Comprehensive Financial Analysis: Applied Accounting & Budgeting

VerifiedAdded on 2023/05/28

|13

|1847

|439

Project

AI Summary

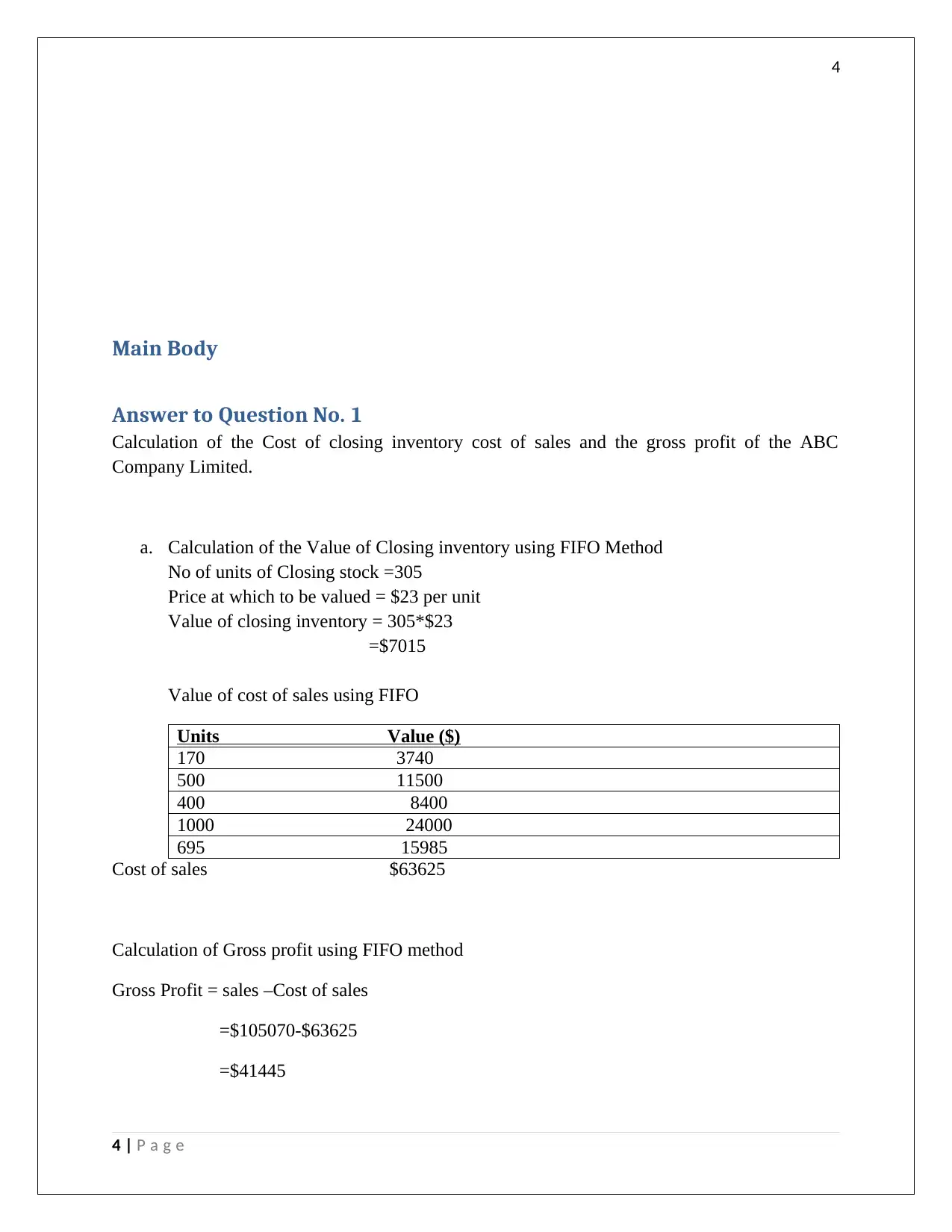

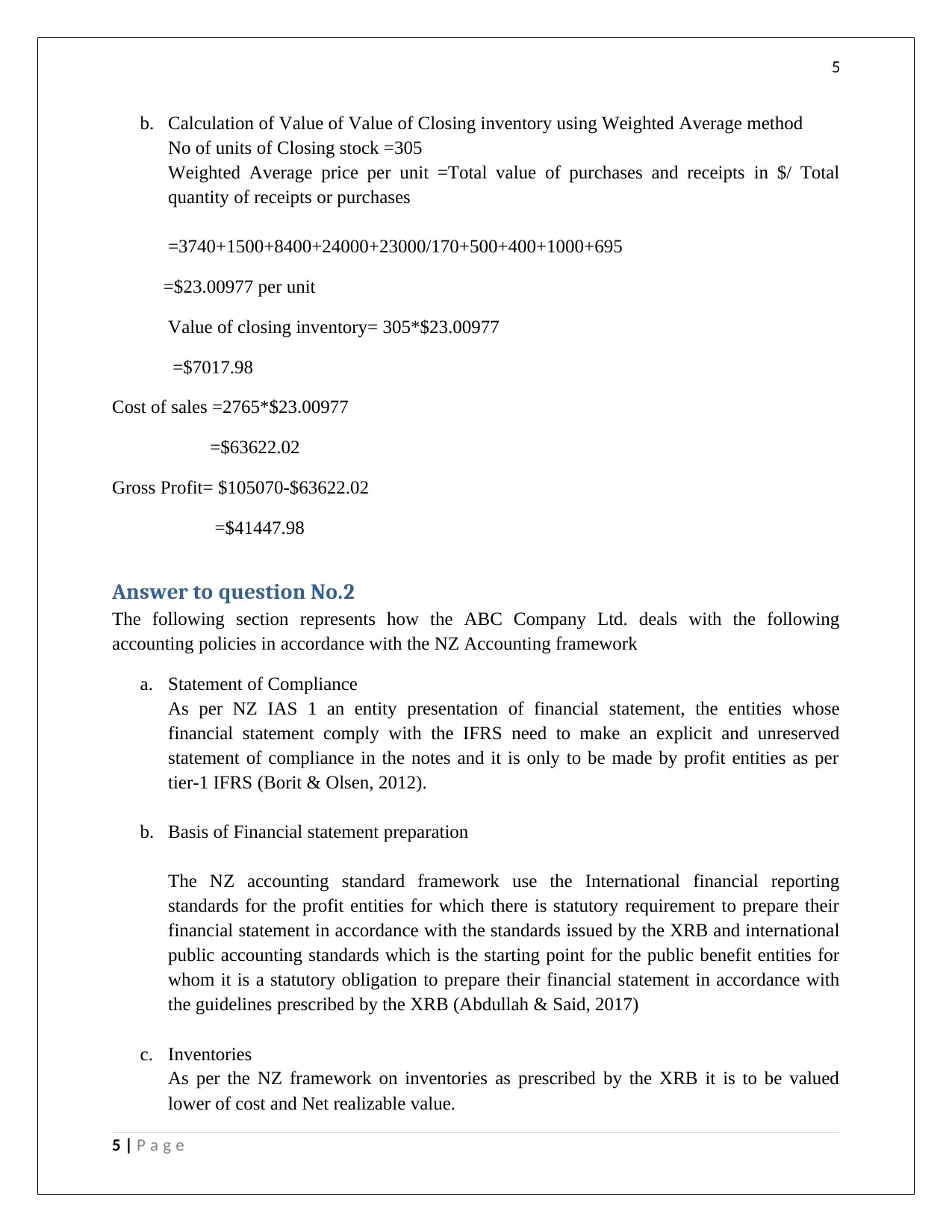

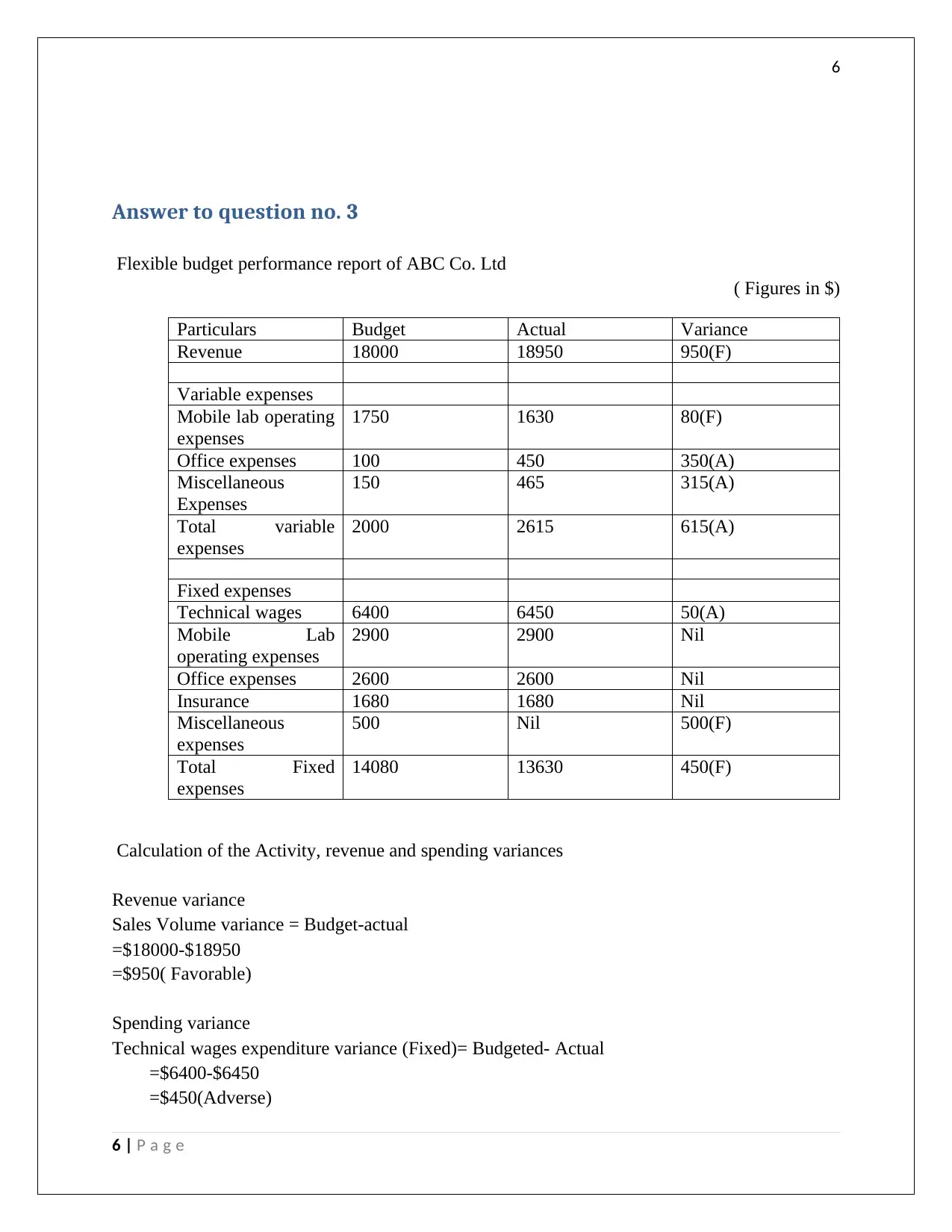

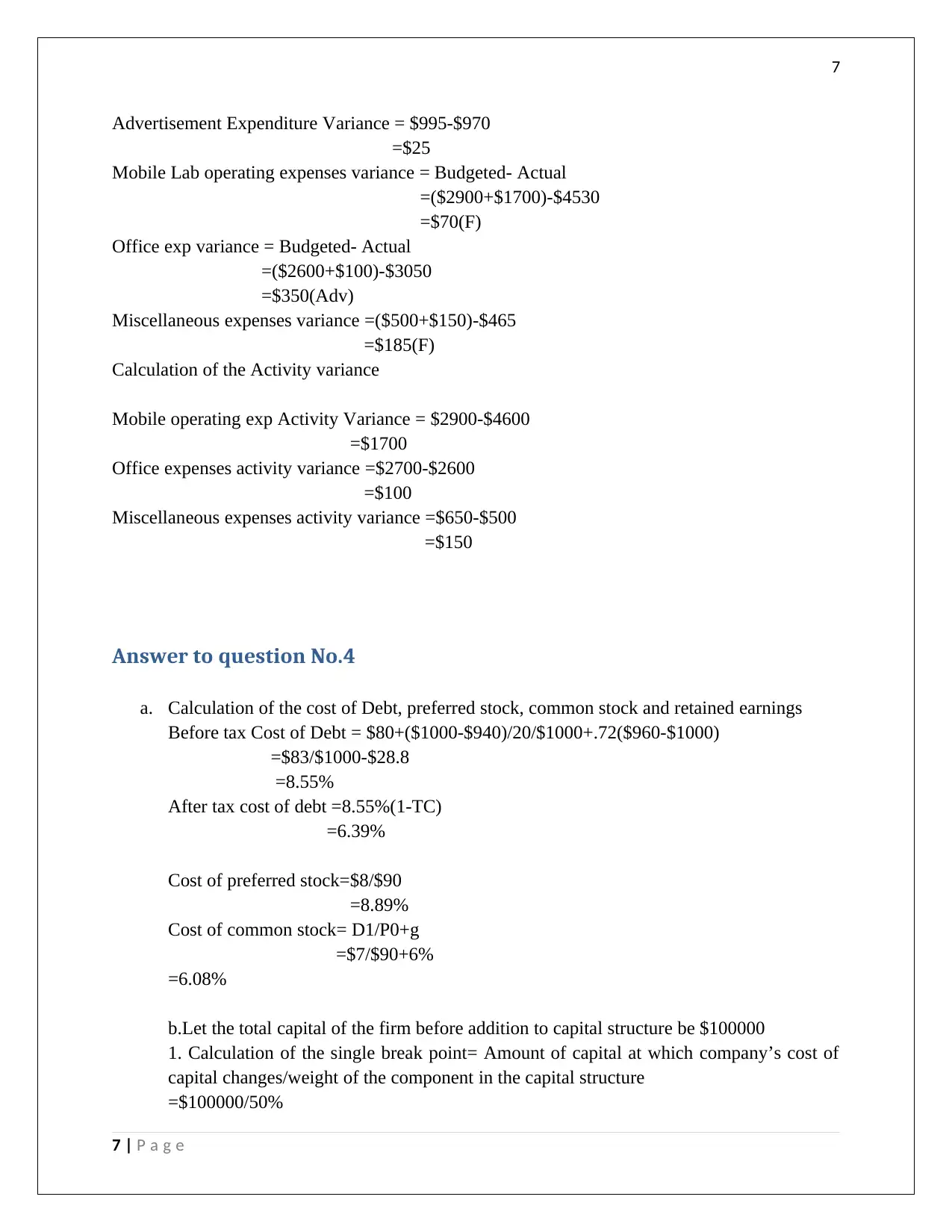

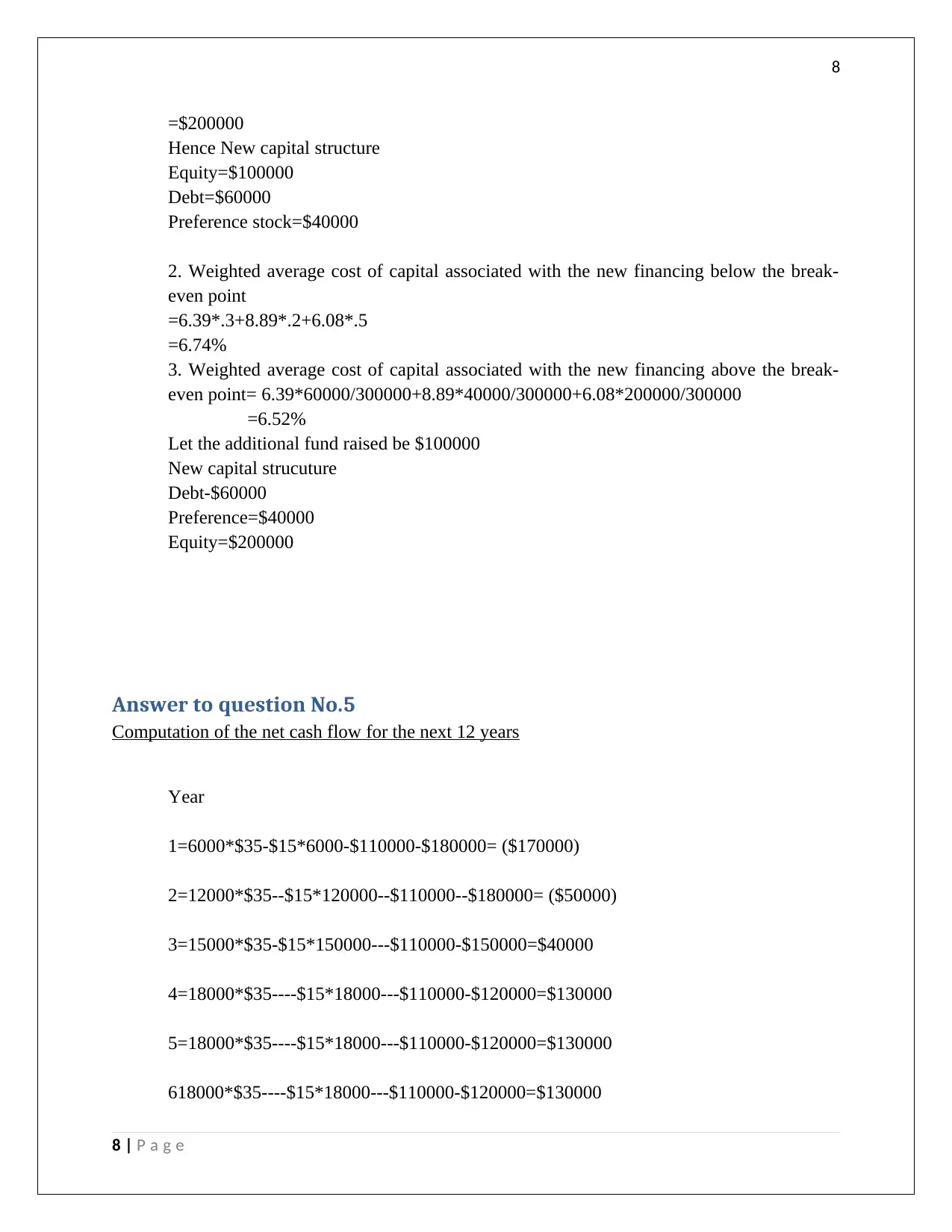

This document presents a comprehensive solution to an applied accounting and budgeting project. It covers fundamental accounting principles, regulatory frameworks, and their impact on budgets, controls, and profitability. The project includes calculations using FIFO and weighted average methods for inventory valuation, analysis of accounting policies in accordance with NZ accounting standards, and flexible budget performance reports. Furthermore, it delves into the cost of debt, preferred stock, common stock, and retained earnings, along with weighted average cost of capital calculations. The project also features capital budgeting, including net cash flow and net present value computations. Finally, it includes a production budget and direct material budget preparation, providing a holistic view of accounting and budgeting concepts. Desklib is the perfect platform for students looking for solved assignments and past papers.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.