Comprehensive Accounting Analysis of Apple Inc. Financial Performance

VerifiedAdded on 2021/04/24

|12

|2532

|65

Homework Assignment

AI Summary

This document provides a detailed solution to an accounting assignment focused on analyzing Apple Inc.'s financial statements. The assignment covers key aspects of financial accounting, including the calculation and interpretation of cash flow from operating activities, and the analysis of cash and cash equivalents. It examines Apple's use of the indirect method for cash flow calculations, and analyzes changes in accounts receivable, inventories, and accounts payable. The assignment also delves into investing activities, including the purchase and sale of marketable securities. Furthermore, it addresses interest and taxes paid by Apple. Part 2 of the assignment examines Apple's common stock, including par value, authorized stock, and the percentage of authorized stock issued. It also covers common stock outstanding, stock repurchasing, and calculates financial ratios such as the payout ratio, earnings per share, and return on common stockholders' equity. The solution provides a thorough understanding of Apple's financial performance based on the provided data.

Running head: ACCOUNTING

Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to question A:................................................................................................................2

Answer to question B:................................................................................................................2

Answer to question C:................................................................................................................2

Answer to question D:................................................................................................................3

Answer to question E:................................................................................................................4

Answer to question F:................................................................................................................4

Answer to part 2:........................................................................................................................5

Answer to question 1:.................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................7

Reference List:.........................................................................................................................10

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to question A:................................................................................................................2

Answer to question B:................................................................................................................2

Answer to question C:................................................................................................................2

Answer to question D:................................................................................................................3

Answer to question E:................................................................................................................4

Answer to question F:................................................................................................................4

Answer to part 2:........................................................................................................................5

Answer to question 1:.................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to question 3:.................................................................................................................6

Answer to question 4:.................................................................................................................7

Reference List:.........................................................................................................................10

2ACCOUNTING

Answer to Part 1:

Answer to question A:

In the financial accounting the operating cash flow or in other words the cash flow

generated from the operations refers to the cash flow from the operating activities or cash

flow form the operations (Bouville, 2016). Cash flow from operating activities is referred as

the sum of cash that an organization generates from the incomes exclusive of the cash that is

related with the long term investment on the capital items.

As evident from the financial statement of the apple annual report, the present

question is based on the ascertainment of the net cash flow by the operating activities from

the cash flow statement during the year 2013 and 2014 will be stated. For Apple, INC during

the financial year ended 2013 the net cash flow from operating activities stood $53,666

million. On the other hand, taking into the considerations the net cash flow from the

operating activities during the year 2014 stood 59,713 million.

Answer to question B:

The term cash and cash equivalent comprises of the currency coins, receipts of

cheques which is yet to be deposited, reserves of petty cash, accounts of money market and

highly liquid short term investment that are having the maturity period of three months or less

during the time of purchase of treasury bills (Scott, 2015). As evident from the annual report

of the Apple 2014 it is noticed that cash and cash equivalents of stood negatively to ($415)

million. This represents that there was the decrease in the cash and cash equivalents for Apple

during the financial year of 2014.

Answer to Part 1:

Answer to question A:

In the financial accounting the operating cash flow or in other words the cash flow

generated from the operations refers to the cash flow from the operating activities or cash

flow form the operations (Bouville, 2016). Cash flow from operating activities is referred as

the sum of cash that an organization generates from the incomes exclusive of the cash that is

related with the long term investment on the capital items.

As evident from the financial statement of the apple annual report, the present

question is based on the ascertainment of the net cash flow by the operating activities from

the cash flow statement during the year 2013 and 2014 will be stated. For Apple, INC during

the financial year ended 2013 the net cash flow from operating activities stood $53,666

million. On the other hand, taking into the considerations the net cash flow from the

operating activities during the year 2014 stood 59,713 million.

Answer to question B:

The term cash and cash equivalent comprises of the currency coins, receipts of

cheques which is yet to be deposited, reserves of petty cash, accounts of money market and

highly liquid short term investment that are having the maturity period of three months or less

during the time of purchase of treasury bills (Scott, 2015). As evident from the annual report

of the Apple 2014 it is noticed that cash and cash equivalents of stood negatively to ($415)

million. This represents that there was the decrease in the cash and cash equivalents for Apple

during the financial year of 2014.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

Answer to question C:

As evident from the annual report of the Apple uses the Indirect method of calculating

the net cash flow from the operating activities. Apple uses the indirect method by adjusting

the net income for the items that does not create an impact on the cash to ascertain the net

cash flow from the operating activities (Williams, 2014). It is noteworthy to denote that a

large number of corporation makes the use of the indirect method to ascertain the net cash

flow from the operating activities. Apple favours the indirect method because of primarily

two reasons;

a. It is easy to prepare and it is less costly

b. This method helps in focusing on the differences that are formed among the net

income and net cash generated from the operating activities.

Answer to question D:

As per the annual report of the Apple Inc, cash flow statement for the year ended

September 27, 2014. Apple reported an accounts receivable of $4232 million however during

the year ended September 28 2013 the accounts receivable for apple stood 2172. An

important assertion can be bought forward by stating that the accounts receivables of apple

increased from the year ended 2013 to 2014 with total increase of $2060. Apple also reported

a total decrease in the cash receipts for the same amount of from the total of accounts

receivables increased.

Apple Inc, also reported an inventories during the financial year of September 27,

2014 to a total amount of million 76 and in the financial year 2013 September 28 inventories

totalled approximately $973 million. It can be stated that the inventories decreased from 2013

to 2014 by 897 that stood negatively on the cash flow statement representing an increase in

inventory and decrease in cash balance (Macve, 2015). Taking into the account the accounts

Answer to question C:

As evident from the annual report of the Apple uses the Indirect method of calculating

the net cash flow from the operating activities. Apple uses the indirect method by adjusting

the net income for the items that does not create an impact on the cash to ascertain the net

cash flow from the operating activities (Williams, 2014). It is noteworthy to denote that a

large number of corporation makes the use of the indirect method to ascertain the net cash

flow from the operating activities. Apple favours the indirect method because of primarily

two reasons;

a. It is easy to prepare and it is less costly

b. This method helps in focusing on the differences that are formed among the net

income and net cash generated from the operating activities.

Answer to question D:

As per the annual report of the Apple Inc, cash flow statement for the year ended

September 27, 2014. Apple reported an accounts receivable of $4232 million however during

the year ended September 28 2013 the accounts receivable for apple stood 2172. An

important assertion can be bought forward by stating that the accounts receivables of apple

increased from the year ended 2013 to 2014 with total increase of $2060. Apple also reported

a total decrease in the cash receipts for the same amount of from the total of accounts

receivables increased.

Apple Inc, also reported an inventories during the financial year of September 27,

2014 to a total amount of million 76 and in the financial year 2013 September 28 inventories

totalled approximately $973 million. It can be stated that the inventories decreased from 2013

to 2014 by 897 that stood negatively on the cash flow statement representing an increase in

inventory and decrease in cash balance (Macve, 2015). Taking into the account the accounts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

payable of Apple it increased from the year ended September 28 2013 from $2,340 to $5,938

million for the year ended September 2014. The accounts payable of the Apple has increased

by $3,598 millions this is because the Apple accounts payable increased their amount of

liabilities with decrease in their cash accounts.

Answer to question E:

For the year ended 2014 September 28 the net cash used by the investing activities for

the year ended September 2014 stood $22,579 million. There was the purchase of the

marketable securities of $217,128 representing as the highest outflow of cash. On the other

hand, the highest amount of inflow of cash in investing activities was the proceeds that were

derived from the sale of marketable securities (Trotman et al., 2015). The amount Apple

derived from the marketable securities stood $189,301. Additionally, the $18,810 million of

proceeds generated from the maturity of marketable securities is also regarded as the cash

inflow of the company.

Answer to question F:

As evident from the annual report of Apple Inc the amount of interest paid by Apple

during the financial year of 2014 September 28 stood $339 million. On the other hand, taking

into the account the annual report it is evidently noticed that Apple during the year 2014

September stood $10,026 million. The amount of interest paid and taxes paid by Apple Inc

are shown in the form of supplemental cash flow disclosure.

On a conclusive note the cash management for apple has not been on the effective this

is because the company has failed to manage its cash effectively and the figures stood

negatively for the year ended 2014. It is recommended that Apple should make use of the

cash collection system to reduce the time that is taken to collect the cash that is owed to the

payable of Apple it increased from the year ended September 28 2013 from $2,340 to $5,938

million for the year ended September 2014. The accounts payable of the Apple has increased

by $3,598 millions this is because the Apple accounts payable increased their amount of

liabilities with decrease in their cash accounts.

Answer to question E:

For the year ended 2014 September 28 the net cash used by the investing activities for

the year ended September 2014 stood $22,579 million. There was the purchase of the

marketable securities of $217,128 representing as the highest outflow of cash. On the other

hand, the highest amount of inflow of cash in investing activities was the proceeds that were

derived from the sale of marketable securities (Trotman et al., 2015). The amount Apple

derived from the marketable securities stood $189,301. Additionally, the $18,810 million of

proceeds generated from the maturity of marketable securities is also regarded as the cash

inflow of the company.

Answer to question F:

As evident from the annual report of Apple Inc the amount of interest paid by Apple

during the financial year of 2014 September 28 stood $339 million. On the other hand, taking

into the account the annual report it is evidently noticed that Apple during the year 2014

September stood $10,026 million. The amount of interest paid and taxes paid by Apple Inc

are shown in the form of supplemental cash flow disclosure.

On a conclusive note the cash management for apple has not been on the effective this

is because the company has failed to manage its cash effectively and the figures stood

negatively for the year ended 2014. It is recommended that Apple should make use of the

cash collection system to reduce the time that is taken to collect the cash that is owed to the

5ACCOUNTING

company (Smith, 2015). The cash collection attempts to decrease the length and impact of

these floats period.

company (Smith, 2015). The cash collection attempts to decrease the length and impact of

these floats period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

Answer to part 2:

Answer to question 1:

Apple has the par or stated value of the common stock of $0.00001. The value derived

is different from the market price of the stock but this represents the value which is stated on

the common stock certificate. This represents the price the shares were originally offered for

the purpose of sale. Par value is used by apple in the form of guarantee for the potential

investors which the company would not issue the shares under the par value (Fisher, 2015).

As evident from the annual report Apple has the total amount of $12,600,000,000 shares of

authorized common stock. Therefore, authorized stock can be defined as the amount of stock

which the corporation is authorized to sell as stated in the charter of the company.

Answer to question 2:

Authorized stock can be defined as the maximum number of common shares which

can issued by the company in the stated charter of the organization. The total number of

authorized shares that is recognized in the charter of the organization usually goes past the

number of shares that issued by the firm in the process of organization Initial Public Offer

(IPO). The authorized stock represents the total amount of stock that the company is

authorized to sell (Meaning, 2016). As evident from the annual report of the Apple, the

company has reported a total of 12,600,000,000 shares in the form of authorized stock. At the

end of the financial year September 2017, the total number of issued and outstanding share

for Apple stood 5,886,161,000. In order to compute the percentage of the authorized common

stock issues the total number of issued shares are divided by the total number of authorized

common stock and the same is then multiplied by 100.

Computation of Percentage of Authorized Common Stock

Particulars Amount ($)

Number of Shares issued 5866161000

Answer to part 2:

Answer to question 1:

Apple has the par or stated value of the common stock of $0.00001. The value derived

is different from the market price of the stock but this represents the value which is stated on

the common stock certificate. This represents the price the shares were originally offered for

the purpose of sale. Par value is used by apple in the form of guarantee for the potential

investors which the company would not issue the shares under the par value (Fisher, 2015).

As evident from the annual report Apple has the total amount of $12,600,000,000 shares of

authorized common stock. Therefore, authorized stock can be defined as the amount of stock

which the corporation is authorized to sell as stated in the charter of the company.

Answer to question 2:

Authorized stock can be defined as the maximum number of common shares which

can issued by the company in the stated charter of the organization. The total number of

authorized shares that is recognized in the charter of the organization usually goes past the

number of shares that issued by the firm in the process of organization Initial Public Offer

(IPO). The authorized stock represents the total amount of stock that the company is

authorized to sell (Meaning, 2016). As evident from the annual report of the Apple, the

company has reported a total of 12,600,000,000 shares in the form of authorized stock. At the

end of the financial year September 2017, the total number of issued and outstanding share

for Apple stood 5,886,161,000. In order to compute the percentage of the authorized common

stock issues the total number of issued shares are divided by the total number of authorized

common stock and the same is then multiplied by 100.

Computation of Percentage of Authorized Common Stock

Particulars Amount ($)

Number of Shares issued 5866161000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

Authorized Common Stock 12600000000

Percentage of Authorized Common Stock (%) 46.56

At the end of the financial year September 2014 it is evident from the above stated

computation that Apple has 46.56% of the authorized common stock that has been issued by

the company.

Answer to question 3:

Common stock can be defined as the one form of ownership for an organization.

Common stock enables the stakeholders to vote on the corporate issues namely the board of

directors and accepting the takeover bids. It is noteworthy to denote that the holders of the

common stock help in exercising the control by electing the board of directors and casting

their vote on the corporate policy (Gandhi & Lustig, 2015). Common stockholders are

regarded on the bottom of the priority ladder for the purpose of ownership structure. An

important assertion can be bought forward by stating that at the time of liquidation common

shareholders have the right to the company assets only after the bondholders, debtholders and

the preferred shareholders are paid in full.

As evident from the annual report of Apple for the year ended September 28, 2013 the

total number of common stock that stood outstanding are 5,866,161,000. During the financial

year of 2014 in September 2014 Apple has reported 6,294,494,000 shares of common stock

outstanding. An important assertion can be bought forward by stating that during the financial

year of 2014, the number of outstanding shares declined by 428,333,000 or 7.30%. The fall in

the share is primarily because of the repurchasing of their stock. Therefore, a conclusion can

be drawn on reviewing the cash flow statement of apple that the buyback of the stocks in

terms of amount stood $45,000 million.

Authorized Common Stock 12600000000

Percentage of Authorized Common Stock (%) 46.56

At the end of the financial year September 2014 it is evident from the above stated

computation that Apple has 46.56% of the authorized common stock that has been issued by

the company.

Answer to question 3:

Common stock can be defined as the one form of ownership for an organization.

Common stock enables the stakeholders to vote on the corporate issues namely the board of

directors and accepting the takeover bids. It is noteworthy to denote that the holders of the

common stock help in exercising the control by electing the board of directors and casting

their vote on the corporate policy (Gandhi & Lustig, 2015). Common stockholders are

regarded on the bottom of the priority ladder for the purpose of ownership structure. An

important assertion can be bought forward by stating that at the time of liquidation common

shareholders have the right to the company assets only after the bondholders, debtholders and

the preferred shareholders are paid in full.

As evident from the annual report of Apple for the year ended September 28, 2013 the

total number of common stock that stood outstanding are 5,866,161,000. During the financial

year of 2014 in September 2014 Apple has reported 6,294,494,000 shares of common stock

outstanding. An important assertion can be bought forward by stating that during the financial

year of 2014, the number of outstanding shares declined by 428,333,000 or 7.30%. The fall in

the share is primarily because of the repurchasing of their stock. Therefore, a conclusion can

be drawn on reviewing the cash flow statement of apple that the buyback of the stocks in

terms of amount stood $45,000 million.

8ACCOUNTING

Answer to question 4:

Pay-out Ratio: The organizations does not declare the overall amount of the income

either in the form of dividend to its common stockholders. Apple retains some portion of their

reserve with them so that the company can finance for their future business requirements as

the expansion of the capacity or acquiring of other firms. The dividend pay-out ratio is used

to measure the percentage of net income which the company has distributed in the form of

dividend to its stakeholders (Cremers et al., 2017). The ratio represents the percentage of net

income which the company aims to retain in order to finance its business requirements along

with the percentage of net income distributed in the form of dividend.

Calculation of Pay-out Ratio

Particulars Amount ($)

Total Dividend Declared 11,125

Net Income 39510

Payout Ratio 28.16%

As evident from the above stated computations Apple has declared and distributed the

dividend of 28.39% of its net income as dividend to its shareholders.

Earnings Per Share:

The earnings per share represents the share of business’s income that is allotted to

each of the outstanding share of common stock. The earnings per share also represents the net

income per share. This ratio explains the amount the stakeholders would be getting given the

entire amount of net income is distributed in the form of dividend to its stockholders. It is

computed from the profitability of the organization on the basis of the shareholders. To

compute the earnings per share the net income of the company is divided by the number of

weighted common stock outstanding.

Answer to question 4:

Pay-out Ratio: The organizations does not declare the overall amount of the income

either in the form of dividend to its common stockholders. Apple retains some portion of their

reserve with them so that the company can finance for their future business requirements as

the expansion of the capacity or acquiring of other firms. The dividend pay-out ratio is used

to measure the percentage of net income which the company has distributed in the form of

dividend to its stakeholders (Cremers et al., 2017). The ratio represents the percentage of net

income which the company aims to retain in order to finance its business requirements along

with the percentage of net income distributed in the form of dividend.

Calculation of Pay-out Ratio

Particulars Amount ($)

Total Dividend Declared 11,125

Net Income 39510

Payout Ratio 28.16%

As evident from the above stated computations Apple has declared and distributed the

dividend of 28.39% of its net income as dividend to its shareholders.

Earnings Per Share:

The earnings per share represents the share of business’s income that is allotted to

each of the outstanding share of common stock. The earnings per share also represents the net

income per share. This ratio explains the amount the stakeholders would be getting given the

entire amount of net income is distributed in the form of dividend to its stockholders. It is

computed from the profitability of the organization on the basis of the shareholders. To

compute the earnings per share the net income of the company is divided by the number of

weighted common stock outstanding.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

Computation of Earnings Per Share

Particulars Amount ($)

Net Income 39510

Weighted Common stock outstanding 6086

Earnings per share 6.49

As evident from the above stated computations the earnings per share of the Apple Inc

stood $6.49 per share given that all the earnings per share of the company is distributed

among the shareholders as dividend. An assertion can be bought forward by stating that the

earnings per share of the company stood relatively higher than the other firms.

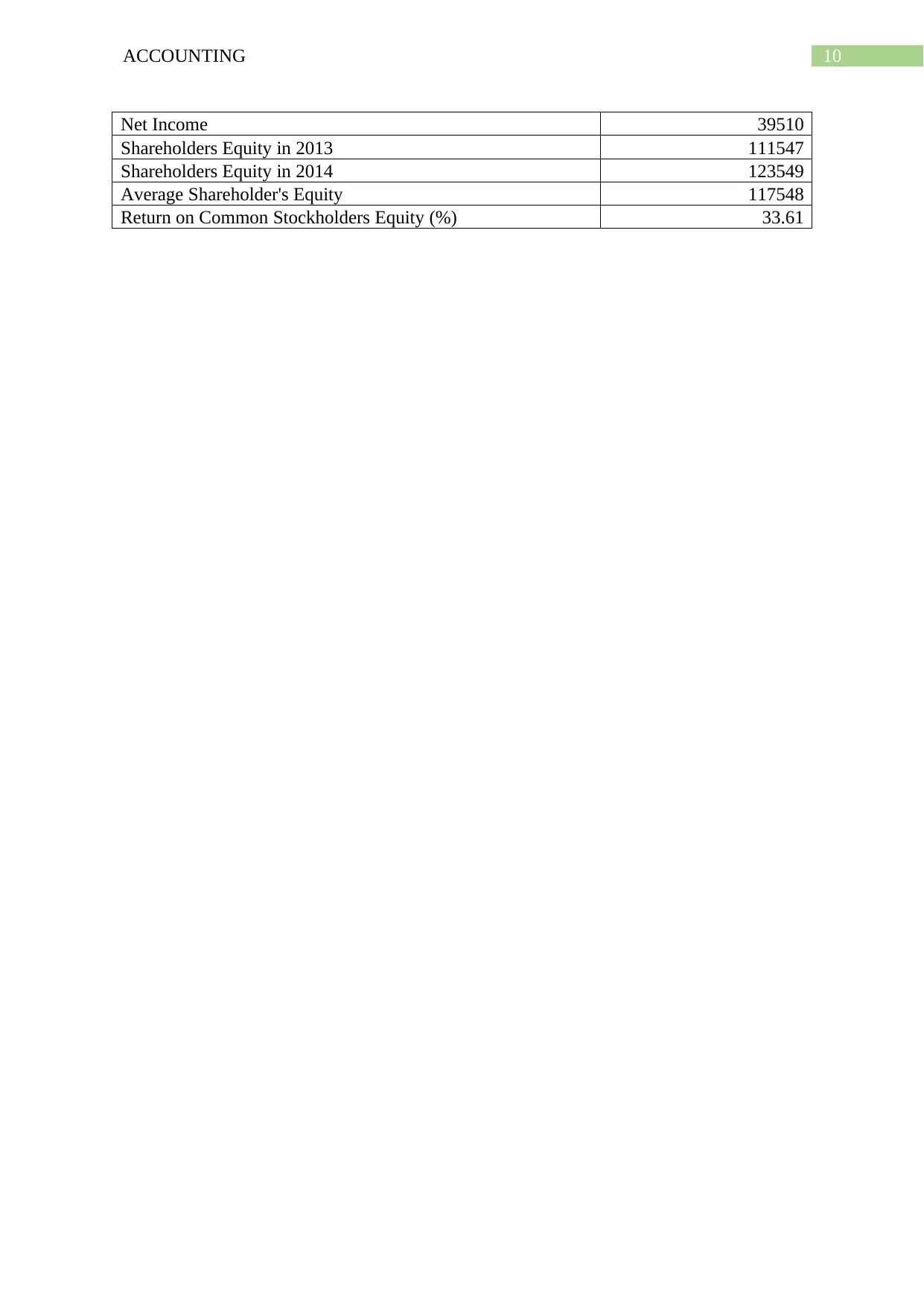

Return on Common Stockholders’ Equity:

The return on common stockholder’s equity ratio refers to the measurement of the

organization success in deriving the net income for the benefit of the common shareholders

(Cremers et al., 2017). The shareholders are calculated by dividing the net income that is

accessible to the common stockholders by common stockholder’s equity. The ratio is

generally computed in the form of percentage.

As evident from the above stated computations the common stockholder’s equity

arrives at 33.61% that indicates Apple has used its shareholder’s wealth in an effective

manner.

Conclusion:

On a conclusive note the computation provides an in-depth understanding of the

Apple company’s financial health. It represents that the organization has managed its assets

and resources effectively. The investors in the upcoming years can use this information to

undertake their decisions.

Computation of Common stockholders

Particulars Amount ($) million

Computation of Earnings Per Share

Particulars Amount ($)

Net Income 39510

Weighted Common stock outstanding 6086

Earnings per share 6.49

As evident from the above stated computations the earnings per share of the Apple Inc

stood $6.49 per share given that all the earnings per share of the company is distributed

among the shareholders as dividend. An assertion can be bought forward by stating that the

earnings per share of the company stood relatively higher than the other firms.

Return on Common Stockholders’ Equity:

The return on common stockholder’s equity ratio refers to the measurement of the

organization success in deriving the net income for the benefit of the common shareholders

(Cremers et al., 2017). The shareholders are calculated by dividing the net income that is

accessible to the common stockholders by common stockholder’s equity. The ratio is

generally computed in the form of percentage.

As evident from the above stated computations the common stockholder’s equity

arrives at 33.61% that indicates Apple has used its shareholder’s wealth in an effective

manner.

Conclusion:

On a conclusive note the computation provides an in-depth understanding of the

Apple company’s financial health. It represents that the organization has managed its assets

and resources effectively. The investors in the upcoming years can use this information to

undertake their decisions.

Computation of Common stockholders

Particulars Amount ($) million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

Net Income 39510

Shareholders Equity in 2013 111547

Shareholders Equity in 2014 123549

Average Shareholder's Equity 117548

Return on Common Stockholders Equity (%) 33.61

Net Income 39510

Shareholders Equity in 2013 111547

Shareholders Equity in 2014 123549

Average Shareholder's Equity 117548

Return on Common Stockholders Equity (%) 33.61

11ACCOUNTING

Reference List:

Bouville, M. (2016). When investing in stocks, the long term starts at three decades.

Cremers, M., Pareek, A., & Sautner, Z. (2017). Short-term investors, long-term investments,

and firm value.

Fisher, P. A. (2015). Common stocks and uncommon profits and other writings (Vol. 44).

John Wiley & Sons.

Gandhi, P., & Lustig, H. (2015). Size anomalies in US bank stock returns. The Journal of

Finance, 70(2), 733-768.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Meaning, C. (2016). Securities regulation. Stat, 8(1118), 1.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Smith, E. L. (2015). Common stocks as long term investments. Pickle Partners Publishing.

Trotman, K., Carson, E., & Gibbins, M. (2015). Financial accounting: an integrated

approach. Cengage Australia.

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

Reference List:

Bouville, M. (2016). When investing in stocks, the long term starts at three decades.

Cremers, M., Pareek, A., & Sautner, Z. (2017). Short-term investors, long-term investments,

and firm value.

Fisher, P. A. (2015). Common stocks and uncommon profits and other writings (Vol. 44).

John Wiley & Sons.

Gandhi, P., & Lustig, H. (2015). Size anomalies in US bank stock returns. The Journal of

Finance, 70(2), 733-768.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Meaning, C. (2016). Securities regulation. Stat, 8(1118), 1.

Scott, W. R. (2015). Financial accounting theory (Vol. 2, No. 0, p. 0). Prentice Hall.

Smith, E. L. (2015). Common stocks as long term investments. Pickle Partners Publishing.

Trotman, K., Carson, E., & Gibbins, M. (2015). Financial accounting: an integrated

approach. Cengage Australia.

Williams, J. (2014). Financial accounting. McGraw-Hill Higher Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.