HI6026 Auditing Report: An Analysis of Apollo Minerals Limited

VerifiedAdded on 2023/06/07

|16

|3696

|363

Report

AI Summary

This report evaluates the effectiveness of material information presented in the annual report of Apollo Minerals Limited, an Australian Stock Exchange-listed company. It examines the auditor's assurance services, compliance with independence requirements, and the nature of non-audit services provided. The analysis includes a review of auditor remuneration, key audit matters, and the audit committee's composition, functions, and responsibilities. The audit opinion expressed is evaluated, along with the differences between management and auditor responsibilities. Key audit matters, such as expenditures incurred in rights acquisition, asset impairment, and deferred tax liabilities, are addressed through specific audit procedures. The report concludes with an assessment of the audit committee's role in ensuring effective financial reporting and governance.

Running head: AUDITING THEORY AND PRACTICE

Auditing theory and practice

Name of the University

Name of the student

Authors note

Auditing theory and practice

Name of the University

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING THEORY AND PRACTICE

Executive summary:

The report is prepared for evaluating the effectiveness of any material information that is

presented in the annual report of one of the Australian stock exchange listed companies. The

chosen company for the analysis purpose is Apollo minerals limited. Data relating to the auditing

report and matters on audit have been extracted from the annual report published by the company

which is sourced from its website. Explanation of audit committee is terms of its functions,

composition and responsibilities. Each of the identified key audit matters have been explained by

performing the audit procedures that helps in providing assurance. Remuneration of auditors

have been depicted in the table format that facilitates comparison of the payment made by

company in different years.

AUDITING THEORY AND PRACTICE

Executive summary:

The report is prepared for evaluating the effectiveness of any material information that is

presented in the annual report of one of the Australian stock exchange listed companies. The

chosen company for the analysis purpose is Apollo minerals limited. Data relating to the auditing

report and matters on audit have been extracted from the annual report published by the company

which is sourced from its website. Explanation of audit committee is terms of its functions,

composition and responsibilities. Each of the identified key audit matters have been explained by

performing the audit procedures that helps in providing assurance. Remuneration of auditors

have been depicted in the table format that facilitates comparison of the payment made by

company in different years.

2

AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

1) Evaluation of the auditor’s assurance services:...........................................................................3

2) Evaluation of Compliance of auditors with independence requirements:...................................3

3) Nature of non audit services:.......................................................................................................3

4) Analysis of remuneration of auditors:.........................................................................................3

5) Evaluation of key audit matters:..................................................................................................3

6) Evaluation of audit committee:...................................................................................................4

7) Audit opinion expressed:.............................................................................................................4

8) Difference between the responsibilities of management and auditors:.......................................4

Conclusion:......................................................................................................................................4

Reference list:..................................................................................................................................4

AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................3

Discussion:.......................................................................................................................................3

1) Evaluation of the auditor’s assurance services:...........................................................................3

2) Evaluation of Compliance of auditors with independence requirements:...................................3

3) Nature of non audit services:.......................................................................................................3

4) Analysis of remuneration of auditors:.........................................................................................3

5) Evaluation of key audit matters:..................................................................................................3

6) Evaluation of audit committee:...................................................................................................4

7) Audit opinion expressed:.............................................................................................................4

8) Difference between the responsibilities of management and auditors:.......................................4

Conclusion:......................................................................................................................................4

Reference list:..................................................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING THEORY AND PRACTICE

Introduction:

The report demonstrates the evaluation and summary of auditor’s assurance services

provided by the auditors to their clients. For this purpose, the analysis of the auditor’s report and

the data relating to the same has been extracted from the annual report of the selected company.

The chosen company for the analysis of auditor’s functions is an Apollo mineral limited that is

listed on the Australian stock exchange. The main focus of company is to develop the Southern

France Couflens project along with progressing the Aurene project in neighboring Spain.

Company main objective regarding the Couflens project is to focus on the potential Salau mine

reactivation. Several regional exploration programs have been conducted by company that has

been identified by the Aurene and Couflens project. There are several areas related to the

auditing that have been analyzed in the report that include non assurance services, remuneration,

key audit matters, audit committee and audit opinion (Knechel et al., 2016). In addition to this,

the effectiveness of material information has been assessed in the report. All the information

relating to auditing of Apollo minerals have been extracted from the annual report of the

company.

Discussion:

1) Evaluation of the auditor’s assurance services:

The relevant government authority conducts inspection for indentifying the instances of

the environmental non compliance in terms of operations. Auditor of Apollo minerals limited has

conducted review of financial report that comprises of the condensed consolidated statements

financial position, condensed consolidated statement changes in equity, condensed consolidated

statement profit and loss, and condensed consolidated statement comprehensive income as at 31st

December, 2017. The auditor to the best of their belief and knowledge makes the declaration that

AUDITING THEORY AND PRACTICE

Introduction:

The report demonstrates the evaluation and summary of auditor’s assurance services

provided by the auditors to their clients. For this purpose, the analysis of the auditor’s report and

the data relating to the same has been extracted from the annual report of the selected company.

The chosen company for the analysis of auditor’s functions is an Apollo mineral limited that is

listed on the Australian stock exchange. The main focus of company is to develop the Southern

France Couflens project along with progressing the Aurene project in neighboring Spain.

Company main objective regarding the Couflens project is to focus on the potential Salau mine

reactivation. Several regional exploration programs have been conducted by company that has

been identified by the Aurene and Couflens project. There are several areas related to the

auditing that have been analyzed in the report that include non assurance services, remuneration,

key audit matters, audit committee and audit opinion (Knechel et al., 2016). In addition to this,

the effectiveness of material information has been assessed in the report. All the information

relating to auditing of Apollo minerals have been extracted from the annual report of the

company.

Discussion:

1) Evaluation of the auditor’s assurance services:

The relevant government authority conducts inspection for indentifying the instances of

the environmental non compliance in terms of operations. Auditor of Apollo minerals limited has

conducted review of financial report that comprises of the condensed consolidated statements

financial position, condensed consolidated statement changes in equity, condensed consolidated

statement profit and loss, and condensed consolidated statement comprehensive income as at 31st

December, 2017. The auditor to the best of their belief and knowledge makes the declaration that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING THEORY AND PRACTICE

there have been no contraventions of independence requirements of auditors and any code that is

applicable to the professional conduct in relation to the review (Khelil et al., 2016).

2) Evaluation of Compliance of auditors with independence requirements:

The external compliance audit is responsible for indentifying any instances of non

compliance with the environmental matters. Financial report of Apollo minerals limited

complies with the IFRS (International financial reporting standard) and AAS (Australian

accounting standard) that is issued by IASB (International accounting standard board) (Tepalagul

& Lin, 2015).

3) Nature of non audit services:

The auditor of Apollo minerals limited has not performed any non audit services in the

financial year 2017. However, during the financial year 2016, few non audit services were

provided by the auditor of Apollo minerals limited. For the taxation services, company made

payment of fees to Hall Chadwick of amount $ 1650. Reviewing and approval of all non audit

services are done by the directors for ensuring that the objectivity and integrity of auditors is not

adversely affected by providing such services. In relation to non audit services provisions,

directors are satisfied in terms of the services compatibility with the auditor independence

standard. Performance of such services by internal auditor has not compromised the

independence of external auditor (Brasel et al., 2016). There is no comprising of the nature of

services with the general principles of independence of auditors according to ARES 110.

4) Analysis of remuneration of auditors:

The table below illustrates the total amount of remuneration paid to the auditors for the

financial year 2017 and 2016. Remuneration is paid to the auditors for conducting the review of

AUDITING THEORY AND PRACTICE

there have been no contraventions of independence requirements of auditors and any code that is

applicable to the professional conduct in relation to the review (Khelil et al., 2016).

2) Evaluation of Compliance of auditors with independence requirements:

The external compliance audit is responsible for indentifying any instances of non

compliance with the environmental matters. Financial report of Apollo minerals limited

complies with the IFRS (International financial reporting standard) and AAS (Australian

accounting standard) that is issued by IASB (International accounting standard board) (Tepalagul

& Lin, 2015).

3) Nature of non audit services:

The auditor of Apollo minerals limited has not performed any non audit services in the

financial year 2017. However, during the financial year 2016, few non audit services were

provided by the auditor of Apollo minerals limited. For the taxation services, company made

payment of fees to Hall Chadwick of amount $ 1650. Reviewing and approval of all non audit

services are done by the directors for ensuring that the objectivity and integrity of auditors is not

adversely affected by providing such services. In relation to non audit services provisions,

directors are satisfied in terms of the services compatibility with the auditor independence

standard. Performance of such services by internal auditor has not compromised the

independence of external auditor (Brasel et al., 2016). There is no comprising of the nature of

services with the general principles of independence of auditors according to ARES 110.

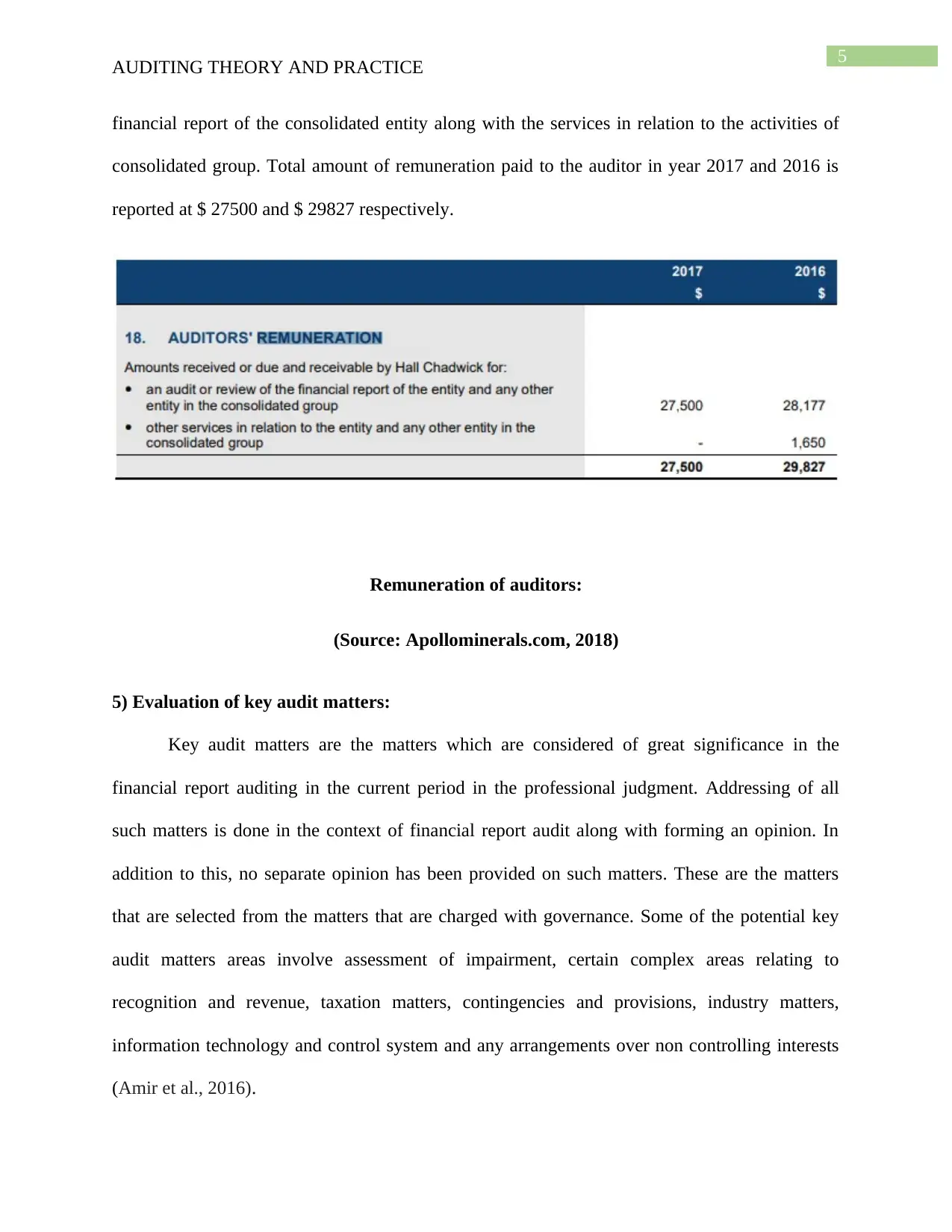

4) Analysis of remuneration of auditors:

The table below illustrates the total amount of remuneration paid to the auditors for the

financial year 2017 and 2016. Remuneration is paid to the auditors for conducting the review of

5

AUDITING THEORY AND PRACTICE

financial report of the consolidated entity along with the services in relation to the activities of

consolidated group. Total amount of remuneration paid to the auditor in year 2017 and 2016 is

reported at $ 27500 and $ 29827 respectively.

Remuneration of auditors:

(Source: Apollominerals.com, 2018)

5) Evaluation of key audit matters:

Key audit matters are the matters which are considered of great significance in the

financial report auditing in the current period in the professional judgment. Addressing of all

such matters is done in the context of financial report audit along with forming an opinion. In

addition to this, no separate opinion has been provided on such matters. These are the matters

that are selected from the matters that are charged with governance. Some of the potential key

audit matters areas involve assessment of impairment, certain complex areas relating to

recognition and revenue, taxation matters, contingencies and provisions, industry matters,

information technology and control system and any arrangements over non controlling interests

(Amir et al., 2016).

AUDITING THEORY AND PRACTICE

financial report of the consolidated entity along with the services in relation to the activities of

consolidated group. Total amount of remuneration paid to the auditor in year 2017 and 2016 is

reported at $ 27500 and $ 29827 respectively.

Remuneration of auditors:

(Source: Apollominerals.com, 2018)

5) Evaluation of key audit matters:

Key audit matters are the matters which are considered of great significance in the

financial report auditing in the current period in the professional judgment. Addressing of all

such matters is done in the context of financial report audit along with forming an opinion. In

addition to this, no separate opinion has been provided on such matters. These are the matters

that are selected from the matters that are charged with governance. Some of the potential key

audit matters areas involve assessment of impairment, certain complex areas relating to

recognition and revenue, taxation matters, contingencies and provisions, industry matters,

information technology and control system and any arrangements over non controlling interests

(Amir et al., 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING THEORY AND PRACTICE

Key audit matters Addressing of key audit matters

Expenditures that have been incurred in the rights

acquisition

For recording and exploring the assets, the group

capitalized the expenditures that is incurred and is

likely to recover and requires a reasonable

assessment of existence of reserves. The ability of

organization to continue as a going concern is

dependent upon the entity to manage the expenses

including the minimum expenditure so that they do

not exceed the existing cash reserves.

Assets impairment Some of the carrying value of evaluation

expenditure and exploration has been written down

by the company during the particular financial year

as depicted in the note i(v). In addition to this, there

are certain reserves areas for which there has not

been extraction of any reserves. However, it is

continuously believed by the directors that since

there is not any inclusion of feasibility studies,

there should not be writing off such expenditures

(Byrnes et al., 2018). At the report date, the

carrying value of capitalized expenditure stood at $

6667645.

Deferred tax liabilities and assets.

Recognition of deferred tax liabilities and assets are

done for the temporary differences in the tax rate

that is expected to be applicable when the liabilities

In recognition of deferred liabilities and

taxes, judgment of management is

required in making estimation of future

taxable income that is recognized as

AUDITING THEORY AND PRACTICE

Key audit matters Addressing of key audit matters

Expenditures that have been incurred in the rights

acquisition

For recording and exploring the assets, the group

capitalized the expenditures that is incurred and is

likely to recover and requires a reasonable

assessment of existence of reserves. The ability of

organization to continue as a going concern is

dependent upon the entity to manage the expenses

including the minimum expenditure so that they do

not exceed the existing cash reserves.

Assets impairment Some of the carrying value of evaluation

expenditure and exploration has been written down

by the company during the particular financial year

as depicted in the note i(v). In addition to this, there

are certain reserves areas for which there has not

been extraction of any reserves. However, it is

continuously believed by the directors that since

there is not any inclusion of feasibility studies,

there should not be writing off such expenditures

(Byrnes et al., 2018). At the report date, the

carrying value of capitalized expenditure stood at $

6667645.

Deferred tax liabilities and assets.

Recognition of deferred tax liabilities and assets are

done for the temporary differences in the tax rate

that is expected to be applicable when the liabilities

In recognition of deferred liabilities and

taxes, judgment of management is

required in making estimation of future

taxable income that is recognized as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING THEORY AND PRACTICE

are settled and assets are recovered. Such

settlements are done based on the rate of taxation

that is enacted substantively for each jurisdiction

(Gaynor et al., 2016).

key audit matter. The assumptions

made by management are assessed for

the appropriate current and deferred tax

provisions (Cordos et al., 2015). It has

been found that the disclosures relating

to the deferred tax and income tax

balances have found to be appropriate.

6) Evaluation of audit committee:

For the financial year 2016, there has not been establishment of audit committee by the

board and until the time, it has been established by the board that establishing the audit

committee is considered appropriate and the auditing charter has been performed by the board.

The audit committee of Apollo minerals limited is the committee of the board of company that is

entrusted with the specific powers that is delegated in the charter. The composition, functions,

authorities and responsibilities along with the mode of operations is set out by the audit charter

(Beck et al., 2014). On any external audit arrangements, it is the responsibility of committee to

make reporting to the board.

Composition of audit committee:

The members of audit committee should be appointed by the board and reviewing of the

composition should be done annually. The audit committee of Apollo Minerals limited is

comprised of

at least three members

AUDITING THEORY AND PRACTICE

are settled and assets are recovered. Such

settlements are done based on the rate of taxation

that is enacted substantively for each jurisdiction

(Gaynor et al., 2016).

key audit matter. The assumptions

made by management are assessed for

the appropriate current and deferred tax

provisions (Cordos et al., 2015). It has

been found that the disclosures relating

to the deferred tax and income tax

balances have found to be appropriate.

6) Evaluation of audit committee:

For the financial year 2016, there has not been establishment of audit committee by the

board and until the time, it has been established by the board that establishing the audit

committee is considered appropriate and the auditing charter has been performed by the board.

The audit committee of Apollo minerals limited is the committee of the board of company that is

entrusted with the specific powers that is delegated in the charter. The composition, functions,

authorities and responsibilities along with the mode of operations is set out by the audit charter

(Beck et al., 2014). On any external audit arrangements, it is the responsibility of committee to

make reporting to the board.

Composition of audit committee:

The members of audit committee should be appointed by the board and reviewing of the

composition should be done annually. The audit committee of Apollo Minerals limited is

comprised of

at least three members

8

AUDITING THEORY AND PRACTICE

a majority of independent non executive directors

Independent chairman who is appointed by the board and such independent chairman is

not boards’ chairman.

The members that are considered relevant to the functioning of audit are the member

having sufficient experience and financial skills (Roy et al., 2016).

Function of audit committee:

Providing assistance to the board in fulfilling the responsibilities relating to the reporting

and accounting practices of company is the audit committee primary function (Barua et al.,

2016). In addition to this, the audit committee performs the following listed functions.

They are entitled to determine the effectiveness and independence of internal and external

auditors of Apollo minerals limited.

Audit committee is required to coordinate, oversee and appraise the quality of audits that

is conducted by the internal and external auditors of company.

Reviewing of the accounting control and the adequacy of reporting is required to be done

by audit committee.

For reviewing the financial information that is submitted to the board by management for

issuing to the regulatory authorities, shareholders and general public are done by the audit

committee that serve as objective and independent party.

The exchange of information and views is facilitated by maintaining open lines of

communication between internal and external auditors and board for exchanging

information and views along with confirming their respective responsibilities and

authorities (DeZoort & Taylor, 2015).

AUDITING THEORY AND PRACTICE

a majority of independent non executive directors

Independent chairman who is appointed by the board and such independent chairman is

not boards’ chairman.

The members that are considered relevant to the functioning of audit are the member

having sufficient experience and financial skills (Roy et al., 2016).

Function of audit committee:

Providing assistance to the board in fulfilling the responsibilities relating to the reporting

and accounting practices of company is the audit committee primary function (Barua et al.,

2016). In addition to this, the audit committee performs the following listed functions.

They are entitled to determine the effectiveness and independence of internal and external

auditors of Apollo minerals limited.

Audit committee is required to coordinate, oversee and appraise the quality of audits that

is conducted by the internal and external auditors of company.

Reviewing of the accounting control and the adequacy of reporting is required to be done

by audit committee.

For reviewing the financial information that is submitted to the board by management for

issuing to the regulatory authorities, shareholders and general public are done by the audit

committee that serve as objective and independent party.

The exchange of information and views is facilitated by maintaining open lines of

communication between internal and external auditors and board for exchanging

information and views along with confirming their respective responsibilities and

authorities (DeZoort & Taylor, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING THEORY AND PRACTICE

However, it is not required by audit committee to personally conduct audit and

accounting reviews and they rely on the professional advisers and employees of company.

Responsibilities of audit committee:

It is required by audit committee to promote an environment that is consistent with the

financial reporting that is best practiced. Committee in particular is required to perform several

responsibilities that are listed below:

They are responsible for monitoring the effectiveness and integrity of the financial

reporting process.

For external reporting, audit committee should conduct an independent review of the

financial information presented by the management. Such activities incorporate

conducting reviews of annual financial statements, director’s report, annual report and

other externally produced financial report (Christ et al., 2015).

Assessment and reviewing of the external audit arrangements should be done by the

auditors.

Audit committee should ensure that the adequate systems are in place and established

policies are appropriate and assessing the related party transactions propriety.

The internal audit arrangements is reviewed, appointed and assessed by audit committee

and they are required to take into account responses of management, findings of internal

audit and related actions (Crockett & Ali, 2015).

AUDITING THEORY AND PRACTICE

However, it is not required by audit committee to personally conduct audit and

accounting reviews and they rely on the professional advisers and employees of company.

Responsibilities of audit committee:

It is required by audit committee to promote an environment that is consistent with the

financial reporting that is best practiced. Committee in particular is required to perform several

responsibilities that are listed below:

They are responsible for monitoring the effectiveness and integrity of the financial

reporting process.

For external reporting, audit committee should conduct an independent review of the

financial information presented by the management. Such activities incorporate

conducting reviews of annual financial statements, director’s report, annual report and

other externally produced financial report (Christ et al., 2015).

Assessment and reviewing of the external audit arrangements should be done by the

auditors.

Audit committee should ensure that the adequate systems are in place and established

policies are appropriate and assessing the related party transactions propriety.

The internal audit arrangements is reviewed, appointed and assessed by audit committee

and they are required to take into account responses of management, findings of internal

audit and related actions (Crockett & Ali, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING THEORY AND PRACTICE

7) Audit opinion expressed:

The independent auditor of Apollo minerals limited is Deloitte that has made independent

declaration about the financial report. It has been concluded by the auditor based on the review

that they have not been acquainted with any matters that made them believe that financial report

have not been prepared according to the requirements of Corporation Act, 2001. They have

concluded that the financial report of Apollo minerals limited have complied with the AASB 134

accounting standard interim financial reporting and the financial position of the consolidated

entity gives a true and fair view in reference to the financial report ending financial year 2017

(Sultana et al., 2015). Furthermore, an attention to the note 2 in the financial report for financial

year 2017 have been drawn by auditors which is indicative of the fact that organization has

experienced a net cash outflow from operating activities and has incurred a net loss. The matters

set forth in the notes and the conditions are indicative of the fact of existence of material

uncertainty about the consolidated entity to continue as going concern (Alzeban & Sawan, 2015).

In respect of this matter, there has not been any modification in the conclusion made.

8) Difference between the responsibilities of management and auditors:

The responsibility of the directors and management of Apollo minerals limited is involve

in the preparation of the financial report that provides users with the true and fair view of the

financial statements. Such true and fair view of the financial statements should be according to

the requirements of the Corporations Act and Australian accounting standard. In addition to this,

directors of organization are also entitled to implement the appropriate internal control system

which is considered essential for the preparation of the financial report. Such internal control

AUDITING THEORY AND PRACTICE

7) Audit opinion expressed:

The independent auditor of Apollo minerals limited is Deloitte that has made independent

declaration about the financial report. It has been concluded by the auditor based on the review

that they have not been acquainted with any matters that made them believe that financial report

have not been prepared according to the requirements of Corporation Act, 2001. They have

concluded that the financial report of Apollo minerals limited have complied with the AASB 134

accounting standard interim financial reporting and the financial position of the consolidated

entity gives a true and fair view in reference to the financial report ending financial year 2017

(Sultana et al., 2015). Furthermore, an attention to the note 2 in the financial report for financial

year 2017 have been drawn by auditors which is indicative of the fact that organization has

experienced a net cash outflow from operating activities and has incurred a net loss. The matters

set forth in the notes and the conditions are indicative of the fact of existence of material

uncertainty about the consolidated entity to continue as going concern (Alzeban & Sawan, 2015).

In respect of this matter, there has not been any modification in the conclusion made.

8) Difference between the responsibilities of management and auditors:

The responsibility of the directors and management of Apollo minerals limited is involve

in the preparation of the financial report that provides users with the true and fair view of the

financial statements. Such true and fair view of the financial statements should be according to

the requirements of the Corporations Act and Australian accounting standard. In addition to this,

directors of organization are also entitled to implement the appropriate internal control system

which is considered essential for the preparation of the financial report. Such internal control

11

AUDITING THEORY AND PRACTICE

system helps in ensuring that the financial statements are free from misrepresentation and they

are not materially represented due to the occurrence of fraud and errors.

On other hand, the responsibility of the auditors of Apollo minerals limited is to express

an opinion on the financial report presented and make conclusion on the review of the

management about report that is of great assistance to users in their investment decision making.

The review of the financial report has been conducted according to the auditing standard on

review engagement ASRE 2410 of the reviewing financial report. Such reviewing is done by the

independent auditors of the Apollo limited. Auditors are entitled to report if the financial report

is not prepared according to the Corporation Act, 2001 and they do not provide true and fair view

to the users (Lisic et al., 2016). As per the requirement of ASRE 2410, the auditors of Apollo

minerals should comply with the ethical requirements that are significant to the auditing of the

annual report or financial report of the company. Reviewing of the annual report requires

auditors to make enquiries of the persons who are responsible for accounting and financial

matters along with reviewing of procedures and applying analytical. A review conducted that is

considered to have lesser scope does not lead to obtaining of assurance that they would become

acquainted with the matters that are identified in the audit (Power & Gendron, 2015). According

to that, no opinions have been expressed by the auditors.

Conclusion:

The current study elucidating on determining the effectiveness of the role of auditors in

providing assurance services to the Apollo minerals limited have found that they play a

significant role in assessing the financial statements in relation to its fair and true presentation

that is free from any material misrepresentation. Several assurance services have been provided

by auditors along with some non audit services in previous financial year. However, no such

AUDITING THEORY AND PRACTICE

system helps in ensuring that the financial statements are free from misrepresentation and they

are not materially represented due to the occurrence of fraud and errors.

On other hand, the responsibility of the auditors of Apollo minerals limited is to express

an opinion on the financial report presented and make conclusion on the review of the

management about report that is of great assistance to users in their investment decision making.

The review of the financial report has been conducted according to the auditing standard on

review engagement ASRE 2410 of the reviewing financial report. Such reviewing is done by the

independent auditors of the Apollo limited. Auditors are entitled to report if the financial report

is not prepared according to the Corporation Act, 2001 and they do not provide true and fair view

to the users (Lisic et al., 2016). As per the requirement of ASRE 2410, the auditors of Apollo

minerals should comply with the ethical requirements that are significant to the auditing of the

annual report or financial report of the company. Reviewing of the annual report requires

auditors to make enquiries of the persons who are responsible for accounting and financial

matters along with reviewing of procedures and applying analytical. A review conducted that is

considered to have lesser scope does not lead to obtaining of assurance that they would become

acquainted with the matters that are identified in the audit (Power & Gendron, 2015). According

to that, no opinions have been expressed by the auditors.

Conclusion:

The current study elucidating on determining the effectiveness of the role of auditors in

providing assurance services to the Apollo minerals limited have found that they play a

significant role in assessing the financial statements in relation to its fair and true presentation

that is free from any material misrepresentation. Several assurance services have been provided

by auditors along with some non audit services in previous financial year. However, no such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.