Analyzing Islamic Financial Instruments for Small Medium Enterprises

VerifiedAdded on 2020/02/14

|18

|4605

|86

Report

AI Summary

This report provides a comprehensive analysis of the applications of Islamic financial instruments within the Small and Medium Enterprise (SME) sector. It explores the concepts of Musharakah and Mudarabah, detailing their structures and benefits for SMEs in raising capital and managing business operations. The report also examines the role of Waqf in providing financial assistance to SMEs, particularly those excluded by conventional financial institutions, and how Zakat can contribute to SME development. Furthermore, it investigates the potential of microfinance within the Islamic framework to encourage SME growth, the role of Islamic joint capital ventures, and contrasts Islamic financing methods with conventional lending practices. The report also includes an evaluation of initiatives in the GCC and Malaysia to foster SME development, concluding with recommendations to enhance the role of Islamic finance in the sustainable growth of SMEs.

Applications of Islamic Instruments in

the Financial Industry

the Financial Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................1

Introduction to SMEs and its importance to any economy..........................................................1

SMEs using Musharakah.............................................................................................................2

SMEs using Mudarabah...............................................................................................................3

How can Waqf Money be used in helping SMEs........................................................................5

The Role zakat can play in SMEs................................................................................................7

Analyse how Islamic finance can use the concept of micro Finance to encourage SMEs..........8

How Islamic joint capital venture could be the way forward in Islamic investment..................8

How Islamic Financing (Musharakah and Mudarabah contracts) differ from conventional

Lending........................................................................................................................................9

Evaluate the effort in the GCC and Malaysia to encourage SME’s development.....................10

Conclusion & Recommendations..................................................................................................12

References......................................................................................................................................14

Introduction......................................................................................................................................1

Introduction to SMEs and its importance to any economy..........................................................1

SMEs using Musharakah.............................................................................................................2

SMEs using Mudarabah...............................................................................................................3

How can Waqf Money be used in helping SMEs........................................................................5

The Role zakat can play in SMEs................................................................................................7

Analyse how Islamic finance can use the concept of micro Finance to encourage SMEs..........8

How Islamic joint capital venture could be the way forward in Islamic investment..................8

How Islamic Financing (Musharakah and Mudarabah contracts) differ from conventional

Lending........................................................................................................................................9

Evaluate the effort in the GCC and Malaysia to encourage SME’s development.....................10

Conclusion & Recommendations..................................................................................................12

References......................................................................................................................................14

LIST OF FIGURES

Figure 1: Simple Mudarabah Structure............................................................................................4

Figure 2: Waqf Financing Model....................................................................................................6

Figure 3: Anchor Companies and the number of Vendors under the VDP...................................11

Figure 4: Local vendors doing business with Japanese firms........................................................12

Figure 1: Simple Mudarabah Structure............................................................................................4

Figure 2: Waqf Financing Model....................................................................................................6

Figure 3: Anchor Companies and the number of Vendors under the VDP...................................11

Figure 4: Local vendors doing business with Japanese firms........................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the present era, small medium enterprises play significant role in creating employment

as well as enhancing the growth of gross domestic products in a developing country. However, in

order to grow and positively contribute towards the economy, SMEs face various constraints

(Jaffar and Musa, 2013). In this, one of the major constraints faced by small medium enterprises

is lack of finance. Herein, to resolve such constraints Islamic financing portfolios provides great

deal of assistance to the entrepreneurs operating in developing nations like Mena (Middle East

and North Africa).

In the present research project, investigator focuses on various aspects about Islamic

financing that assist SMEs to enhance their business operations and generate higher employment

opportunities for the nation. Furthermore, concept of Musharakah and Mudarabah has been

focused on and the role Zakat plays in SMEs. Thereafter, researcher illustrates the concept of

micro finance to encourage SMEs. Lastly, efforts in the GCC and Malaysia to encourage the

development of small medium enterprise. On the basis of whole study, recommendations to

improve the existing role Islamic finance in the sustainable development of small and medium

enterprises.

Introduction to SMEs and its importance to any economy

In general, small medium enterprises are highly recognized as the engines of economic

growth and the key contributor to the sustainable gross domestic producer (GDP) around the

globe. However, SMEs mainly operates under the manufacturing and service sectors which

encourages the employment opportunities for both skills and unskilled personnel’s. In recent

time, it has been identified that, market conditions and regulatory environment are not in support

to the growth of SMEs and access to formal finance which is one of the major obstacle or

hindrance that companies operating at small level faces (Aris and et.al, 2012). Furthermore, the

SME sector forms the backbone of economic development, private sector employment, capital

investment and GDP growth. Despite of their great importance to developing economy, SMEs

face major concerns regarding inadequacy of funds or lack of access to other banking services.

However, this is the only major reason due to which companies operating at small scale level

tend to concentrate on less capital intensive sectors like retail and wholesale trade. By the means

1

In the present era, small medium enterprises play significant role in creating employment

as well as enhancing the growth of gross domestic products in a developing country. However, in

order to grow and positively contribute towards the economy, SMEs face various constraints

(Jaffar and Musa, 2013). In this, one of the major constraints faced by small medium enterprises

is lack of finance. Herein, to resolve such constraints Islamic financing portfolios provides great

deal of assistance to the entrepreneurs operating in developing nations like Mena (Middle East

and North Africa).

In the present research project, investigator focuses on various aspects about Islamic

financing that assist SMEs to enhance their business operations and generate higher employment

opportunities for the nation. Furthermore, concept of Musharakah and Mudarabah has been

focused on and the role Zakat plays in SMEs. Thereafter, researcher illustrates the concept of

micro finance to encourage SMEs. Lastly, efforts in the GCC and Malaysia to encourage the

development of small medium enterprise. On the basis of whole study, recommendations to

improve the existing role Islamic finance in the sustainable development of small and medium

enterprises.

Introduction to SMEs and its importance to any economy

In general, small medium enterprises are highly recognized as the engines of economic

growth and the key contributor to the sustainable gross domestic producer (GDP) around the

globe. However, SMEs mainly operates under the manufacturing and service sectors which

encourages the employment opportunities for both skills and unskilled personnel’s. In recent

time, it has been identified that, market conditions and regulatory environment are not in support

to the growth of SMEs and access to formal finance which is one of the major obstacle or

hindrance that companies operating at small level faces (Aris and et.al, 2012). Furthermore, the

SME sector forms the backbone of economic development, private sector employment, capital

investment and GDP growth. Despite of their great importance to developing economy, SMEs

face major concerns regarding inadequacy of funds or lack of access to other banking services.

However, this is the only major reason due to which companies operating at small scale level

tend to concentrate on less capital intensive sectors like retail and wholesale trade. By the means

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

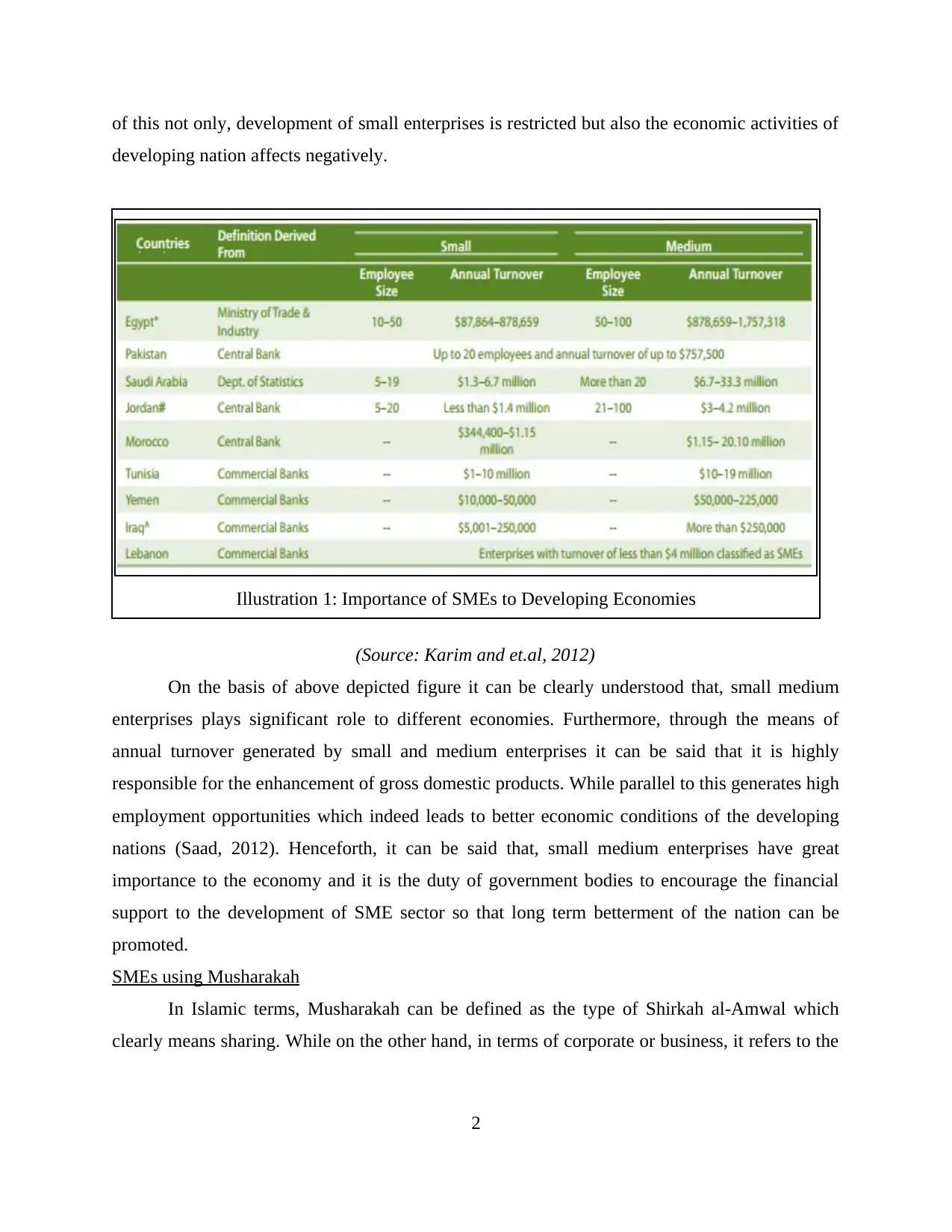

of this not only, development of small enterprises is restricted but also the economic activities of

developing nation affects negatively.

(Source: Karim and et.al, 2012)

On the basis of above depicted figure it can be clearly understood that, small medium

enterprises plays significant role to different economies. Furthermore, through the means of

annual turnover generated by small and medium enterprises it can be said that it is highly

responsible for the enhancement of gross domestic products. While parallel to this generates high

employment opportunities which indeed leads to better economic conditions of the developing

nations (Saad, 2012). Henceforth, it can be said that, small medium enterprises have great

importance to the economy and it is the duty of government bodies to encourage the financial

support to the development of SME sector so that long term betterment of the nation can be

promoted.

SMEs using Musharakah

In Islamic terms, Musharakah can be defined as the type of Shirkah al-Amwal which

clearly means sharing. While on the other hand, in terms of corporate or business, it refers to the

2

Illustration 1: Importance of SMEs to Developing Economies

developing nation affects negatively.

(Source: Karim and et.al, 2012)

On the basis of above depicted figure it can be clearly understood that, small medium

enterprises plays significant role to different economies. Furthermore, through the means of

annual turnover generated by small and medium enterprises it can be said that it is highly

responsible for the enhancement of gross domestic products. While parallel to this generates high

employment opportunities which indeed leads to better economic conditions of the developing

nations (Saad, 2012). Henceforth, it can be said that, small medium enterprises have great

importance to the economy and it is the duty of government bodies to encourage the financial

support to the development of SME sector so that long term betterment of the nation can be

promoted.

SMEs using Musharakah

In Islamic terms, Musharakah can be defined as the type of Shirkah al-Amwal which

clearly means sharing. While on the other hand, in terms of corporate or business, it refers to the

2

Illustration 1: Importance of SMEs to Developing Economies

joint venture between enterprises which shares the profit and loss of the business functioning.

Furthermore, Shirkah is divided into two kinds such as: Shirkat-ul-Milk: In general, it can be defined as the joint property of two or more person

in a property. However, the existence of Shirkah comes in two different ways: into the

operations at the options of the parties and it comes into operation automatically without

any action taken by the parties (Abozaid, 2014).

Shirkat-ul-Aqd: This is considered as the second type of Shirkah which means a

partnership effected by a mutual concept. Further it is divided into three kinds: Shirkat-

ul- Amwal, Shirkat-ul-A'mal and Shirkat-ul-wujooh. However, all these modes of sharing

or partnership are termed as Shirkah in the Islamic Fiqh.

In terms of using Musharakah as the source of finance for the small medium enterprise it

can be said that, owner or entrepreneur in order to raise the fund has to either collaborate with

big brand name or the can introduce friends or family member as the partners with equal profit

and loss sharing. However, the normal principle of Musharakah is that every partner has a right

to take part in its management process so that decisions can be made collectively. According to

Islamic financing, this is one of the major source of finance that, SMEs of developing countries

uses to raise the capital and carry out the activities (Ilias, 2012).

Furthermore, small medium companies has to follow certain rules and stipulations in

order to carry out business through the means of Musharakah contract. These are as follows: Distribution of Profit: The proportion of the profit must be decided at the time of

commencing the contract. However, in this if proportion is not decided at the initial stage

of contract than contract is not valid in Shari'ah. Ration of Profit: According to the Islamic jurists, it is necessary for the validity of

Musharakah that each partner gets the profit exactly in the proportion of his investment.

Thus, companies operating with Islamic financing and using Musharakah as the source

of raising funds.

Sharing of Loss: In case of the loss, SMEs using Musharakah should bear the loss

according to the ratio of investment. Therefore, as per Islamic financing pundits, ratio of

share of a partner in profit and loss both must be as per the investment made by the

partners (Ashoor, 2014).

3

Furthermore, Shirkah is divided into two kinds such as: Shirkat-ul-Milk: In general, it can be defined as the joint property of two or more person

in a property. However, the existence of Shirkah comes in two different ways: into the

operations at the options of the parties and it comes into operation automatically without

any action taken by the parties (Abozaid, 2014).

Shirkat-ul-Aqd: This is considered as the second type of Shirkah which means a

partnership effected by a mutual concept. Further it is divided into three kinds: Shirkat-

ul- Amwal, Shirkat-ul-A'mal and Shirkat-ul-wujooh. However, all these modes of sharing

or partnership are termed as Shirkah in the Islamic Fiqh.

In terms of using Musharakah as the source of finance for the small medium enterprise it

can be said that, owner or entrepreneur in order to raise the fund has to either collaborate with

big brand name or the can introduce friends or family member as the partners with equal profit

and loss sharing. However, the normal principle of Musharakah is that every partner has a right

to take part in its management process so that decisions can be made collectively. According to

Islamic financing, this is one of the major source of finance that, SMEs of developing countries

uses to raise the capital and carry out the activities (Ilias, 2012).

Furthermore, small medium companies has to follow certain rules and stipulations in

order to carry out business through the means of Musharakah contract. These are as follows: Distribution of Profit: The proportion of the profit must be decided at the time of

commencing the contract. However, in this if proportion is not decided at the initial stage

of contract than contract is not valid in Shari'ah. Ration of Profit: According to the Islamic jurists, it is necessary for the validity of

Musharakah that each partner gets the profit exactly in the proportion of his investment.

Thus, companies operating with Islamic financing and using Musharakah as the source

of raising funds.

Sharing of Loss: In case of the loss, SMEs using Musharakah should bear the loss

according to the ratio of investment. Therefore, as per Islamic financing pundits, ratio of

share of a partner in profit and loss both must be as per the investment made by the

partners (Ashoor, 2014).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

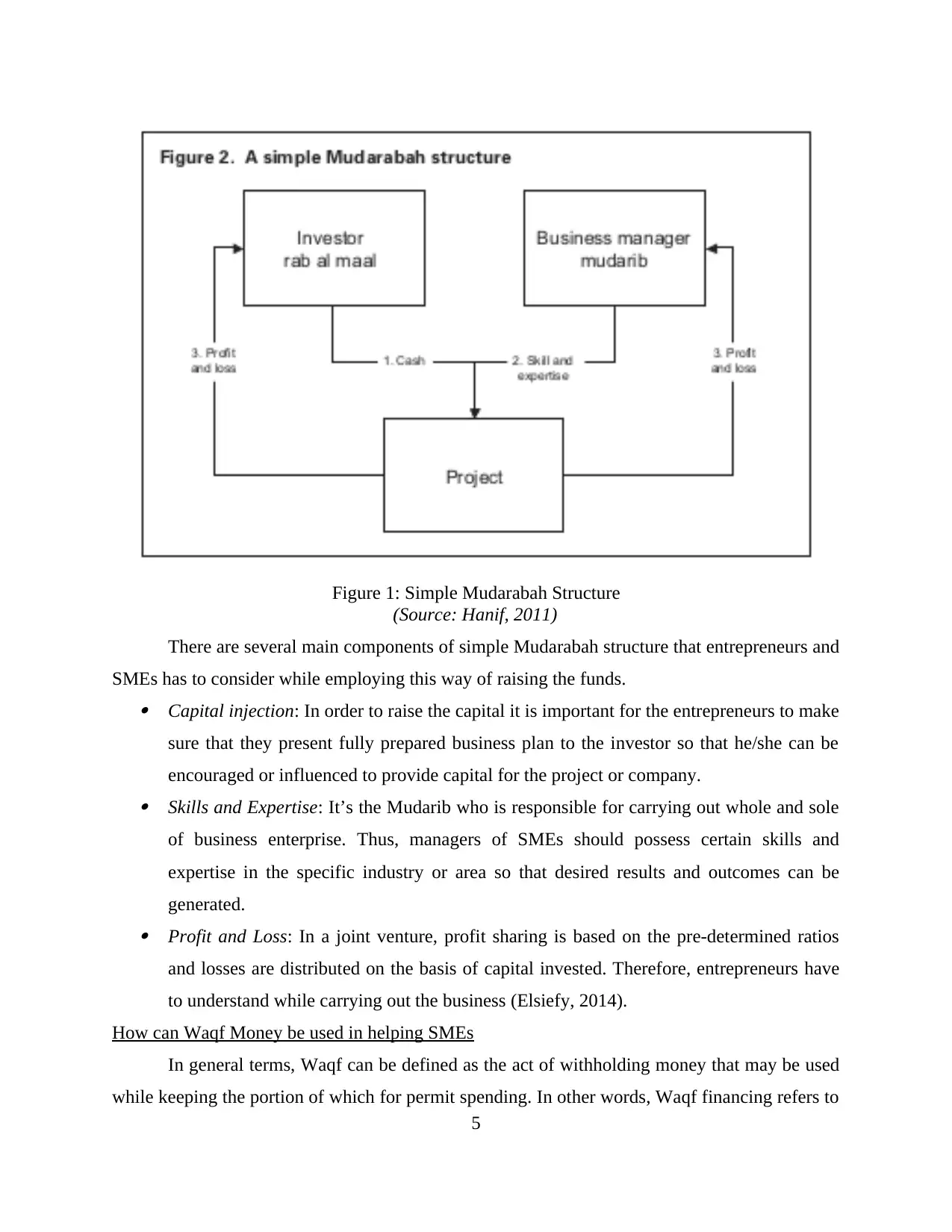

SMEs using Mudarabah

In general, Mudarabah can defined as the kind of partnership where one partner gives

money to another for investing it in a commercial enterprise. However, the investment comes

from the first partner is defined as the rabb-ul-mal, while the management and operations is an

exclusive responsibility of the other who is called mudarib. In simple terms, it is a passive

partnership in which one contributes capital and other contributes skills and expertise (Karikomi,

1998).

However, SMEs can also use this as the source of raising the funds for either initiating a

business enterprise or expanding the operations for future growth and sustainability.

Furthermore, in this, financial institution or bank (rabb-ul-mal) is responsible for providing the

funds while on the other hand, client or entrepreneur (Mudarib) is responsible for managing the

activities of business enterprise. However, the small enterprises using this source has the full

authority of making use of funds raised through financial institution because they are authorized

to interfere into the day to day functioning of the business. The structure that SMEs has to abide

is as follows:

4

In general, Mudarabah can defined as the kind of partnership where one partner gives

money to another for investing it in a commercial enterprise. However, the investment comes

from the first partner is defined as the rabb-ul-mal, while the management and operations is an

exclusive responsibility of the other who is called mudarib. In simple terms, it is a passive

partnership in which one contributes capital and other contributes skills and expertise (Karikomi,

1998).

However, SMEs can also use this as the source of raising the funds for either initiating a

business enterprise or expanding the operations for future growth and sustainability.

Furthermore, in this, financial institution or bank (rabb-ul-mal) is responsible for providing the

funds while on the other hand, client or entrepreneur (Mudarib) is responsible for managing the

activities of business enterprise. However, the small enterprises using this source has the full

authority of making use of funds raised through financial institution because they are authorized

to interfere into the day to day functioning of the business. The structure that SMEs has to abide

is as follows:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: Hanif, 2011)

There are several main components of simple Mudarabah structure that entrepreneurs and

SMEs has to consider while employing this way of raising the funds. Capital injection: In order to raise the capital it is important for the entrepreneurs to make

sure that they present fully prepared business plan to the investor so that he/she can be

encouraged or influenced to provide capital for the project or company. Skills and Expertise: It’s the Mudarib who is responsible for carrying out whole and sole

of business enterprise. Thus, managers of SMEs should possess certain skills and

expertise in the specific industry or area so that desired results and outcomes can be

generated. Profit and Loss: In a joint venture, profit sharing is based on the pre-determined ratios

and losses are distributed on the basis of capital invested. Therefore, entrepreneurs have

to understand while carrying out the business (Elsiefy, 2014).

How can Waqf Money be used in helping SMEs

In general terms, Waqf can be defined as the act of withholding money that may be used

while keeping the portion of which for permit spending. In other words, Waqf financing refers to

5

Figure 1: Simple Mudarabah Structure

There are several main components of simple Mudarabah structure that entrepreneurs and

SMEs has to consider while employing this way of raising the funds. Capital injection: In order to raise the capital it is important for the entrepreneurs to make

sure that they present fully prepared business plan to the investor so that he/she can be

encouraged or influenced to provide capital for the project or company. Skills and Expertise: It’s the Mudarib who is responsible for carrying out whole and sole

of business enterprise. Thus, managers of SMEs should possess certain skills and

expertise in the specific industry or area so that desired results and outcomes can be

generated. Profit and Loss: In a joint venture, profit sharing is based on the pre-determined ratios

and losses are distributed on the basis of capital invested. Therefore, entrepreneurs have

to understand while carrying out the business (Elsiefy, 2014).

How can Waqf Money be used in helping SMEs

In general terms, Waqf can be defined as the act of withholding money that may be used

while keeping the portion of which for permit spending. In other words, Waqf financing refers to

5

Figure 1: Simple Mudarabah Structure

looking after those enterprises who are not looked after by the market, as well as who cannot

play with economic forces or cannot exploit the economic opportunities available to them.

However, the main purpose of Waqf is to provide financial help of Muslim small enterprises so

that they can carry out their business enterprise in effective and efficient manner.

The Waqf based model of financing consist of two principal objectives on the basis of

which overall financing process of Muslim small business enterprise is based:

Firstly, Waqf financing is provided to those entrepreneurs who refuse to partake in

conventional finance which is based on interest. However, it is because interest based

financing is contravention of Quranic teachings (JOGERAN, 2010).

Secondly, Waqf financing is provided to poorer segments of society which is ignored by

the conventional financial institution with access to finance.

Furthermore, Waqf financing is based on model on the basis of researcher is able to

understand the whole concept as well as illustrate who this type of financing is helpful for the

Muslim small business enterprise (Hasan, 2013).

6

play with economic forces or cannot exploit the economic opportunities available to them.

However, the main purpose of Waqf is to provide financial help of Muslim small enterprises so

that they can carry out their business enterprise in effective and efficient manner.

The Waqf based model of financing consist of two principal objectives on the basis of

which overall financing process of Muslim small business enterprise is based:

Firstly, Waqf financing is provided to those entrepreneurs who refuse to partake in

conventional finance which is based on interest. However, it is because interest based

financing is contravention of Quranic teachings (JOGERAN, 2010).

Secondly, Waqf financing is provided to poorer segments of society which is ignored by

the conventional financial institution with access to finance.

Furthermore, Waqf financing is based on model on the basis of researcher is able to

understand the whole concept as well as illustrate who this type of financing is helpful for the

Muslim small business enterprise (Hasan, 2013).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

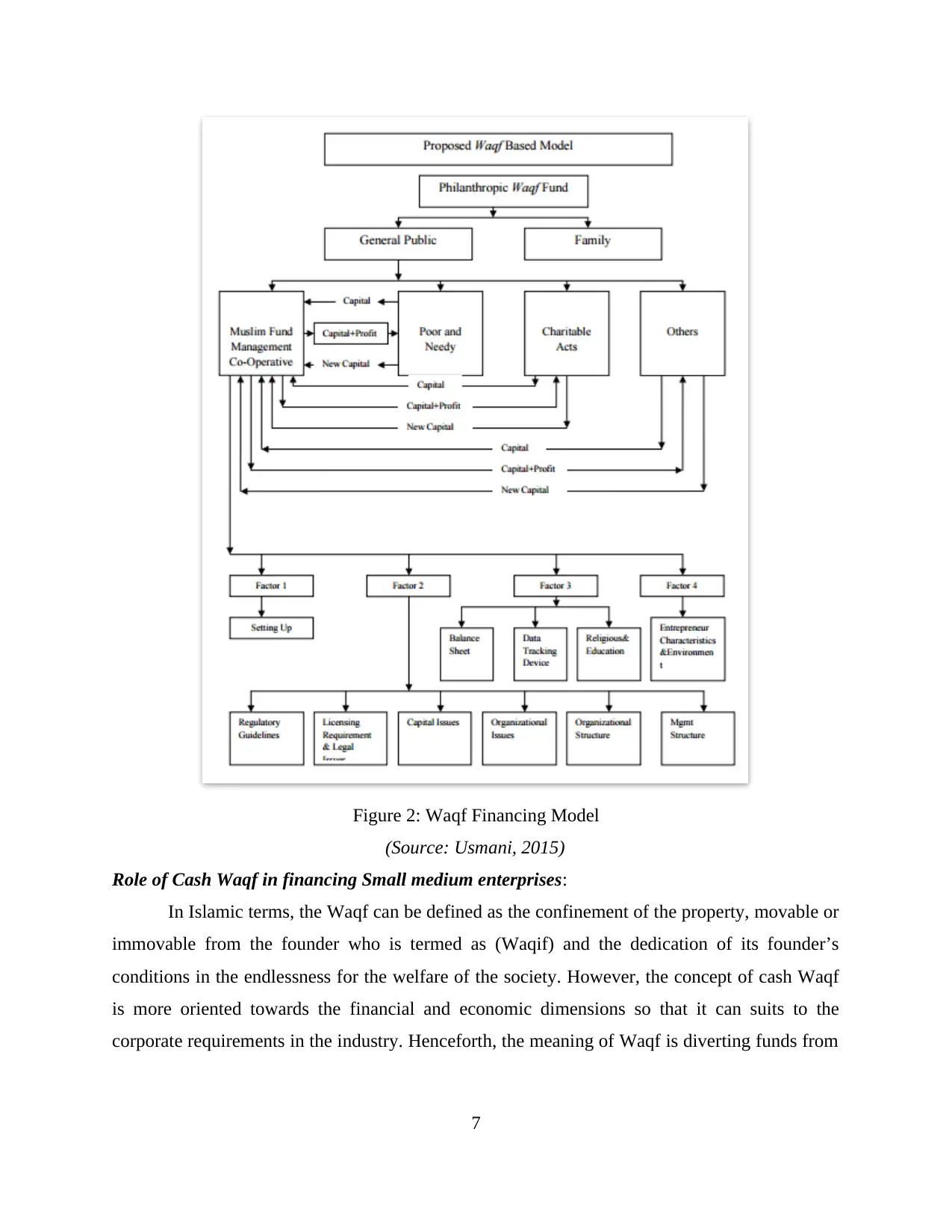

Figure 2: Waqf Financing Model

(Source: Usmani, 2015)

Role of Cash Waqf in financing Small medium enterprises:

In Islamic terms, the Waqf can be defined as the confinement of the property, movable or

immovable from the founder who is termed as (Waqif) and the dedication of its founder’s

conditions in the endlessness for the welfare of the society. However, the concept of cash Waqf

is more oriented towards the financial and economic dimensions so that it can suits to the

corporate requirements in the industry. Henceforth, the meaning of Waqf is diverting funds from

7

(Source: Usmani, 2015)

Role of Cash Waqf in financing Small medium enterprises:

In Islamic terms, the Waqf can be defined as the confinement of the property, movable or

immovable from the founder who is termed as (Waqif) and the dedication of its founder’s

conditions in the endlessness for the welfare of the society. However, the concept of cash Waqf

is more oriented towards the financial and economic dimensions so that it can suits to the

corporate requirements in the industry. Henceforth, the meaning of Waqf is diverting funds from

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the consumptions and investing them into fruitful and productive assets that assist in providing

suitable returns.

In addition to it, Waqf with its commercial and economic aspects is beneficial for the

SMEs and for the societies at the macroeconomic level (Abozaid, 2014). Furthermore, cash

endowment creates great opportunities for the Muslim small medium enterprises by getting

financial rewards and profit which can be used to satisfy their different needs and wants. There

are several benefits of Waqf for the SMEs:

It enhances the market by increasing level of business operations.

It enhances the domestic economic by offering liquidity to the SME sector.

Providing the adequate source of financing.

Constantly circulating the fund within the small scale business industry.

Developing better employment opportunities.

The Role zakat can play in SMEs

Zakat in Islamic terms can be defined as the act of faith carried out the Muslims to purify

themselves and in order to do so entrepreneurs share some of their wealth in the form of religious

tax for the betterment of needy people. Furthermore, all the listed companies are eligible to

perform their zakat on enterprise according to the annual profit gained. Considering the example

of Malacca which comprises of six business category named as manufacturing sector, retail

sector, community, social and other private sectors, restaurants, hotel and construction sector.

According to the report made by Pusat Zakat Malacca Zakah Collection report 2008-09, it can be

said that, only 40.54% of SMEs enterprises in the cited location are successfully contributing

their Zakat (Jaffar and Musa, 2013).

Year Agencies Reported

Agencies

Agencies that

comply Zakah

on business

Percentage

2009 Micro, Small

and Medium

Enterprises

698 283 40.54%

However, the contribution rate of Zakah on business is only 2.5% which is considered as

the very small amount of the total wealth of the business but still only 40.54% of SMEs in

8

suitable returns.

In addition to it, Waqf with its commercial and economic aspects is beneficial for the

SMEs and for the societies at the macroeconomic level (Abozaid, 2014). Furthermore, cash

endowment creates great opportunities for the Muslim small medium enterprises by getting

financial rewards and profit which can be used to satisfy their different needs and wants. There

are several benefits of Waqf for the SMEs:

It enhances the market by increasing level of business operations.

It enhances the domestic economic by offering liquidity to the SME sector.

Providing the adequate source of financing.

Constantly circulating the fund within the small scale business industry.

Developing better employment opportunities.

The Role zakat can play in SMEs

Zakat in Islamic terms can be defined as the act of faith carried out the Muslims to purify

themselves and in order to do so entrepreneurs share some of their wealth in the form of religious

tax for the betterment of needy people. Furthermore, all the listed companies are eligible to

perform their zakat on enterprise according to the annual profit gained. Considering the example

of Malacca which comprises of six business category named as manufacturing sector, retail

sector, community, social and other private sectors, restaurants, hotel and construction sector.

According to the report made by Pusat Zakat Malacca Zakah Collection report 2008-09, it can be

said that, only 40.54% of SMEs enterprises in the cited location are successfully contributing

their Zakat (Jaffar and Musa, 2013).

Year Agencies Reported

Agencies

Agencies that

comply Zakah

on business

Percentage

2009 Micro, Small

and Medium

Enterprises

698 283 40.54%

However, the contribution rate of Zakah on business is only 2.5% which is considered as

the very small amount of the total wealth of the business but still only 40.54% of SMEs in

8

Malacca are spending their 2.5% of wealth in the form of Zakah. Furthermore, if any

organisation after getting eligible fails to comply with any zakah and the zakah fitrah payment

will be considered as the Syariah’s crime offender in the Syariah’s law as per the section 51

Enactment of Hukum Syarak Administration 1991. Furthermore, under this, SME either could be

fined for not more than five thousand Malaysian Ringgit or prison of not more than 36 months or

both if subjected to guilty as charged.

Analyse how Islamic finance can use the concept of micro Finance to encourage SMEs

In general, Micro finance can be defined as the source of financial services for the

entrepreneurs and the small scale business who are lacking in accessing the banking and other

related services. However, the main purpose of microfinance to SMEs is that it helps in playing

pivotal role in economic growth. By offering small loans or micro-loans to the people who are

unable to access conventional loan.

Around 72% of people living in Muslim majority country does not undertake the use of

formal or conventional financial services. However, despite of availability of financial services,

Muslim community does not prefer because people thinks that these are incompatible with their

financial principles as defined in the Islamic law (Karim and et.al, 2012). In this regard, there are

several microfinance institutions which have initiated to provide services to low income Muslims

who demand products as per the Islamic rules and regulation.

However, this is the major reason behind which large number of Muslim SMEs has been

promoted in the recent past. Islamic microfinance consist of two constantly growing industries:

Islamic finance and micro finance. The main purpose for the existence of both industries is to

encourage or support Muslim SMEs financially so that they can grow their business in effective

and efficient manner (Ilias, 2012).

Henceforth, it is important for the Islamic financial institution to make the use of

microfinance for the Muslim people around the globe so that they can be encouraged to carry out

small scale enterprise in appropriate manner and helps in creating employment opportunities.

Furthermore, promoting more of the SMEs will assist the course of respective countries to

enhance their economic conditions.

How Islamic joint capital venture could be the way forward in Islamic investment

The structure of venture capital is considered as the equity investment which really

matches up with the Islamic financial concept of diminishing Musharaka. However, in particular

9

organisation after getting eligible fails to comply with any zakah and the zakah fitrah payment

will be considered as the Syariah’s crime offender in the Syariah’s law as per the section 51

Enactment of Hukum Syarak Administration 1991. Furthermore, under this, SME either could be

fined for not more than five thousand Malaysian Ringgit or prison of not more than 36 months or

both if subjected to guilty as charged.

Analyse how Islamic finance can use the concept of micro Finance to encourage SMEs

In general, Micro finance can be defined as the source of financial services for the

entrepreneurs and the small scale business who are lacking in accessing the banking and other

related services. However, the main purpose of microfinance to SMEs is that it helps in playing

pivotal role in economic growth. By offering small loans or micro-loans to the people who are

unable to access conventional loan.

Around 72% of people living in Muslim majority country does not undertake the use of

formal or conventional financial services. However, despite of availability of financial services,

Muslim community does not prefer because people thinks that these are incompatible with their

financial principles as defined in the Islamic law (Karim and et.al, 2012). In this regard, there are

several microfinance institutions which have initiated to provide services to low income Muslims

who demand products as per the Islamic rules and regulation.

However, this is the major reason behind which large number of Muslim SMEs has been

promoted in the recent past. Islamic microfinance consist of two constantly growing industries:

Islamic finance and micro finance. The main purpose for the existence of both industries is to

encourage or support Muslim SMEs financially so that they can grow their business in effective

and efficient manner (Ilias, 2012).

Henceforth, it is important for the Islamic financial institution to make the use of

microfinance for the Muslim people around the globe so that they can be encouraged to carry out

small scale enterprise in appropriate manner and helps in creating employment opportunities.

Furthermore, promoting more of the SMEs will assist the course of respective countries to

enhance their economic conditions.

How Islamic joint capital venture could be the way forward in Islamic investment

The structure of venture capital is considered as the equity investment which really

matches up with the Islamic financial concept of diminishing Musharaka. However, in particular

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.