Analysis of Apollo Minerals Limited's 2019 Budgeted Income Statement

VerifiedAdded on 2022/05/10

|21

|4306

|11

Report

AI Summary

This report provides an in-depth analysis of Apollo Minerals Limited's budgeted income statement for 2019, focusing on the company's financial performance based on the previous year's data. It explores the concept of the master budget, detailing its various elements such as sales, capital expenditure, production, cash, manufacturing overhead, direct materials, direct labor, and selling and administrative budgets. The report also compares and contrasts the top-down and bottom-up approaches to budgeting, evaluating their suitability for Apollo Minerals. Furthermore, the analysis includes a detailed examination of the budgeted income statement for 2019, offering opinions on observed changes and concluding with key findings and recommendations. The report aims to provide a comprehensive understanding of financial planning and budgeting within the context of a specific ASX-listed company.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 1

Executive summary

The aim of the report is to analyse the budgeted incomes statement for the year 2019 of the

company. The ASX Company that has been selected for the analysis is Apollo Minerals Limited

and it focuses on the development of the Couflens Project in the area of Southern France and

progress of the adjacent Aurenere project in the neighbouring country that is Spain. The findings

of the report include the in-depth explanation related to the master budget and its different types

of elements which makes this concept easily approachable for any company. The two approaches

which are majorly used by the company are top-down and the bottom-up approach. These

approaches are compared in the assessment to identify the best suitable approach for Apollo

Minerals Limited. In the end, it includes the findings related to the budgeted income statement of

the company for the year 2019 that is based on the year 2018.

Executive summary

The aim of the report is to analyse the budgeted incomes statement for the year 2019 of the

company. The ASX Company that has been selected for the analysis is Apollo Minerals Limited

and it focuses on the development of the Couflens Project in the area of Southern France and

progress of the adjacent Aurenere project in the neighbouring country that is Spain. The findings

of the report include the in-depth explanation related to the master budget and its different types

of elements which makes this concept easily approachable for any company. The two approaches

which are majorly used by the company are top-down and the bottom-up approach. These

approaches are compared in the assessment to identify the best suitable approach for Apollo

Minerals Limited. In the end, it includes the findings related to the budgeted income statement of

the company for the year 2019 that is based on the year 2018.

Accounting 2

Contents

Introduction......................................................................................................................................4

About Apollo Minerals Limited..................................................................................................4

Master budget..................................................................................................................................5

Elements of Master budget..............................................................................................................5

Sales budget.................................................................................................................................5

Capital expenditure budgets........................................................................................................6

Production budget........................................................................................................................6

Cash budget.................................................................................................................................7

Manufacturing overhead budget..................................................................................................8

Direct materials budget................................................................................................................8

Direct labour budget....................................................................................................................8

Selling and administrative budget...............................................................................................8

Budgeted financial statements.....................................................................................................9

Comparison of a top-down and bottom-up approach to the budget process...................................9

Bottom-up approach....................................................................................................................9

Top-down approach...................................................................................................................10

Comparison chart.......................................................................................................................10

Suggestion for the approach to the company.................................................................................11

Budgeted income statement for 2019............................................................................................12

Contents

Introduction......................................................................................................................................4

About Apollo Minerals Limited..................................................................................................4

Master budget..................................................................................................................................5

Elements of Master budget..............................................................................................................5

Sales budget.................................................................................................................................5

Capital expenditure budgets........................................................................................................6

Production budget........................................................................................................................6

Cash budget.................................................................................................................................7

Manufacturing overhead budget..................................................................................................8

Direct materials budget................................................................................................................8

Direct labour budget....................................................................................................................8

Selling and administrative budget...............................................................................................8

Budgeted financial statements.....................................................................................................9

Comparison of a top-down and bottom-up approach to the budget process...................................9

Bottom-up approach....................................................................................................................9

Top-down approach...................................................................................................................10

Comparison chart.......................................................................................................................10

Suggestion for the approach to the company.................................................................................11

Budgeted income statement for 2019............................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 3

Opinion on Changes..................................................................................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Appendix........................................................................................................................................18

Opinion on Changes..................................................................................................................13

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Appendix........................................................................................................................................18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 4

Introduction

The report focuses on understanding the concept of the budgeted income statement of the Apollo

Minerals Limited for the year 2019 which is based on the revenue and expenses for the year

2018. The income statement of the company majorly reflects the expenditure and revenue for the

particular period of time which generally includes 12 months. The report includes the

explanation of the master budget which is considered as one of the effective concepts of the

accounting. Along with this, the details related to the elements of the accounting are also

discussed in the report which shows the way master budget is created by the company with the

use of its elements. Moreover, the budgeting of the elements needs the company to implement

the budgeting approach which majorly includes top-down approach and bottom-up approach.

The differences among both the approaches are conducted in the report which will help in

analysing the suitable option for the Apollo Minerals Limited. Further, it includes the analysis of

the budgeted income statement of Apollo Minerals Limited for the year 2019 with the opinion of

the differences that take place.

About Apollo Minerals Limited

Apollo Mineral is one of the ASX listed company who majorly focuses on the development of

the Couflens Project in southern France. This has been found that the company is exploring

different gold and tungsten targets in the wider region around both the Couflens Project France

and Aurenere Project in Spain (Apollo minerals, 2018). The company is committed to

developing a modern and responsible as they believe in transparency which the company is

committed to majorly form the sustainable value for our stakeholders (Apollo minerals, 2018).

Introduction

The report focuses on understanding the concept of the budgeted income statement of the Apollo

Minerals Limited for the year 2019 which is based on the revenue and expenses for the year

2018. The income statement of the company majorly reflects the expenditure and revenue for the

particular period of time which generally includes 12 months. The report includes the

explanation of the master budget which is considered as one of the effective concepts of the

accounting. Along with this, the details related to the elements of the accounting are also

discussed in the report which shows the way master budget is created by the company with the

use of its elements. Moreover, the budgeting of the elements needs the company to implement

the budgeting approach which majorly includes top-down approach and bottom-up approach.

The differences among both the approaches are conducted in the report which will help in

analysing the suitable option for the Apollo Minerals Limited. Further, it includes the analysis of

the budgeted income statement of Apollo Minerals Limited for the year 2019 with the opinion of

the differences that take place.

About Apollo Minerals Limited

Apollo Mineral is one of the ASX listed company who majorly focuses on the development of

the Couflens Project in southern France. This has been found that the company is exploring

different gold and tungsten targets in the wider region around both the Couflens Project France

and Aurenere Project in Spain (Apollo minerals, 2018). The company is committed to

developing a modern and responsible as they believe in transparency which the company is

committed to majorly form the sustainable value for our stakeholders (Apollo minerals, 2018).

Accounting 5

Master budget

Master budget is considered as one of the effective accounting concepts which help the business

in performing their operations effectively. The master budget is referred to as one of the plans

which are prepared with the objective to manage the activities like manufacturing and sales of

the company. These activities help the company in accomplishing the cash flow goods and profit

of the company. In other words, this can be said that master budget majorly reflects the

management strategic plan for the future aspects of the company (Accounting tools, 2018). The

company ensure that every aspect of operations is documented and charted with the motive of

the future estimations.

Elements of Master budget

Master budget includes different elements which are essential to be considered by the company

while preparing a master budget. These elements of master budget are discussed below: -

Sales budget

The sales budget is considered as one of the important budgets which is essential to be

considered by the company while preparing the master budget. The sales budget leads to the

straight results that are based on the prediction of related the demand and supply situation, the

competition that is present in the market, the estimation of sales, historical data related to sales

and changes that create the impact on sales (Gitman, Juchau and Flanagan, 2015). These factors

are considered by the company while preparing the sales budget which contributes to master

budget. This has been found that most of the companies make use of this budget with the motive

to prepare the departmental goals. For instance; the marketing and sales team need to ensure the

units of products that they have to sell to meet their targets. Moreover, the sales budget will also

Master budget

Master budget is considered as one of the effective accounting concepts which help the business

in performing their operations effectively. The master budget is referred to as one of the plans

which are prepared with the objective to manage the activities like manufacturing and sales of

the company. These activities help the company in accomplishing the cash flow goods and profit

of the company. In other words, this can be said that master budget majorly reflects the

management strategic plan for the future aspects of the company (Accounting tools, 2018). The

company ensure that every aspect of operations is documented and charted with the motive of

the future estimations.

Elements of Master budget

Master budget includes different elements which are essential to be considered by the company

while preparing a master budget. These elements of master budget are discussed below: -

Sales budget

The sales budget is considered as one of the important budgets which is essential to be

considered by the company while preparing the master budget. The sales budget leads to the

straight results that are based on the prediction of related the demand and supply situation, the

competition that is present in the market, the estimation of sales, historical data related to sales

and changes that create the impact on sales (Gitman, Juchau and Flanagan, 2015). These factors

are considered by the company while preparing the sales budget which contributes to master

budget. This has been found that most of the companies make use of this budget with the motive

to prepare the departmental goals. For instance; the marketing and sales team need to ensure the

units of products that they have to sell to meet their targets. Moreover, the sales budget will also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 6

show the estimation of the earning that will be attained by the companies. Thus, this has been

found that sales budget created the impact in both the overall master budget and the operating

master budget.

Capital expenditure budgets

Capital expenditure budget is referred to a budget plan which is essential to be prepared by the

long term investment. This includes the prediction for new plant’s and equipment’s that are

planned by the company, foremost installation and many other expenses which are faced by the

company in their businesses. The capital budgeting is done by the companies mainly because of

the long term planning that includes the various phase of the database which is considered as

milestones (Kapinos and Mitnik, 2016). Each phase of capital budgeting is estimated and

planned on the basis of time, cost, efforts that are available in the self-controlled method.

Production budget

The production budget is another important element or component of the master budget which is

required to be considered by the company. This budget is majorly prepared for the computation

of the master budget because it requires the production budget which includes the future

estimation of manufacturing operations that has been done on sales budget. Production budget is

prepared with the motive of the high consumption of the approaches and services. This budget

majorly includes the formation of the two budgets which include manufacturing volume budget

and cost of manufacturing budget (Hilton and Platt, 2013).

It has been observed that the volume budget include the estimation of the units of products which

are produced by the company. The budget includes the planning for the goods and services

which are majorly manufactured by them for completing the obligations. The estimation of the

show the estimation of the earning that will be attained by the companies. Thus, this has been

found that sales budget created the impact in both the overall master budget and the operating

master budget.

Capital expenditure budgets

Capital expenditure budget is referred to a budget plan which is essential to be prepared by the

long term investment. This includes the prediction for new plant’s and equipment’s that are

planned by the company, foremost installation and many other expenses which are faced by the

company in their businesses. The capital budgeting is done by the companies mainly because of

the long term planning that includes the various phase of the database which is considered as

milestones (Kapinos and Mitnik, 2016). Each phase of capital budgeting is estimated and

planned on the basis of time, cost, efforts that are available in the self-controlled method.

Production budget

The production budget is another important element or component of the master budget which is

required to be considered by the company. This budget is majorly prepared for the computation

of the master budget because it requires the production budget which includes the future

estimation of manufacturing operations that has been done on sales budget. Production budget is

prepared with the motive of the high consumption of the approaches and services. This budget

majorly includes the formation of the two budgets which include manufacturing volume budget

and cost of manufacturing budget (Hilton and Platt, 2013).

It has been observed that the volume budget include the estimation of the units of products which

are produced by the company. The budget includes the planning for the goods and services

which are majorly manufactured by them for completing the obligations. The estimation of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 7

products that are required to be produced by the company provides the insight about the

production activity and the resources that will be required by the company for conducting the

production activity.

Cash budget

One of the most important elements of the master budget is cash budget; it shows the prediction

for the inflows and outflows of the cash by the company while conducting their business

operations in the specific period of time. The budgets of cash will help the company in analysing

the amount that the company is expected to receive and supposed to pay (Warren, Reeve and

Duchac, 2013). This shows that cash budget is majorly used to analyse that the company is

equipped with sufficient cash or not which is required to be operated by the company for

effective business operations. The forecasting of the cash budget involves the budget of

production and sales as it includes products which are produced by the company and the sales

which will be made by the company.

According to the estimation, the cash budgeting will be done by the company which will help in

maintaining the liquidity of the company in the market. This liquidity will help the company to

meet its obligations. For instance; payroll of the employees which is due to be paid by the

company in the next two weeks and utilities that are required to be paid by the company. Thus,

the prediction in the cash budget will allow the management to predict the shortfalls in the

company and this will help in resolving the problems before the due actually arise. Thus, this can

be said that the cash budget contributes effectively in the formulation of the master budget.

products that are required to be produced by the company provides the insight about the

production activity and the resources that will be required by the company for conducting the

production activity.

Cash budget

One of the most important elements of the master budget is cash budget; it shows the prediction

for the inflows and outflows of the cash by the company while conducting their business

operations in the specific period of time. The budgets of cash will help the company in analysing

the amount that the company is expected to receive and supposed to pay (Warren, Reeve and

Duchac, 2013). This shows that cash budget is majorly used to analyse that the company is

equipped with sufficient cash or not which is required to be operated by the company for

effective business operations. The forecasting of the cash budget involves the budget of

production and sales as it includes products which are produced by the company and the sales

which will be made by the company.

According to the estimation, the cash budgeting will be done by the company which will help in

maintaining the liquidity of the company in the market. This liquidity will help the company to

meet its obligations. For instance; payroll of the employees which is due to be paid by the

company in the next two weeks and utilities that are required to be paid by the company. Thus,

the prediction in the cash budget will allow the management to predict the shortfalls in the

company and this will help in resolving the problems before the due actually arise. Thus, this can

be said that the cash budget contributes effectively in the formulation of the master budget.

Accounting 8

Manufacturing overhead budget

Manufacturing overhead budget is the budget which is prepared by the company which include

the estimation of the cost that indulges in the manufacturing rather than the cost of direct

material and direct labour (Trotman and Carson, 2018). This has been found that in the

preparation of the master budget, manufacturing overhead budget contributes effectively as it

converts the master budget COGS element. Thus, this reflects that it is essential for the company

to predict the amount of manufacturing overhead.

Direct materials budget

Another element of the master budget is Direct material budget which helps the company in

estimating the amount associated with the material which they are purchasing in the set time

period. This budget is prepared by the company who deals on a frequent basis for the raw

material because they want to calculate the exact amount of cash inflows and outflows (Noreen,

Brewer and Garrison, 2014). Thus, it shows that this budget contributes effectively while

forming the master budget.

Direct labour budget

The labour budget is prepared by the company to analyse and evaluate the number of employees

which will be required by the company to meet the details of the master budget. In the budgeting

period, the company ensure that they have proper labour force who will be required for

performing the work effectively (Pilbeam, 2018).

Selling and administrative budget

The administrative and selling are considered as the expenses which are faced by the company

and the budget of these expenses will help in analysing the amount that they are supposed to pay

Manufacturing overhead budget

Manufacturing overhead budget is the budget which is prepared by the company which include

the estimation of the cost that indulges in the manufacturing rather than the cost of direct

material and direct labour (Trotman and Carson, 2018). This has been found that in the

preparation of the master budget, manufacturing overhead budget contributes effectively as it

converts the master budget COGS element. Thus, this reflects that it is essential for the company

to predict the amount of manufacturing overhead.

Direct materials budget

Another element of the master budget is Direct material budget which helps the company in

estimating the amount associated with the material which they are purchasing in the set time

period. This budget is prepared by the company who deals on a frequent basis for the raw

material because they want to calculate the exact amount of cash inflows and outflows (Noreen,

Brewer and Garrison, 2014). Thus, it shows that this budget contributes effectively while

forming the master budget.

Direct labour budget

The labour budget is prepared by the company to analyse and evaluate the number of employees

which will be required by the company to meet the details of the master budget. In the budgeting

period, the company ensure that they have proper labour force who will be required for

performing the work effectively (Pilbeam, 2018).

Selling and administrative budget

The administrative and selling are considered as the expenses which are faced by the company

and the budget of these expenses will help in analysing the amount that they are supposed to pay

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 9

in the budgeted year. This budget includes all non-manufacturing subdivisions which include

book-keeping and services departments, sales and other. The forecasting is spilt into the different

segments so that effective budget is prepared (Accounting tools, 2018). The preparation of the

master budget profit and loss statement is based on the expenses prediction along with the other

expenses which include depreciation and interest.

Budgeted financial statements

This budget is usually limited to the summary level income statement and the balance sheet

which are lined with the model of the budget. The prediction of the master budget requires the

involvement of the budgeted financial statement (Simkin, Norman and Rose, 2014).

The above discussed are the elements of the master budget which are required to be considered

by the company. All these elements include the different budgets which are prepared with the

accurate details.

Comparison of a top-down and bottom-up approach to the budget

process

Bottom-up approach

The bottom-up approach is one of the effective and crucial approaches which is used by the

company at the time of budgeting process. The process in the approach begins with the different

subdivisions available in the company with the motive to form the budget and then send it to the

upward for the approval of the top level management (Weygandt, Kimmel and Kieso, 2015). The

budget is sent for the approval to bring the modification in the master budget by the top level

management so that they can find that the goals of the organisations are properly acknowledged

in the budgeted year. This budget includes all non-manufacturing subdivisions which include

book-keeping and services departments, sales and other. The forecasting is spilt into the different

segments so that effective budget is prepared (Accounting tools, 2018). The preparation of the

master budget profit and loss statement is based on the expenses prediction along with the other

expenses which include depreciation and interest.

Budgeted financial statements

This budget is usually limited to the summary level income statement and the balance sheet

which are lined with the model of the budget. The prediction of the master budget requires the

involvement of the budgeted financial statement (Simkin, Norman and Rose, 2014).

The above discussed are the elements of the master budget which are required to be considered

by the company. All these elements include the different budgets which are prepared with the

accurate details.

Comparison of a top-down and bottom-up approach to the budget

process

Bottom-up approach

The bottom-up approach is one of the effective and crucial approaches which is used by the

company at the time of budgeting process. The process in the approach begins with the different

subdivisions available in the company with the motive to form the budget and then send it to the

upward for the approval of the top level management (Weygandt, Kimmel and Kieso, 2015). The

budget is sent for the approval to bring the modification in the master budget by the top level

management so that they can find that the goals of the organisations are properly acknowledged

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 10

and taken into the consideration by the company. The benefit of the bottom-up budgeting

includes the different types of advantages which show that the computation has been done of the

accurate figure which the motive to improve the budgeting of the company. This has been found

that approach is suitable for the budgeting of the big companies who perform their operations in

different segments and a different number of branches across the world. Though, the

disadvantage of the approach is that employees and manager of the company prepare the budget

in the way so that they can accomplish the goals of the department instead of their organisation.

This has been found that they consider the organisation but goals and objectives remain focuses

towards the department.

Top-down approach

The top-down approach is another effective method of budgeting which is used by the companies

for bringing the improvement in the high-level budget. In this approach, the company prepares

the master budget on the behalf of different departments with the motive that every department

form the objectives that are linked to the goals of the company (Garrison, Noreen, Brewer and

McGowan, 2010). This approach has different benefits and disadvantages that are offered by the

approach to the company. Further, this has been found that top-down strategy calls for every

decision that is required to be made by the senior organisational leaders. The approach includes

the systems which are formulated, specifying but not detailing or any type of the first-level

subsystems. The other benefit of the top-down approach is that decisions can be prepared and

implemented very quickly. Though, the approach has some of the disadvantages which include

the lack of skills of employees that can affect the skills of the budget and will misguide the

employees towards the goal of the organisations.

and taken into the consideration by the company. The benefit of the bottom-up budgeting

includes the different types of advantages which show that the computation has been done of the

accurate figure which the motive to improve the budgeting of the company. This has been found

that approach is suitable for the budgeting of the big companies who perform their operations in

different segments and a different number of branches across the world. Though, the

disadvantage of the approach is that employees and manager of the company prepare the budget

in the way so that they can accomplish the goals of the department instead of their organisation.

This has been found that they consider the organisation but goals and objectives remain focuses

towards the department.

Top-down approach

The top-down approach is another effective method of budgeting which is used by the companies

for bringing the improvement in the high-level budget. In this approach, the company prepares

the master budget on the behalf of different departments with the motive that every department

form the objectives that are linked to the goals of the company (Garrison, Noreen, Brewer and

McGowan, 2010). This approach has different benefits and disadvantages that are offered by the

approach to the company. Further, this has been found that top-down strategy calls for every

decision that is required to be made by the senior organisational leaders. The approach includes

the systems which are formulated, specifying but not detailing or any type of the first-level

subsystems. The other benefit of the top-down approach is that decisions can be prepared and

implemented very quickly. Though, the approach has some of the disadvantages which include

the lack of skills of employees that can affect the skills of the budget and will misguide the

employees towards the goal of the organisations.

Accounting 11

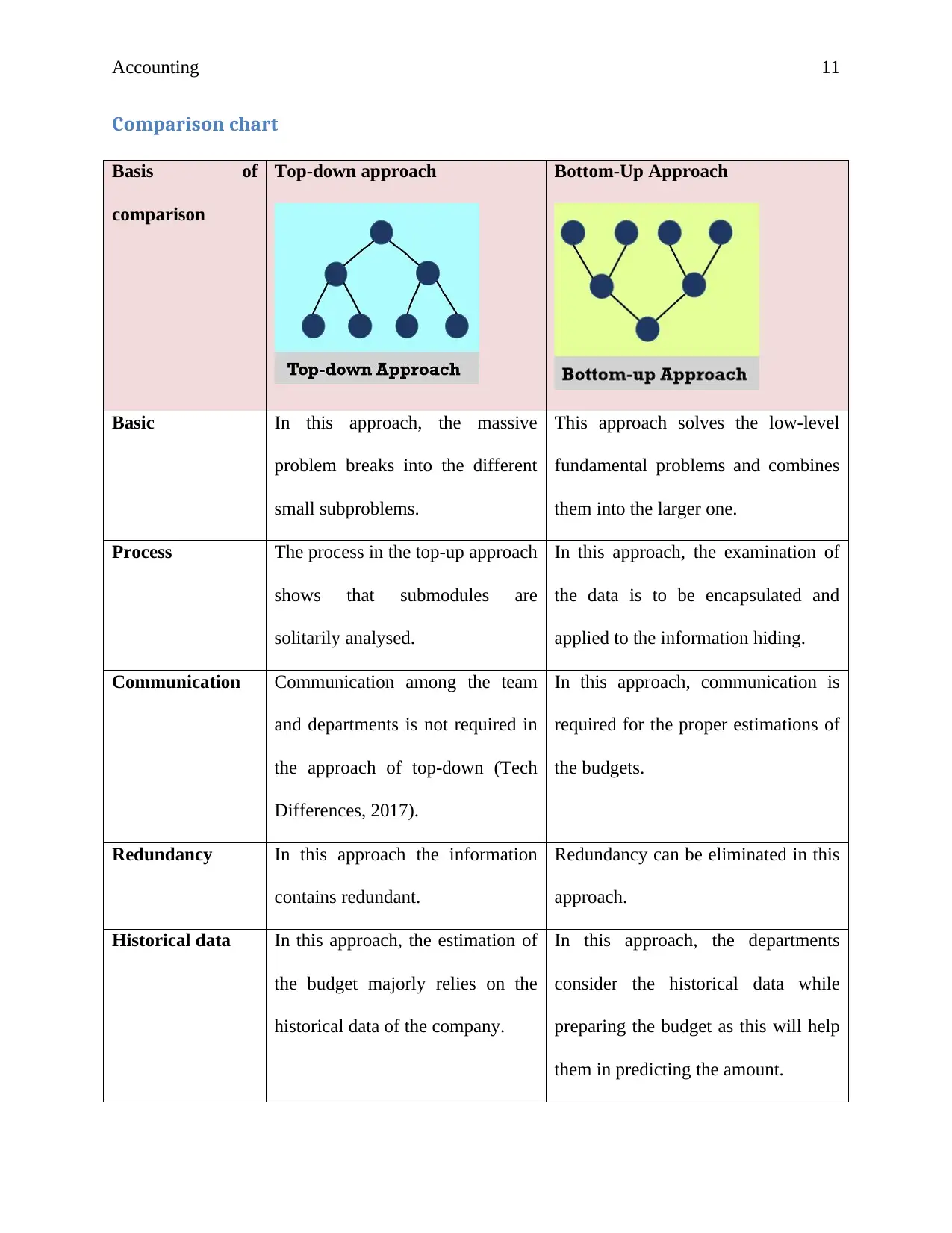

Comparison chart

Basis of

comparison

Top-down approach Bottom-Up Approach

Basic In this approach, the massive

problem breaks into the different

small subproblems.

This approach solves the low-level

fundamental problems and combines

them into the larger one.

Process The process in the top-up approach

shows that submodules are

solitarily analysed.

In this approach, the examination of

the data is to be encapsulated and

applied to the information hiding.

Communication Communication among the team

and departments is not required in

the approach of top-down (Tech

Differences, 2017).

In this approach, communication is

required for the proper estimations of

the budgets.

Redundancy In this approach the information

contains redundant.

Redundancy can be eliminated in this

approach.

Historical data In this approach, the estimation of

the budget majorly relies on the

historical data of the company.

In this approach, the departments

consider the historical data while

preparing the budget as this will help

them in predicting the amount.

Comparison chart

Basis of

comparison

Top-down approach Bottom-Up Approach

Basic In this approach, the massive

problem breaks into the different

small subproblems.

This approach solves the low-level

fundamental problems and combines

them into the larger one.

Process The process in the top-up approach

shows that submodules are

solitarily analysed.

In this approach, the examination of

the data is to be encapsulated and

applied to the information hiding.

Communication Communication among the team

and departments is not required in

the approach of top-down (Tech

Differences, 2017).

In this approach, communication is

required for the proper estimations of

the budgets.

Redundancy In this approach the information

contains redundant.

Redundancy can be eliminated in this

approach.

Historical data In this approach, the estimation of

the budget majorly relies on the

historical data of the company.

In this approach, the departments

consider the historical data while

preparing the budget as this will help

them in predicting the amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.