Semester 2, ANU FINM 8100: Applied Project in Finance Report

VerifiedAdded on 2022/10/19

|14

|2852

|14

Report

AI Summary

This report provides a comprehensive analysis of an applied finance project, focusing on the prediction of portfolio returns and the methodologies employed. The literature review explores the significance of forecasting returns, the use of multi-beta asset pricing models, and the Capital Asset Pricing Model (CAPM). The report emphasizes the importance of data and sample selection, discussing the sources of predictability in portfolio returns and the limitations of forecasting models. The analysis includes data from 1964 to 1986, demonstrating the variations in predicted returns across different industry groups. The report highlights the impact of assumptions and market conditions on return predictions. The report also delves into the formula for predictable changes and data limitations, providing insights into the challenges and complexities of financial forecasting. The project examines the contributions of the paper, results, and conclusions to provide a complete overview of the subject.

Running head: APPLIED PROJECT OF FINANCE

Applied Project of Finance

Name of the Student:

Name of the University:

Authors Note:

Applied Project of Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

APPLIED PROJECT OF FINANCE

Contents

Literature review:.............................................................................................................................2

Data and sample selection:..............................................................................................................6

Overall evaluation of the report:....................................................................................................11

References:....................................................................................................................................12

APPLIED PROJECT OF FINANCE

Contents

Literature review:.............................................................................................................................2

Data and sample selection:..............................................................................................................6

Overall evaluation of the report:....................................................................................................11

References:....................................................................................................................................12

2

APPLIED PROJECT OF FINANCE

Literature review:

Predicting returns on portfolio is one of the most critical and important aspects in financial

management and portfolio selection. The returns are forecasted on the basis of best available data

and information to select best investment options to maximize the return from a portfolio. The

investors have mainly two objectives these are to achieve maximum returns on the overall

portfolio and to minimize the risk in the overall portfolio. Since, it is not possible to exactly

calculate the returns to be earned on a given portfolio the investors are dependent on the

investment experts’ services to determine the investment portfolio (Almahdi and Yang, 2017).

The investment experts calculate the expected rate of return on a given portfolio along with

expected risk associated with the portfolio to enable the investors to take the final call on the

proportion of investment in different funds in the portfolios of investors.

Sources of predictability in portfolio return discusses the sources that are to be used in predicting

the expected returns in the portfolio of an investor. Now why predicting when all the data and

information about the portfolio is available in front of us. The reason that an investors or an

expert providing investment services can only predict the return on investment portfolio is

because the market is vulnerable and the data used to predict the expected rate of return on

portfolio is the best data available (Berry, 2018). The future condition in the market may well be

same as the data available in the past on the basis of which portfolio returns were calculated

however, it is also a possibility that the future market conditions may change completely and

result in different returns and risk from the portfolios. Thus, it is only possible to predict the

expected rate of return on the basis of best possible data and information available about the

market however, it is not guaranteed that such market conditions will be present in the future

thus, the actual rate of return and risks in investment portfolios could be completely different or

APPLIED PROJECT OF FINANCE

Literature review:

Predicting returns on portfolio is one of the most critical and important aspects in financial

management and portfolio selection. The returns are forecasted on the basis of best available data

and information to select best investment options to maximize the return from a portfolio. The

investors have mainly two objectives these are to achieve maximum returns on the overall

portfolio and to minimize the risk in the overall portfolio. Since, it is not possible to exactly

calculate the returns to be earned on a given portfolio the investors are dependent on the

investment experts’ services to determine the investment portfolio (Almahdi and Yang, 2017).

The investment experts calculate the expected rate of return on a given portfolio along with

expected risk associated with the portfolio to enable the investors to take the final call on the

proportion of investment in different funds in the portfolios of investors.

Sources of predictability in portfolio return discusses the sources that are to be used in predicting

the expected returns in the portfolio of an investor. Now why predicting when all the data and

information about the portfolio is available in front of us. The reason that an investors or an

expert providing investment services can only predict the return on investment portfolio is

because the market is vulnerable and the data used to predict the expected rate of return on

portfolio is the best data available (Berry, 2018). The future condition in the market may well be

same as the data available in the past on the basis of which portfolio returns were calculated

however, it is also a possibility that the future market conditions may change completely and

result in different returns and risk from the portfolios. Thus, it is only possible to predict the

expected rate of return on the basis of best possible data and information available about the

market however, it is not guaranteed that such market conditions will be present in the future

thus, the actual rate of return and risks in investment portfolios could be completely different or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

APPLIED PROJECT OF FINANCE

slightly different or not at all different from the ones predicted earlier. However, since, the

investors are expected to take decisions regarding the proportion of different funds or investment

options in the portfolios they have to rely on the forecast services of the investment experts

(Bornholt, 2016).

The article of sources of predictability in portfolio returns discusses the various underlying

factors and methods used in determination of returns expected to be earned by the investors on

different portfolio. A-multi beta asset pricing model is one of the most popular methods used by

the investors and the experts to forecast the expected rate of return on investments. The

underlying variables used in determination of returns on a portfolio using a multi beta asset

pricing model includes risk factors related to the stock market, inflation which is not expected,

expenditures incurred by consumers, and rate of interests in the market. However, the underlying

variables are constantly changes with slightest of changes in the market position thus, forecasting

and predicting expected rate of return on different investment portfolios are only meant to serve

the investors with possible return and risk interplay on investments (Chen and Anderson, 2018).

Thus, it is important to note that the returns on investment can only be predicted however, since

the prediction is dependent on number of underlying variables which are subjected to

fluctuations with slightest of changes in the market condition thus, it would be impossible predict

the returns from different investment portfolios with cent percent guarantee. This is mainly due

to the ever changing market condition. Thus, the investors would be better served and benefitted

from the investment expert analysis of impact on expected rate of return in case the market

condition changes for better, worse or remain the same. Thus, providing scenario analysis by

using best case, worst case and normal scenario would help investors to make their minds on the

APPLIED PROJECT OF FINANCE

slightly different or not at all different from the ones predicted earlier. However, since, the

investors are expected to take decisions regarding the proportion of different funds or investment

options in the portfolios they have to rely on the forecast services of the investment experts

(Bornholt, 2016).

The article of sources of predictability in portfolio returns discusses the various underlying

factors and methods used in determination of returns expected to be earned by the investors on

different portfolio. A-multi beta asset pricing model is one of the most popular methods used by

the investors and the experts to forecast the expected rate of return on investments. The

underlying variables used in determination of returns on a portfolio using a multi beta asset

pricing model includes risk factors related to the stock market, inflation which is not expected,

expenditures incurred by consumers, and rate of interests in the market. However, the underlying

variables are constantly changes with slightest of changes in the market position thus, forecasting

and predicting expected rate of return on different investment portfolios are only meant to serve

the investors with possible return and risk interplay on investments (Chen and Anderson, 2018).

Thus, it is important to note that the returns on investment can only be predicted however, since

the prediction is dependent on number of underlying variables which are subjected to

fluctuations with slightest of changes in the market condition thus, it would be impossible predict

the returns from different investment portfolios with cent percent guarantee. This is mainly due

to the ever changing market condition. Thus, the investors would be better served and benefitted

from the investment expert analysis of impact on expected rate of return in case the market

condition changes for better, worse or remain the same. Thus, providing scenario analysis by

using best case, worst case and normal scenario would help investors to make their minds on the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

APPLIED PROJECT OF FINANCE

selection of different assets in investment portfolio along with proportion of total investment of

these assets to finalize the investment portfolio.

In a multi-beta asset pricing model the little variation is explained by the market efficiency and

helps the investors in finalizing the investment portfolio assets to complete the portfolio. The

discussion in the article on how both betas and risk premiums changes can be predicted overtime

with the importance of changes in risk premium exceeding that of changes in betas explained

effectively (Davidsson, 2018). The fact that investors are expected to make necessary

amendments to update their assessment of expected returns from investment portfolio is maybe

expecting way too much from ordinary investors if they have already hired the services of

investment experts for portfolio management. It is important to note that not all investors are

expected to have advanced knowledge and understanding of market conditions and can make

necessary changes in the underlying variables to update their assessments of expected return

thus, it is important to assess the impact of market vulnerabilities and provide detailed

information on the expected rate of returns and how these can changes over a period of time to

allow the investors to take important decisions (Ostaszewski, 2017).

The fact that to a large extent the expected rate of return on bond and stock can be predicted is

already known and well documented over the years on number of different literature on finance

and investment. The discussion however, is more about the controversial sources used to predict

the returns on bond and stock than the method used to predict the returns on stock and bond.

Required rates or returns were assumed to be constant in the models used in 1960s and 1970s to

predict the returns on bond and stock. Thus, the fundamental market conditions and underlying

factors used in predicting returns on stock and bond was not correct during the 1960s and 1970s.

The shift in the focus came in 1980s by exposing the economic variation to determine the

APPLIED PROJECT OF FINANCE

selection of different assets in investment portfolio along with proportion of total investment of

these assets to finalize the investment portfolio.

In a multi-beta asset pricing model the little variation is explained by the market efficiency and

helps the investors in finalizing the investment portfolio assets to complete the portfolio. The

discussion in the article on how both betas and risk premiums changes can be predicted overtime

with the importance of changes in risk premium exceeding that of changes in betas explained

effectively (Davidsson, 2018). The fact that investors are expected to make necessary

amendments to update their assessment of expected returns from investment portfolio is maybe

expecting way too much from ordinary investors if they have already hired the services of

investment experts for portfolio management. It is important to note that not all investors are

expected to have advanced knowledge and understanding of market conditions and can make

necessary changes in the underlying variables to update their assessments of expected return

thus, it is important to assess the impact of market vulnerabilities and provide detailed

information on the expected rate of returns and how these can changes over a period of time to

allow the investors to take important decisions (Ostaszewski, 2017).

The fact that to a large extent the expected rate of return on bond and stock can be predicted is

already known and well documented over the years on number of different literature on finance

and investment. The discussion however, is more about the controversial sources used to predict

the returns on bond and stock than the method used to predict the returns on stock and bond.

Required rates or returns were assumed to be constant in the models used in 1960s and 1970s to

predict the returns on bond and stock. Thus, the fundamental market conditions and underlying

factors used in predicting returns on stock and bond was not correct during the 1960s and 1970s.

The shift in the focus came in 1980s by exposing the economic variation to determine the

5

APPLIED PROJECT OF FINANCE

changes in expected rate of return over a time period. Thus, allowing the required rate of return

to experience the changes in market condition allowed the investors’ broader range of

information as the investors understood the expected impact of changes in market condition on

the expected rate of return on investment portfolio. However, despite allowing required rate of

returns for exposure to economic risk to vary over time in the 1980s the controversy surrounding

the predictability of returns continued without showing any sign of stopping. Thus, evaluation of

methods to be used to calculate the expected rate of returns continued. The experts have varied

opinion on the market rate of return as some attributed the concept of predictability as prone to

changes with market inefficiencies whereas others defined it as rational updating of required rate

of returns on the basis of investors assessment of different market conditions (Zdorovenin and

Pezier, 2017).

Methodology used in predictable changes as per the analysis of investment experts have been

illustrated using the following formula;

The use of multiple beta, APT type models are supported by extensive research on predictability

of returns. The contemporary practice is represented in the above formula and in using the beta

and APT models. A representative model uses return on data, expected cost of equity, risk free

rate of return and market premium to calculate the expected rate of return on investment

portfolios. Predicting returns using capital asset pricing model (CAPM) further states the

importance of risk free rate of return, market premium for risk undertaken and beta factors to

APPLIED PROJECT OF FINANCE

changes in expected rate of return over a time period. Thus, allowing the required rate of return

to experience the changes in market condition allowed the investors’ broader range of

information as the investors understood the expected impact of changes in market condition on

the expected rate of return on investment portfolio. However, despite allowing required rate of

returns for exposure to economic risk to vary over time in the 1980s the controversy surrounding

the predictability of returns continued without showing any sign of stopping. Thus, evaluation of

methods to be used to calculate the expected rate of returns continued. The experts have varied

opinion on the market rate of return as some attributed the concept of predictability as prone to

changes with market inefficiencies whereas others defined it as rational updating of required rate

of returns on the basis of investors assessment of different market conditions (Zdorovenin and

Pezier, 2017).

Methodology used in predictable changes as per the analysis of investment experts have been

illustrated using the following formula;

The use of multiple beta, APT type models are supported by extensive research on predictability

of returns. The contemporary practice is represented in the above formula and in using the beta

and APT models. A representative model uses return on data, expected cost of equity, risk free

rate of return and market premium to calculate the expected rate of return on investment

portfolios. Predicting returns using capital asset pricing model (CAPM) further states the

importance of risk free rate of return, market premium for risk undertaken and beta factors to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

APPLIED PROJECT OF FINANCE

determine the expected rate of return. However, the difference between the market rate of return

and expected rate of return also need to be understood here (Zhang, 2017).

Data and sample selection:

The data and sample selection covers the range of data selected in predicting the expected rate of

return on different stock and bonds. The researchers has used a gamut of data from different

sources to expand the depth of the research. Considering the importance of the research it was

essential to select appropriate data to ensure that the research is effective useful for the readers.

Earlier it was said that returns on assets are unpredictable however, research such as this have

proven that to a large extent research can be predicted provided the data used are authentic and

correct. In this research the importance of data selection to the final outcome in predicting

expected return has been explained with the help of different data.

In order to explain the concept of predictability of returns and sources of predictability the

research has gathered monthly portfolio return from 1964 to 1986 on different industries. The

selection of this data has been specifically made to discuss the probability of capital asset pricing

model, beta pricing model and other such models to correctly assess the expected rate of returns

on different assets and portfolios by using available information. Nowhere the research has

claimed that the predicted returns would be cent percent correct however, the possibility of

correctly predicting the rate of returns on different portfolios and assets is quite bright by

selecting correct data and using proper methods.

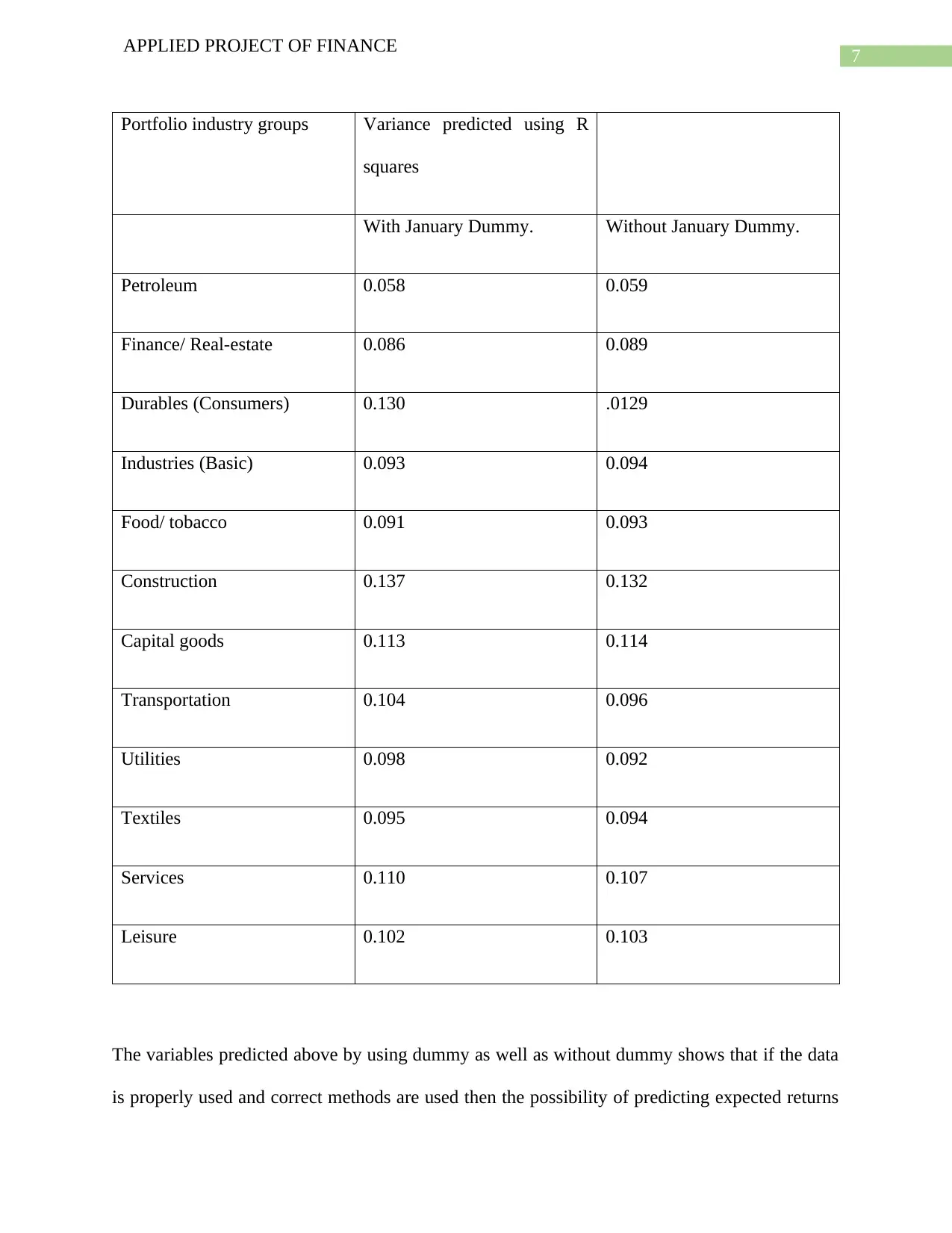

In predicting monthly returns on portfolios between 1964 and 1986 the researcher used

proportion of variance by adjusting R squares. Adjusting data with dummy and without dummy

in January showed the following variations

APPLIED PROJECT OF FINANCE

determine the expected rate of return. However, the difference between the market rate of return

and expected rate of return also need to be understood here (Zhang, 2017).

Data and sample selection:

The data and sample selection covers the range of data selected in predicting the expected rate of

return on different stock and bonds. The researchers has used a gamut of data from different

sources to expand the depth of the research. Considering the importance of the research it was

essential to select appropriate data to ensure that the research is effective useful for the readers.

Earlier it was said that returns on assets are unpredictable however, research such as this have

proven that to a large extent research can be predicted provided the data used are authentic and

correct. In this research the importance of data selection to the final outcome in predicting

expected return has been explained with the help of different data.

In order to explain the concept of predictability of returns and sources of predictability the

research has gathered monthly portfolio return from 1964 to 1986 on different industries. The

selection of this data has been specifically made to discuss the probability of capital asset pricing

model, beta pricing model and other such models to correctly assess the expected rate of returns

on different assets and portfolios by using available information. Nowhere the research has

claimed that the predicted returns would be cent percent correct however, the possibility of

correctly predicting the rate of returns on different portfolios and assets is quite bright by

selecting correct data and using proper methods.

In predicting monthly returns on portfolios between 1964 and 1986 the researcher used

proportion of variance by adjusting R squares. Adjusting data with dummy and without dummy

in January showed the following variations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

APPLIED PROJECT OF FINANCE

Portfolio industry groups Variance predicted using R

squares

With January Dummy. Without January Dummy.

Petroleum 0.058 0.059

Finance/ Real-estate 0.086 0.089

Durables (Consumers) 0.130 .0129

Industries (Basic) 0.093 0.094

Food/ tobacco 0.091 0.093

Construction 0.137 0.132

Capital goods 0.113 0.114

Transportation 0.104 0.096

Utilities 0.098 0.092

Textiles 0.095 0.094

Services 0.110 0.107

Leisure 0.102 0.103

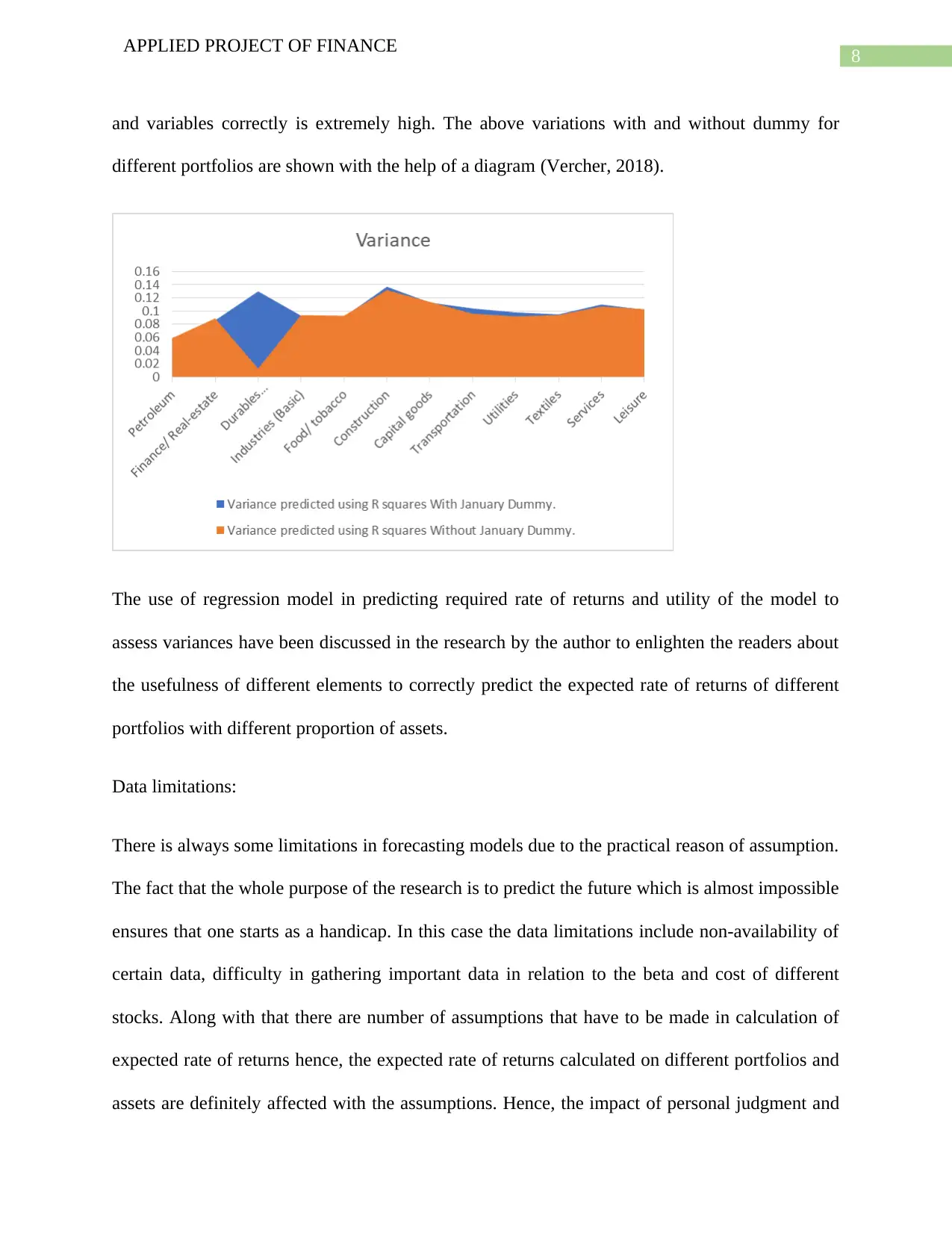

The variables predicted above by using dummy as well as without dummy shows that if the data

is properly used and correct methods are used then the possibility of predicting expected returns

APPLIED PROJECT OF FINANCE

Portfolio industry groups Variance predicted using R

squares

With January Dummy. Without January Dummy.

Petroleum 0.058 0.059

Finance/ Real-estate 0.086 0.089

Durables (Consumers) 0.130 .0129

Industries (Basic) 0.093 0.094

Food/ tobacco 0.091 0.093

Construction 0.137 0.132

Capital goods 0.113 0.114

Transportation 0.104 0.096

Utilities 0.098 0.092

Textiles 0.095 0.094

Services 0.110 0.107

Leisure 0.102 0.103

The variables predicted above by using dummy as well as without dummy shows that if the data

is properly used and correct methods are used then the possibility of predicting expected returns

8

APPLIED PROJECT OF FINANCE

and variables correctly is extremely high. The above variations with and without dummy for

different portfolios are shown with the help of a diagram (Vercher, 2018).

The use of regression model in predicting required rate of returns and utility of the model to

assess variances have been discussed in the research by the author to enlighten the readers about

the usefulness of different elements to correctly predict the expected rate of returns of different

portfolios with different proportion of assets.

Data limitations:

There is always some limitations in forecasting models due to the practical reason of assumption.

The fact that the whole purpose of the research is to predict the future which is almost impossible

ensures that one starts as a handicap. In this case the data limitations include non-availability of

certain data, difficulty in gathering important data in relation to the beta and cost of different

stocks. Along with that there are number of assumptions that have to be made in calculation of

expected rate of returns hence, the expected rate of returns calculated on different portfolios and

assets are definitely affected with the assumptions. Hence, the impact of personal judgment and

APPLIED PROJECT OF FINANCE

and variables correctly is extremely high. The above variations with and without dummy for

different portfolios are shown with the help of a diagram (Vercher, 2018).

The use of regression model in predicting required rate of returns and utility of the model to

assess variances have been discussed in the research by the author to enlighten the readers about

the usefulness of different elements to correctly predict the expected rate of returns of different

portfolios with different proportion of assets.

Data limitations:

There is always some limitations in forecasting models due to the practical reason of assumption.

The fact that the whole purpose of the research is to predict the future which is almost impossible

ensures that one starts as a handicap. In this case the data limitations include non-availability of

certain data, difficulty in gathering important data in relation to the beta and cost of different

stocks. Along with that there are number of assumptions that have to be made in calculation of

expected rate of returns hence, the expected rate of returns calculated on different portfolios and

assets are definitely affected with the assumptions. Hence, the impact of personal judgment and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

APPLIED PROJECT OF FINANCE

biased certainly contribute to the overall limitation of different models used to calculate rate of

return expected to be earned on portfolios and assets (Markovich & Plazzi, 2017).

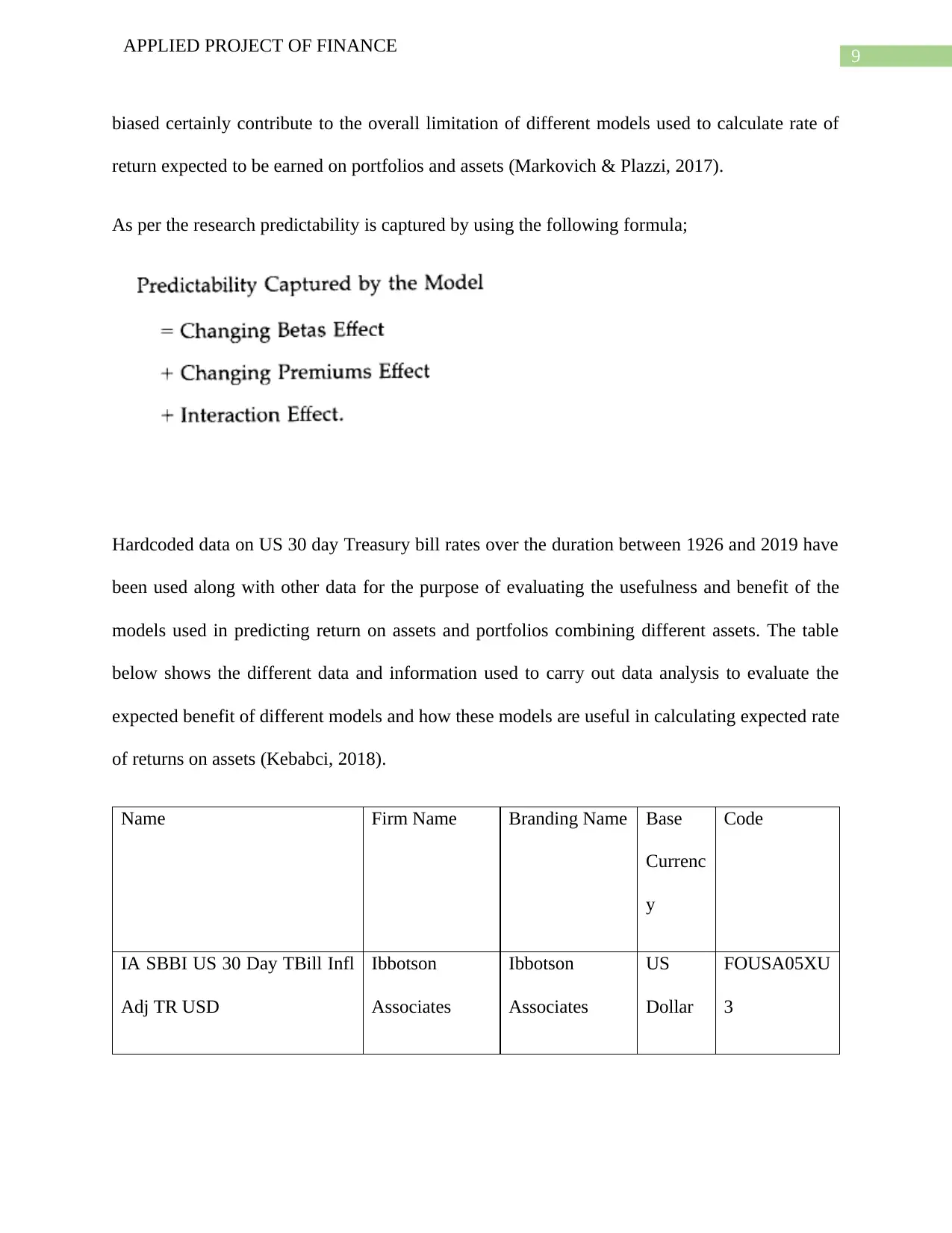

As per the research predictability is captured by using the following formula;

Hardcoded data on US 30 day Treasury bill rates over the duration between 1926 and 2019 have

been used along with other data for the purpose of evaluating the usefulness and benefit of the

models used in predicting return on assets and portfolios combining different assets. The table

below shows the different data and information used to carry out data analysis to evaluate the

expected benefit of different models and how these models are useful in calculating expected rate

of returns on assets (Kebabci, 2018).

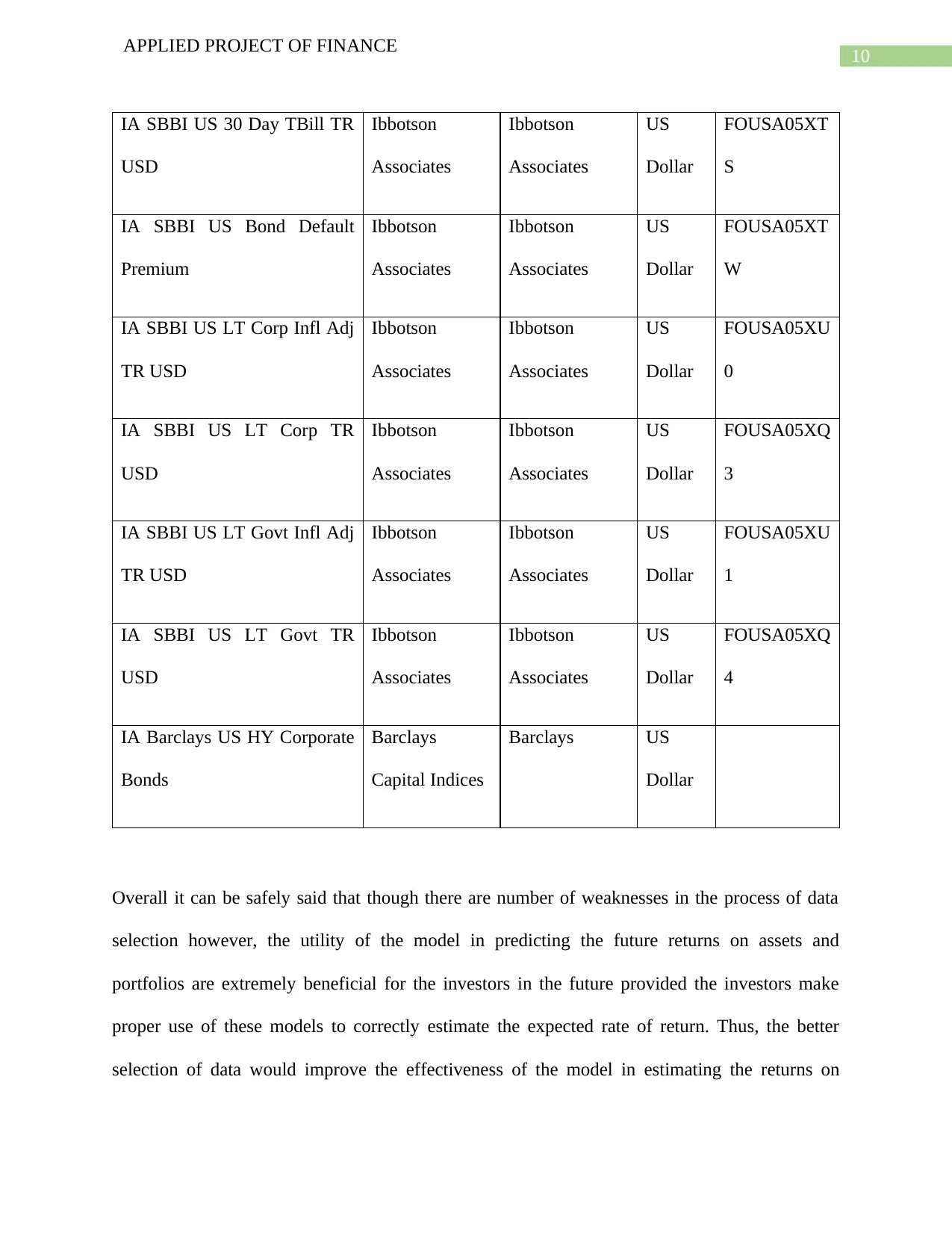

Name Firm Name Branding Name Base

Currenc

y

Code

IA SBBI US 30 Day TBill Infl

Adj TR USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XU

3

APPLIED PROJECT OF FINANCE

biased certainly contribute to the overall limitation of different models used to calculate rate of

return expected to be earned on portfolios and assets (Markovich & Plazzi, 2017).

As per the research predictability is captured by using the following formula;

Hardcoded data on US 30 day Treasury bill rates over the duration between 1926 and 2019 have

been used along with other data for the purpose of evaluating the usefulness and benefit of the

models used in predicting return on assets and portfolios combining different assets. The table

below shows the different data and information used to carry out data analysis to evaluate the

expected benefit of different models and how these models are useful in calculating expected rate

of returns on assets (Kebabci, 2018).

Name Firm Name Branding Name Base

Currenc

y

Code

IA SBBI US 30 Day TBill Infl

Adj TR USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XU

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

APPLIED PROJECT OF FINANCE

IA SBBI US 30 Day TBill TR

USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XT

S

IA SBBI US Bond Default

Premium

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XT

W

IA SBBI US LT Corp Infl Adj

TR USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XU

0

IA SBBI US LT Corp TR

USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XQ

3

IA SBBI US LT Govt Infl Adj

TR USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XU

1

IA SBBI US LT Govt TR

USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XQ

4

IA Barclays US HY Corporate

Bonds

Barclays

Capital Indices

Barclays US

Dollar

Overall it can be safely said that though there are number of weaknesses in the process of data

selection however, the utility of the model in predicting the future returns on assets and

portfolios are extremely beneficial for the investors in the future provided the investors make

proper use of these models to correctly estimate the expected rate of return. Thus, the better

selection of data would improve the effectiveness of the model in estimating the returns on

APPLIED PROJECT OF FINANCE

IA SBBI US 30 Day TBill TR

USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XT

S

IA SBBI US Bond Default

Premium

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XT

W

IA SBBI US LT Corp Infl Adj

TR USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XU

0

IA SBBI US LT Corp TR

USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XQ

3

IA SBBI US LT Govt Infl Adj

TR USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XU

1

IA SBBI US LT Govt TR

USD

Ibbotson

Associates

Ibbotson

Associates

US

Dollar

FOUSA05XQ

4

IA Barclays US HY Corporate

Bonds

Barclays

Capital Indices

Barclays US

Dollar

Overall it can be safely said that though there are number of weaknesses in the process of data

selection however, the utility of the model in predicting the future returns on assets and

portfolios are extremely beneficial for the investors in the future provided the investors make

proper use of these models to correctly estimate the expected rate of return. Thus, the better

selection of data would improve the effectiveness of the model in estimating the returns on

11

APPLIED PROJECT OF FINANCE

different assets and portfolios to take important investment related decision (Ke, Kelly & Xiu,

2019).

Overall evaluation of the report:

The report clearly identifies the number of different aspects and elements that are directly related

to the returns on investment portfolios. The investors as well as the experts providing investment

analysis must consider each and every single factor to follow the correct method to predict the

expected rate of return on different investment portfolios containing different funds and assets in

different proportion as per the wish and desire of investors.

APPLIED PROJECT OF FINANCE

different assets and portfolios to take important investment related decision (Ke, Kelly & Xiu,

2019).

Overall evaluation of the report:

The report clearly identifies the number of different aspects and elements that are directly related

to the returns on investment portfolios. The investors as well as the experts providing investment

analysis must consider each and every single factor to follow the correct method to predict the

expected rate of return on different investment portfolios containing different funds and assets in

different proportion as per the wish and desire of investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.