Comprehensive Audit, Assurance, and Compliance Report: Appen Limited

VerifiedAdded on 2020/10/23

|12

|3345

|126

Report

AI Summary

This report provides a comprehensive analysis of the audit, assurance, and compliance aspects of Appen Limited's annual report. It begins with an overview of the company and then delves into the auditor's independence declaration, exploring the services provided by KPMG, including both audit and non-audit services like employee share schemes, transfer pricing, transaction assistance, and taxation services. The report thoroughly examines auditor remuneration, comparing fees across different service categories and analyzing the percentage changes over time. Key audit matters are discussed, specifically focusing on revenue recognition and the acquisition of Leapforce Inc. and Raterlabs Inc., including the procedures followed by the auditors. Finally, the role of the audit committee is briefly addressed. The report highlights significant financial data, auditor responsibilities, and subsequent events, offering a detailed examination of the audit process and its implications for Appen Limited.

Audit, Assurance

and Compliance

and Compliance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...............................................................................................1

MAIN BODY......................................................................................................1

Overview of company .................................................................................1

Auditor independence declaration ..............................................................1

Various non- audit services provided by auditor and their nature...............2

Auditor remuneration and its comparisons..................................................3

Various Key Audit matter and procedures...................................................4

Audit committee...........................................................................................5

Audit Opinion ..............................................................................................6

Responsibilities of director's and Auditors...................................................6

Subsequent Events......................................................................................7

Material information reported by Auditor as a stakeholder..........................7

Missing Material information........................................................................7

Follow up question.......................................................................................7

CONCLUSION....................................................................................................7

REFERENCES....................................................................................................9

INTRODUCTION ...............................................................................................1

MAIN BODY......................................................................................................1

Overview of company .................................................................................1

Auditor independence declaration ..............................................................1

Various non- audit services provided by auditor and their nature...............2

Auditor remuneration and its comparisons..................................................3

Various Key Audit matter and procedures...................................................4

Audit committee...........................................................................................5

Audit Opinion ..............................................................................................6

Responsibilities of director's and Auditors...................................................6

Subsequent Events......................................................................................7

Material information reported by Auditor as a stakeholder..........................7

Missing Material information........................................................................7

Follow up question.......................................................................................7

CONCLUSION....................................................................................................7

REFERENCES....................................................................................................9

INTRODUCTION

The process of conducting an analysis on the series of activity of an

individual or within an organisation to check that these activity are

maintained and recorded in respect with appropriate guidelines, laws and

procedures is Known as auditing (Ryan and et. al., 2012.). In company

auditing plays an important role as it help them to ensure that accounts are

accurate and its finance are being used in an suitable and effective manner.

Auditing in an organisation can be internal and external process as internal

process means auditor work on mitigating risk and identifying areas which

can be improved. External process involved independent auditor who

demeanour external audit on company account to get the current position of

company.

This project includes analysis of annual report of Appen Limited to

know the significance of Auditor independence declaration and audit report

their remuneration. Various key audit matter and their procedure develop by

KPMG are discussed in this report.

MAIN BODY

Overview of company

Appen is one of the leading dataset company in Australia that listed on

Australian stock exchange. They help other companies to expand their

artificial intelligence, as company improve search engines, social media

program, various e-commerce websites, voice identification system etc.

Appen operate their business in more that 130 countries and have over 1

million of customer those work in more than 180 languages. It provide best

solution to their customers so they can respond to ever changing needs of

people (Prempeh, Twumasi and Kyeremeh, 2015). Company was established

in Chatswood Australia in 1996 now have approx 500 employee working with

them.

1

The process of conducting an analysis on the series of activity of an

individual or within an organisation to check that these activity are

maintained and recorded in respect with appropriate guidelines, laws and

procedures is Known as auditing (Ryan and et. al., 2012.). In company

auditing plays an important role as it help them to ensure that accounts are

accurate and its finance are being used in an suitable and effective manner.

Auditing in an organisation can be internal and external process as internal

process means auditor work on mitigating risk and identifying areas which

can be improved. External process involved independent auditor who

demeanour external audit on company account to get the current position of

company.

This project includes analysis of annual report of Appen Limited to

know the significance of Auditor independence declaration and audit report

their remuneration. Various key audit matter and their procedure develop by

KPMG are discussed in this report.

MAIN BODY

Overview of company

Appen is one of the leading dataset company in Australia that listed on

Australian stock exchange. They help other companies to expand their

artificial intelligence, as company improve search engines, social media

program, various e-commerce websites, voice identification system etc.

Appen operate their business in more that 130 countries and have over 1

million of customer those work in more than 180 languages. It provide best

solution to their customers so they can respond to ever changing needs of

people (Prempeh, Twumasi and Kyeremeh, 2015). Company was established

in Chatswood Australia in 1996 now have approx 500 employee working with

them.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditor independence declaration

Independence of Auditor is defined as the freedom of internal and

external auditors from all those client parties who might have financial

interest. In addition, this concepts means that auditor work is free from any

interruption from client parties and audit must be done in honest and

objective style. An audit or review of financial statements must be performed

at the end of accounting year and should be fair and free from error that

represent the actual position of company. After the audit process auditor

must declare essential information to the directors, satisfy the effect of

subdivision, certified strategy and revealing entity these must be signed by

the individual making the statement. From annual report 2017 of Appen

limited it can be seen that auditing firm KPMG has complied the

independence requirement according to the corporation act 2001 (Mills,

2012). In respect of analyse and review of financial statements of company

the KPMG group in their written statements had declares that:

There is no disputes to the auditor independence requirement that

was set out in the corporation Act 2001 with relation to the audit

conducting within company.

No contravention is related to applicable code of professional conduct

that is related to the audit process.

Various non- audit services provided by auditor and their nature.

Non-audit services are referred to those work done by auditor that is

not related with audit process or review of financial statements within

organisation. Basically auditor provide these services to the company to

increase the effectiveness and improve the performance required. KPMG is a

auditor group that has conducted and provided number of non audit services

other than audit and review of financial statements (Whitaker, 2013). Non-

audit services are transfer pricing, transaction assistance, employee share

scheme and taxation planning. All this information is gained from auditor's

independent report and declaration done by them. For providing these

2

Independence of Auditor is defined as the freedom of internal and

external auditors from all those client parties who might have financial

interest. In addition, this concepts means that auditor work is free from any

interruption from client parties and audit must be done in honest and

objective style. An audit or review of financial statements must be performed

at the end of accounting year and should be fair and free from error that

represent the actual position of company. After the audit process auditor

must declare essential information to the directors, satisfy the effect of

subdivision, certified strategy and revealing entity these must be signed by

the individual making the statement. From annual report 2017 of Appen

limited it can be seen that auditing firm KPMG has complied the

independence requirement according to the corporation act 2001 (Mills,

2012). In respect of analyse and review of financial statements of company

the KPMG group in their written statements had declares that:

There is no disputes to the auditor independence requirement that

was set out in the corporation Act 2001 with relation to the audit

conducting within company.

No contravention is related to applicable code of professional conduct

that is related to the audit process.

Various non- audit services provided by auditor and their nature.

Non-audit services are referred to those work done by auditor that is

not related with audit process or review of financial statements within

organisation. Basically auditor provide these services to the company to

increase the effectiveness and improve the performance required. KPMG is a

auditor group that has conducted and provided number of non audit services

other than audit and review of financial statements (Whitaker, 2013). Non-

audit services are transfer pricing, transaction assistance, employee share

scheme and taxation planning. All this information is gained from auditor's

independent report and declaration done by them. For providing these

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

services auditor charge certain amount from the company such as taxation

fee within Australia of about $72514 in 2017 and in overseas of about

$85793 in 2017. They also charge $153750 for other non audit services with

Australia and $42561 in overseas office in year 2017. Nature of these

services are discussed underneath:

Employee share scheme: This means employee of company has

given an option to buy company share in very low price or may be free

sometime. So group of KPMG provides this service to help Appen limited that

help in developing employee stock exchange schemes for their employee's.

Transfer pricing: It is referred to a price or value that is connected to

transfer of goods and services from one place to another, assuming that two

units are at different location but within the same company. Auditor of Appen

limited fix price for transfer of goods and services within their organisation.

Transaction assistance: This means auditor develop guideline

through which company develop effective and non time consuming activity

to face various upcoming challenges. From annual report it can be said that

this non audit service has been conducted by KPMG in Appen limited.

Taxation services: Tax services are very important for every

organisation as every company or individual has to bear tax at the end of

financial year. So Auditor in Appen limited also conduct taxation service and

facilities the work of management.

Auditor remuneration and its comparisons

Auditor remuneration is defined as the reward or payment for the work

performed by them. These are in the form of wages, salary that also includes

additional benefits like allowances, bonus, cash incentive (Knechel and

Salterio, 2016). According to the corporation Act 2001 remuneration are

those fees payable to auditor for their work done and accompanied by other

expenses that an auditor has incurred with regard to to audit of organisation

annual reports. This also includes sum of fees for non-audit services provided

by auditor. Basically the earnings of auditor are fixed in annual general

3

fee within Australia of about $72514 in 2017 and in overseas of about

$85793 in 2017. They also charge $153750 for other non audit services with

Australia and $42561 in overseas office in year 2017. Nature of these

services are discussed underneath:

Employee share scheme: This means employee of company has

given an option to buy company share in very low price or may be free

sometime. So group of KPMG provides this service to help Appen limited that

help in developing employee stock exchange schemes for their employee's.

Transfer pricing: It is referred to a price or value that is connected to

transfer of goods and services from one place to another, assuming that two

units are at different location but within the same company. Auditor of Appen

limited fix price for transfer of goods and services within their organisation.

Transaction assistance: This means auditor develop guideline

through which company develop effective and non time consuming activity

to face various upcoming challenges. From annual report it can be said that

this non audit service has been conducted by KPMG in Appen limited.

Taxation services: Tax services are very important for every

organisation as every company or individual has to bear tax at the end of

financial year. So Auditor in Appen limited also conduct taxation service and

facilities the work of management.

Auditor remuneration and its comparisons

Auditor remuneration is defined as the reward or payment for the work

performed by them. These are in the form of wages, salary that also includes

additional benefits like allowances, bonus, cash incentive (Knechel and

Salterio, 2016). According to the corporation Act 2001 remuneration are

those fees payable to auditor for their work done and accompanied by other

expenses that an auditor has incurred with regard to to audit of organisation

annual reports. This also includes sum of fees for non-audit services provided

by auditor. Basically the earnings of auditor are fixed in annual general

3

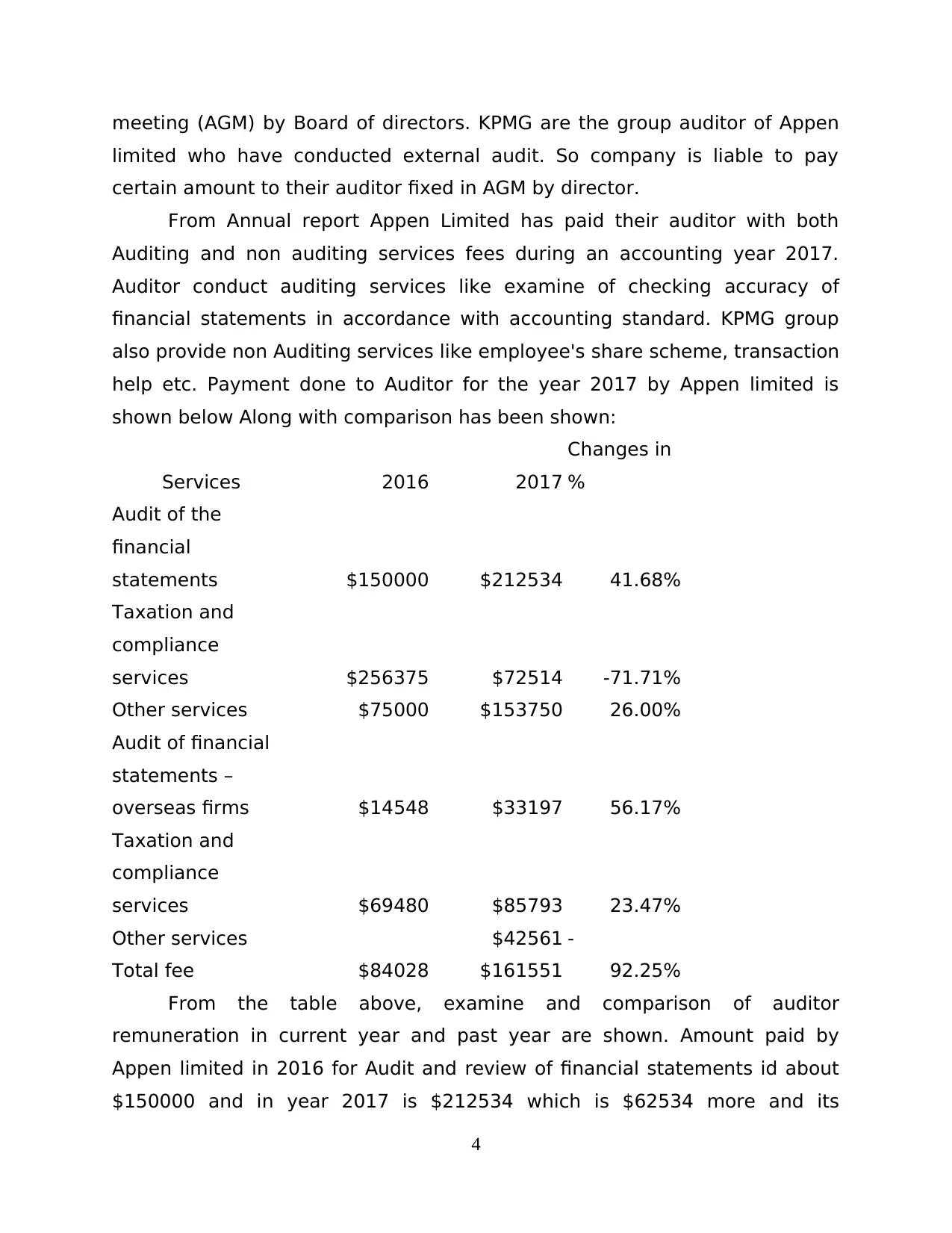

meeting (AGM) by Board of directors. KPMG are the group auditor of Appen

limited who have conducted external audit. So company is liable to pay

certain amount to their auditor fixed in AGM by director.

From Annual report Appen Limited has paid their auditor with both

Auditing and non auditing services fees during an accounting year 2017.

Auditor conduct auditing services like examine of checking accuracy of

financial statements in accordance with accounting standard. KPMG group

also provide non Auditing services like employee's share scheme, transaction

help etc. Payment done to Auditor for the year 2017 by Appen limited is

shown below Along with comparison has been shown:

Services 2016 2017

Changes in

%

Audit of the

financial

statements $150000 $212534 41.68%

Taxation and

compliance

services $256375 $72514 -71.71%

Other services $75000 $153750 26.00%

Audit of financial

statements –

overseas firms $14548 $33197 56.17%

Taxation and

compliance

services $69480 $85793 23.47%

Other services $42561 -

Total fee $84028 $161551 92.25%

From the table above, examine and comparison of auditor

remuneration in current year and past year are shown. Amount paid by

Appen limited in 2016 for Audit and review of financial statements id about

$150000 and in year 2017 is $212534 which is $62534 more and its

4

limited who have conducted external audit. So company is liable to pay

certain amount to their auditor fixed in AGM by director.

From Annual report Appen Limited has paid their auditor with both

Auditing and non auditing services fees during an accounting year 2017.

Auditor conduct auditing services like examine of checking accuracy of

financial statements in accordance with accounting standard. KPMG group

also provide non Auditing services like employee's share scheme, transaction

help etc. Payment done to Auditor for the year 2017 by Appen limited is

shown below Along with comparison has been shown:

Services 2016 2017

Changes in

%

Audit of the

financial

statements $150000 $212534 41.68%

Taxation and

compliance

services $256375 $72514 -71.71%

Other services $75000 $153750 26.00%

Audit of financial

statements –

overseas firms $14548 $33197 56.17%

Taxation and

compliance

services $69480 $85793 23.47%

Other services $42561 -

Total fee $84028 $161551 92.25%

From the table above, examine and comparison of auditor

remuneration in current year and past year are shown. Amount paid by

Appen limited in 2016 for Audit and review of financial statements id about

$150000 and in year 2017 is $212534 which is $62534 more and its

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

percentage change is about 41.68%. Amount paid as remuneration For

performing non audit services of taxation and compliance within Australia is

approx $72514 for year 2017 that is $183861 less to the amount paid during

financial year 2016. There is a drastic change in the percentage about 71.6%

that means that Appen limited has now tried to stop making payment for this

services. Amount spent on other services during year 2017 is $153750 that

is $78750 more paid in 2016. Appen limited also pay remuneration for audit

services performed by auditor in overseas firm like for Audit review $33197

in past year, $85793 for taxation and compliance services during year 2017

and for other services they pay $42561 in 2017. there percentage varies as

56.17%, 23.47% respectively.

Various Key Audit matter and procedures.

Those matter which are discussed with those related to the

governance are then calculated by the auditor then identify those matter

which required important auditor attending during the activity of the audit

process performed with an organisation are called Key audit matter. In

addition, it is defined as the professional judgements that were most

important in the audit of annual report for the current financial year

(.Fiolleau and et. al., 2013). KPMG the audit group identified two key audit

matter in context to Appen limited such as, Revenue recognition and

Acquisition of leapforce Inc and Raterlabs Inc.

Revenue Recognition: Amount of income of group is related to the

income from rendering the services, two largest revenue services

where auditor focus more is, explanation of language resources and

rendering of content connected services. This basically includes

contract accounting that relay on calculation of management like

foreseen time and price to absolute a project and tally the number of

lines is compared to the total number of lines for the whole project.

Revenue that hike up from content connected services like high bulk

5

performing non audit services of taxation and compliance within Australia is

approx $72514 for year 2017 that is $183861 less to the amount paid during

financial year 2016. There is a drastic change in the percentage about 71.6%

that means that Appen limited has now tried to stop making payment for this

services. Amount spent on other services during year 2017 is $153750 that

is $78750 more paid in 2016. Appen limited also pay remuneration for audit

services performed by auditor in overseas firm like for Audit review $33197

in past year, $85793 for taxation and compliance services during year 2017

and for other services they pay $42561 in 2017. there percentage varies as

56.17%, 23.47% respectively.

Various Key Audit matter and procedures.

Those matter which are discussed with those related to the

governance are then calculated by the auditor then identify those matter

which required important auditor attending during the activity of the audit

process performed with an organisation are called Key audit matter. In

addition, it is defined as the professional judgements that were most

important in the audit of annual report for the current financial year

(.Fiolleau and et. al., 2013). KPMG the audit group identified two key audit

matter in context to Appen limited such as, Revenue recognition and

Acquisition of leapforce Inc and Raterlabs Inc.

Revenue Recognition: Amount of income of group is related to the

income from rendering the services, two largest revenue services

where auditor focus more is, explanation of language resources and

rendering of content connected services. This basically includes

contract accounting that relay on calculation of management like

foreseen time and price to absolute a project and tally the number of

lines is compared to the total number of lines for the whole project.

Revenue that hike up from content connected services like high bulk

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of dealings with customer, that shows the effort made by them in

these revenue.

Procedures- Auditor test key control for the revenues of team process

that also includes approval of manager for sales bills and on monthly project

reporting. They also select a statistical sample of language resources that is

based on work value done in a financial year. Under this sample the perform

the comparison of time and costs budgeted with detail given by report

manager on customer project. They also re-evaluate total percentage

evolved in completion of project by agreeing the number of lines at the end

of financial year. Auditor ensure the logged performance date of customer

project work across annual period. They also help to check the accuracy of

all project in progress, check every receivables and revenue on balance

sheet form bill embossed and cash receiving from customers (Tepalagul and

Lin, 2015). KPMG performed various analytical procedure finished revenue

from language and content that is the compared to cash receipts of the year.

They also select a revenue sample dealing form months December 2017 to

January 2018 to check that revenue was recognised at the time when service

provided.

Acquisition of leapforce Inc and Raterlabs Inc- Auditor identified

this key audit matter during the year an income from relevance

service. They identify that in the financial year explanation for

business collection was a key matter in Appen limited because the

Size of dealing with other organisation and level of judgements. This

includes various key areas of functionary such as, identification of

purchase circumstance, exact value of involved assets and liabilities at

acquisition date, disclosure of transfer in final statements.

Procedure- Auditor adopts process to solve this matter as they form a

purchase agreements, key term of payment are understand. They calculate

transfer circumstance and transaction costs to make sure that these are

under criteria of accounting standard. They start testing transfer date

balance with provided documents that includes fair values at that date. They

6

these revenue.

Procedures- Auditor test key control for the revenues of team process

that also includes approval of manager for sales bills and on monthly project

reporting. They also select a statistical sample of language resources that is

based on work value done in a financial year. Under this sample the perform

the comparison of time and costs budgeted with detail given by report

manager on customer project. They also re-evaluate total percentage

evolved in completion of project by agreeing the number of lines at the end

of financial year. Auditor ensure the logged performance date of customer

project work across annual period. They also help to check the accuracy of

all project in progress, check every receivables and revenue on balance

sheet form bill embossed and cash receiving from customers (Tepalagul and

Lin, 2015). KPMG performed various analytical procedure finished revenue

from language and content that is the compared to cash receipts of the year.

They also select a revenue sample dealing form months December 2017 to

January 2018 to check that revenue was recognised at the time when service

provided.

Acquisition of leapforce Inc and Raterlabs Inc- Auditor identified

this key audit matter during the year an income from relevance

service. They identify that in the financial year explanation for

business collection was a key matter in Appen limited because the

Size of dealing with other organisation and level of judgements. This

includes various key areas of functionary such as, identification of

purchase circumstance, exact value of involved assets and liabilities at

acquisition date, disclosure of transfer in final statements.

Procedure- Auditor adopts process to solve this matter as they form a

purchase agreements, key term of payment are understand. They calculate

transfer circumstance and transaction costs to make sure that these are

under criteria of accounting standard. They start testing transfer date

balance with provided documents that includes fair values at that date. They

6

also check numerical quality of the team procedure of goodwill at the time of

transfer. Auditor also aid management in the formation of those business

combination revelation that are shown in the accounting year (Jones, 2017).

Audit committee

It is refereed to the group of individual or team member who comes

together to perform a common task like auditing within an organisation is

known as audit committee. These committee member are executive

director's and non-executive director who inspect and analyse the accuracy

and correctness of financial statements of a company. From the annual

report of it is clear that Appen limited has A chairman named Robin Low and

two supporting member Chris Vonwiller and Deena shiff those are

responsible to inspect final report.

The other Non-executive directors of the company are independent

external auditor that are not a part of Appen limited they comes form outside

to audit statements. There were six non-executive managers which are

responsible for audit work and has been paid by company accordingly. The

total amount spent by management on non-executive director during current

year 2017 is approx $70000. Main motive of this committee is to develop

audit report free from error that help the management and other investor to

know about the financial position of Appen limited.

Audit Opinion

As the process of Auditing complete within an organisation auditor

have their opinion on the report and statements provided by the company

(Audit Opinion, 2017). These opinion may be real unbiased and free from any

type of frauds that shows the result given by auditor. Auditor may give their

opinion in document form that shows the accuracy of organisation financial

statements and reporting. These documents of audit opinion are further

classified such as Adverse opinion, qualified opinion and disclaimer of

opinion.

7

transfer. Auditor also aid management in the formation of those business

combination revelation that are shown in the accounting year (Jones, 2017).

Audit committee

It is refereed to the group of individual or team member who comes

together to perform a common task like auditing within an organisation is

known as audit committee. These committee member are executive

director's and non-executive director who inspect and analyse the accuracy

and correctness of financial statements of a company. From the annual

report of it is clear that Appen limited has A chairman named Robin Low and

two supporting member Chris Vonwiller and Deena shiff those are

responsible to inspect final report.

The other Non-executive directors of the company are independent

external auditor that are not a part of Appen limited they comes form outside

to audit statements. There were six non-executive managers which are

responsible for audit work and has been paid by company accordingly. The

total amount spent by management on non-executive director during current

year 2017 is approx $70000. Main motive of this committee is to develop

audit report free from error that help the management and other investor to

know about the financial position of Appen limited.

Audit Opinion

As the process of Auditing complete within an organisation auditor

have their opinion on the report and statements provided by the company

(Audit Opinion, 2017). These opinion may be real unbiased and free from any

type of frauds that shows the result given by auditor. Auditor may give their

opinion in document form that shows the accuracy of organisation financial

statements and reporting. These documents of audit opinion are further

classified such as Adverse opinion, qualified opinion and disclaimer of

opinion.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the annual report of Appen Limited external auditor KPMG has

provided unmodified opinion. This type of opinion means that auditor has

given all the information related to the financial statements in a adequate

and befitting manner and these opinion are not required to be changed in

future. This opinion further help shareholder and other investor as the know

more about the company (Ng, Chong and Ismail, 2012). So group auditor of

Appen limited has provided their opinion in the audit report that state that all

the financial information and statements are being made by accountant in

accordance to the corporation Act 2001.

Responsibilities of director's and Auditors

Director are the main part of company who manages internal activity

and are responsible for internal control (Nicolăescu, 2013). In Appen limited

director's plays an important role some of these are described below:

They make sure that report give the actual view of financial

performance and these must be prepared in accordance to Australian

Accounting standard.

These report are maintained and prepared by effective internal control

and there must be free from error and frauds.

They also select best method for Appen limited like director decide to

follow going concern method and there is no need to change this

method and strategy.

Auditor are the one who inspect the financial report and statements and

make sure that these are formed according to standard within an

organisation. From the annual report of Appen limited different role

performed by Auditor are described underneath.

To assure that reports prepared does not have any material

information

They must ensure that all the procedures are done with fair perception

and account depicts true value

8

provided unmodified opinion. This type of opinion means that auditor has

given all the information related to the financial statements in a adequate

and befitting manner and these opinion are not required to be changed in

future. This opinion further help shareholder and other investor as the know

more about the company (Ng, Chong and Ismail, 2012). So group auditor of

Appen limited has provided their opinion in the audit report that state that all

the financial information and statements are being made by accountant in

accordance to the corporation Act 2001.

Responsibilities of director's and Auditors

Director are the main part of company who manages internal activity

and are responsible for internal control (Nicolăescu, 2013). In Appen limited

director's plays an important role some of these are described below:

They make sure that report give the actual view of financial

performance and these must be prepared in accordance to Australian

Accounting standard.

These report are maintained and prepared by effective internal control

and there must be free from error and frauds.

They also select best method for Appen limited like director decide to

follow going concern method and there is no need to change this

method and strategy.

Auditor are the one who inspect the financial report and statements and

make sure that these are formed according to standard within an

organisation. From the annual report of Appen limited different role

performed by Auditor are described underneath.

To assure that reports prepared does not have any material

information

They must ensure that all the procedures are done with fair perception

and account depicts true value

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Subsequent Events

It is refereed to those events that occur after the financial reporting

period with an organisation but may be presented in the accounting

statements of financial year are known as subsequent events. In analyses of

annual report of Appen limited it can be observed that there is only one such

type of event that is dividend declaration which is being reported after

reporting period (Sarkar and Sarkar, 2012).

Material information reported by Auditor as a stakeholder

There are shareholder, other investors and supplier those wants exact

information about the company performance and current position. From their

point of view material information from the annual reports of Appen limited

are profitable ratio, various budgets that shows the realistic position of

company.

Missing Material information

From the analyses of annual report of Appen limited there is no such

missing information related to any event happen within company (Greiner,

Kohlbeck and Smith, 2013). This state that information provided by the

auditor shows the actual performance and market standing about the

company.

Follow up question

Q1) Have accounting standard are complied and processed by Appen

limited?

Q2) All those account prepared by audit team are free from error and fraud?

Q3) Was audit committee is aware about the changes in accounting polices?

CONCLUSION

In this project report it has been concluded that audit is the most

important process for every organisation that shows the exact position about

company. From analyses of annual report of Appen limited KPMG has given

their unmodified opinion about the financial statements and various key

Audit matter are identify and they develop procedure regarding them.

9

It is refereed to those events that occur after the financial reporting

period with an organisation but may be presented in the accounting

statements of financial year are known as subsequent events. In analyses of

annual report of Appen limited it can be observed that there is only one such

type of event that is dividend declaration which is being reported after

reporting period (Sarkar and Sarkar, 2012).

Material information reported by Auditor as a stakeholder

There are shareholder, other investors and supplier those wants exact

information about the company performance and current position. From their

point of view material information from the annual reports of Appen limited

are profitable ratio, various budgets that shows the realistic position of

company.

Missing Material information

From the analyses of annual report of Appen limited there is no such

missing information related to any event happen within company (Greiner,

Kohlbeck and Smith, 2013). This state that information provided by the

auditor shows the actual performance and market standing about the

company.

Follow up question

Q1) Have accounting standard are complied and processed by Appen

limited?

Q2) All those account prepared by audit team are free from error and fraud?

Q3) Was audit committee is aware about the changes in accounting polices?

CONCLUSION

In this project report it has been concluded that audit is the most

important process for every organisation that shows the exact position about

company. From analyses of annual report of Appen limited KPMG has given

their unmodified opinion about the financial statements and various key

Audit matter are identify and they develop procedure regarding them.

9

REFERENCES

Books and Journals:

Mills, J., 2012. Quality auditing. Springer Science & Business Media.

Ryan, K., and et. al., 2012. Development of a standardised approach to

observing hand hygiene compliance in Australia. Healthcare

infection. 17(4). pp.115-121.

Prempeh, K. B., Twumasi, P. and Kyeremeh, K., 2015. Assessment of financial

control practices in Polytechnics in Ghana. A case study of Sunyani

Polytechnic.

Whitaker, S., 2013. PMP Rapid Review. Microsoft Press.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk.

Routledge.

Fiolleau, K., and et. al ., 2013. How do regulatory reforms to enhance auditor

independence work in practice?. Contemporary Accounting Research.

30(3). pp.864-890.

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A

literature review. Journal of Accounting, Auditing & Finance. 30(1).

pp.101-121.

Jones, P., 2017. Statistical sampling and risk analysis in auditing. Routledge.

Ng, T. H., Chong, L. L. and Ismail, H., 2012. Is the risk management

committee only a procedural compliance? An insight into managing

risk taking among insurance companies in Malaysia. The Journal of

Risk Finance. 14(1). pp.71-86.

Sarkar, J. and Sarkar, S., 2012. Auditor and audit committee independence in

India.

Greiner, A., Kohlbeck, M. and Smith, T., 2013. Do auditors perceive real

earnings management as a business risk?.

Nicolăescu, E., 2013. Understanding Risk Factors for Weaknesses in Internal

Controls over Financial Reporting. Journal of Self-Governance and

Management Economics. 1(3).

Online

Audit Opinion . 2017. [Online]. Available through:

<https://www.dvphilippines.com/blog/understanding-audits-the-four-

types-of-audit-reports>

10

Books and Journals:

Mills, J., 2012. Quality auditing. Springer Science & Business Media.

Ryan, K., and et. al., 2012. Development of a standardised approach to

observing hand hygiene compliance in Australia. Healthcare

infection. 17(4). pp.115-121.

Prempeh, K. B., Twumasi, P. and Kyeremeh, K., 2015. Assessment of financial

control practices in Polytechnics in Ghana. A case study of Sunyani

Polytechnic.

Whitaker, S., 2013. PMP Rapid Review. Microsoft Press.

Knechel, W. R. and Salterio, S. E., 2016. Auditing: Assurance and risk.

Routledge.

Fiolleau, K., and et. al ., 2013. How do regulatory reforms to enhance auditor

independence work in practice?. Contemporary Accounting Research.

30(3). pp.864-890.

Tepalagul, N. and Lin, L., 2015. Auditor independence and audit quality: A

literature review. Journal of Accounting, Auditing & Finance. 30(1).

pp.101-121.

Jones, P., 2017. Statistical sampling and risk analysis in auditing. Routledge.

Ng, T. H., Chong, L. L. and Ismail, H., 2012. Is the risk management

committee only a procedural compliance? An insight into managing

risk taking among insurance companies in Malaysia. The Journal of

Risk Finance. 14(1). pp.71-86.

Sarkar, J. and Sarkar, S., 2012. Auditor and audit committee independence in

India.

Greiner, A., Kohlbeck, M. and Smith, T., 2013. Do auditors perceive real

earnings management as a business risk?.

Nicolăescu, E., 2013. Understanding Risk Factors for Weaknesses in Internal

Controls over Financial Reporting. Journal of Self-Governance and

Management Economics. 1(3).

Online

Audit Opinion . 2017. [Online]. Available through:

<https://www.dvphilippines.com/blog/understanding-audits-the-four-

types-of-audit-reports>

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.