Applied Advanced Analytics: Monte Carlo and Bootstrap Sampling Report

VerifiedAdded on 2023/03/17

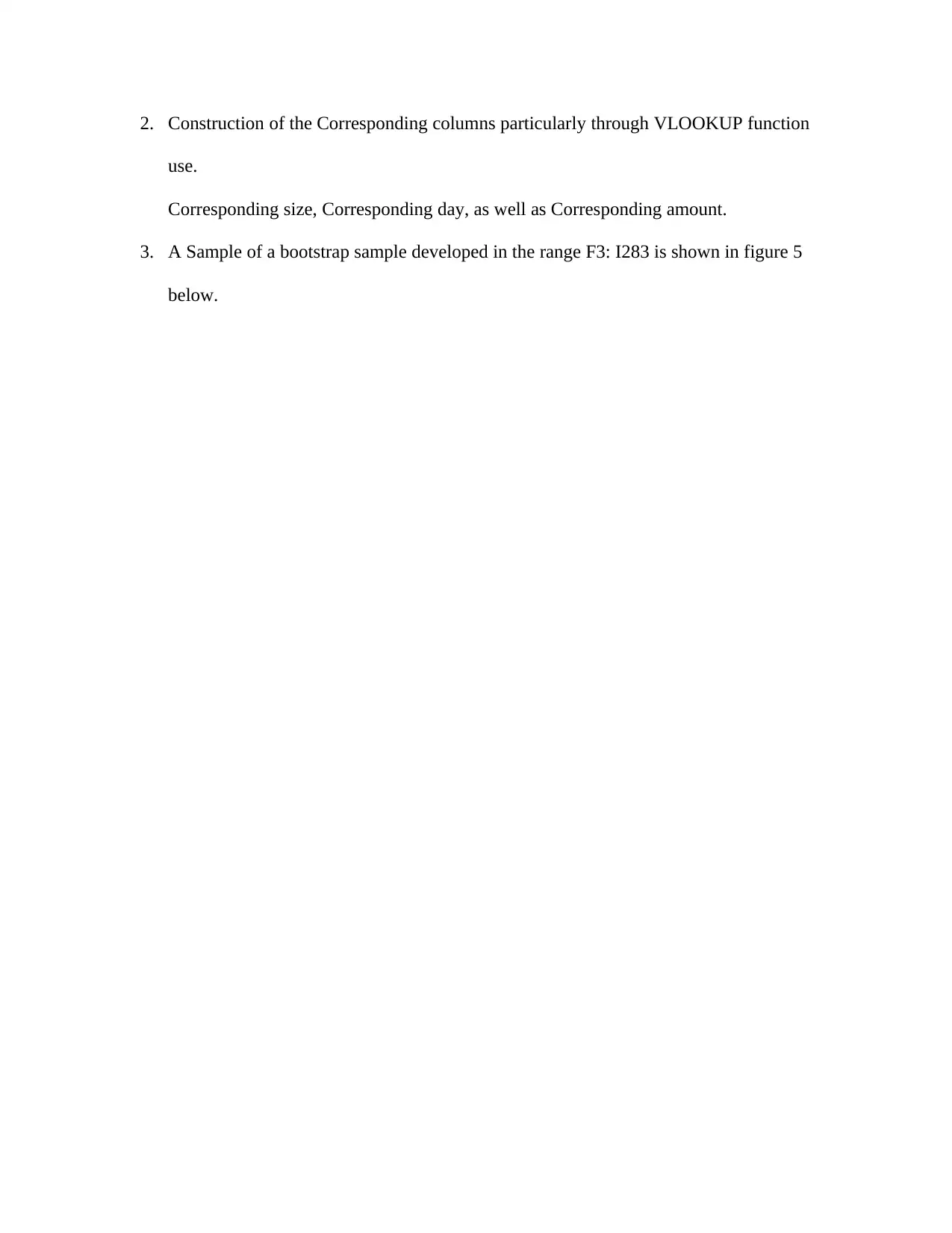

|14

|1452

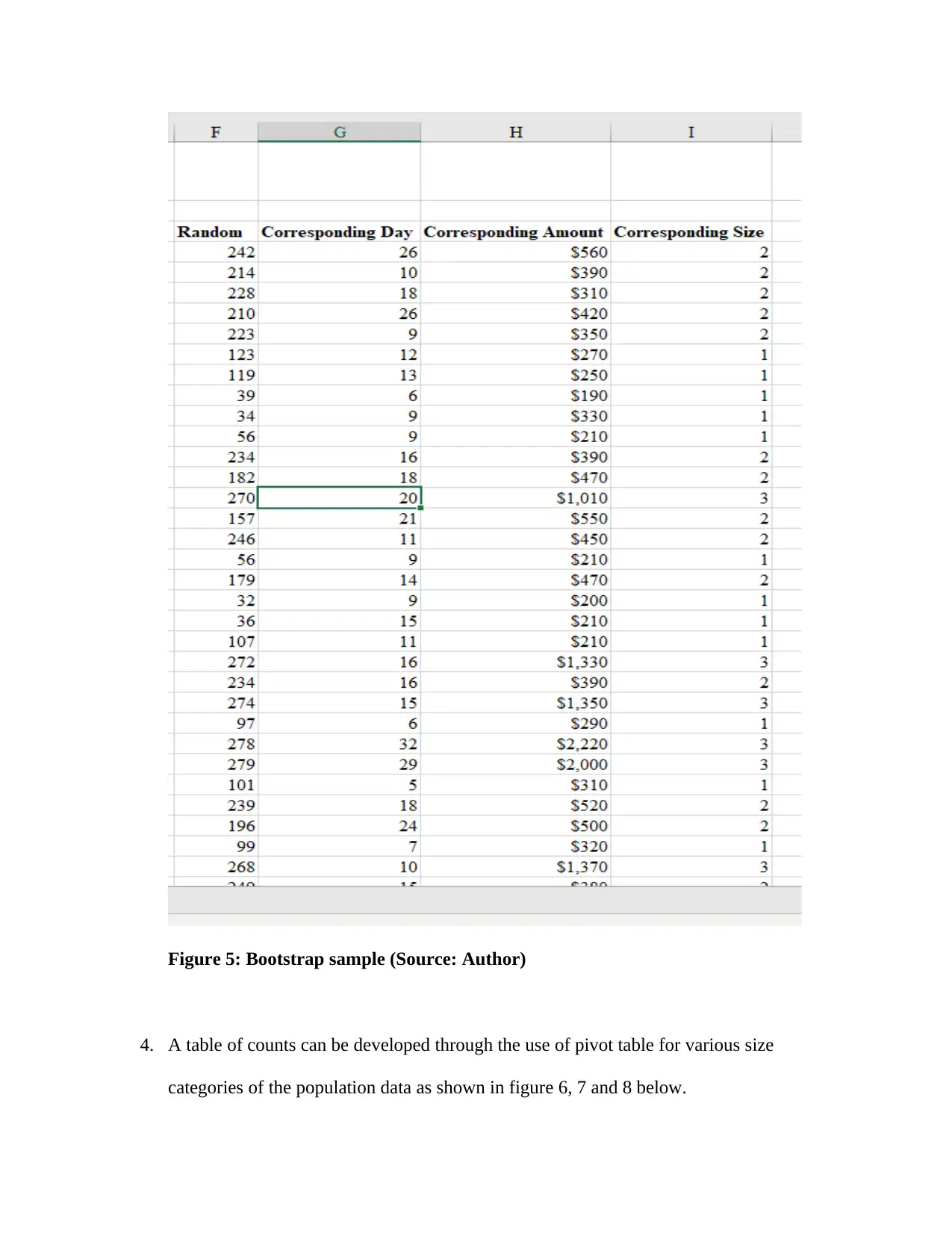

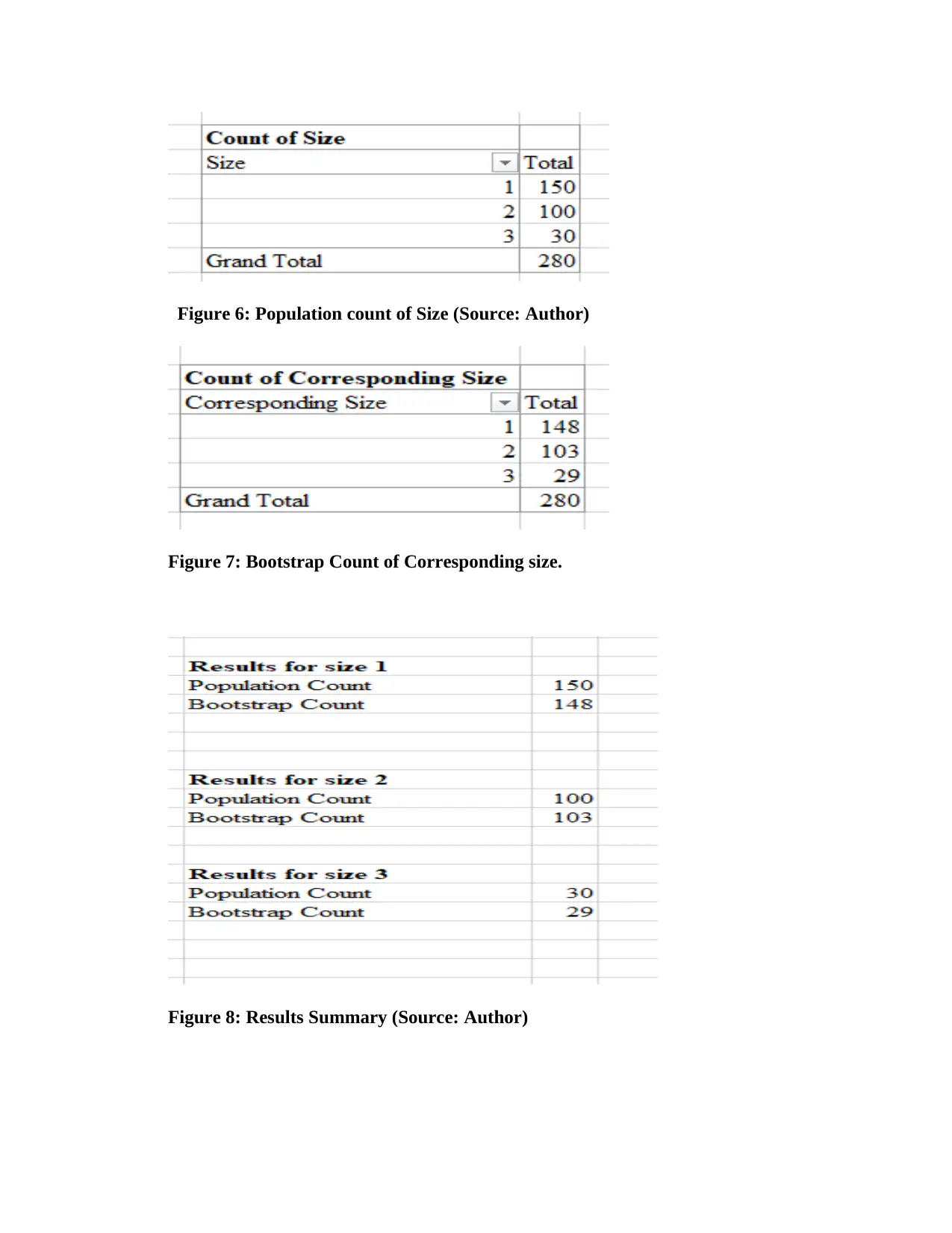

|66

Report

AI Summary

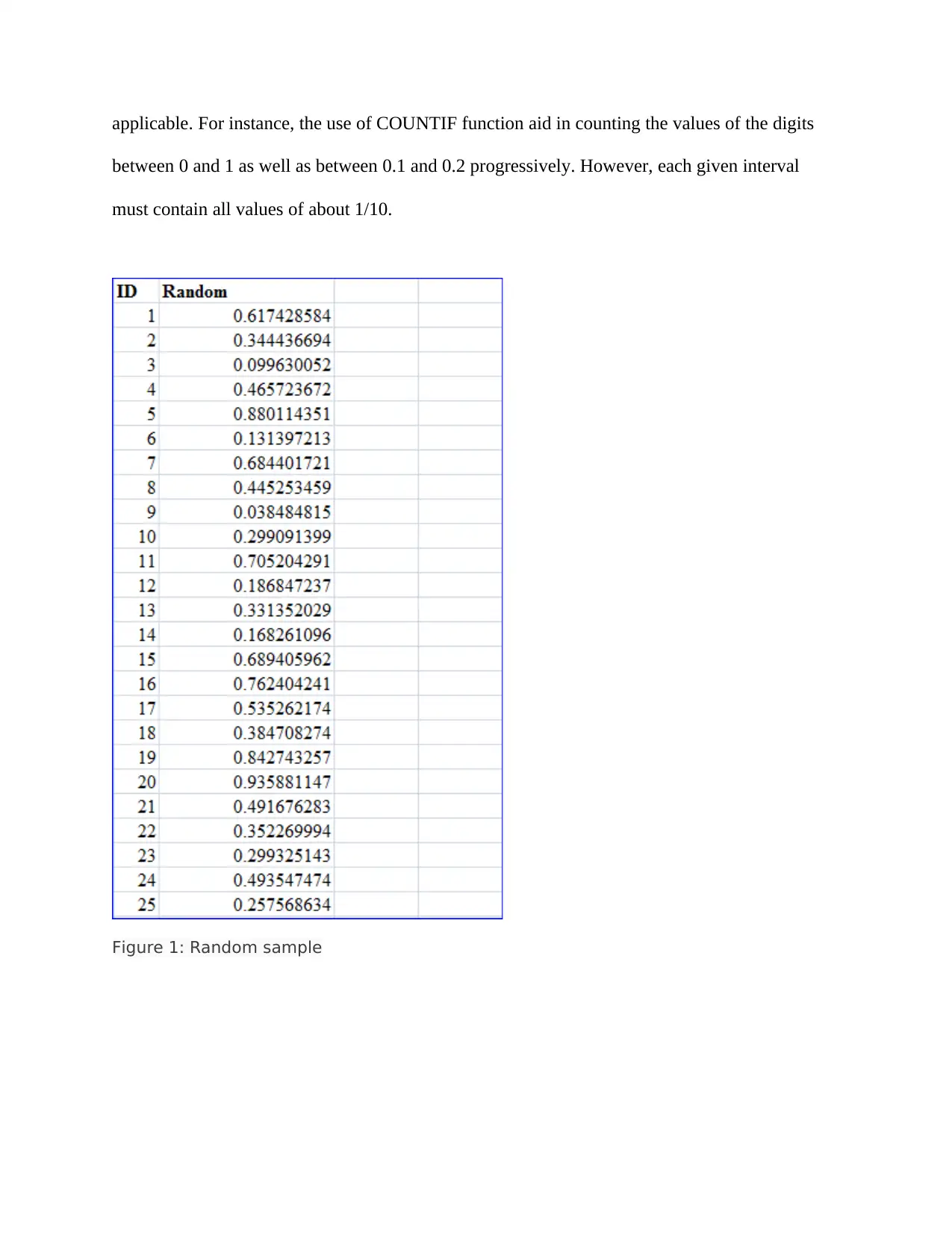

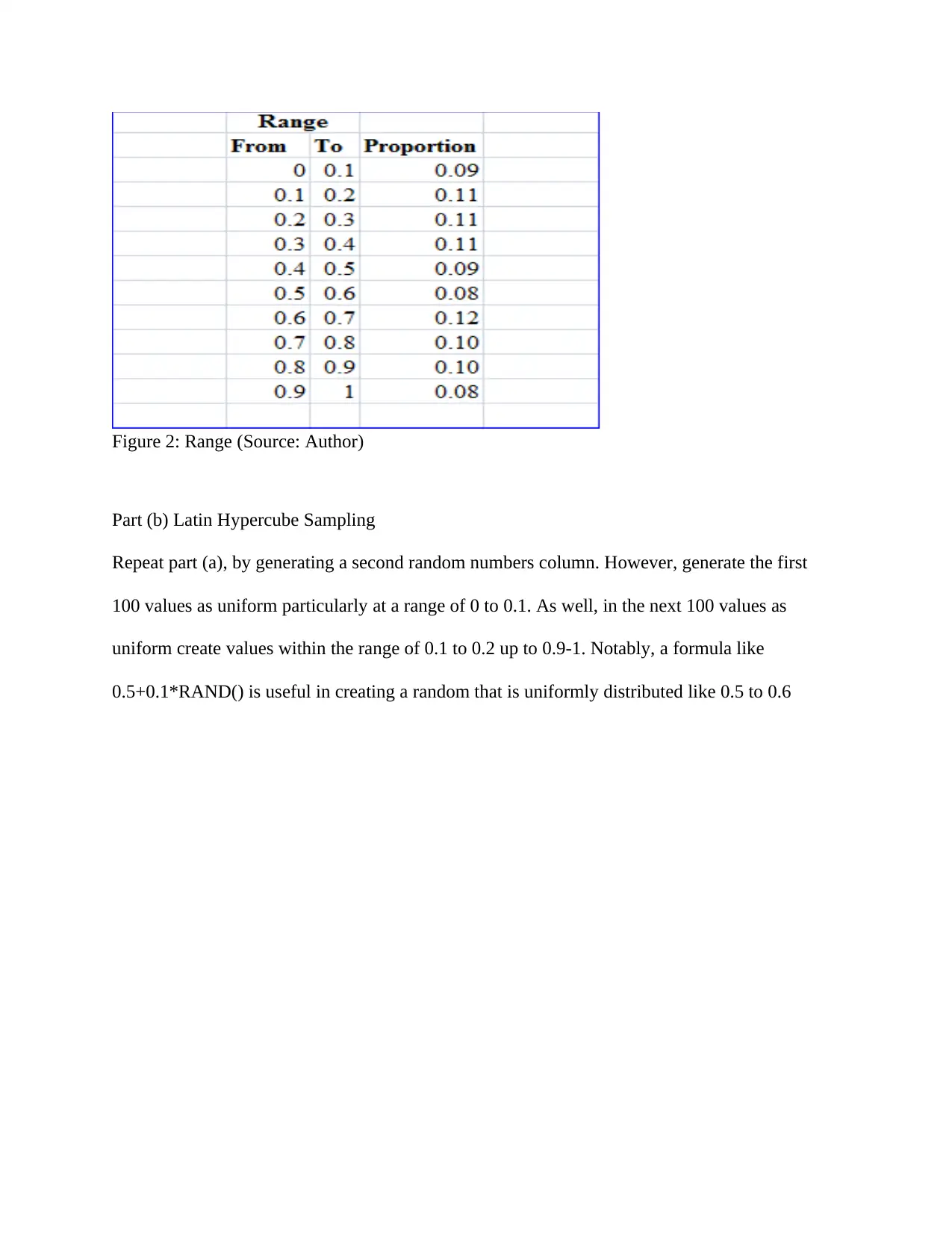

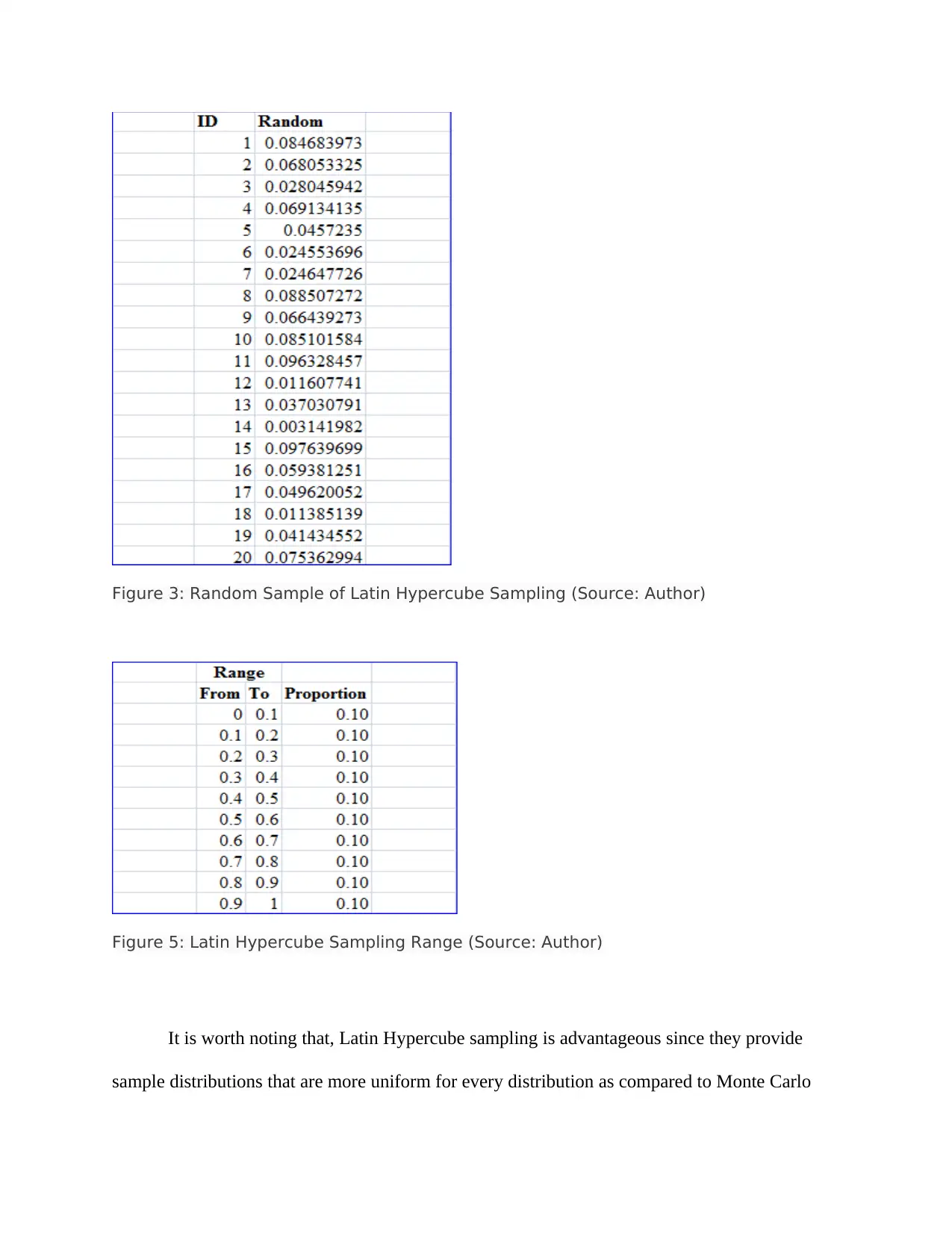

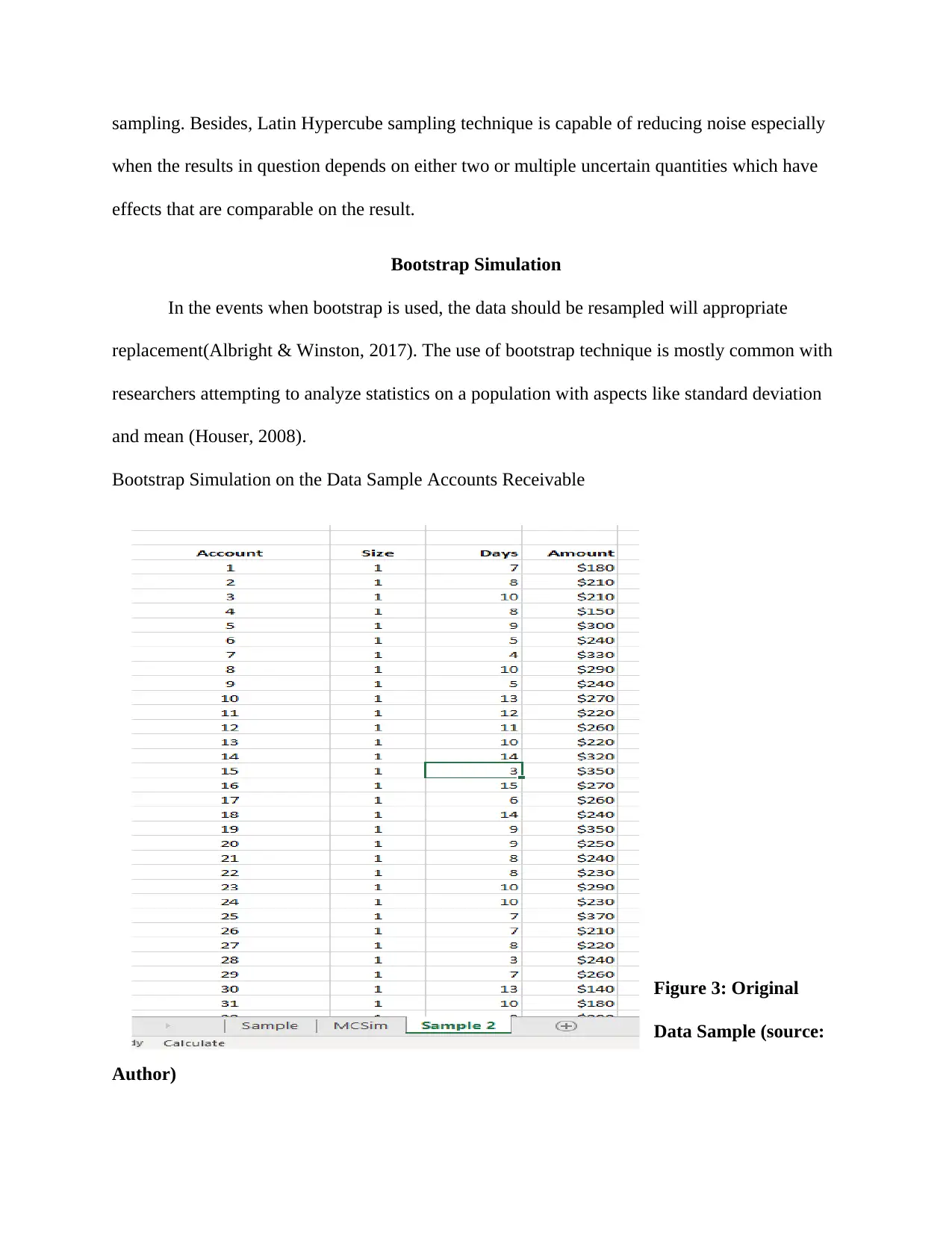

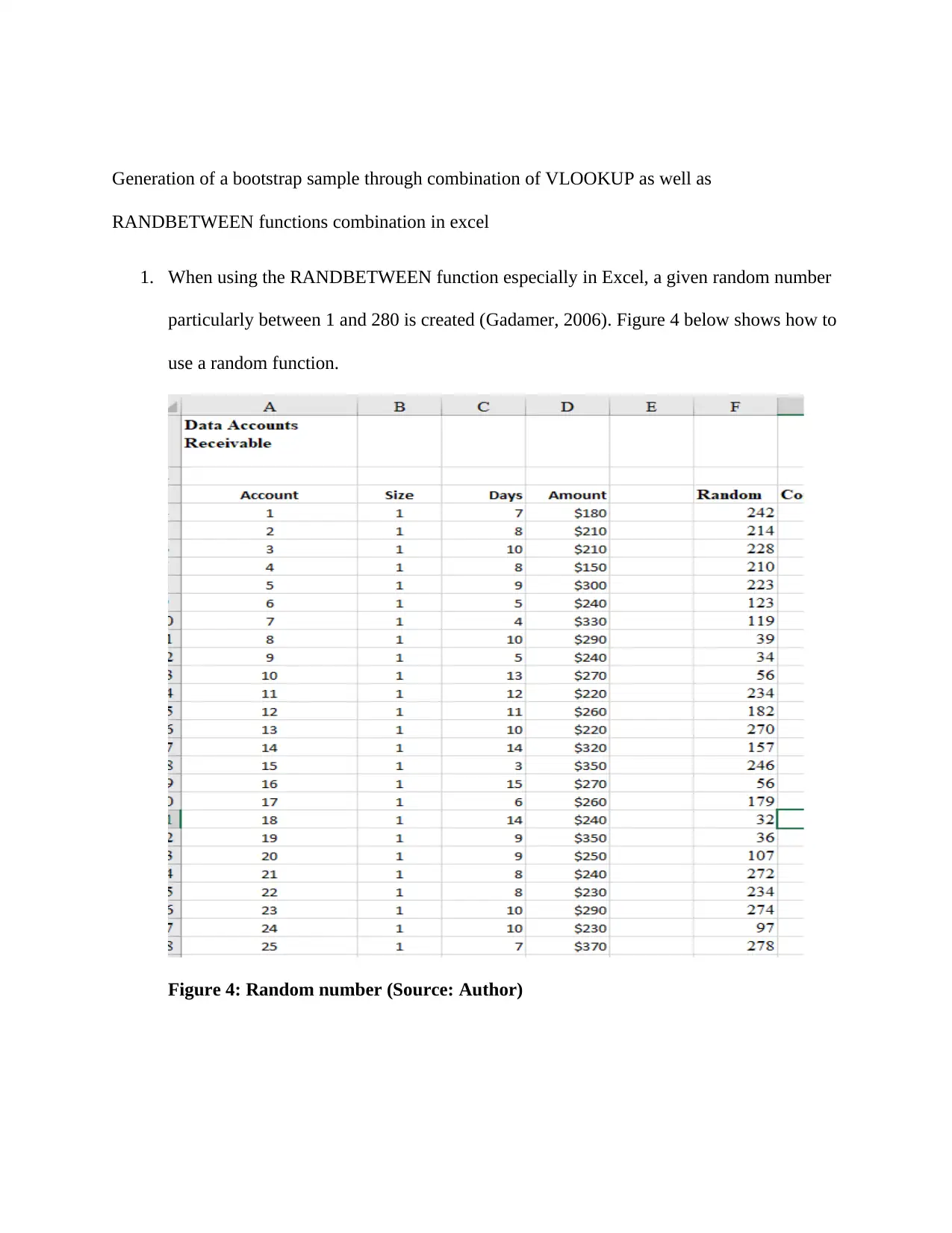

This report explores data sampling techniques, focusing on probability sampling, Monte Carlo simulation, and Bootstrap simulation within the context of applied advanced analytics. The introduction highlights the increasing reliance of businesses on data analytics for decision-making and growth, emphasizing the importance of analyzing populations and samples to identify trends and predict performance. The report then delves into probability sampling methods, including simple random sampling, and contrasts it with quota sampling, explaining the advantages of random sampling. The core of the report covers Monte Carlo and Latin Hypercube simulations, detailing their application in assessing risks and uncertainties, particularly in financial and project management sectors. It describes the process of generating random numbers and the benefits of Latin Hypercube sampling. The report concludes by explaining the bootstrap simulation technique, which is used for resampling data, and demonstrates its application using a sample accounts receivable dataset. The analysis includes the generation of bootstrap samples using Excel functions, the creation of count tables via pivot tables, and the calculation of mean and standard deviation for both the bootstrap sample and the original population data. The conclusion reiterates the importance of data sampling techniques in analyzing large populations and making informed decisions, emphasizing the need for measurable, goal-oriented, and practical sampling designs. The references provided support the methods and concepts discussed.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.