Case Study: Auditing and Assurance of API (ACC568) Audit Memo

VerifiedAdded on 2023/03/17

|19

|4421

|24

Case Study

AI Summary

This case study presents an audit memo analyzing the financial statements of Always Precise Instruments Private Limited (API), a supplier of military equipment. The memo, written from the perspective of an audit manager, addresses key aspects of the audit, including ratio analysis to identify potential audit risks, such as those related to current and quick ratios, return on equity, and gross margin. It also identifies internal control weaknesses within API's inventory system, outlining potential audit risks and proposing appropriate audit procedures. Furthermore, the memo examines specific audit assertions and recommends suitable sampling procedures, providing justifications for each. The analysis covers various financial ratios, including current ratio, quick asset ratio, return on equity, return on total assets, gross margin, marketing expense, administrative expenses, times earned interest, days in inventory, days in accounts receivable, and debt to equity ratio. For each ratio, the memo identifies potential audit risks and suggests corresponding audit procedures. The memo also details internal control weaknesses, potential audit risks, and suggested audit procedures related to authorization of purchase orders and production orders. This case study provides a comprehensive overview of the auditing process and helps in understanding the various aspects of an audit.

Running head: AUDITING AND ASSURANCE IN AUSTRALIA

Auditing and Assurance in Australia

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing and Assurance in Australia

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE IN AUSTRALIA

Table of Contents

Potential audit risks and procedures for minimising those risks:...............................................2

Identification of internal control weaknesses, potential audit risk and audit procedure:...........9

Sampling methods:...................................................................................................................13

References:...............................................................................................................................16

Table of Contents

Potential audit risks and procedures for minimising those risks:...............................................2

Identification of internal control weaknesses, potential audit risk and audit procedure:...........9

Sampling methods:...................................................................................................................13

References:...............................................................................................................................16

2AUDITING AND ASSURANCE IN AUSTRALIA

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 09/05/2019

Subject: Significant aspects under consideration for conducting the audit of API

In order to carry out audit operations, the auditors are required to take into account all

the crucial aspects, which are deemed to be necessary. These mainly include critical analysis

of different line items in the disclosed financial statements of an organisation and the internal

control systems in place. The memo is prepared for addressing those areas having concern in

internal control and financial statements of Always Precise Instruments Private Limited

(API). The organisation is a supplier and producer of small arms military equipment. There

are three particular aspects that have been addressed in this memo. Firstly, evaluation of the

provided ratios is made for detecting the potential risks in order to outline sound auditing

procedures. Secondly, the weaknesses in internal control of API are identified for the

inventory system in order to find out the potential audit risks and accordingly, appropriate

audit procedures could be developed. Finally, it considers the analysis of two particular audit

assertions as well as suitable sampling procedures by providing adequate justifications for the

same.

Potential audit risks and procedures for minimising those risks:

Ratio Analysis Audit Risk Audit Procedures

Current ratio It could be seen that

API has experienced an

increase in this ratio,

This rise in current

ratio is subject to audit

risk, as the current

In this case, the necessary audit

procedure would be to

investigate the liquidity position

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 09/05/2019

Subject: Significant aspects under consideration for conducting the audit of API

In order to carry out audit operations, the auditors are required to take into account all

the crucial aspects, which are deemed to be necessary. These mainly include critical analysis

of different line items in the disclosed financial statements of an organisation and the internal

control systems in place. The memo is prepared for addressing those areas having concern in

internal control and financial statements of Always Precise Instruments Private Limited

(API). The organisation is a supplier and producer of small arms military equipment. There

are three particular aspects that have been addressed in this memo. Firstly, evaluation of the

provided ratios is made for detecting the potential risks in order to outline sound auditing

procedures. Secondly, the weaknesses in internal control of API are identified for the

inventory system in order to find out the potential audit risks and accordingly, appropriate

audit procedures could be developed. Finally, it considers the analysis of two particular audit

assertions as well as suitable sampling procedures by providing adequate justifications for the

same.

Potential audit risks and procedures for minimising those risks:

Ratio Analysis Audit Risk Audit Procedures

Current ratio It could be seen that

API has experienced an

increase in this ratio,

This rise in current

ratio is subject to audit

risk, as the current

In this case, the necessary audit

procedure would be to

investigate the liquidity position

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE IN AUSTRALIA

which signifies the

increase in current

assets in opposition to

current liabilities. This

is deemed to be

favourable in terms of

working capital for the

organisation (Abbott et

al., 2016).

assets of API might be

overstated for

showing better

working capital

management to the

users of the financial

reports. The motive of

the management of

API in conducting the

same might be to

show increased

working capital and

minimised short-term

debt position.

of the organisation by

scrutinising the balances of

current assets as well as current

liabilities.

Quick asset ratio Increase in this ratio

denotes quick

conversion of most

liquid assets into cash

so that short-term debt

obligations could be

managed effectively.

This implies

improvement in the

liquidity position of the

organisation, as it has

The aspect is deemed

to have association

with specific audit

risk, in which the

present status of API

has been misstated by

converting them into

quick assets resulting

in increase in this

ratio.

The auditor, in this case, has to

analyse and check the current

assets, which are converted into

most liquid assets recently. In

addition, the quick assets’

balances have to be checked

alongside the essential

documents for identification of

any type of misstatements.

which signifies the

increase in current

assets in opposition to

current liabilities. This

is deemed to be

favourable in terms of

working capital for the

organisation (Abbott et

al., 2016).

assets of API might be

overstated for

showing better

working capital

management to the

users of the financial

reports. The motive of

the management of

API in conducting the

same might be to

show increased

working capital and

minimised short-term

debt position.

of the organisation by

scrutinising the balances of

current assets as well as current

liabilities.

Quick asset ratio Increase in this ratio

denotes quick

conversion of most

liquid assets into cash

so that short-term debt

obligations could be

managed effectively.

This implies

improvement in the

liquidity position of the

organisation, as it has

The aspect is deemed

to have association

with specific audit

risk, in which the

present status of API

has been misstated by

converting them into

quick assets resulting

in increase in this

ratio.

The auditor, in this case, has to

analyse and check the current

assets, which are converted into

most liquid assets recently. In

addition, the quick assets’

balances have to be checked

alongside the essential

documents for identification of

any type of misstatements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE IN AUSTRALIA

more cash in the form of

working capital for

meeting its short-term

dues. This might place

the status of going

concern at risk for API,

as the ratio is lower

compared to the

industrial benchmark

(Ahmed Haji &

Anifowose, 2016).

Return on equity The fall in this ratio

indicates decline in

shareholder value in

API and increase in debt

at the same time

(Bédard et al., 2016).

The situation could be

associated with audit

risk, in which there

could be

understatement of net

profit to avoid tax

liability and increase

in debt capital to

minimise the weighted

average cost of

capital.

The audit procedure to be

undertaken in this case includes

thorough analysis of all line

items in the income statement

and debt obligations of the

organisation for finding out any

misstatement in net income in

the existing period. s

Return on total

assets

Even though fall in this

ratio is not favourable

for API, it signifies

This situation is

subject to audit risk

owing to the

All crucial documents have to

be checked, which include the

asset balances and line items in

more cash in the form of

working capital for

meeting its short-term

dues. This might place

the status of going

concern at risk for API,

as the ratio is lower

compared to the

industrial benchmark

(Ahmed Haji &

Anifowose, 2016).

Return on equity The fall in this ratio

indicates decline in

shareholder value in

API and increase in debt

at the same time

(Bédard et al., 2016).

The situation could be

associated with audit

risk, in which there

could be

understatement of net

profit to avoid tax

liability and increase

in debt capital to

minimise the weighted

average cost of

capital.

The audit procedure to be

undertaken in this case includes

thorough analysis of all line

items in the income statement

and debt obligations of the

organisation for finding out any

misstatement in net income in

the existing period. s

Return on total

assets

Even though fall in this

ratio is not favourable

for API, it signifies

This situation is

subject to audit risk

owing to the

All crucial documents have to

be checked, which include the

asset balances and line items in

5AUDITING AND ASSURANCE IN AUSTRALIA

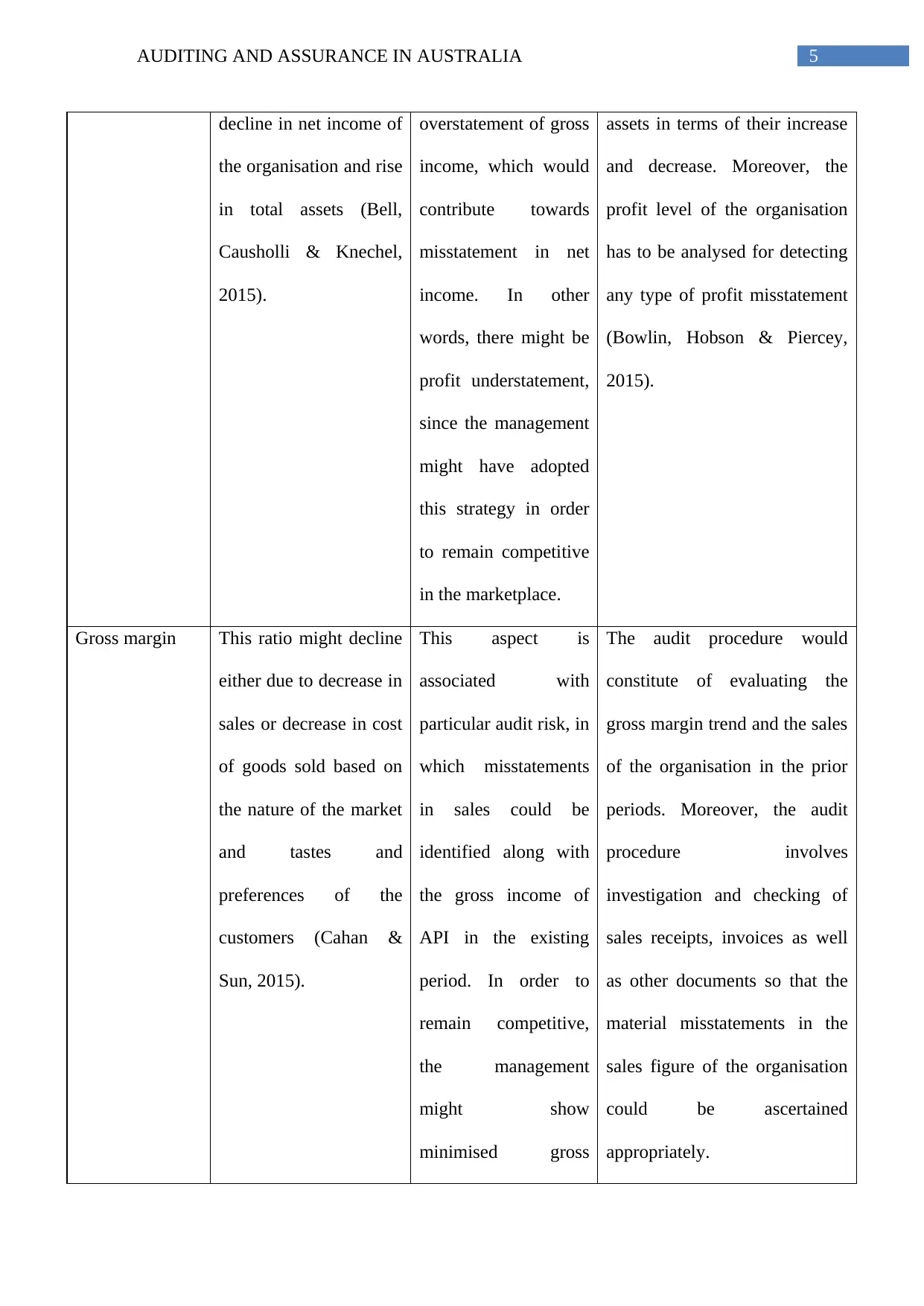

decline in net income of

the organisation and rise

in total assets (Bell,

Causholli & Knechel,

2015).

overstatement of gross

income, which would

contribute towards

misstatement in net

income. In other

words, there might be

profit understatement,

since the management

might have adopted

this strategy in order

to remain competitive

in the marketplace.

assets in terms of their increase

and decrease. Moreover, the

profit level of the organisation

has to be analysed for detecting

any type of profit misstatement

(Bowlin, Hobson & Piercey,

2015).

Gross margin This ratio might decline

either due to decrease in

sales or decrease in cost

of goods sold based on

the nature of the market

and tastes and

preferences of the

customers (Cahan &

Sun, 2015).

This aspect is

associated with

particular audit risk, in

which misstatements

in sales could be

identified along with

the gross income of

API in the existing

period. In order to

remain competitive,

the management

might show

minimised gross

The audit procedure would

constitute of evaluating the

gross margin trend and the sales

of the organisation in the prior

periods. Moreover, the audit

procedure involves

investigation and checking of

sales receipts, invoices as well

as other documents so that the

material misstatements in the

sales figure of the organisation

could be ascertained

appropriately.

decline in net income of

the organisation and rise

in total assets (Bell,

Causholli & Knechel,

2015).

overstatement of gross

income, which would

contribute towards

misstatement in net

income. In other

words, there might be

profit understatement,

since the management

might have adopted

this strategy in order

to remain competitive

in the marketplace.

assets in terms of their increase

and decrease. Moreover, the

profit level of the organisation

has to be analysed for detecting

any type of profit misstatement

(Bowlin, Hobson & Piercey,

2015).

Gross margin This ratio might decline

either due to decrease in

sales or decrease in cost

of goods sold based on

the nature of the market

and tastes and

preferences of the

customers (Cahan &

Sun, 2015).

This aspect is

associated with

particular audit risk, in

which misstatements

in sales could be

identified along with

the gross income of

API in the existing

period. In order to

remain competitive,

the management

might show

minimised gross

The audit procedure would

constitute of evaluating the

gross margin trend and the sales

of the organisation in the prior

periods. Moreover, the audit

procedure involves

investigation and checking of

sales receipts, invoices as well

as other documents so that the

material misstatements in the

sales figure of the organisation

could be ascertained

appropriately.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE IN AUSTRALIA

income.

Marketing

expense

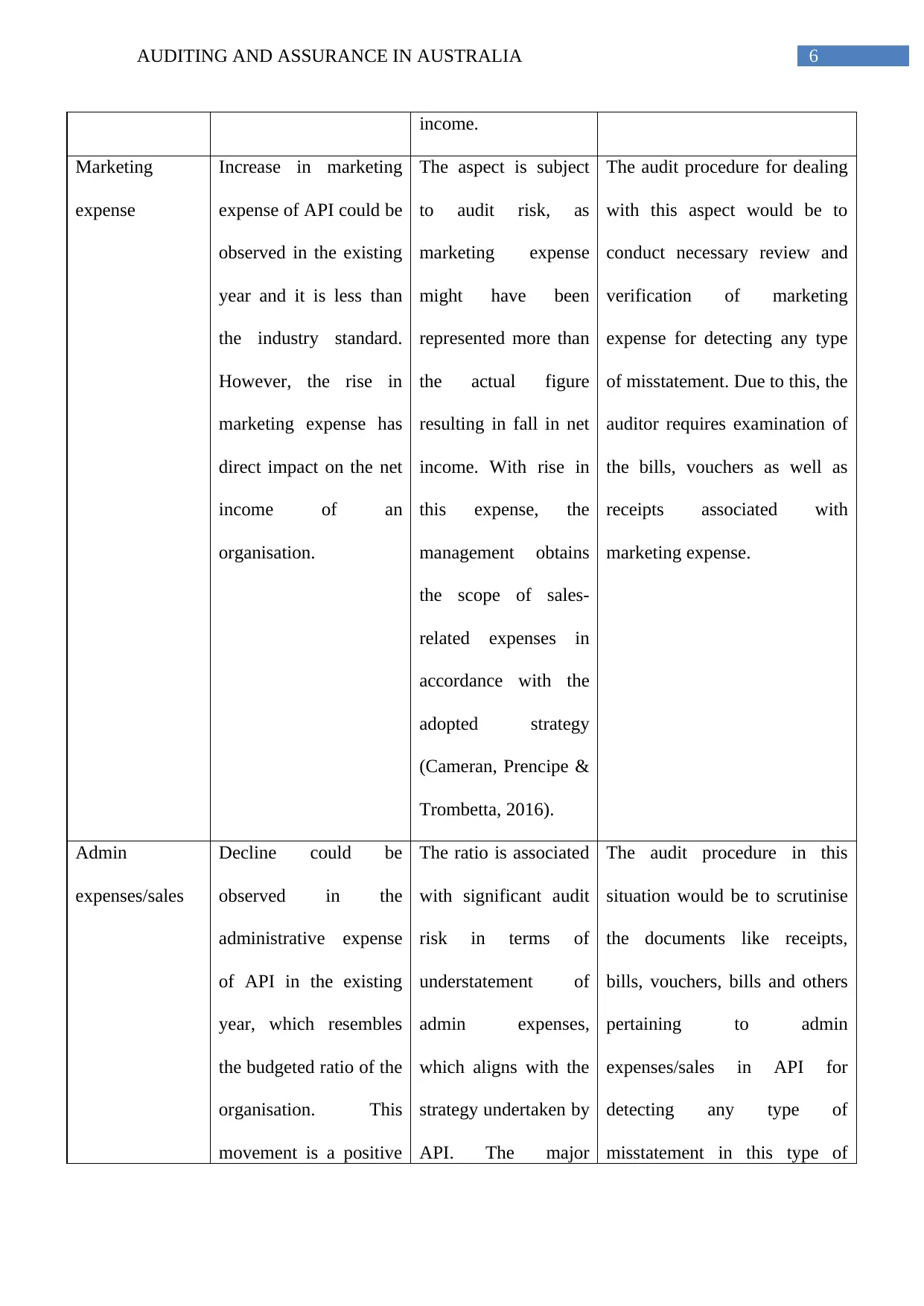

Increase in marketing

expense of API could be

observed in the existing

year and it is less than

the industry standard.

However, the rise in

marketing expense has

direct impact on the net

income of an

organisation.

The aspect is subject

to audit risk, as

marketing expense

might have been

represented more than

the actual figure

resulting in fall in net

income. With rise in

this expense, the

management obtains

the scope of sales-

related expenses in

accordance with the

adopted strategy

(Cameran, Prencipe &

Trombetta, 2016).

The audit procedure for dealing

with this aspect would be to

conduct necessary review and

verification of marketing

expense for detecting any type

of misstatement. Due to this, the

auditor requires examination of

the bills, vouchers as well as

receipts associated with

marketing expense.

Admin

expenses/sales

Decline could be

observed in the

administrative expense

of API in the existing

year, which resembles

the budgeted ratio of the

organisation. This

movement is a positive

The ratio is associated

with significant audit

risk in terms of

understatement of

admin expenses,

which aligns with the

strategy undertaken by

API. The major

The audit procedure in this

situation would be to scrutinise

the documents like receipts,

bills, vouchers, bills and others

pertaining to admin

expenses/sales in API for

detecting any type of

misstatement in this type of

income.

Marketing

expense

Increase in marketing

expense of API could be

observed in the existing

year and it is less than

the industry standard.

However, the rise in

marketing expense has

direct impact on the net

income of an

organisation.

The aspect is subject

to audit risk, as

marketing expense

might have been

represented more than

the actual figure

resulting in fall in net

income. With rise in

this expense, the

management obtains

the scope of sales-

related expenses in

accordance with the

adopted strategy

(Cameran, Prencipe &

Trombetta, 2016).

The audit procedure for dealing

with this aspect would be to

conduct necessary review and

verification of marketing

expense for detecting any type

of misstatement. Due to this, the

auditor requires examination of

the bills, vouchers as well as

receipts associated with

marketing expense.

Admin

expenses/sales

Decline could be

observed in the

administrative expense

of API in the existing

year, which resembles

the budgeted ratio of the

organisation. This

movement is a positive

The ratio is associated

with significant audit

risk in terms of

understatement of

admin expenses,

which aligns with the

strategy undertaken by

API. The major

The audit procedure in this

situation would be to scrutinise

the documents like receipts,

bills, vouchers, bills and others

pertaining to admin

expenses/sales in API for

detecting any type of

misstatement in this type of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE IN AUSTRALIA

sign in terms of

business profitability for

API.

incentive behind the

management of the

organisation might be

the strategy of cost

minimisation,

particularly selling

expenses (Campa and

Donnelly 2016).

expense in the organisation.

Times interest

earned

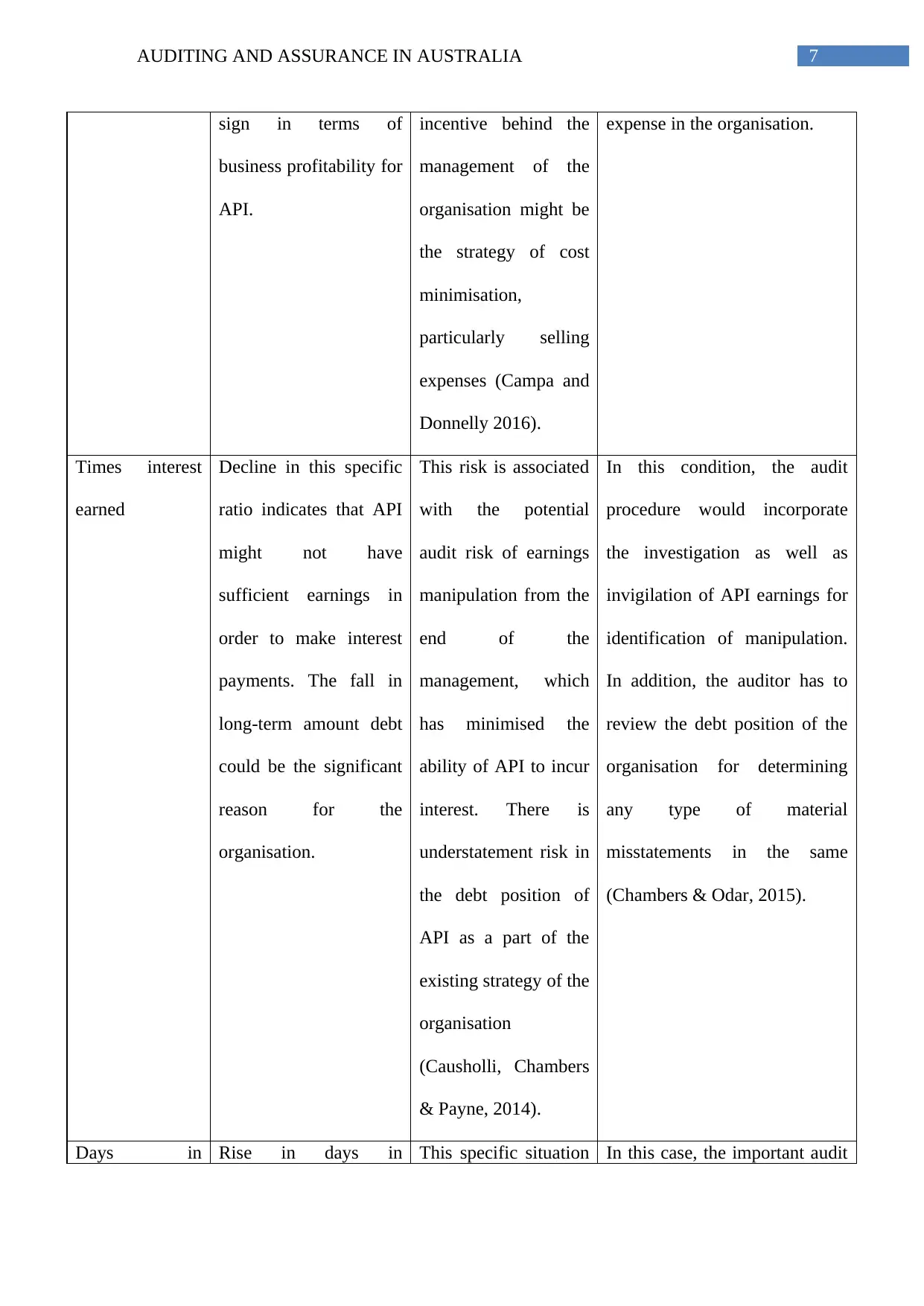

Decline in this specific

ratio indicates that API

might not have

sufficient earnings in

order to make interest

payments. The fall in

long-term amount debt

could be the significant

reason for the

organisation.

This risk is associated

with the potential

audit risk of earnings

manipulation from the

end of the

management, which

has minimised the

ability of API to incur

interest. There is

understatement risk in

the debt position of

API as a part of the

existing strategy of the

organisation

(Causholli, Chambers

& Payne, 2014).

In this condition, the audit

procedure would incorporate

the investigation as well as

invigilation of API earnings for

identification of manipulation.

In addition, the auditor has to

review the debt position of the

organisation for determining

any type of material

misstatements in the same

(Chambers & Odar, 2015).

Days in Rise in days in This specific situation In this case, the important audit

sign in terms of

business profitability for

API.

incentive behind the

management of the

organisation might be

the strategy of cost

minimisation,

particularly selling

expenses (Campa and

Donnelly 2016).

expense in the organisation.

Times interest

earned

Decline in this specific

ratio indicates that API

might not have

sufficient earnings in

order to make interest

payments. The fall in

long-term amount debt

could be the significant

reason for the

organisation.

This risk is associated

with the potential

audit risk of earnings

manipulation from the

end of the

management, which

has minimised the

ability of API to incur

interest. There is

understatement risk in

the debt position of

API as a part of the

existing strategy of the

organisation

(Causholli, Chambers

& Payne, 2014).

In this condition, the audit

procedure would incorporate

the investigation as well as

invigilation of API earnings for

identification of manipulation.

In addition, the auditor has to

review the debt position of the

organisation for determining

any type of material

misstatements in the same

(Chambers & Odar, 2015).

Days in Rise in days in This specific situation In this case, the important audit

8AUDITING AND ASSURANCE IN AUSTRALIA

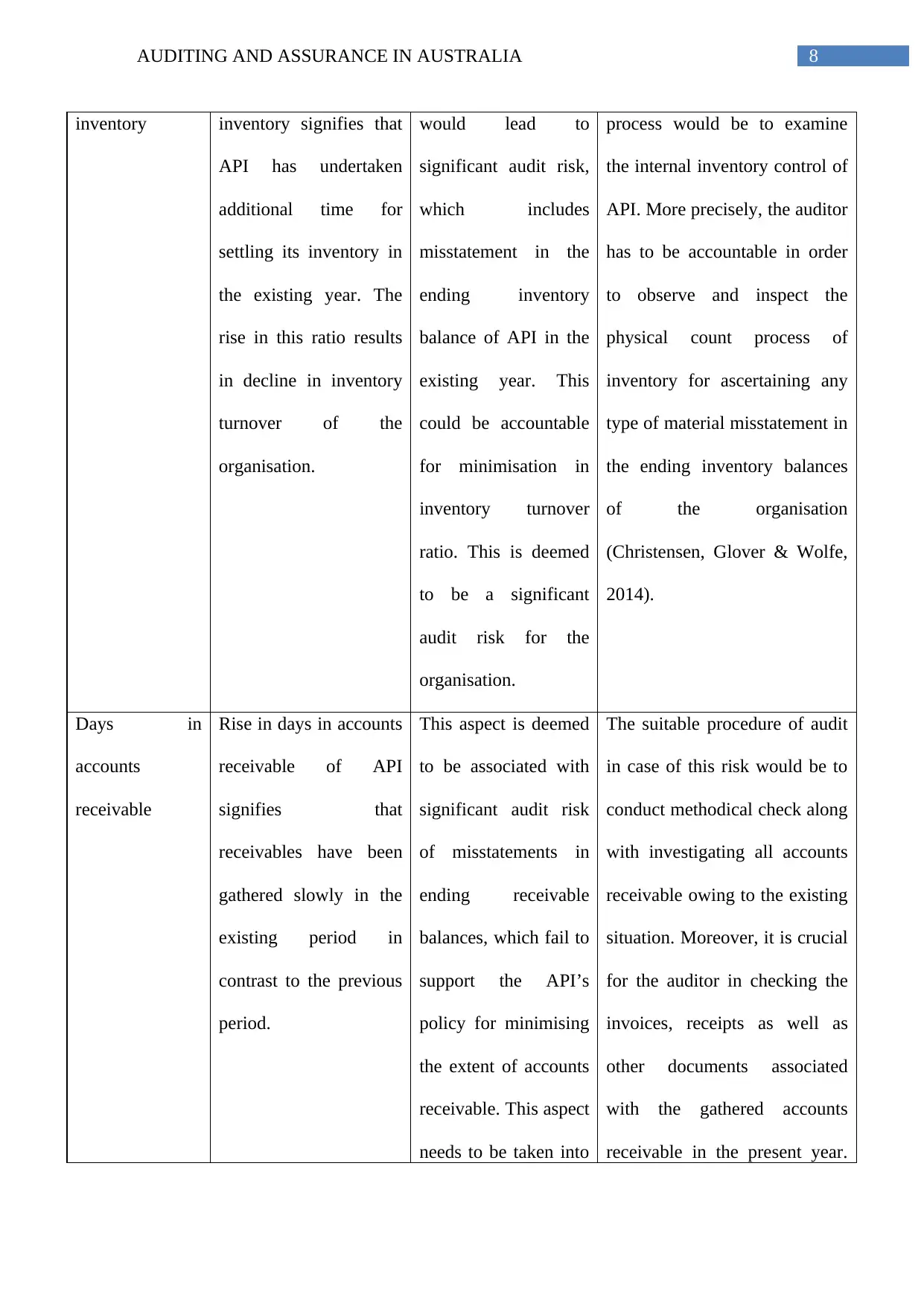

inventory inventory signifies that

API has undertaken

additional time for

settling its inventory in

the existing year. The

rise in this ratio results

in decline in inventory

turnover of the

organisation.

would lead to

significant audit risk,

which includes

misstatement in the

ending inventory

balance of API in the

existing year. This

could be accountable

for minimisation in

inventory turnover

ratio. This is deemed

to be a significant

audit risk for the

organisation.

process would be to examine

the internal inventory control of

API. More precisely, the auditor

has to be accountable in order

to observe and inspect the

physical count process of

inventory for ascertaining any

type of material misstatement in

the ending inventory balances

of the organisation

(Christensen, Glover & Wolfe,

2014).

Days in

accounts

receivable

Rise in days in accounts

receivable of API

signifies that

receivables have been

gathered slowly in the

existing period in

contrast to the previous

period.

This aspect is deemed

to be associated with

significant audit risk

of misstatements in

ending receivable

balances, which fail to

support the API’s

policy for minimising

the extent of accounts

receivable. This aspect

needs to be taken into

The suitable procedure of audit

in case of this risk would be to

conduct methodical check along

with investigating all accounts

receivable owing to the existing

situation. Moreover, it is crucial

for the auditor in checking the

invoices, receipts as well as

other documents associated

with the gathered accounts

receivable in the present year.

inventory inventory signifies that

API has undertaken

additional time for

settling its inventory in

the existing year. The

rise in this ratio results

in decline in inventory

turnover of the

organisation.

would lead to

significant audit risk,

which includes

misstatement in the

ending inventory

balance of API in the

existing year. This

could be accountable

for minimisation in

inventory turnover

ratio. This is deemed

to be a significant

audit risk for the

organisation.

process would be to examine

the internal inventory control of

API. More precisely, the auditor

has to be accountable in order

to observe and inspect the

physical count process of

inventory for ascertaining any

type of material misstatement in

the ending inventory balances

of the organisation

(Christensen, Glover & Wolfe,

2014).

Days in

accounts

receivable

Rise in days in accounts

receivable of API

signifies that

receivables have been

gathered slowly in the

existing period in

contrast to the previous

period.

This aspect is deemed

to be associated with

significant audit risk

of misstatements in

ending receivable

balances, which fail to

support the API’s

policy for minimising

the extent of accounts

receivable. This aspect

needs to be taken into

The suitable procedure of audit

in case of this risk would be to

conduct methodical check along

with investigating all accounts

receivable owing to the existing

situation. Moreover, it is crucial

for the auditor in checking the

invoices, receipts as well as

other documents associated

with the gathered accounts

receivable in the present year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE IN AUSTRALIA

account by the auditor

of API.

Such processes would be

beneficial to identify any sort of

material misstatement in

accounts receivable of the

organisation (Christensen et al.,

2016).

Debt to equity

ratio

Rise in debt to equity

ratio denotes that the

organisation is highly

leveraged and it is a

sound indicator for

stable cash flow of the

organisation. Along

with this, it signifies rise

in debt and fall in equity

of the organisation.

The rise in this ratio is

subject to audit risk of

misstatement in debt

balances with the

intent to improve the

cash flow of the

business. Moreover,

the likelihood of

misstatement in the

value of equity could

not be ignored in this

condition.

In this situation, the suitable

audit process is to investigate

the agreement papers and

documents pertaining to term

loans for determining the loan

amount misstatement.

Moreover, the equity capital

value has to be verified by

investigating the associated

documents of share issuance

(Gay & Simnett, 2017).

Identification of internal control weaknesses, potential audit risk and audit procedure:

Internal control weakness Audit risk Audit procedure

The authorisation for meeting

the purchase orders as well as

the Copy 2 of GRN lies on

This weakness in internal

control possesses the

capability of developing

The audit procedure involves

appropriate division of

duties. This denotes that two

account by the auditor

of API.

Such processes would be

beneficial to identify any sort of

material misstatement in

accounts receivable of the

organisation (Christensen et al.,

2016).

Debt to equity

ratio

Rise in debt to equity

ratio denotes that the

organisation is highly

leveraged and it is a

sound indicator for

stable cash flow of the

organisation. Along

with this, it signifies rise

in debt and fall in equity

of the organisation.

The rise in this ratio is

subject to audit risk of

misstatement in debt

balances with the

intent to improve the

cash flow of the

business. Moreover,

the likelihood of

misstatement in the

value of equity could

not be ignored in this

condition.

In this situation, the suitable

audit process is to investigate

the agreement papers and

documents pertaining to term

loans for determining the loan

amount misstatement.

Moreover, the equity capital

value has to be verified by

investigating the associated

documents of share issuance

(Gay & Simnett, 2017).

Identification of internal control weaknesses, potential audit risk and audit procedure:

Internal control weakness Audit risk Audit procedure

The authorisation for meeting

the purchase orders as well as

the Copy 2 of GRN lies on

This weakness in internal

control possesses the

capability of developing

The audit procedure involves

appropriate division of

duties. This denotes that two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE IN AUSTRALIA

the same individual, which is

the accounts clerk of API.

significant audit risk in

purchase orders. It provides

scope to the accounts clerk in

order to manipulate purchase

orders, which could result in

additional or less raw

material orders (Gaynor et

al., 2016).

different individuals have to

be accountable to look after

the purchase orders in order

to fill the GRN Copy 2. This

would assist in minimisation

of purchase order

misstatement of the

organisation.

The production controller

copy that the individual fills

is taken into account for

matching the orders of

production and this is

deemed to be a loophole in

internal control.

In this situation, audit risk

could arise from placing

incorrect orders of

production in presence of the

fact that it is troublesome to

check any error or mistake in

the production report filled

from the end of the

production controller.

The accurate audit procedure

would be to develop an

authority approval in the

system where any particular

personnel would have the

authorisation of looking into

the production report that the

production controller has

filed. This would result in

lowering audit risk (Goodwin

& Wu, 2016).

The API computerised

system is accountable in

order to select the raw

material suppliers as well as

finished goods based on the

current price and time of

This deficiency results in

significant audit risk, in

which raw material and

finished product supply could

be misstated owing to the

errors in computer program

Testing and reviewing the

computer system is the

crucial audit procedure in

this case in order to identify

and eliminate any type of

errors in the system.

the same individual, which is

the accounts clerk of API.

significant audit risk in

purchase orders. It provides

scope to the accounts clerk in

order to manipulate purchase

orders, which could result in

additional or less raw

material orders (Gaynor et

al., 2016).

different individuals have to

be accountable to look after

the purchase orders in order

to fill the GRN Copy 2. This

would assist in minimisation

of purchase order

misstatement of the

organisation.

The production controller

copy that the individual fills

is taken into account for

matching the orders of

production and this is

deemed to be a loophole in

internal control.

In this situation, audit risk

could arise from placing

incorrect orders of

production in presence of the

fact that it is troublesome to

check any error or mistake in

the production report filled

from the end of the

production controller.

The accurate audit procedure

would be to develop an

authority approval in the

system where any particular

personnel would have the

authorisation of looking into

the production report that the

production controller has

filed. This would result in

lowering audit risk (Goodwin

& Wu, 2016).

The API computerised

system is accountable in

order to select the raw

material suppliers as well as

finished goods based on the

current price and time of

This deficiency results in

significant audit risk, in

which raw material and

finished product supply could

be misstated owing to the

errors in computer program

Testing and reviewing the

computer system is the

crucial audit procedure in

this case in order to identify

and eliminate any type of

errors in the system.

11AUDITING AND ASSURANCE IN AUSTRALIA

delivery. The entire

computerised system could

be viewed as a weakness, as

computer programming

errors could influence the

entire process.

(Johnstone, Li & Luo, 2014).

The API accounts clerk

obtains the password access

of the amendment in master

file. Therefore, by using the

password, it becomes

possible for the individual to

undertake amendments in the

master file. This is identified

as a significant deficiency in

the system of internal

control.

The weakness in internal

control could result in

potential audit risk, in which

the accounts clerk might

make undesired

modifications in the master

file in certain areas of the

current stock items as well as

sub-contractors and approved

suppliers.

The appropriate division of

duty is the needed audit for

minimising this risk. This

step would engage in

providing access of password

of the master file to any

individual not having the

authority of accessing

transactions like raw

materials, purchase orders,

finished products and others

(Johnstone, Li & Luo, 2014).

The sub-contractors and

suppliers that are listed in the

master file are allowed to

receive orders.

This results in critical audit

risk, in which the staffs

would have access to the

master file along with other

transactions and they could

modify the sub-contractors

and suppliers wrongly, which

The appropriate division of

duties is the significant audit

procedure in this situation, in

which the staffs with access

to the master file would not

be entitled to any other

access associated with the

delivery. The entire

computerised system could

be viewed as a weakness, as

computer programming

errors could influence the

entire process.

(Johnstone, Li & Luo, 2014).

The API accounts clerk

obtains the password access

of the amendment in master

file. Therefore, by using the

password, it becomes

possible for the individual to

undertake amendments in the

master file. This is identified

as a significant deficiency in

the system of internal

control.

The weakness in internal

control could result in

potential audit risk, in which

the accounts clerk might

make undesired

modifications in the master

file in certain areas of the

current stock items as well as

sub-contractors and approved

suppliers.

The appropriate division of

duty is the needed audit for

minimising this risk. This

step would engage in

providing access of password

of the master file to any

individual not having the

authority of accessing

transactions like raw

materials, purchase orders,

finished products and others

(Johnstone, Li & Luo, 2014).

The sub-contractors and

suppliers that are listed in the

master file are allowed to

receive orders.

This results in critical audit

risk, in which the staffs

would have access to the

master file along with other

transactions and they could

modify the sub-contractors

and suppliers wrongly, which

The appropriate division of

duties is the significant audit

procedure in this situation, in

which the staffs with access

to the master file would not

be entitled to any other

access associated with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.