Analysis of APN Outdoor Group's Capital Structure and Financials

VerifiedAdded on 2020/04/01

|13

|2112

|116

Report

AI Summary

This finance report provides a comprehensive analysis of APN Outdoor Group's capital structure based on its 2016 annual report. The report examines the company's debt-equity ratio, weighted average cost of capital (WACC), and financial performance, including profitability and return on equity (ROE). It uses ratio analysis and trend analysis to assess the company's financial health and compares it to a competitor, oOh!media Limited. The analysis covers the impact of changes in capital structure, the importance of minimizing the cost of capital, and how the company aims for wealth maximization for its shareholders. The report concludes with key findings and recommendations for the company's financial strategy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 16 Spetember 2017.

1 | P a g e

By student name

Professor

University

Date: 16 Spetember 2017.

1 | P a g e

2

Contents

Executive Summary…..……………………..........……………………………..……………………...3

Introduction……………………………………..........……………………………..……………………...4

Analysis and calculations..………………..........……………………………..……………………...5

Conclusion…..…………………………………..........……………………………..……………………...11

Refrences.....……………………………………………………………….......................................12

2 | P a g e

Contents

Executive Summary…..……………………..........……………………………..……………………...3

Introduction……………………………………..........……………………………..……………………...4

Analysis and calculations..………………..........……………………………..……………………...5

Conclusion…..…………………………………..........……………………………..……………………...11

Refrences.....……………………………………………………………….......................................12

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Executive Summary

In the given report, we are going to analyse the company APN Outdoor Group on the basis of the annual

report for the year ended 2016 and being a part of the finance team of APN group, it becomes chief

responsibility for reviewing and preparing a report on the same. In the give assignment, a report on the

capital structure of the company is to be prepared and to coe out with the view that whether the

company is generating wealth for the shareholders and is involved in the wealth maximisation. The

analysis would be done based on the various analystical procedures including the ratio analysis and

trend analysis for the past few years. Moreover, it has to be compared with the another company of the

same industry to comment upon the firm’s capital structure and the composition of the same. This will

also include the in depth analysis on the cost of capital and how it can be minimised in the long run to

increase th eefficieny of the firm and to increase the profitability as well as th wealth for the company.

In addition to all this, it will include the alternative capital structure that can be implemented in the firm

so as to lower the cost of weighted average cost of capital.

3 | P a g e

Executive Summary

In the given report, we are going to analyse the company APN Outdoor Group on the basis of the annual

report for the year ended 2016 and being a part of the finance team of APN group, it becomes chief

responsibility for reviewing and preparing a report on the same. In the give assignment, a report on the

capital structure of the company is to be prepared and to coe out with the view that whether the

company is generating wealth for the shareholders and is involved in the wealth maximisation. The

analysis would be done based on the various analystical procedures including the ratio analysis and

trend analysis for the past few years. Moreover, it has to be compared with the another company of the

same industry to comment upon the firm’s capital structure and the composition of the same. This will

also include the in depth analysis on the cost of capital and how it can be minimised in the long run to

increase th eefficieny of the firm and to increase the profitability as well as th wealth for the company.

In addition to all this, it will include the alternative capital structure that can be implemented in the firm

so as to lower the cost of weighted average cost of capital.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

APN Outdoor group is one of the pioneer companies in operating in Australia. It is dealing in

advertisement services including putting up of digital billboards, billboards found on the roadside, rail

advertisement, advertisement on airport, etc. throughout the boundaries of Australia and New Zealand.

It also provides online media services in both the countries. It was founded in 2004 and is

headquartered in Pyrmont, Australia. This is also listed on the Australian Stock Exchange. This has been

one of the fast growing advertising company in Australia with the average growth rates over the last 5

years being 26.08% in terms of revenue, 791.49% in terms of net profit and 44.14% in terms of the Gross

Profit. The cash flows have also increased positively at the rate of 192.92% over the past 5 years and

capital spending has increased at the rate of 172.355 implying higher growth in terms of the business for

the company. From the financials of the company, it is evident that the net income has increased from

negative $ 10 Mn in 2014 to around $ 50 Mn in 2016. (Boccia & Leonardi, 2016)

4 | P a g e

Introduction

APN Outdoor group is one of the pioneer companies in operating in Australia. It is dealing in

advertisement services including putting up of digital billboards, billboards found on the roadside, rail

advertisement, advertisement on airport, etc. throughout the boundaries of Australia and New Zealand.

It also provides online media services in both the countries. It was founded in 2004 and is

headquartered in Pyrmont, Australia. This is also listed on the Australian Stock Exchange. This has been

one of the fast growing advertising company in Australia with the average growth rates over the last 5

years being 26.08% in terms of revenue, 791.49% in terms of net profit and 44.14% in terms of the Gross

Profit. The cash flows have also increased positively at the rate of 192.92% over the past 5 years and

capital spending has increased at the rate of 172.355 implying higher growth in terms of the business for

the company. From the financials of the company, it is evident that the net income has increased from

negative $ 10 Mn in 2014 to around $ 50 Mn in 2016. (Boccia & Leonardi, 2016)

4 | P a g e

5

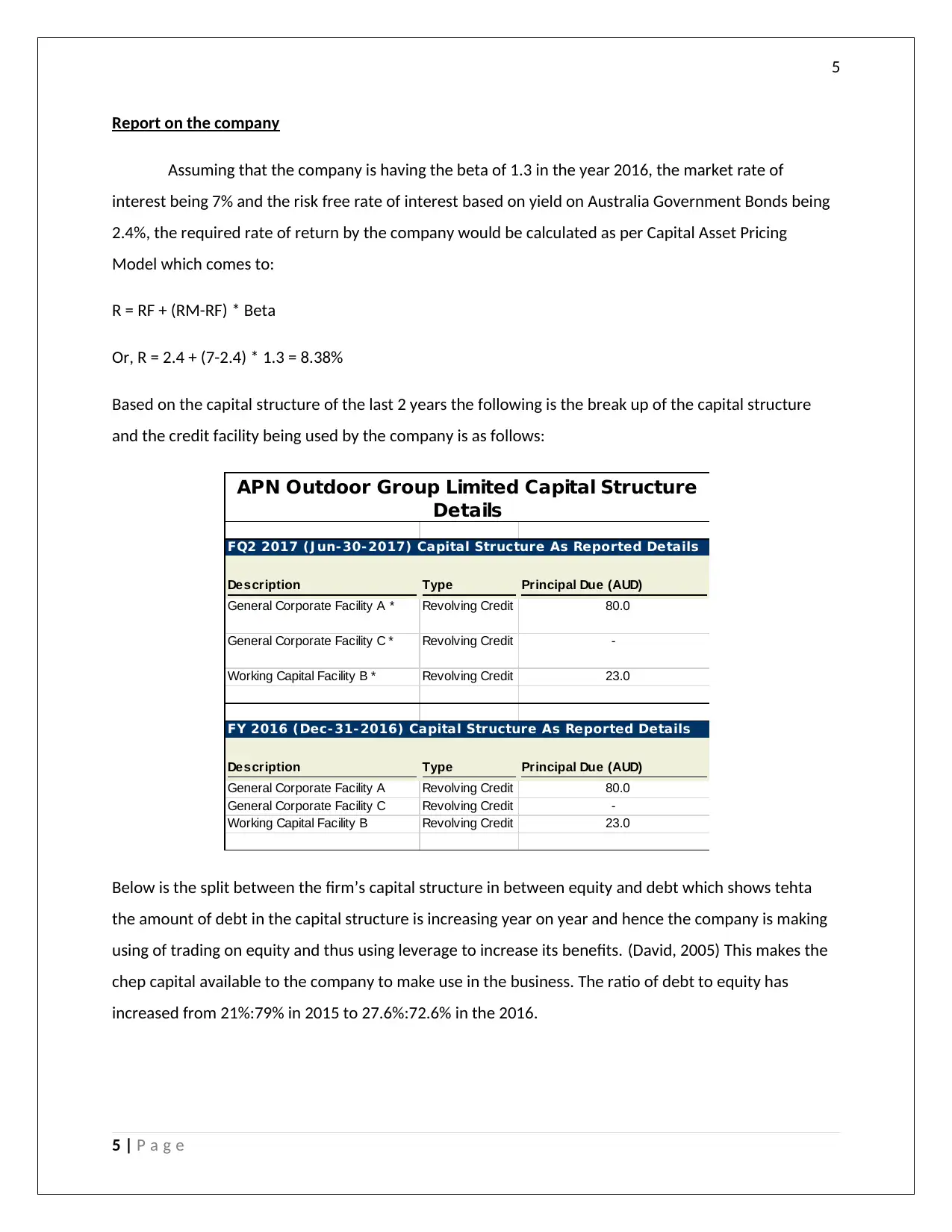

Report on the company

Assuming that the company is having the beta of 1.3 in the year 2016, the market rate of

interest being 7% and the risk free rate of interest based on yield on Australia Government Bonds being

2.4%, the required rate of return by the company would be calculated as per Capital Asset Pricing

Model which comes to:

R = RF + (RM-RF) * Beta

Or, R = 2.4 + (7-2.4) * 1.3 = 8.38%

Based on the capital structure of the last 2 years the following is the break up of the capital structure

and the credit facility being used by the company is as follows:

FQ2 2017 (J un- 30- 2017) Capital Structure As Reported Details

Description Type Principal Due (AUD)

General Corporate Facility A * Revolving Credit 80.0

General Corporate Facility C * Revolving Credit -

Working Capital Facility B * Revolving Credit 23.0

FY 2016 (Dec- 31- 2016) Capital Structure As Reported Details

Description Type Principal Due (AUD)

General Corporate Facility A Revolving Credit 80.0

General Corporate Facility C Revolving Credit -

Working Capital Facility B Revolving Credit 23.0

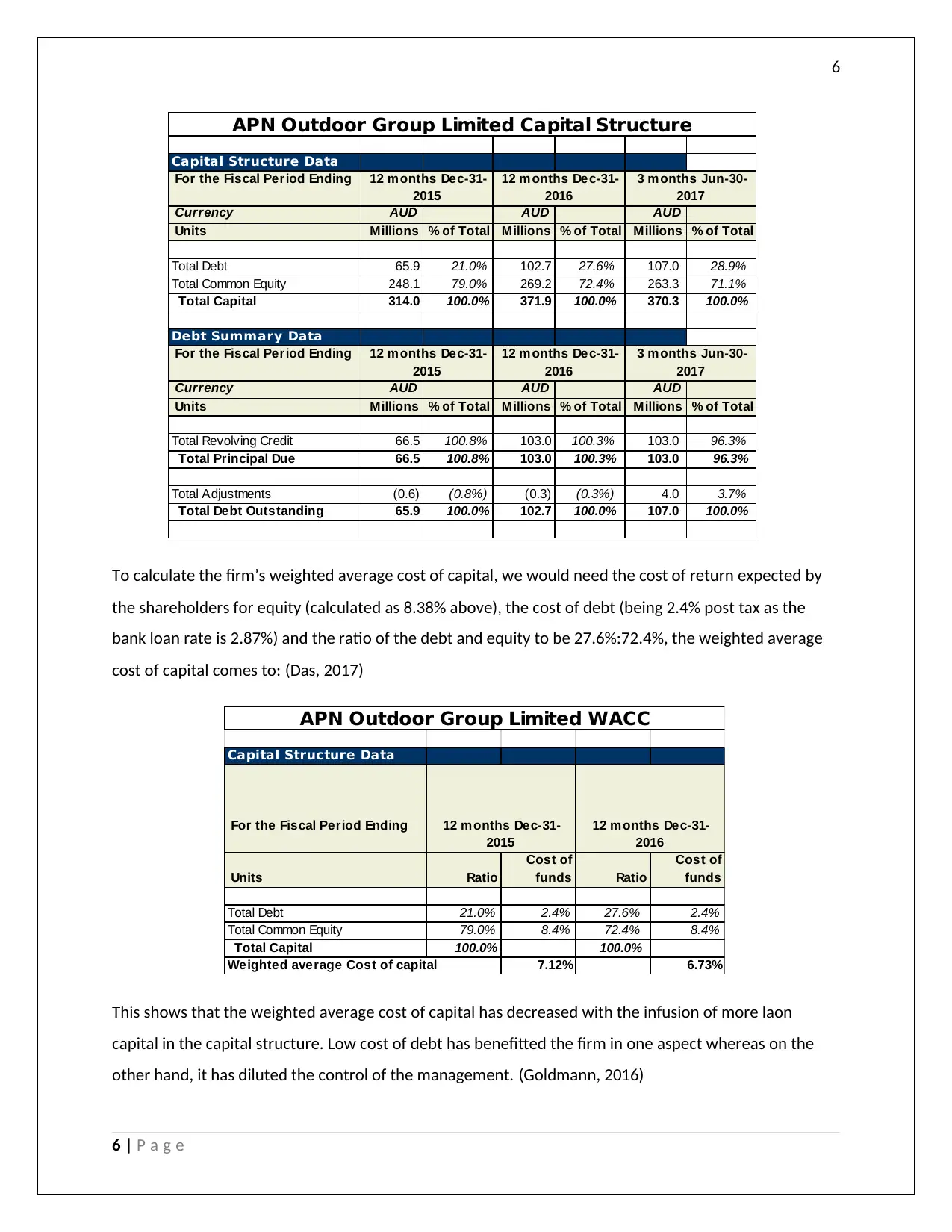

APN Outdoor Group Limited Capital Structure

Details

Below is the split between the firm’s capital structure in between equity and debt which shows tehta

the amount of debt in the capital structure is increasing year on year and hence the company is making

using of trading on equity and thus using leverage to increase its benefits. (David, 2005) This makes the

chep capital available to the company to make use in the business. The ratio of debt to equity has

increased from 21%:79% in 2015 to 27.6%:72.6% in the 2016.

5 | P a g e

Report on the company

Assuming that the company is having the beta of 1.3 in the year 2016, the market rate of

interest being 7% and the risk free rate of interest based on yield on Australia Government Bonds being

2.4%, the required rate of return by the company would be calculated as per Capital Asset Pricing

Model which comes to:

R = RF + (RM-RF) * Beta

Or, R = 2.4 + (7-2.4) * 1.3 = 8.38%

Based on the capital structure of the last 2 years the following is the break up of the capital structure

and the credit facility being used by the company is as follows:

FQ2 2017 (J un- 30- 2017) Capital Structure As Reported Details

Description Type Principal Due (AUD)

General Corporate Facility A * Revolving Credit 80.0

General Corporate Facility C * Revolving Credit -

Working Capital Facility B * Revolving Credit 23.0

FY 2016 (Dec- 31- 2016) Capital Structure As Reported Details

Description Type Principal Due (AUD)

General Corporate Facility A Revolving Credit 80.0

General Corporate Facility C Revolving Credit -

Working Capital Facility B Revolving Credit 23.0

APN Outdoor Group Limited Capital Structure

Details

Below is the split between the firm’s capital structure in between equity and debt which shows tehta

the amount of debt in the capital structure is increasing year on year and hence the company is making

using of trading on equity and thus using leverage to increase its benefits. (David, 2005) This makes the

chep capital available to the company to make use in the business. The ratio of debt to equity has

increased from 21%:79% in 2015 to 27.6%:72.6% in the 2016.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Capital Structure Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Debt 65.9 21.0% 102.7 27.6% 107.0 28.9%

Total Common Equity 248.1 79.0% 269.2 72.4% 263.3 71.1%

Total Capital 314.0 100.0% 371.9 100.0% 370.3 100.0%

Debt Summary Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Revolving Credit 66.5 100.8% 103.0 100.3% 103.0 96.3%

Total Principal Due 66.5 100.8% 103.0 100.3% 103.0 96.3%

Total Adjustments (0.6) (0.8%) (0.3) (0.3%) 4.0 3.7%

Total Debt Outstanding 65.9 100.0% 102.7 100.0% 107.0 100.0%

APN Outdoor Group Limited Capital Structure

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

To calculate the firm’s weighted average cost of capital, we would need the cost of return expected by

the shareholders for equity (calculated as 8.38% above), the cost of debt (being 2.4% post tax as the

bank loan rate is 2.87%) and the ratio of the debt and equity to be 27.6%:72.4%, the weighted average

cost of capital comes to: (Das, 2017)

Capital Structure Data

For the Fiscal Period Ending

Units Ratio

Cost of

funds Ratio

Cost of

funds

Total Debt 21.0% 2.4% 27.6% 2.4%

Total Common Equity 79.0% 8.4% 72.4% 8.4%

Total Capital 100.0% 100.0%

Weighted average Cost of capital 7.12% 6.73%

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

APN Outdoor Group Limited WACC

This shows that the weighted average cost of capital has decreased with the infusion of more laon

capital in the capital structure. Low cost of debt has benefitted the firm in one aspect whereas on the

other hand, it has diluted the control of the management. (Goldmann, 2016)

6 | P a g e

Capital Structure Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Debt 65.9 21.0% 102.7 27.6% 107.0 28.9%

Total Common Equity 248.1 79.0% 269.2 72.4% 263.3 71.1%

Total Capital 314.0 100.0% 371.9 100.0% 370.3 100.0%

Debt Summary Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Revolving Credit 66.5 100.8% 103.0 100.3% 103.0 96.3%

Total Principal Due 66.5 100.8% 103.0 100.3% 103.0 96.3%

Total Adjustments (0.6) (0.8%) (0.3) (0.3%) 4.0 3.7%

Total Debt Outstanding 65.9 100.0% 102.7 100.0% 107.0 100.0%

APN Outdoor Group Limited Capital Structure

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

To calculate the firm’s weighted average cost of capital, we would need the cost of return expected by

the shareholders for equity (calculated as 8.38% above), the cost of debt (being 2.4% post tax as the

bank loan rate is 2.87%) and the ratio of the debt and equity to be 27.6%:72.4%, the weighted average

cost of capital comes to: (Das, 2017)

Capital Structure Data

For the Fiscal Period Ending

Units Ratio

Cost of

funds Ratio

Cost of

funds

Total Debt 21.0% 2.4% 27.6% 2.4%

Total Common Equity 79.0% 8.4% 72.4% 8.4%

Total Capital 100.0% 100.0%

Weighted average Cost of capital 7.12% 6.73%

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

APN Outdoor Group Limited WACC

This shows that the weighted average cost of capital has decreased with the infusion of more laon

capital in the capital structure. Low cost of debt has benefitted the firm in one aspect whereas on the

other hand, it has diluted the control of the management. (Goldmann, 2016)

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

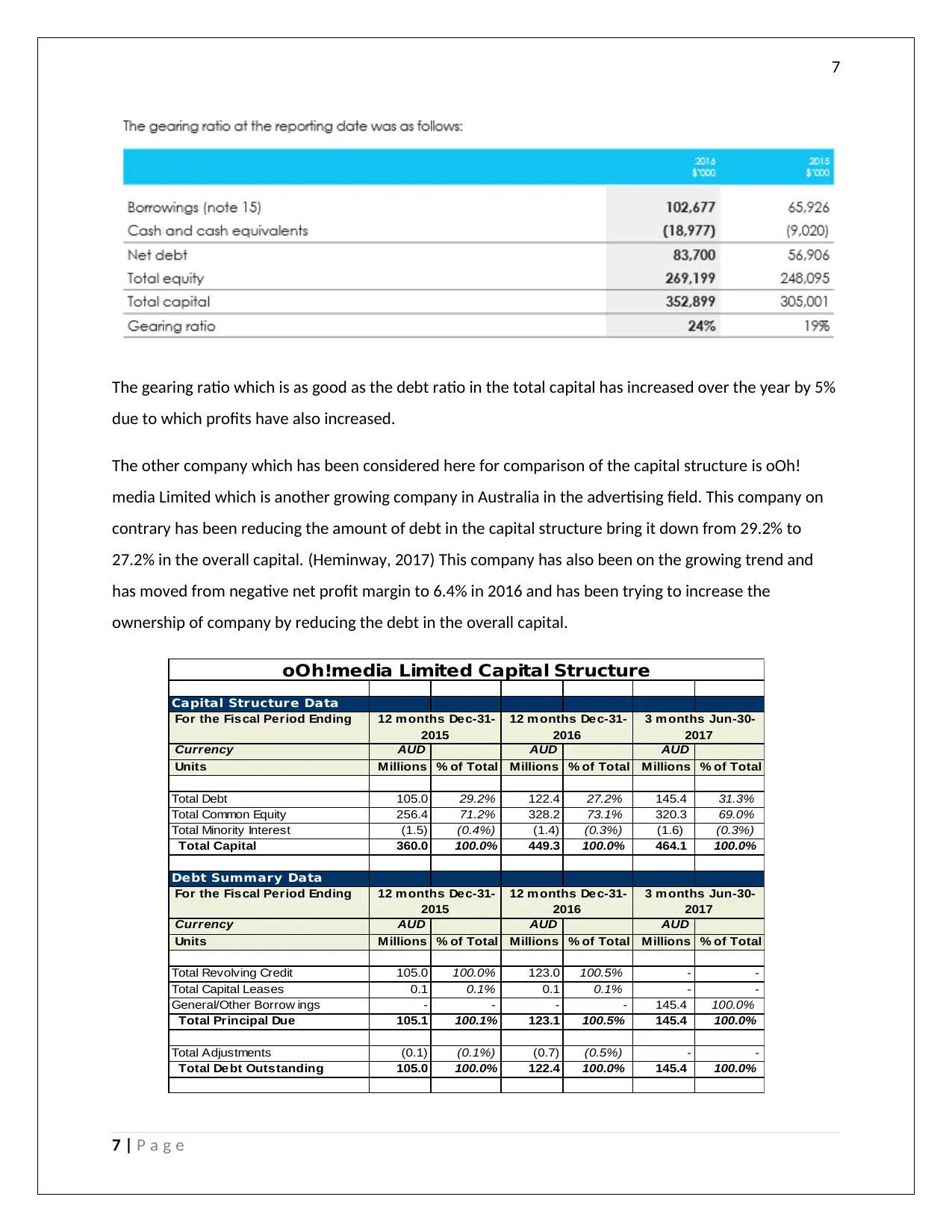

The gearing ratio which is as good as the debt ratio in the total capital has increased over the year by 5%

due to which profits have also increased.

The other company which has been considered here for comparison of the capital structure is oOh!

media Limited which is another growing company in Australia in the advertising field. This company on

contrary has been reducing the amount of debt in the capital structure bring it down from 29.2% to

27.2% in the overall capital. (Heminway, 2017) This company has also been on the growing trend and

has moved from negative net profit margin to 6.4% in 2016 and has been trying to increase the

ownership of company by reducing the debt in the overall capital.

Capital Structure Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Debt 105.0 29.2% 122.4 27.2% 145.4 31.3%

Total Common Equity 256.4 71.2% 328.2 73.1% 320.3 69.0%

Total Minority Interest (1.5) (0.4%) (1.4) (0.3%) (1.6) (0.3%)

Total Capital 360.0 100.0% 449.3 100.0% 464.1 100.0%

Debt Summary Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Revolving Credit 105.0 100.0% 123.0 100.5% - -

Total Capital Leases 0.1 0.1% 0.1 0.1% - -

General/Other Borrow ings - - - - 145.4 100.0%

Total Principal Due 105.1 100.1% 123.1 100.5% 145.4 100.0%

Total Adjustments (0.1) (0.1%) (0.7) (0.5%) - -

Total Debt Outstanding 105.0 100.0% 122.4 100.0% 145.4 100.0%

oOh!media Limited Capital Structure

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

7 | P a g e

The gearing ratio which is as good as the debt ratio in the total capital has increased over the year by 5%

due to which profits have also increased.

The other company which has been considered here for comparison of the capital structure is oOh!

media Limited which is another growing company in Australia in the advertising field. This company on

contrary has been reducing the amount of debt in the capital structure bring it down from 29.2% to

27.2% in the overall capital. (Heminway, 2017) This company has also been on the growing trend and

has moved from negative net profit margin to 6.4% in 2016 and has been trying to increase the

ownership of company by reducing the debt in the overall capital.

Capital Structure Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Debt 105.0 29.2% 122.4 27.2% 145.4 31.3%

Total Common Equity 256.4 71.2% 328.2 73.1% 320.3 69.0%

Total Minority Interest (1.5) (0.4%) (1.4) (0.3%) (1.6) (0.3%)

Total Capital 360.0 100.0% 449.3 100.0% 464.1 100.0%

Debt Summary Data

For the Fiscal Period Ending

Currency AUD AUD AUD

Units Millions % of Total Millions % of Total Millions % of Total

Total Revolving Credit 105.0 100.0% 123.0 100.5% - -

Total Capital Leases 0.1 0.1% 0.1 0.1% - -

General/Other Borrow ings - - - - 145.4 100.0%

Total Principal Due 105.1 100.1% 123.1 100.5% 145.4 100.0%

Total Adjustments (0.1) (0.1%) (0.7) (0.5%) - -

Total Debt Outstanding 105.0 100.0% 122.4 100.0% 145.4 100.0%

oOh!media Limited Capital Structure

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

12 m onths Dec-31-

2015

12 m onths Dec-31-

2016

3 m onths Jun-30-

2017

7 | P a g e

8

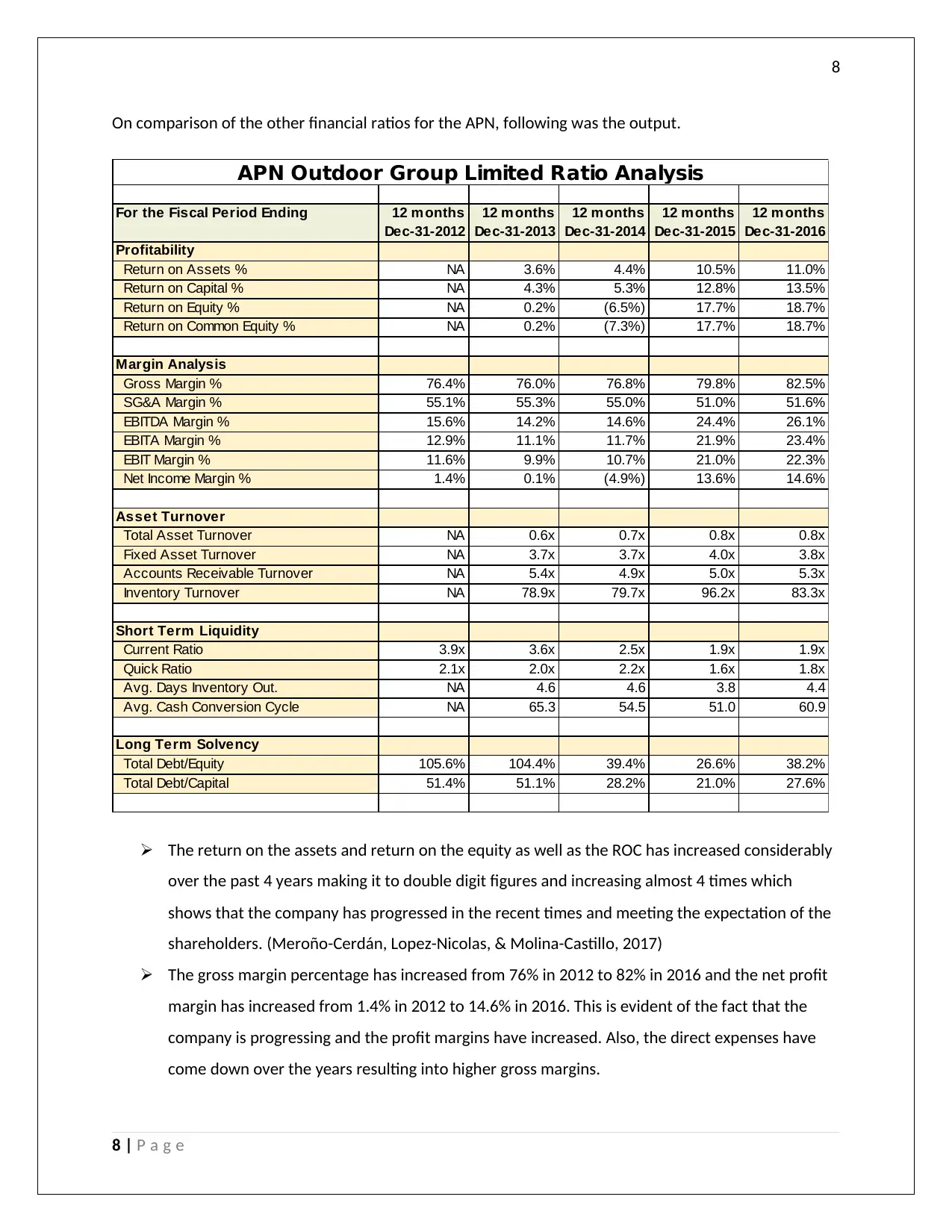

On comparison of the other financial ratios for the APN, following was the output.

For the Fiscal Period Ending 12 m onths

Dec-31-2012

12 m onths

Dec-31-2013

12 m onths

Dec-31-2014

12 m onths

Dec-31-2015

12 m onths

Dec-31-2016

Profitability

Return on Assets % NA 3.6% 4.4% 10.5% 11.0%

Return on Capital % NA 4.3% 5.3% 12.8% 13.5%

Return on Equity % NA 0.2% (6.5%) 17.7% 18.7%

Return on Common Equity % NA 0.2% (7.3%) 17.7% 18.7%

Margin Analysis

Gross Margin % 76.4% 76.0% 76.8% 79.8% 82.5%

SG&A Margin % 55.1% 55.3% 55.0% 51.0% 51.6%

EBITDA Margin % 15.6% 14.2% 14.6% 24.4% 26.1%

EBITA Margin % 12.9% 11.1% 11.7% 21.9% 23.4%

EBIT Margin % 11.6% 9.9% 10.7% 21.0% 22.3%

Net Income Margin % 1.4% 0.1% (4.9%) 13.6% 14.6%

Asset Turnover

Total Asset Turnover NA 0.6x 0.7x 0.8x 0.8x

Fixed Asset Turnover NA 3.7x 3.7x 4.0x 3.8x

Accounts Receivable Turnover NA 5.4x 4.9x 5.0x 5.3x

Inventory Turnover NA 78.9x 79.7x 96.2x 83.3x

Short Term Liquidity

Current Ratio 3.9x 3.6x 2.5x 1.9x 1.9x

Quick Ratio 2.1x 2.0x 2.2x 1.6x 1.8x

Avg. Days Inventory Out. NA 4.6 4.6 3.8 4.4

Avg. Cash Conversion Cycle NA 65.3 54.5 51.0 60.9

Long Term Solvency

Total Debt/Equity 105.6% 104.4% 39.4% 26.6% 38.2%

Total Debt/Capital 51.4% 51.1% 28.2% 21.0% 27.6%

APN Outdoor Group Limited Ratio Analysis

The return on the assets and return on the equity as well as the ROC has increased considerably

over the past 4 years making it to double digit figures and increasing almost 4 times which

shows that the company has progressed in the recent times and meeting the expectation of the

shareholders. (Meroño-Cerdán, Lopez-Nicolas, & Molina-Castillo, 2017)

The gross margin percentage has increased from 76% in 2012 to 82% in 2016 and the net profit

margin has increased from 1.4% in 2012 to 14.6% in 2016. This is evident of the fact that the

company is progressing and the profit margins have increased. Also, the direct expenses have

come down over the years resulting into higher gross margins.

8 | P a g e

On comparison of the other financial ratios for the APN, following was the output.

For the Fiscal Period Ending 12 m onths

Dec-31-2012

12 m onths

Dec-31-2013

12 m onths

Dec-31-2014

12 m onths

Dec-31-2015

12 m onths

Dec-31-2016

Profitability

Return on Assets % NA 3.6% 4.4% 10.5% 11.0%

Return on Capital % NA 4.3% 5.3% 12.8% 13.5%

Return on Equity % NA 0.2% (6.5%) 17.7% 18.7%

Return on Common Equity % NA 0.2% (7.3%) 17.7% 18.7%

Margin Analysis

Gross Margin % 76.4% 76.0% 76.8% 79.8% 82.5%

SG&A Margin % 55.1% 55.3% 55.0% 51.0% 51.6%

EBITDA Margin % 15.6% 14.2% 14.6% 24.4% 26.1%

EBITA Margin % 12.9% 11.1% 11.7% 21.9% 23.4%

EBIT Margin % 11.6% 9.9% 10.7% 21.0% 22.3%

Net Income Margin % 1.4% 0.1% (4.9%) 13.6% 14.6%

Asset Turnover

Total Asset Turnover NA 0.6x 0.7x 0.8x 0.8x

Fixed Asset Turnover NA 3.7x 3.7x 4.0x 3.8x

Accounts Receivable Turnover NA 5.4x 4.9x 5.0x 5.3x

Inventory Turnover NA 78.9x 79.7x 96.2x 83.3x

Short Term Liquidity

Current Ratio 3.9x 3.6x 2.5x 1.9x 1.9x

Quick Ratio 2.1x 2.0x 2.2x 1.6x 1.8x

Avg. Days Inventory Out. NA 4.6 4.6 3.8 4.4

Avg. Cash Conversion Cycle NA 65.3 54.5 51.0 60.9

Long Term Solvency

Total Debt/Equity 105.6% 104.4% 39.4% 26.6% 38.2%

Total Debt/Capital 51.4% 51.1% 28.2% 21.0% 27.6%

APN Outdoor Group Limited Ratio Analysis

The return on the assets and return on the equity as well as the ROC has increased considerably

over the past 4 years making it to double digit figures and increasing almost 4 times which

shows that the company has progressed in the recent times and meeting the expectation of the

shareholders. (Meroño-Cerdán, Lopez-Nicolas, & Molina-Castillo, 2017)

The gross margin percentage has increased from 76% in 2012 to 82% in 2016 and the net profit

margin has increased from 1.4% in 2012 to 14.6% in 2016. This is evident of the fact that the

company is progressing and the profit margins have increased. Also, the direct expenses have

come down over the years resulting into higher gross margins.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

All the turnover ratios namely total asset turnover ratio, fixed assets turnover ratio, Accounts

receivable turnover ratio and the inventory turnover ratio, all of tehm have remained more or

less constant over the last 4 years implying the company is having good control over the

debtors, credoitors, inventory and the fixed assets and thus being able to churn the cash out of

it.

The short term liquidity ratios namely current ratio and the quick rati both have decreased over

the past 5 years from 3.9 times to 1.9 times and 2.1 times to 1.8 times respectively which shows

that the company has been able to utilise it working capital aptly and is not unnecessarily

blocking the funds in the current assets. Not of both is near the industry trend of 2 and 1

respectively which shows the healthy ratios for the firm.

Lastly the debt capital ratio implies the growth in debt over the last one year which shows that

the company is aiming to use the low cost funding to its best benefit such that the profitability

can be increased. (Heminway, 2017)

Significant changes to the capital structure during the past 3 years

Before 2013 the company capital structure was such that it has more than 50% of the funds through

debts and the bank loans and then since 2014 it has tried to keep the share the proportion of debt in the

entire capital to be below 30% by infusion of the funds from the investors. This is because the owners

are aware of the fact that now the company has broke even and is growing superbly with increased

profitability and return for the shareholders. Therefore, now they want to increase the ownership in the

company and thus reduce the dilution in the company’s capital structure.

Wealth maximisation for the shareholders in the past 3 years

We already saw with the help of the ratio analysis that the company has been preforming well in the

recent times and the return on equity which is the foremost measure of wealth maximisation for the

shareholders has increased from negative (-6.5%) in 2014 to to 17.7% in 2015 to 18.7% in 2016. This

shows that the company is growing the wealth for the shareholders, and they are happy to invest and

use more of own capital instead of loan capital. (Jefferson, 2017) It has been beating the market rate of

return of 8.38% which was calculated above. In addition to this, the return on capital has also grown

thrice from 5.3% in 2014 to 13.5% in 2016 which again is the indicator of rapid growth.

9 | P a g e

All the turnover ratios namely total asset turnover ratio, fixed assets turnover ratio, Accounts

receivable turnover ratio and the inventory turnover ratio, all of tehm have remained more or

less constant over the last 4 years implying the company is having good control over the

debtors, credoitors, inventory and the fixed assets and thus being able to churn the cash out of

it.

The short term liquidity ratios namely current ratio and the quick rati both have decreased over

the past 5 years from 3.9 times to 1.9 times and 2.1 times to 1.8 times respectively which shows

that the company has been able to utilise it working capital aptly and is not unnecessarily

blocking the funds in the current assets. Not of both is near the industry trend of 2 and 1

respectively which shows the healthy ratios for the firm.

Lastly the debt capital ratio implies the growth in debt over the last one year which shows that

the company is aiming to use the low cost funding to its best benefit such that the profitability

can be increased. (Heminway, 2017)

Significant changes to the capital structure during the past 3 years

Before 2013 the company capital structure was such that it has more than 50% of the funds through

debts and the bank loans and then since 2014 it has tried to keep the share the proportion of debt in the

entire capital to be below 30% by infusion of the funds from the investors. This is because the owners

are aware of the fact that now the company has broke even and is growing superbly with increased

profitability and return for the shareholders. Therefore, now they want to increase the ownership in the

company and thus reduce the dilution in the company’s capital structure.

Wealth maximisation for the shareholders in the past 3 years

We already saw with the help of the ratio analysis that the company has been preforming well in the

recent times and the return on equity which is the foremost measure of wealth maximisation for the

shareholders has increased from negative (-6.5%) in 2014 to to 17.7% in 2015 to 18.7% in 2016. This

shows that the company is growing the wealth for the shareholders, and they are happy to invest and

use more of own capital instead of loan capital. (Jefferson, 2017) It has been beating the market rate of

return of 8.38% which was calculated above. In addition to this, the return on capital has also grown

thrice from 5.3% in 2014 to 13.5% in 2016 which again is the indicator of rapid growth.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Why is it important to minimise the cost of capital and how can the cost of capital be reduced

The cost of capital represents the cost that the company is incurring on both the loan and the own

capital to get the requisite rate of return by the shareholders. The cost of capital can be decreased by

using more of debt and less of equity in the capital structure. This asks for low interest cost being

incurred on the debt and thus more return left to be distributed among the shareholders. Minimising

the cost of capital is need of the hour considering the immense competition in the market and the hig

returns being expected by the stakeholders. (Murray & Markey Towler, 2017)‐ The alternative for this is

choosing a alternative debt equity structure where the shareholder’s ownership in the company is being

diluted through infusion of low capital. Capital can also be infused by raising the funds from the public

via issue of the shares or through debentures.

10 | P a g e

Why is it important to minimise the cost of capital and how can the cost of capital be reduced

The cost of capital represents the cost that the company is incurring on both the loan and the own

capital to get the requisite rate of return by the shareholders. The cost of capital can be decreased by

using more of debt and less of equity in the capital structure. This asks for low interest cost being

incurred on the debt and thus more return left to be distributed among the shareholders. Minimising

the cost of capital is need of the hour considering the immense competition in the market and the hig

returns being expected by the stakeholders. (Murray & Markey Towler, 2017)‐ The alternative for this is

choosing a alternative debt equity structure where the shareholder’s ownership in the company is being

diluted through infusion of low capital. Capital can also be infused by raising the funds from the public

via issue of the shares or through debentures.

10 | P a g e

11

Conclusion

We made a bried analysis of the company based on various indicators and facts using the annual report

of the company. The capital structure as well as the various ratios is evident of the fact the the company

is in the rising stage and is working effectively and efficiently towards it but since there exists

competition in the market from other rising advertising companies in Australia it needs to hold on to its

competitive advantage. Further, the company needs to improve its capital structure to have the boost to

its profitability as it has the cushion to do so.

11 | P a g e

Conclusion

We made a bried analysis of the company based on various indicators and facts using the annual report

of the company. The capital structure as well as the various ratios is evident of the fact the the company

is in the rising stage and is working effectively and efficiently towards it but since there exists

competition in the market from other rising advertising companies in Australia it needs to hold on to its

competitive advantage. Further, the company needs to improve its capital structure to have the boost to

its profitability as it has the cushion to do so.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.