Applied Business Finance: Financial Management, Statements & Ratios

VerifiedAdded on 2022/12/27

|13

|2505

|68

Report

AI Summary

This report provides an evaluation of applied business finance, beginning with a definition and discussion of financial management and its importance in meeting operational expenses, financial planning, protecting business funds, fund allocation, and enhancing profitability. It describes the main financial statements—balance sheet, income statement, and cash flow statement—explaining their components and how they reflect a company's financial position and performance. The report also explains the utilization of ratios for financial management, including their role in forecasting, budgeting, assessing operational efficiency, and evaluating liquidity. Finally, the report includes a ratio analysis of a company's financial data to interpret its profitability, liquidity, and efficiency, concluding with insights into areas for improvement. Desklib offers a platform where students can find this and other solved assignments.

Applied

Business

Finance

Business

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

Defining and discussing on concept as well as importance of financial management:...............3

SECTION 2......................................................................................................................................4

Describing financial statements and explaining utilization of ratios for financial management:4

SECTION 3......................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION...........................................................................................................................3

SECTION 1......................................................................................................................................3

Defining and discussing on concept as well as importance of financial management:...............3

SECTION 2......................................................................................................................................4

Describing financial statements and explaining utilization of ratios for financial management:4

SECTION 3......................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

INTRODUCTION

Business finance refers to funds as well as credits that are employed in a business. finance

can be termed as foundation for business activities of an organization. Hence, business finance is

concerned towards raising and management of funds in a firm. Planning, analysis as well as

controlling of operations comes up as a responsibility of a financial manager. Decisions

regarding finance affects both profitability as well as risk factor which are associated with

operations of business. therefore, business finance is applied in an enterprise for the purpose of

assisting external monetary which is availed when an organization runs towards shortage of

capital (Schaltegger, Hörisch and Freeman, 2019).

This report is based on evaluation of applied business finance. It covers description of

financial management along with its importance. Further, main financial statements are

described and discussed and utilization of ratios in context to financial management is explained.

Lasty, efficiency of a company is analysed by interpreting its profitability, liquidity as well as

efficiency position.

SECTION 1

Defining and discussing on concept as well as importance of financial management:

Financial management indicates strategic planning, organization, direction as well as

controlling in relevance to financial undertaking of business. it involves application of

management principles in regards to financial assets of firm. While considering scope of

financial management it can be stated that financial management fosters decisions of an

organization regarding investments (Sugiyanto and Candra, 2019). Further, financial decisions

incorporate raising of funds from different sources along with evaluation of such sources by

analysing time period allocated with it, cost of financing as well as expected return.

Importance of financial management are discussed below:

Meeting operational expenses: Finance is required by business in working capital form

for the purpose of meeting operational expenses of an organization. Such operational

expenses are of various types such as, remunerative payments, payment of interest, raw

material, stock etc. Adequate financial planning and maintenance for short term is

essential for ensuring smooth flow of business opera

3

Business finance refers to funds as well as credits that are employed in a business. finance

can be termed as foundation for business activities of an organization. Hence, business finance is

concerned towards raising and management of funds in a firm. Planning, analysis as well as

controlling of operations comes up as a responsibility of a financial manager. Decisions

regarding finance affects both profitability as well as risk factor which are associated with

operations of business. therefore, business finance is applied in an enterprise for the purpose of

assisting external monetary which is availed when an organization runs towards shortage of

capital (Schaltegger, Hörisch and Freeman, 2019).

This report is based on evaluation of applied business finance. It covers description of

financial management along with its importance. Further, main financial statements are

described and discussed and utilization of ratios in context to financial management is explained.

Lasty, efficiency of a company is analysed by interpreting its profitability, liquidity as well as

efficiency position.

SECTION 1

Defining and discussing on concept as well as importance of financial management:

Financial management indicates strategic planning, organization, direction as well as

controlling in relevance to financial undertaking of business. it involves application of

management principles in regards to financial assets of firm. While considering scope of

financial management it can be stated that financial management fosters decisions of an

organization regarding investments (Sugiyanto and Candra, 2019). Further, financial decisions

incorporate raising of funds from different sources along with evaluation of such sources by

analysing time period allocated with it, cost of financing as well as expected return.

Importance of financial management are discussed below:

Meeting operational expenses: Finance is required by business in working capital form

for the purpose of meeting operational expenses of an organization. Such operational

expenses are of various types such as, remunerative payments, payment of interest, raw

material, stock etc. Adequate financial planning and maintenance for short term is

essential for ensuring smooth flow of business opera

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

tions (Van, and et.al, 2021). Financial management facilitates adequate maintenance of

cash flow in an enterprise which leads to encouragement of efficiency of an organization.

Planning of financials: Financial management plays a crucial role in development and

implementation of effective financial planning in an entity. It evaluates necessities of

business in relation to its financials. Apart from it, financial planning fosters

identification of areas in which company is required to tale corrective measures. Hence,

sustainability and success factor of an organization.

Protects funds of business: Financial management enables protection and maintenance

of finance of an organization which helps in attainment of business goals. It helps an

entity to measure areas of fund requirement and ensures adequate allocation of financial

resources of an enterprise. It leads to enhancement of level of efficiency of a firm as

overspending is eliminated which pertains crucial impact on operations of an

organization (Xie and et.al, 2019).

Fund allocation: Another importance which is associated with financial management in

business is that it ensures appropriate allocation of funds. Proper utilization of finance in

business enables enhancement of its operational proficiency. It eliminates unnecessary

expenditures and helps in improvement of estimated capital of an enterprise.

Enhances profitability: Profitability of an enterprise is highly dependent on adequate

fund utilization as well as efficiency of business. as, financial management enables

improvement of position of profitability of an organization

SECTION 2

Describing financial statements and explaining utilization of ratios for financial management:

Financial statements indicate such reports which provides a detailed information in relation

to finances of a company. It involves assets, equities, expenses, liabilities, cash flow etc.

Financial statement can be defined as an indicator which enables illustration of business

activities of an organization during a specific period of time. It provides outline for financial

position of business. It is a written record that provides written records which conveys activities

of business and evaluates financial performance of an enterprise. Investors as well as financial

analysts are highly reliable on such financial information of an entity for the purpose of

analysing performance of an enterprise. Financial statements are utilised by investors, market

analysts as well as creditors for evaluating financial health as well as earning potential of a

4

cash flow in an enterprise which leads to encouragement of efficiency of an organization.

Planning of financials: Financial management plays a crucial role in development and

implementation of effective financial planning in an entity. It evaluates necessities of

business in relation to its financials. Apart from it, financial planning fosters

identification of areas in which company is required to tale corrective measures. Hence,

sustainability and success factor of an organization.

Protects funds of business: Financial management enables protection and maintenance

of finance of an organization which helps in attainment of business goals. It helps an

entity to measure areas of fund requirement and ensures adequate allocation of financial

resources of an enterprise. It leads to enhancement of level of efficiency of a firm as

overspending is eliminated which pertains crucial impact on operations of an

organization (Xie and et.al, 2019).

Fund allocation: Another importance which is associated with financial management in

business is that it ensures appropriate allocation of funds. Proper utilization of finance in

business enables enhancement of its operational proficiency. It eliminates unnecessary

expenditures and helps in improvement of estimated capital of an enterprise.

Enhances profitability: Profitability of an enterprise is highly dependent on adequate

fund utilization as well as efficiency of business. as, financial management enables

improvement of position of profitability of an organization

SECTION 2

Describing financial statements and explaining utilization of ratios for financial management:

Financial statements indicate such reports which provides a detailed information in relation

to finances of a company. It involves assets, equities, expenses, liabilities, cash flow etc.

Financial statement can be defined as an indicator which enables illustration of business

activities of an organization during a specific period of time. It provides outline for financial

position of business. It is a written record that provides written records which conveys activities

of business and evaluates financial performance of an enterprise. Investors as well as financial

analysts are highly reliable on such financial information of an entity for the purpose of

analysing performance of an enterprise. Financial statements are utilised by investors, market

analysts as well as creditors for evaluating financial health as well as earning potential of a

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company. Main financial statements which are prepared by financial managers of an

organization are, income statement, balance sheet and cash flow statement (Begenau and

Salomao, 2019).

Balance sheet:

Balance sheet can be described as a financial statement which reports regarding assets,

liabilities as well as shareholder’s equity of a company at a period of time. It serves as a basis for

the purpose of computation of return rate as well as evaluation of capital structure of business. It

signifies a snapshot for own as well as owes of an enterprise and represents the amount which is

invested by shareholders of business. It adheres an accounting equation which pertains assets on

a side and another side involves liabilities and shareholder’s equity. It states that assets of an

organization equal to its liabilities plus equity of shareholders.

Assets: In this segment of balance sheet, those items are included which proves to be

asset for a firm, i.e., such assets which can be liquidity or converted into cash. It is

divided into two forms, that are, current assets and non-current assets. Current assets

indicate those type of assets which can be liquidated within a year while on the other

hand, non-current assets refer to such type of assets which cannot be liquidated

within a year. Cash and cash equivalents, marketable securities, accounts receivable,

inventory, and prepaid expenses are considered under the section of current assets.

Apart form it, non-current asset involves long term investments, fixed assets, and

intangible assets (Fosso Wamba and et.al, 2020).

Liabilities: It refers to money which an organization owes to external parties. It

includes amount which is payable to suppliers, interest that is payable by an

enterprise to debt holders, creditors etc. it is further divided into two parts, that are,

current liabilities and non-current liabilities. Current liabilities refer to such liabilities

which are due for payment within a year. On the contrary, non-current liabilities

involves such type of liabilities which are due for payment after a year. Current

liabilities involve bank indebtedness, interest payable, wages payable customer

prepayments, dividends payable, and accounts payable. Further, non-current

liabilities include long term debts, liability of pension fund, and deferred tax liability.

Shareholders’ equity: It involves money which is attributable to shareholders of a

company. It indicates amount which equals to total assets of a firm minus total

5

organization are, income statement, balance sheet and cash flow statement (Begenau and

Salomao, 2019).

Balance sheet:

Balance sheet can be described as a financial statement which reports regarding assets,

liabilities as well as shareholder’s equity of a company at a period of time. It serves as a basis for

the purpose of computation of return rate as well as evaluation of capital structure of business. It

signifies a snapshot for own as well as owes of an enterprise and represents the amount which is

invested by shareholders of business. It adheres an accounting equation which pertains assets on

a side and another side involves liabilities and shareholder’s equity. It states that assets of an

organization equal to its liabilities plus equity of shareholders.

Assets: In this segment of balance sheet, those items are included which proves to be

asset for a firm, i.e., such assets which can be liquidity or converted into cash. It is

divided into two forms, that are, current assets and non-current assets. Current assets

indicate those type of assets which can be liquidated within a year while on the other

hand, non-current assets refer to such type of assets which cannot be liquidated

within a year. Cash and cash equivalents, marketable securities, accounts receivable,

inventory, and prepaid expenses are considered under the section of current assets.

Apart form it, non-current asset involves long term investments, fixed assets, and

intangible assets (Fosso Wamba and et.al, 2020).

Liabilities: It refers to money which an organization owes to external parties. It

includes amount which is payable to suppliers, interest that is payable by an

enterprise to debt holders, creditors etc. it is further divided into two parts, that are,

current liabilities and non-current liabilities. Current liabilities refer to such liabilities

which are due for payment within a year. On the contrary, non-current liabilities

involves such type of liabilities which are due for payment after a year. Current

liabilities involve bank indebtedness, interest payable, wages payable customer

prepayments, dividends payable, and accounts payable. Further, non-current

liabilities include long term debts, liability of pension fund, and deferred tax liability.

Shareholders’ equity: It involves money which is attributable to shareholders of a

company. It indicates amount which equals to total assets of a firm minus total

5

liabilities of an organization. Retained earning does not form a part of it (Mnif

Sellami and Gafsi, 2019).

Income statement: It indicates performance of a business over a period of time. Hence,

income statement refers to a financial statement which showcase income as well as expenditure

of an organization. It enables firm in evaluating financial health of a business. Apart from it,

income statement ensures owners of an organization to decide proficiency of business in

enhancing its revenue generation capacity and ensures decrement in costs which is associated

with business. in addition to it, computation of income statement showcases efficiency of a firm

in regards to strategies that is formulated by management team of business. income statements

inform regarding performance track of an enterprise which helps in making informed decisions.

Apart form it, it highlights upcoming or future expenditures of an organization along with

unexpected expenses that incurs in business. in addition to it, preparation of income statement

enables overall analysis of a firm.

Cash flow statement: This financial statement pinpoints amount of cash as well as cash

equivalents which is earned or paid by an organization. Apart from it, cash flow statement

enables measurement of efficiency level of an enterprise in relevance to management of its

position of cash. It indicates proficiency of an enterprise in generating cash for the purpose of

paying its debtors or der obligations as well as funding operational expenditures of business.

Cash flow from operating activities, cash flow from financing activities and cash flow from

activities related to financing comes up as a component for statement of cash flow (Sanfelici and

Halbert, 2019). Preparation of cash flow statement allows investors of an enterprise in

understanding operational efficiency of business. It is important because it ensures determination

of company’s financial footing by its investors.

Ratios: It is a technique of determining or gaining insight regarding liquidity position of

a company, its operational efficiency as well as level of profitability. It serves as a corner stone

for analysis of fundamental equity. It reveals insight of a company in relevance to profitability,

solvency, operational efficiency as well as liquidity position of an organization. Apart from it,

analysis of ratios marks efficiency a performance of a company over a period of time and

provides an opportunity for comparing its performance with another similar entity. Overall, ratio

analysis provides a wider level of picture regarding financial health of an enterprise.

Uses of ratio are further described below:

6

Sellami and Gafsi, 2019).

Income statement: It indicates performance of a business over a period of time. Hence,

income statement refers to a financial statement which showcase income as well as expenditure

of an organization. It enables firm in evaluating financial health of a business. Apart from it,

income statement ensures owners of an organization to decide proficiency of business in

enhancing its revenue generation capacity and ensures decrement in costs which is associated

with business. in addition to it, computation of income statement showcases efficiency of a firm

in regards to strategies that is formulated by management team of business. income statements

inform regarding performance track of an enterprise which helps in making informed decisions.

Apart form it, it highlights upcoming or future expenditures of an organization along with

unexpected expenses that incurs in business. in addition to it, preparation of income statement

enables overall analysis of a firm.

Cash flow statement: This financial statement pinpoints amount of cash as well as cash

equivalents which is earned or paid by an organization. Apart from it, cash flow statement

enables measurement of efficiency level of an enterprise in relevance to management of its

position of cash. It indicates proficiency of an enterprise in generating cash for the purpose of

paying its debtors or der obligations as well as funding operational expenditures of business.

Cash flow from operating activities, cash flow from financing activities and cash flow from

activities related to financing comes up as a component for statement of cash flow (Sanfelici and

Halbert, 2019). Preparation of cash flow statement allows investors of an enterprise in

understanding operational efficiency of business. It is important because it ensures determination

of company’s financial footing by its investors.

Ratios: It is a technique of determining or gaining insight regarding liquidity position of

a company, its operational efficiency as well as level of profitability. It serves as a corner stone

for analysis of fundamental equity. It reveals insight of a company in relevance to profitability,

solvency, operational efficiency as well as liquidity position of an organization. Apart from it,

analysis of ratios marks efficiency a performance of a company over a period of time and

provides an opportunity for comparing its performance with another similar entity. Overall, ratio

analysis provides a wider level of picture regarding financial health of an enterprise.

Uses of ratio are further described below:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Forecasting as well as planning: Computation of ratio fosters activities of forecasting

and planning. Ratio analysis helps an organization is estimating its business activities.

Budgeting: Analysis of ratio enables estimation for future or up coming activities of

prior experience. It helps in estimating budgeting figures.

Operational efficiency: It evaluated degree of operational efficiency in context to

management as well as utilization of its assets. Solvency of an organization in

dependence on revenue which is generated by its asset utilization.

Evaluation of position of liquidity: Ratio analysis enables assessment of position of

liquidity of an organization in context to paying capacity of business for short term (Khan

Yaseen and Ali, 2019).

SECTION 3

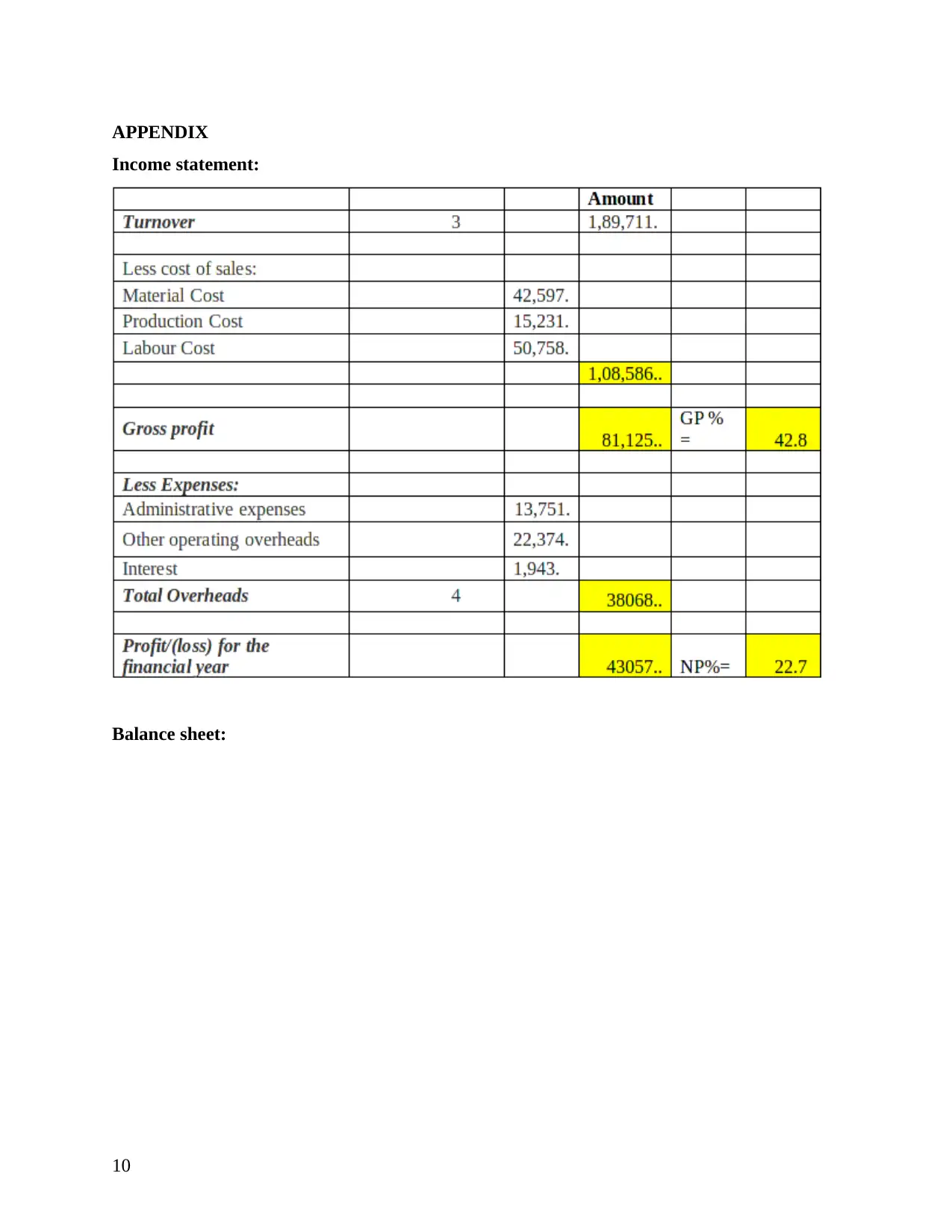

Net profit margin = 43057 / 189711 * 100

= 22.69%

Gross profit margin= 81125 / 189711 * 100

= 42.76%

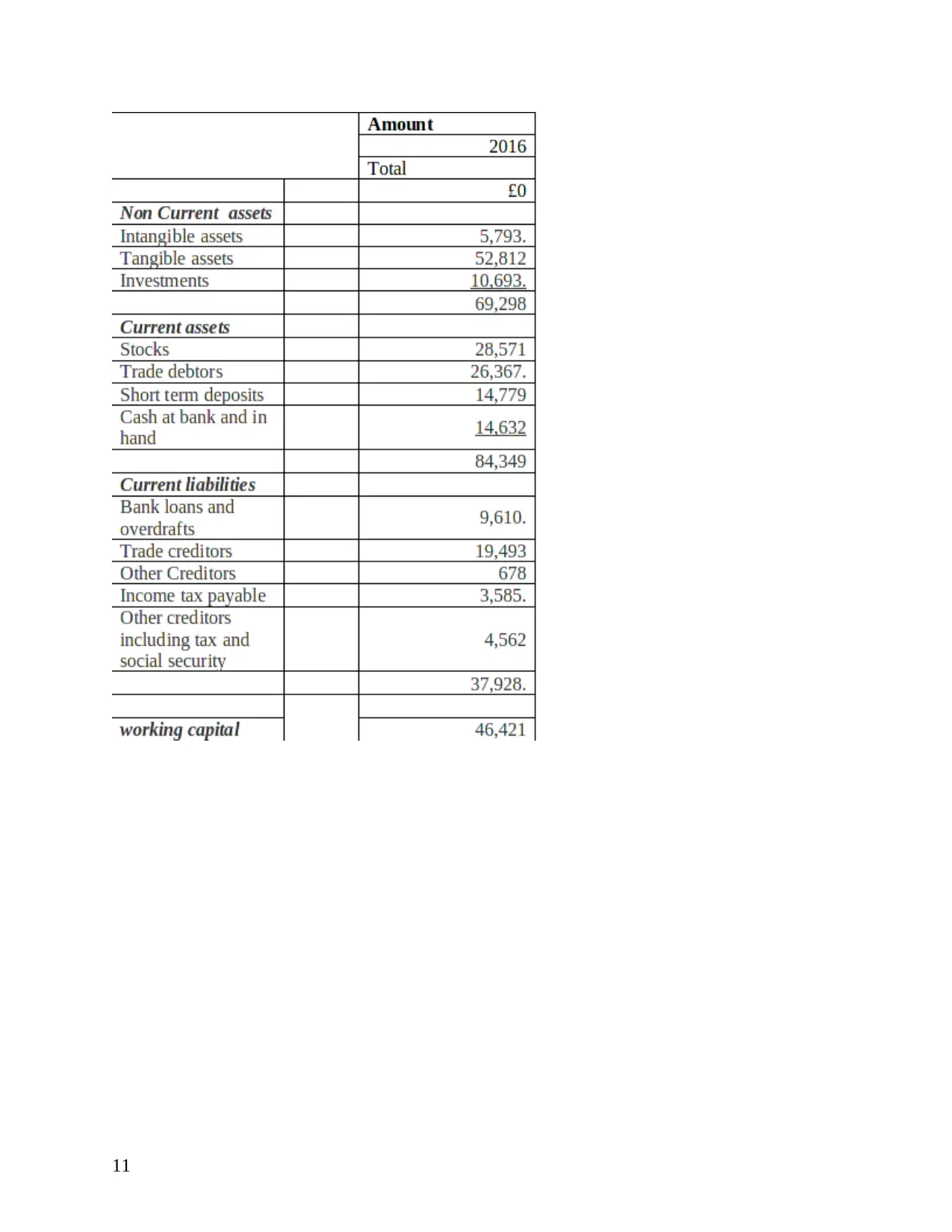

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

From the above ratio analysis, it can be interpreted that efficiency of company in

generating profitability from its core operations is high as gross profit margin of an organization

is high. While on the other hand, firm is required to improves its net profit margin which can be

done through deducting unnecessary expenditures. Further, liquidity position of an organization

is adequate.

CONCLUSION

From the above report it can be concluded that financial management refers to practice of

handling finances of an organization. It helps in analysing success factor of business and ensures

its compliance along with regulations of business. It is practice of tracking financial performance

of an organization. It supports creation of financial objectives of an enterprise for long term,

7

and planning. Ratio analysis helps an organization is estimating its business activities.

Budgeting: Analysis of ratio enables estimation for future or up coming activities of

prior experience. It helps in estimating budgeting figures.

Operational efficiency: It evaluated degree of operational efficiency in context to

management as well as utilization of its assets. Solvency of an organization in

dependence on revenue which is generated by its asset utilization.

Evaluation of position of liquidity: Ratio analysis enables assessment of position of

liquidity of an organization in context to paying capacity of business for short term (Khan

Yaseen and Ali, 2019).

SECTION 3

Net profit margin = 43057 / 189711 * 100

= 22.69%

Gross profit margin= 81125 / 189711 * 100

= 42.76%

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

From the above ratio analysis, it can be interpreted that efficiency of company in

generating profitability from its core operations is high as gross profit margin of an organization

is high. While on the other hand, firm is required to improves its net profit margin which can be

done through deducting unnecessary expenditures. Further, liquidity position of an organization

is adequate.

CONCLUSION

From the above report it can be concluded that financial management refers to practice of

handling finances of an organization. It helps in analysing success factor of business and ensures

its compliance along with regulations of business. It is practice of tracking financial performance

of an organization. It supports creation of financial objectives of an enterprise for long term,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enables making of informed decisions, and yields insight of business in relevance to funds and

investments. Financial statements are analysed in case of financial management. Financial

statement includes three types of components, that are balance sheet, cash flow statement as well

as income statement. Apart from it, ratio analysis helps in evaluating financial position of an

enterprise.

8

investments. Financial statements are analysed in case of financial management. Financial

statement includes three types of components, that are balance sheet, cash flow statement as well

as income statement. Apart from it, ratio analysis helps in evaluating financial position of an

enterprise.

8

REFERENCES

Books and Journals:

Schaltegger, S., Hörisch, J. and Freeman, R. E., 2019. Business cases for sustainability: A

stakeholder theory perspective. Organization & Environment. 32(3). pp.191-212.

Sugiyanto, S. and Candra, A., 2019. Good Corporate Governance, Conservatism Accounting,

Real Earnings Management, And Information Asymmetry On Share Return. Jiafe

(Jurnal Ilmiah Akuntansi Fakultas Ekonomi). 4(1). pp.9-18.

Van, L. T. H. and et.al, 2021. Financial inclusion and economic growth: An international

evidence. Emerging Markets Finance and Trade. 57(1). pp.239-263.

Xie, J., Nozawa, W., Yagi, M., Fujii, H. and Managi, S., 2019. Do environmental, social, and

governance activities improve corporate financial performance?. Business Strategy and

the Environment. 28(2). pp.286-300.

Begenau, J. and Salomao, J., 2019. Firm financing over the business cycle. The Review of

Financial Studies. 32(4). pp.1235-1274.

Sanfelici, D. and Halbert, L., 2019. Financial market actors as urban policy-makers: the case of

real estate investment trusts in Brazil. Urban Geography. 40(1). pp.83-103.

Khan, M. T. I., Yaseen, M. R. and Ali, Q., 2019. Nexus between financial development, tourism,

renewable energy, and greenhouse gas emission in high-income countries: A continent-

wise analysis. Energy Economics, 83, pp.293-310.

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration. 42(2). pp.119-131.

Fosso Wamba, S. and et.al, 2020. Bitcoin, Blockchain and Fintech: a systematic review and case

studies in the supply chain. Production Planning & Control. 31(2-3). pp.115-142.

9

Books and Journals:

Schaltegger, S., Hörisch, J. and Freeman, R. E., 2019. Business cases for sustainability: A

stakeholder theory perspective. Organization & Environment. 32(3). pp.191-212.

Sugiyanto, S. and Candra, A., 2019. Good Corporate Governance, Conservatism Accounting,

Real Earnings Management, And Information Asymmetry On Share Return. Jiafe

(Jurnal Ilmiah Akuntansi Fakultas Ekonomi). 4(1). pp.9-18.

Van, L. T. H. and et.al, 2021. Financial inclusion and economic growth: An international

evidence. Emerging Markets Finance and Trade. 57(1). pp.239-263.

Xie, J., Nozawa, W., Yagi, M., Fujii, H. and Managi, S., 2019. Do environmental, social, and

governance activities improve corporate financial performance?. Business Strategy and

the Environment. 28(2). pp.286-300.

Begenau, J. and Salomao, J., 2019. Firm financing over the business cycle. The Review of

Financial Studies. 32(4). pp.1235-1274.

Sanfelici, D. and Halbert, L., 2019. Financial market actors as urban policy-makers: the case of

real estate investment trusts in Brazil. Urban Geography. 40(1). pp.83-103.

Khan, M. T. I., Yaseen, M. R. and Ali, Q., 2019. Nexus between financial development, tourism,

renewable energy, and greenhouse gas emission in high-income countries: A continent-

wise analysis. Energy Economics, 83, pp.293-310.

Mnif Sellami, Y. and Gafsi, Y., 2019. Institutional and economic factors affecting the adoption

of international public sector accounting standards. International Journal of Public

Administration. 42(2). pp.119-131.

Fosso Wamba, S. and et.al, 2020. Bitcoin, Blockchain and Fintech: a systematic review and case

studies in the supply chain. Production Planning & Control. 31(2-3). pp.115-142.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

APPENDIX

Income statement:

Balance sheet:

10

Income statement:

Balance sheet:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Business review:

12

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.