API Audit: Financial Ratio Analysis and Internal Control Review

VerifiedAdded on 2023/03/17

|21

|4270

|45

Report

AI Summary

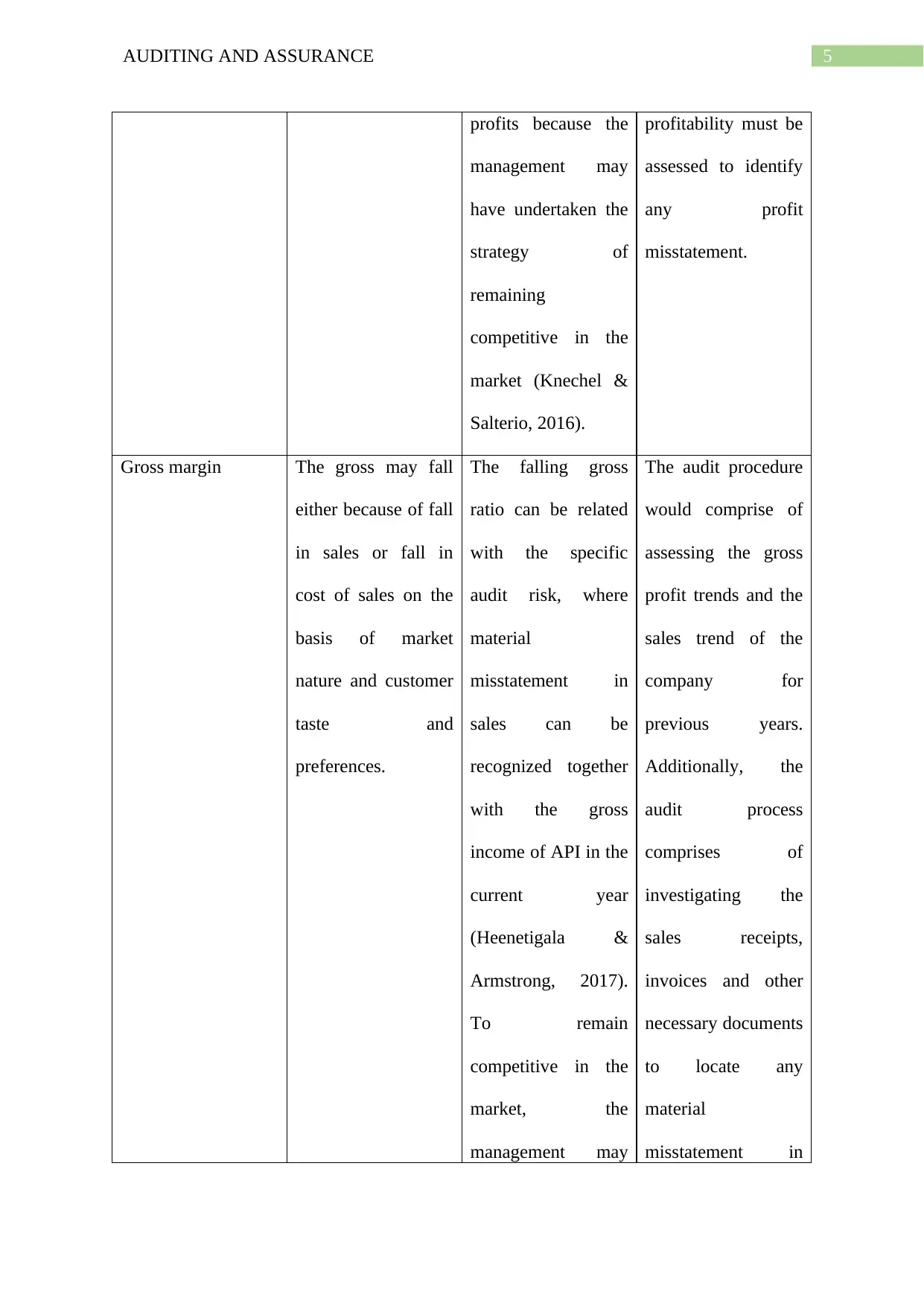

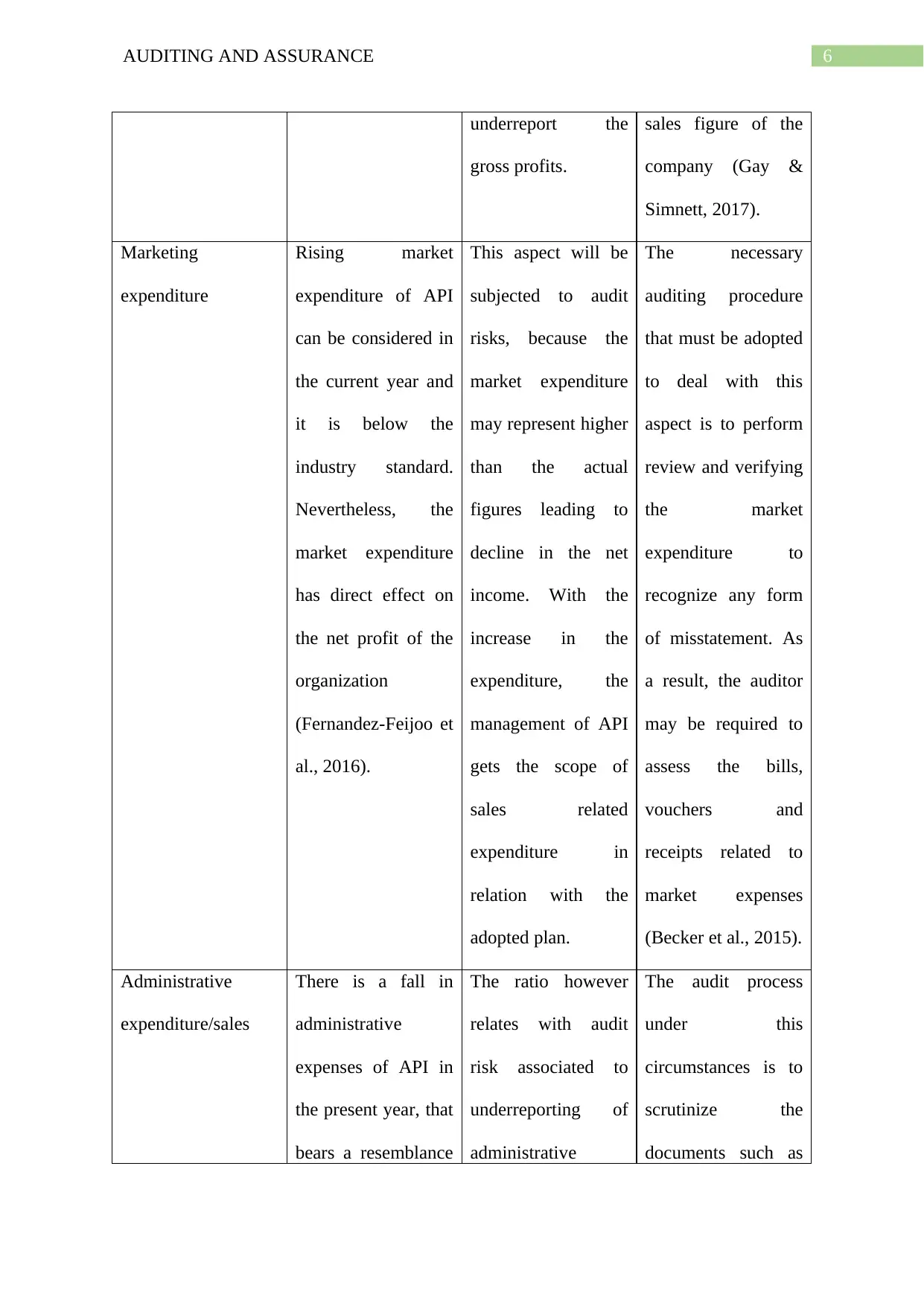

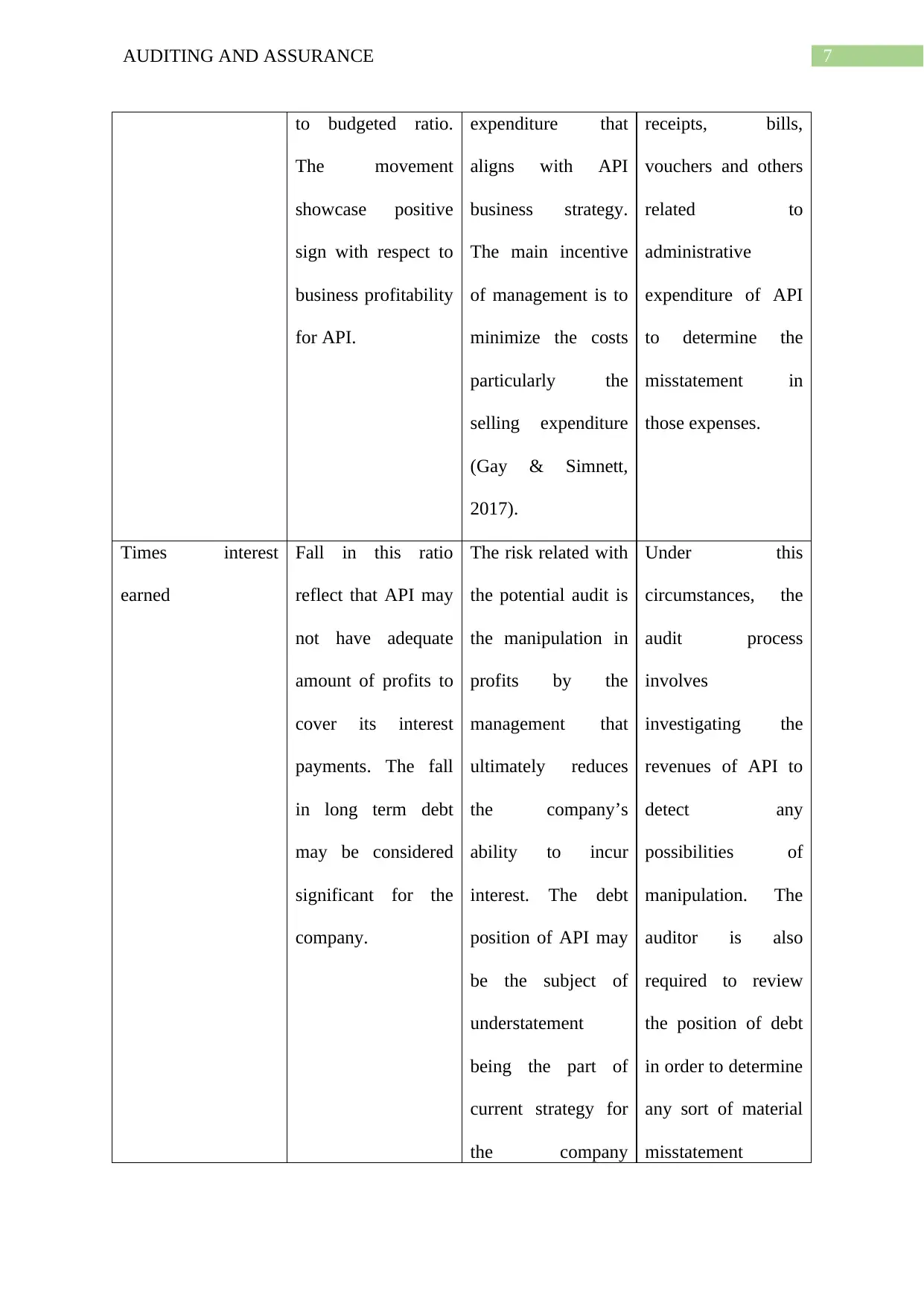

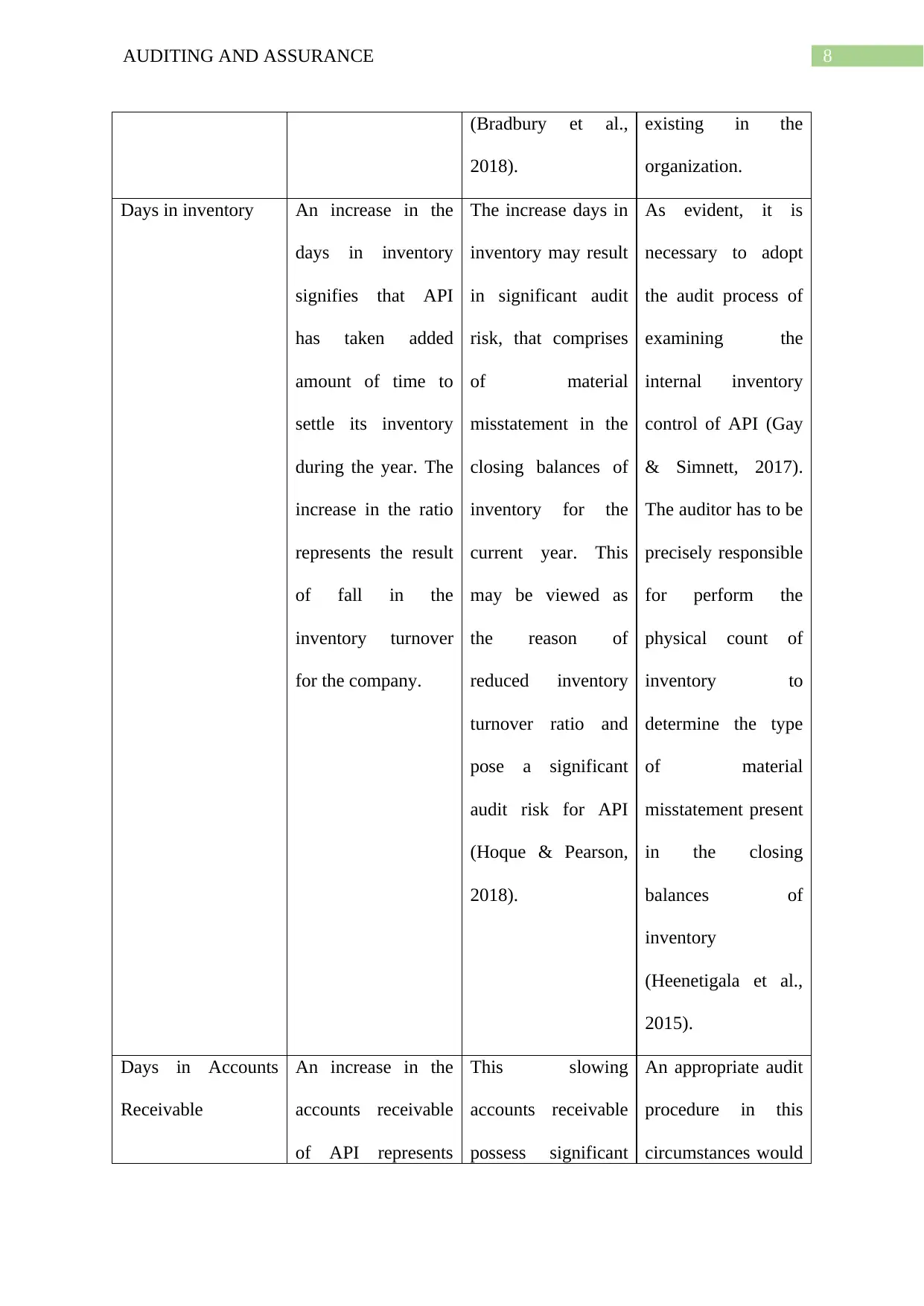

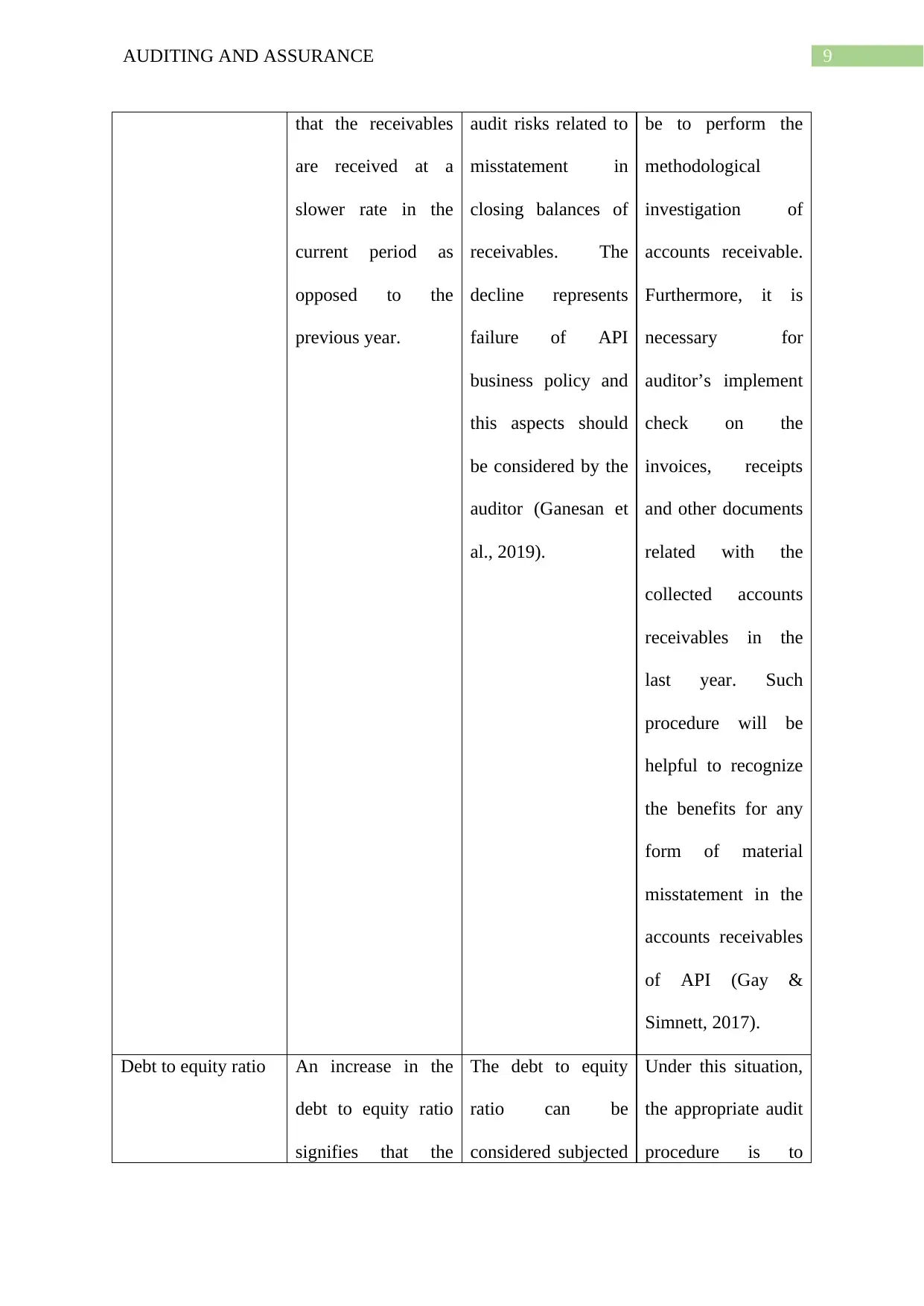

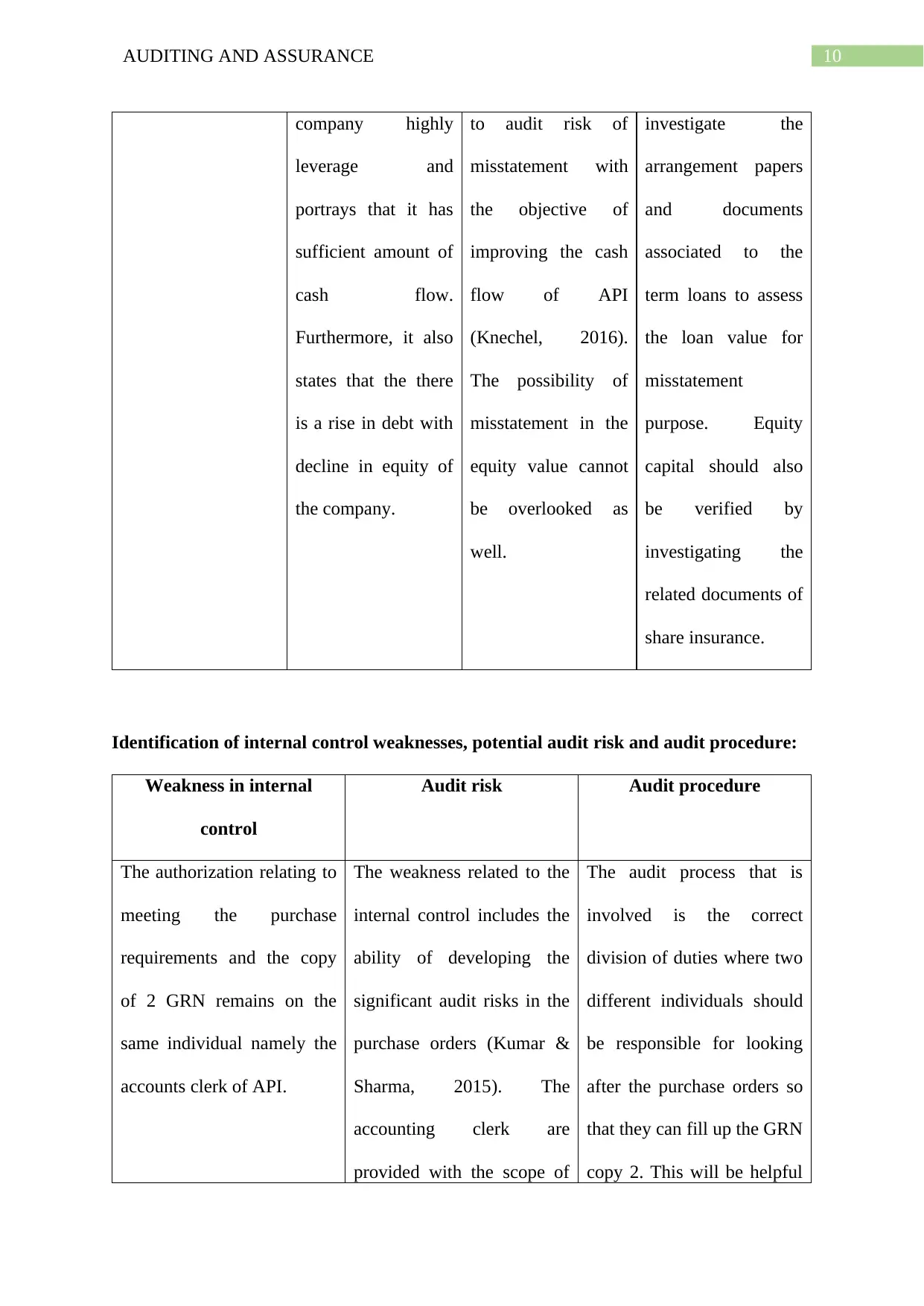

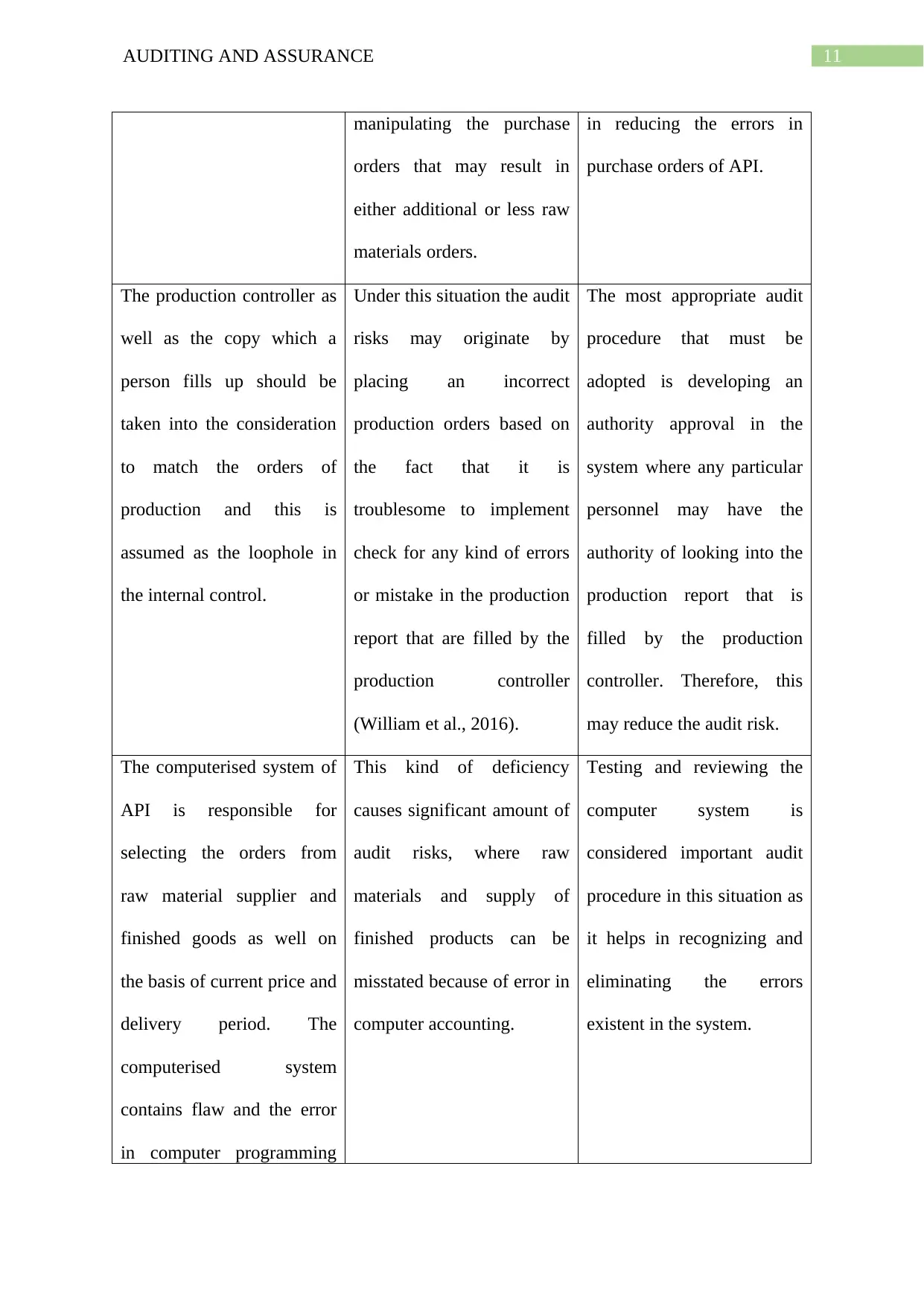

This report presents an audit analysis of Always Precise Instrument Private Limited (API), a manufacturer and supplier of small military equipment. It identifies potential audit risks by performing financial ratio analysis, highlighting concerns such as increased current ratio, quick asset ratio fluctuations, declining return on equity and assets, and gross margin variations. The report also assesses weaknesses in API's internal control system, particularly within the inventory system, including authorization issues and potential manipulation of purchase orders and production orders. Furthermore, the document outlines appropriate audit procedures and sampling processes for key audit assertions, emphasizing the need for thorough examination of inventory balances, accounts receivable, and debt-to-equity ratios. The report concludes by recommending improvements to internal controls and suggesting specific audit measures to minimize identified risks, ensuring a more accurate and reliable financial reporting process. Desklib provides students access to similar past papers and solved assignments for academic assistance.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.