aspect is concerned with that an individual’ interests

act as a motivating factor for performance and the normative aspect is concerned with that

individuals should stay motivated regardless of what the motivating factors (Overall & Gedeon,

2019). The behavior of Mr. Goodrich was motivated by his great personal ambitions. In the

beginning of the case, it was described that Mr. Goodrich wants to portray himself as a

distinctive personality to the visitors, which was reflective of his self-obsession. According to the

egoism theory, Mr. Goodrich reflected self-obsession in his attitude. When the Amanda and

Arnold communicated to him regarding the 6$ million fines to Fair work Commission for the

Introduction

A company faces various ethical dilemmas in its workings. These ethical issues arise due

to the lack of knowledge of ethics or the insincerity of the employee for its applications. The

ethical issues, which arise, are inevitable from the organization. The most important thing that

matters is how the management takes the decision when such unethical issues arise. In the case

study, Mr. Goodrich who is the CEO of the company is faced with the dilemma to take the

ethical decision regarding the exploitation of labor union. The following report will be discussing

the application of ethical theories to the case study in its first section and the usage of AAA

model of ethical decision making in the organization in the section B. It also discusses about

APES 110 Code of ethics for professional accountants and its application according to the case-

study in section C.

CASE STUDY: FROM BAD TO WORSE

Part A: Application of ethical theories

Mr. Goodrich’s Behavior according to the theory of Egoism

The theory of egoism is concerned with an individual whose primary motive is

satisfaction of his wants and desires (Gates, 2013). The theory has two aspects, which are

descriptive and normative. The descriptive aspect is concerned with that an individual’ interests

act as a motivating factor for performance and the normative aspect is concerned with that

individuals should stay motivated regardless of what the motivating factors (Overall & Gedeon,

2019). The behavior of Mr. Goodrich was motivated by his great personal ambitions. In the

beginning of the case, it was described that Mr. Goodrich wants to portray himself as a

distinctive personality to the visitors, which was reflective of his self-obsession. According to the

egoism theory, Mr. Goodrich reflected self-obsession in his attitude. When the Amanda and

Arnold communicated to him regarding the 6$ million fines to Fair work Commission for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ETHICS AND GOVERNANCE 5

underpayment of the workers. Mr. Goodrich gets furious instead of accepting the company’s

fault. He fired Amanda for researching about the company’s fault and very bluntly asked the

accountant to prepare the full financial report. This is representative of Mr. Goodrich selfish

behavior as he is not concerned about the conditions of the factory workers; his only concern is

the company’s reputation. The selfish behavior is one of the elements of egoism theory. Mr.

Goodrich portrayed the selfish behavior by not concerning to the needs of factory workers and

moreover, when the accountant presented the second option to Mr. Goodrich, he got furious and

asked him to keep it confidential. In the motive of safeguarding, the company’s reputation, he

did not care about the interest of factory workers, which is reflective of the egoism behavior of

the company.

Mr. Goodrich’s Behavior according to the theory of Utilitarianism

Theory of utilitarianism states an action is considered, right or moral when it has the

capability to do good for the large number of populations (Bradt, 2016). Any form of action that

has potential to do the best for the large numbers come under the theory utilitarianism (Mill,

2017). For example, an individual who follows the utilitarianism theory in his life might

introspect whether spending money is good in a meal program organized by the charitable

organization for poor or spending it on election campaign by a political party. In the case study,

the Mr. Goodrich behavior is more on egoism side than on the utilitarianism side as he is less

concerned about the good of the greatest number rather, he is concerned about the company’s

reputation and his reputation as a COO of a company. Looking from the company perspective,

his behavior according to the theory is justified to some extent as he tried saving the interest of

all stakeholders associated with the company but at the same time, he did not consider whether

the action was moral or not. The behavior of Mr. Goodrich did not comply with the theory of

utilitarianism. As saving, the interest of the company was associated to his own good as he had a

motive achieving the profit by hook or crook. As according to the Utilitarianism theory which is

concerned with doing best for the greatest numbers but Mr. Goodrich in the case was concerned

in doing good to himself.

His tough and successful image in the company compelled him to save the company from

any further losses.

underpayment of the workers. Mr. Goodrich gets furious instead of accepting the company’s

fault. He fired Amanda for researching about the company’s fault and very bluntly asked the

accountant to prepare the full financial report. This is representative of Mr. Goodrich selfish

behavior as he is not concerned about the conditions of the factory workers; his only concern is

the company’s reputation. The selfish behavior is one of the elements of egoism theory. Mr.

Goodrich portrayed the selfish behavior by not concerning to the needs of factory workers and

moreover, when the accountant presented the second option to Mr. Goodrich, he got furious and

asked him to keep it confidential. In the motive of safeguarding, the company’s reputation, he

did not care about the interest of factory workers, which is reflective of the egoism behavior of

the company.

Mr. Goodrich’s Behavior according to the theory of Utilitarianism

Theory of utilitarianism states an action is considered, right or moral when it has the

capability to do good for the large number of populations (Bradt, 2016). Any form of action that

has potential to do the best for the large numbers come under the theory utilitarianism (Mill,

2017). For example, an individual who follows the utilitarianism theory in his life might

introspect whether spending money is good in a meal program organized by the charitable

organization for poor or spending it on election campaign by a political party. In the case study,

the Mr. Goodrich behavior is more on egoism side than on the utilitarianism side as he is less

concerned about the good of the greatest number rather, he is concerned about the company’s

reputation and his reputation as a COO of a company. Looking from the company perspective,

his behavior according to the theory is justified to some extent as he tried saving the interest of

all stakeholders associated with the company but at the same time, he did not consider whether

the action was moral or not. The behavior of Mr. Goodrich did not comply with the theory of

utilitarianism. As saving, the interest of the company was associated to his own good as he had a

motive achieving the profit by hook or crook. As according to the Utilitarianism theory which is

concerned with doing best for the greatest numbers but Mr. Goodrich in the case was concerned

in doing good to himself.

His tough and successful image in the company compelled him to save the company from

any further losses.

ETHICS AND GOVERNANCE 6

Mr. Arnold’s Behavior according to the theory of Utilitarianism

MR. Arnold behavior, when analyzed according to the theory of Utilitarianism. It is

reflected that he was concerned about the interest of the union workers as they were underpaid

which is depicted through his fearless in bringing the matter to the Chief operating officer who

was simply concerned about making profits by hook or nook. As according to the Utilitarianism

theory, the main motive is to serve the interest for the larger good, Mr. Arnold ‘s fearless attitude

to save the interest of factory workers. His behavior of discussing the matter with the Mr.

Goodrich depicts his inclination for doing a morally justified action. Mr. Arnold was concerned

about doing well to the greatest number. When Mr. Arnold was asked to present the report by his

boss. The report presented by him reflected his flexible behavior as he mentioned two options

one was ignoring the matter of underpayment of wages and the other was acceptance of the

misconduct by the company to the Fair Commission. Initially, in the case, there was greater

inclination of Mr. Arnold towards the Utilitarianism but later he developed the flexible approach

to it.

Mr. Arnold’s Behavior according to the Deontological theory

The word deontological, derived from the word “Deon” which means duty. The

deontological theory is concerned with doing the right action no matter whether its consequences

are good or not (Chandler, 2019). In the theory, what matters is the intention to do an act is right

for example stealing the loaf of bread to serve a poor child is not a right action (Friedland &

Cole, 2019). The behavior of Mr. Arnold did not adhere to the deontological theory. When Mr.

Goodrich got furious on the issue and asked Mr. Arnold to come up with solution of the problem.

The fearful Mr. Arnold was afraid of losing his job. He did not stand tall on the ethics of saving

the rights of the factory workers. The next day he came up with the report having the two options

in it. The first option stated to ignore the issue completely and the second option stated the

company to accept the fault of underpayment to the Fair communication then conversation can

fix the issue. In a deontological theory, it is important to work according to the set ethical rules

and regulations, Mr. Arnold did not stand with the first ethical and correct option of saving the

factory workers instead he opined the boss to let the matter go. The reflection of the option

Mr. Arnold’s Behavior according to the theory of Utilitarianism

MR. Arnold behavior, when analyzed according to the theory of Utilitarianism. It is

reflected that he was concerned about the interest of the union workers as they were underpaid

which is depicted through his fearless in bringing the matter to the Chief operating officer who

was simply concerned about making profits by hook or nook. As according to the Utilitarianism

theory, the main motive is to serve the interest for the larger good, Mr. Arnold ‘s fearless attitude

to save the interest of factory workers. His behavior of discussing the matter with the Mr.

Goodrich depicts his inclination for doing a morally justified action. Mr. Arnold was concerned

about doing well to the greatest number. When Mr. Arnold was asked to present the report by his

boss. The report presented by him reflected his flexible behavior as he mentioned two options

one was ignoring the matter of underpayment of wages and the other was acceptance of the

misconduct by the company to the Fair Commission. Initially, in the case, there was greater

inclination of Mr. Arnold towards the Utilitarianism but later he developed the flexible approach

to it.

Mr. Arnold’s Behavior according to the Deontological theory

The word deontological, derived from the word “Deon” which means duty. The

deontological theory is concerned with doing the right action no matter whether its consequences

are good or not (Chandler, 2019). In the theory, what matters is the intention to do an act is right

for example stealing the loaf of bread to serve a poor child is not a right action (Friedland &

Cole, 2019). The behavior of Mr. Arnold did not adhere to the deontological theory. When Mr.

Goodrich got furious on the issue and asked Mr. Arnold to come up with solution of the problem.

The fearful Mr. Arnold was afraid of losing his job. He did not stand tall on the ethics of saving

the rights of the factory workers. The next day he came up with the report having the two options

in it. The first option stated to ignore the issue completely and the second option stated the

company to accept the fault of underpayment to the Fair communication then conversation can

fix the issue. In a deontological theory, it is important to work according to the set ethical rules

and regulations, Mr. Arnold did not stand with the first ethical and correct option of saving the

factory workers instead he opined the boss to let the matter go. The reflection of the option

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ETHICS AND GOVERNANCE 7

second in the report made Mr. Goodrich furious and asked Mr. Arnold to delete the report

completely from the computer. Mr. Arnold did not reply and left which shows he was not duty-

bond to protect the interest of the workers thus the behavior of Mr. Arnold did not comply with

deontological theory.

Part B: AAA Ethical Decision- making Model used by Mr. Goodrich

The AAA Ethical Decision-making is a seven-step process of reaching at the best ethical

decision possible. The model application gives the clarity of the decisions to be taken by

recognizing the facts and the issues (Payne, Corey, Raiborn, & Zingoni, 2019). In the case, Mr.

Goodrich now interested in reaching to the ethical decision of the case. The following steps will

be involved in it.

The information of the case-

The account and human resource manager visits the office of the Chief operating officer

of the company to discuss the issue of short payment of wages, leaves and superannuation faced

by the factory workers for the past two years and the unions are pressurizing them to compensate

the amount lost with $6million.

Ethical issues involved-

The ethical issue involved is the company’s black practices of reimbursing its factory

employees with low wages, leave and superannuation. The practice meant violation of the rights

of factory workers. It is the responsibility of the company to take care of the stakeholder’s rights

and to control any form of unjust practices done to them.

The principals and norms in the case-

There are principles and norms in the case. It is the responsibility of the company to take

care of the rights of the people associated with it. The company’s motive is not just earning

profits and gains; it has some duties towards the society to offer as form of corporate social

initiative. Any kind of harm done by the company is unethical and it should try to control its bad

actions with the positive ones.

The course of actions to applied-

second in the report made Mr. Goodrich furious and asked Mr. Arnold to delete the report

completely from the computer. Mr. Arnold did not reply and left which shows he was not duty-

bond to protect the interest of the workers thus the behavior of Mr. Arnold did not comply with

deontological theory.

Part B: AAA Ethical Decision- making Model used by Mr. Goodrich

The AAA Ethical Decision-making is a seven-step process of reaching at the best ethical

decision possible. The model application gives the clarity of the decisions to be taken by

recognizing the facts and the issues (Payne, Corey, Raiborn, & Zingoni, 2019). In the case, Mr.

Goodrich now interested in reaching to the ethical decision of the case. The following steps will

be involved in it.

The information of the case-

The account and human resource manager visits the office of the Chief operating officer

of the company to discuss the issue of short payment of wages, leaves and superannuation faced

by the factory workers for the past two years and the unions are pressurizing them to compensate

the amount lost with $6million.

Ethical issues involved-

The ethical issue involved is the company’s black practices of reimbursing its factory

employees with low wages, leave and superannuation. The practice meant violation of the rights

of factory workers. It is the responsibility of the company to take care of the stakeholder’s rights

and to control any form of unjust practices done to them.

The principals and norms in the case-

There are principles and norms in the case. It is the responsibility of the company to take

care of the rights of the people associated with it. The company’s motive is not just earning

profits and gains; it has some duties towards the society to offer as form of corporate social

initiative. Any kind of harm done by the company is unethical and it should try to control its bad

actions with the positive ones.

The course of actions to applied-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ETHICS AND GOVERNANCE 8

The first action is ignoring the plea of the unions, to protect the image of the company.

The other option is the acceptance of the mistake committed by the company to the fair

commission and asking them some time to pay the compensation amount.

The best course of action-

The best course of action according to the principles and norms is the second alternative.

MR. Goodrich as a COO of the company will accept his company’s mistake of paying short

wages to factory workers to the fair commission. After, acceptance of the mistake, he will ask

them some time to fix the problem, during which time he will arrange money with bank to pay

the specified amount or he could genuinely bargain with them to lower the amount.

Action consequences-

Following the second course of action will have positive consequences as the company

will be able to take care of the interest of the factory workers and at the same time, it will secure

the future of the company. The action taken will also help the company from getting into the

insolvency in the future, as the fair commission will bargain the amount and give them enough

time for its repayment. Overall, it will improve the company’s image. The first option, if chosen

will put the company in trouble as at some time there would be strong opposition from the union

thus hampering the company’s image.

The final decision-

The ethical decision chosen is the second option because this is the best ethical option as

it compensates the unethical actions caused by the company in past.

Part C: Application of APES 110

APES 110 are the ethical professional code of conducts for the professional accountants

of Australia to be followed. It lays down principles, guidelines that are essential for the

accountants to comply with in order to be considered the member of Chartered Accountants

Australia and New Zealand (Yesseleva, 2013). The APES has a list of principles to be followed

by the registered professional accountants. The APES 110 structure is divided into three parts the

first part explains the important principals of professional practice (Gabbitas, 2010). The second

and the third part explain the applications of the practice to the various specific situations. The

The first action is ignoring the plea of the unions, to protect the image of the company.

The other option is the acceptance of the mistake committed by the company to the fair

commission and asking them some time to pay the compensation amount.

The best course of action-

The best course of action according to the principles and norms is the second alternative.

MR. Goodrich as a COO of the company will accept his company’s mistake of paying short

wages to factory workers to the fair commission. After, acceptance of the mistake, he will ask

them some time to fix the problem, during which time he will arrange money with bank to pay

the specified amount or he could genuinely bargain with them to lower the amount.

Action consequences-

Following the second course of action will have positive consequences as the company

will be able to take care of the interest of the factory workers and at the same time, it will secure

the future of the company. The action taken will also help the company from getting into the

insolvency in the future, as the fair commission will bargain the amount and give them enough

time for its repayment. Overall, it will improve the company’s image. The first option, if chosen

will put the company in trouble as at some time there would be strong opposition from the union

thus hampering the company’s image.

The final decision-

The ethical decision chosen is the second option because this is the best ethical option as

it compensates the unethical actions caused by the company in past.

Part C: Application of APES 110

APES 110 are the ethical professional code of conducts for the professional accountants

of Australia to be followed. It lays down principles, guidelines that are essential for the

accountants to comply with in order to be considered the member of Chartered Accountants

Australia and New Zealand (Yesseleva, 2013). The APES has a list of principles to be followed

by the registered professional accountants. The APES 110 structure is divided into three parts the

first part explains the important principals of professional practice (Gabbitas, 2010). The second

and the third part explain the applications of the practice to the various specific situations. The

ETHICS AND GOVERNANCE 9

code has five essential principles which are Integrity, objectivity, professional skill and due care,

confidentiality and professional behavior. The Integrity principal states the professional

accountant to be honest in all the dealings and affairs. It is considered a solid rock foundation on

which the conduct of the accountant is evaluated. According to the code, the practicing

professional accountant must be honest and straightforward in all his dealings. It is concerned

with being truthful and fair in all business relationships. The second principle is of objectivity

where the professional accountants are instructed to never guide their decision based on

emotions, bias or under somebody’s influence. The third principal is of professional skill and due

care where the professional accountant is expected to maintain the skills and knowledge of

profession at all the levels and they are expected to act according to the professional and

technical standards.

The fourth principal is of confidentiality where the professional accountant is expected to

maintain the secrecy of the information provided to them, they are made to keep the information.

Confidential (Farooq & de Villiers, 2019). The last principal is of professional behavior that is

concerned with dealings with clients in respectful manner. It focuses that having professional

knowledge is not enough; one needs to have a proper and respectful conduct with colleagues and

clients. The good professional behavior is required to make the dealings successful (Dellaportas

& Davenport, 2008). In the case, if Mr. Arnold is considered the member of charted accountancy

Australia and New Zealand than it is mandatory for Mr. Arnold to follow all the principles

diligently. The APEC110 is also applicable on Mr. Arnold. The APEC 110 describes the threats

and risks, which are present in professional life of an accountant. These threats are self-interest,

self-review, advocacy, familiarity and Intimidation (Duff, 2016). The first threat is self-interest

where an individual could ignore the interest of the public at large over his own interest in this

case the Mr. Arnold who is an accountant, can be swayed away by the interest by the incentives

provided to him by his boss to not disclose the underpayment of factory staff to anyone.

Intimidation is another threat where an individual can be pressurized by someone in authority to

not to act in a public interest. The intimidation is negative which pressurizes an individual to act

in a certain way (Davenport & Dellaportas, 2009). In the case Mr. Arnold was dominated by his

boss decision to not to disclose the underpayments of staff to anyone otherwise he would be fired

from his job. His boss negatively threatened him. The third type of threat that comes up is the

familiarity threat in this an individual working in a organization develops relationship with the

code has five essential principles which are Integrity, objectivity, professional skill and due care,

confidentiality and professional behavior. The Integrity principal states the professional

accountant to be honest in all the dealings and affairs. It is considered a solid rock foundation on

which the conduct of the accountant is evaluated. According to the code, the practicing

professional accountant must be honest and straightforward in all his dealings. It is concerned

with being truthful and fair in all business relationships. The second principle is of objectivity

where the professional accountants are instructed to never guide their decision based on

emotions, bias or under somebody’s influence. The third principal is of professional skill and due

care where the professional accountant is expected to maintain the skills and knowledge of

profession at all the levels and they are expected to act according to the professional and

technical standards.

The fourth principal is of confidentiality where the professional accountant is expected to

maintain the secrecy of the information provided to them, they are made to keep the information.

Confidential (Farooq & de Villiers, 2019). The last principal is of professional behavior that is

concerned with dealings with clients in respectful manner. It focuses that having professional

knowledge is not enough; one needs to have a proper and respectful conduct with colleagues and

clients. The good professional behavior is required to make the dealings successful (Dellaportas

& Davenport, 2008). In the case, if Mr. Arnold is considered the member of charted accountancy

Australia and New Zealand than it is mandatory for Mr. Arnold to follow all the principles

diligently. The APEC110 is also applicable on Mr. Arnold. The APEC 110 describes the threats

and risks, which are present in professional life of an accountant. These threats are self-interest,

self-review, advocacy, familiarity and Intimidation (Duff, 2016). The first threat is self-interest

where an individual could ignore the interest of the public at large over his own interest in this

case the Mr. Arnold who is an accountant, can be swayed away by the interest by the incentives

provided to him by his boss to not disclose the underpayment of factory staff to anyone.

Intimidation is another threat where an individual can be pressurized by someone in authority to

not to act in a public interest. The intimidation is negative which pressurizes an individual to act

in a certain way (Davenport & Dellaportas, 2009). In the case Mr. Arnold was dominated by his

boss decision to not to disclose the underpayments of staff to anyone otherwise he would be fired

from his job. His boss negatively threatened him. The third type of threat that comes up is the

familiarity threat in this an individual working in a organization develops relationship with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ETHICS AND GOVERNANCE 10

client or boss due to the long term association with the organization. The familiarity hinders the

professional in working justly thus resulting in complete ignorance of the public interest, as the

emotions and connections with the person comes in between (West, 2018) .In case, Mr. Arnold

who worked as an accountant could be sharing a long-term employer and employee relationship

with Mr. Goodrich thus breeding familiarity between the two. The long-term acquaintance might

stop him to act against the company and his boss.

The fourth kind of threat is advocacy threat where the member supports the clients or

employer’s judgment. The member is aware of the unethical act but he becomes a sales person

for employee. He does what the employer tells him to do (Cameron & O'Leary, 2015). In the

case, Mr. Arnold might act as sales person for his boss Mr. Goodrich that means supporting his

judgment of keeping the issue of underpayment, confidential. The fourth threat is self-review

threat, where a member stops evaluating his own work or the work of his colleague. The lack of

evaluation of one’s work could lead to corruption in ones professional code of conduct like in

this case there is greater chance of Mr. Arnold not evaluating his actions according to the

professional code of conduct, which might lead to corrupted actions on his part. In order to

eliminate these threats, there are some safeguard measures provided by the APES 110 (Clayton

& van Staden, 2015). There two options, the first one is application of safeguard until it is

removed and the second is removing it disassociating oneself from the job. There are safeguards

of different levels. The first one is having an appropriate knowledge of the regulatory framework

of the APES110. In the case, Mr. Arnold as a professional accountant and a registered member

of the company has an appropriate knowledge of the code of conducts. He can base his

unwillingness to not disclose the issue by standing tall on the principle of Integrity or by sticking

to his objectivity. Another level of safeguard is the working environment of the company with

the help of a policy or procedures; one can use it for beneficial in the case, if the company has a

special cell for union rights then the member can directly report the matter there (Perera &

Chand, 2015). The last level of safeguard is the personal level, which involves the strong sense

of judgment of what is right or wrong. Mr. Arnold can fearlessly deny the boss request of not

disclosing the matter. After, the application of all safeguard levels, nothing works than Mr.

Arnold can disassociate with the organization.

client or boss due to the long term association with the organization. The familiarity hinders the

professional in working justly thus resulting in complete ignorance of the public interest, as the

emotions and connections with the person comes in between (West, 2018) .In case, Mr. Arnold

who worked as an accountant could be sharing a long-term employer and employee relationship

with Mr. Goodrich thus breeding familiarity between the two. The long-term acquaintance might

stop him to act against the company and his boss.

The fourth kind of threat is advocacy threat where the member supports the clients or

employer’s judgment. The member is aware of the unethical act but he becomes a sales person

for employee. He does what the employer tells him to do (Cameron & O'Leary, 2015). In the

case, Mr. Arnold might act as sales person for his boss Mr. Goodrich that means supporting his

judgment of keeping the issue of underpayment, confidential. The fourth threat is self-review

threat, where a member stops evaluating his own work or the work of his colleague. The lack of

evaluation of one’s work could lead to corruption in ones professional code of conduct like in

this case there is greater chance of Mr. Arnold not evaluating his actions according to the

professional code of conduct, which might lead to corrupted actions on his part. In order to

eliminate these threats, there are some safeguard measures provided by the APES 110 (Clayton

& van Staden, 2015). There two options, the first one is application of safeguard until it is

removed and the second is removing it disassociating oneself from the job. There are safeguards

of different levels. The first one is having an appropriate knowledge of the regulatory framework

of the APES110. In the case, Mr. Arnold as a professional accountant and a registered member

of the company has an appropriate knowledge of the code of conducts. He can base his

unwillingness to not disclose the issue by standing tall on the principle of Integrity or by sticking

to his objectivity. Another level of safeguard is the working environment of the company with

the help of a policy or procedures; one can use it for beneficial in the case, if the company has a

special cell for union rights then the member can directly report the matter there (Perera &

Chand, 2015). The last level of safeguard is the personal level, which involves the strong sense

of judgment of what is right or wrong. Mr. Arnold can fearlessly deny the boss request of not

disclosing the matter. After, the application of all safeguard levels, nothing works than Mr.

Arnold can disassociate with the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ETHICS AND GOVERNANCE 11

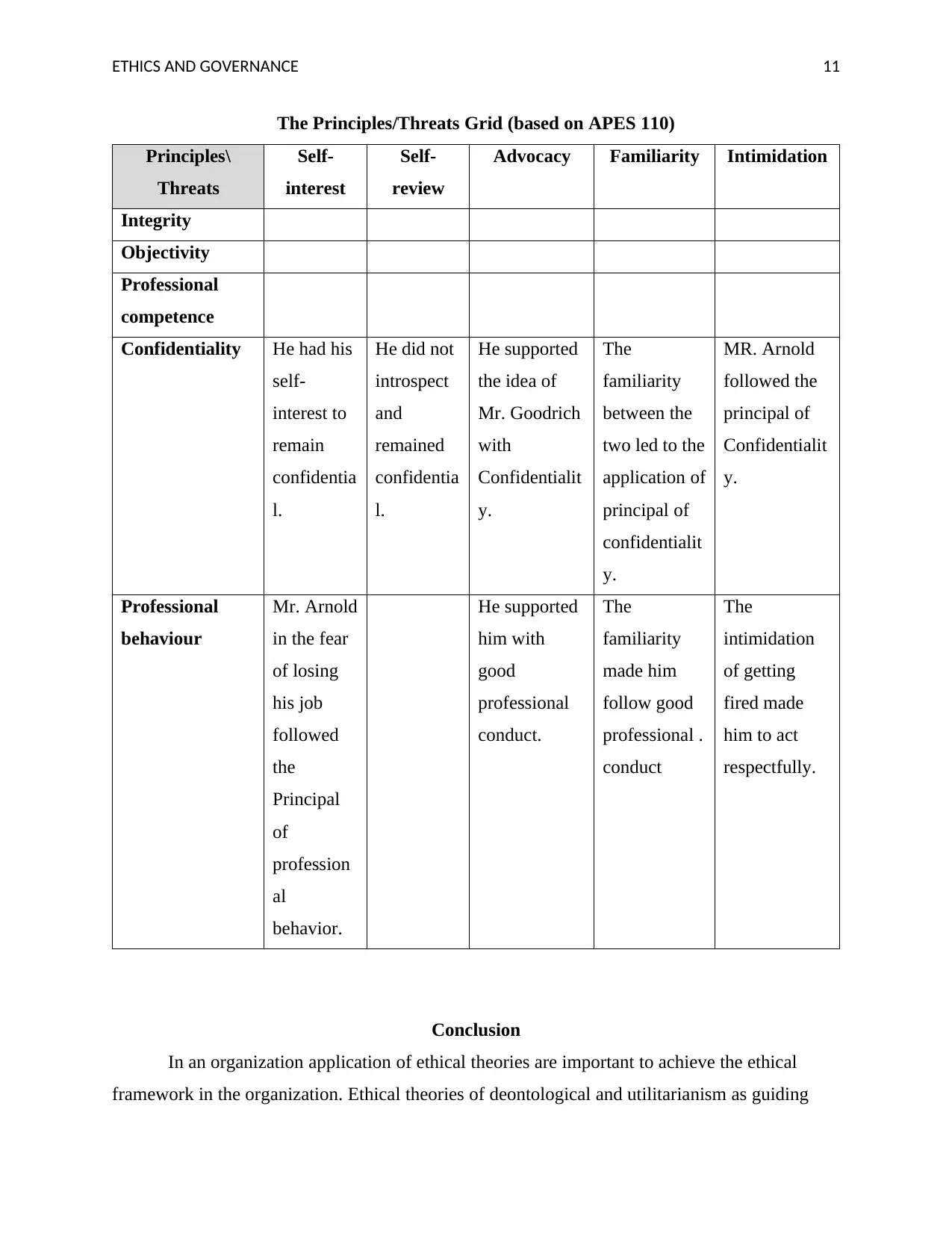

The Principles/Threats Grid (based on APES 110)

Principles\

Threats

Self-

interest

Self-

review

Advocacy Familiarity Intimidation

Integrity

Objectivity

Professional

competence

Confidentiality He had his

self-

interest to

remain

confidentia

l.

He did not

introspect

and

remained

confidentia

l.

He supported

the idea of

Mr. Goodrich

with

Confidentialit

y.

The

familiarity

between the

two led to the

application of

principal of

confidentialit

y.

MR. Arnold

followed the

principal of

Confidentialit

y.

Professional

behaviour

Mr. Arnold

in the fear

of losing

his job

followed

the

Principal

of

profession

al

behavior.

He supported

him with

good

professional

conduct.

The

familiarity

made him

follow good

professional .

conduct

The

intimidation

of getting

fired made

him to act

respectfully.

Conclusion

In an organization application of ethical theories are important to achieve the ethical

framework in the organization. Ethical theories of deontological and utilitarianism as guiding

The Principles/Threats Grid (based on APES 110)

Principles\

Threats

Self-

interest

Self-

review

Advocacy Familiarity Intimidation

Integrity

Objectivity

Professional

competence

Confidentiality He had his

self-

interest to

remain

confidentia

l.

He did not

introspect

and

remained

confidentia

l.

He supported

the idea of

Mr. Goodrich

with

Confidentialit

y.

The

familiarity

between the

two led to the

application of

principal of

confidentialit

y.

MR. Arnold

followed the

principal of

Confidentialit

y.

Professional

behaviour

Mr. Arnold

in the fear

of losing

his job

followed

the

Principal

of

profession

al

behavior.

He supported

him with

good

professional

conduct.

The

familiarity

made him

follow good

professional .

conduct

The

intimidation

of getting

fired made

him to act

respectfully.

Conclusion

In an organization application of ethical theories are important to achieve the ethical

framework in the organization. Ethical theories of deontological and utilitarianism as guiding

ETHICS AND GOVERNANCE 12

principal for an organization to follow if employees of the organization are trained on these

theories then unethical issues can be avoided. The AAA model of ethical decision-making is

helpful in arriving at a right decision. The auditors and accountants who are the registered

members of APES110 should follow the professional code of conduct diligently to avoid any

kind of unethical conduct in the organization.

principal for an organization to follow if employees of the organization are trained on these

theories then unethical issues can be avoided. The AAA model of ethical decision-making is

helpful in arriving at a right decision. The auditors and accountants who are the registered

members of APES110 should follow the professional code of conduct diligently to avoid any

kind of unethical conduct in the organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.