Applied Income Tax: Comprehensive Analysis for Assessment 2 Part A

VerifiedAdded on 2023/06/10

|6

|581

|467

Homework Assignment

AI Summary

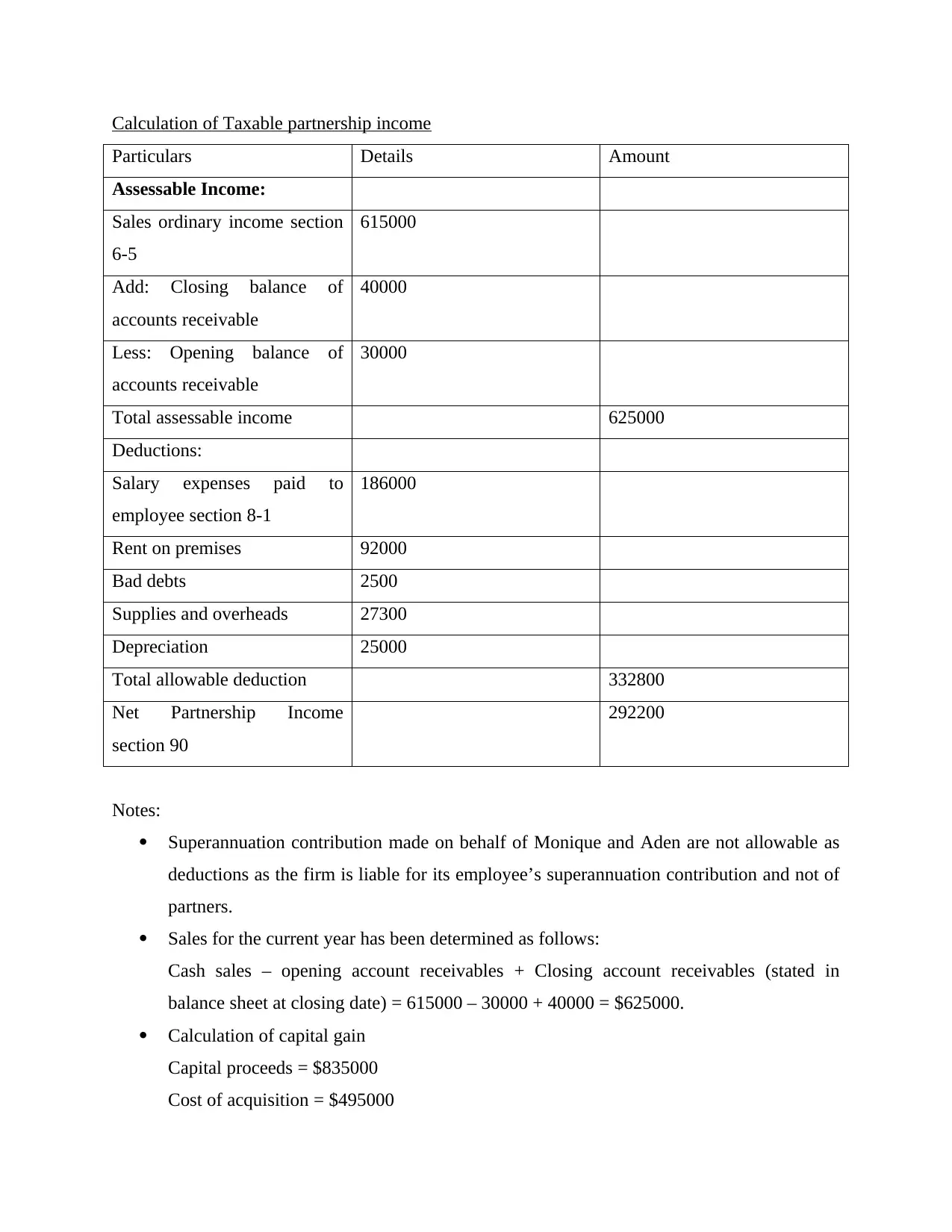

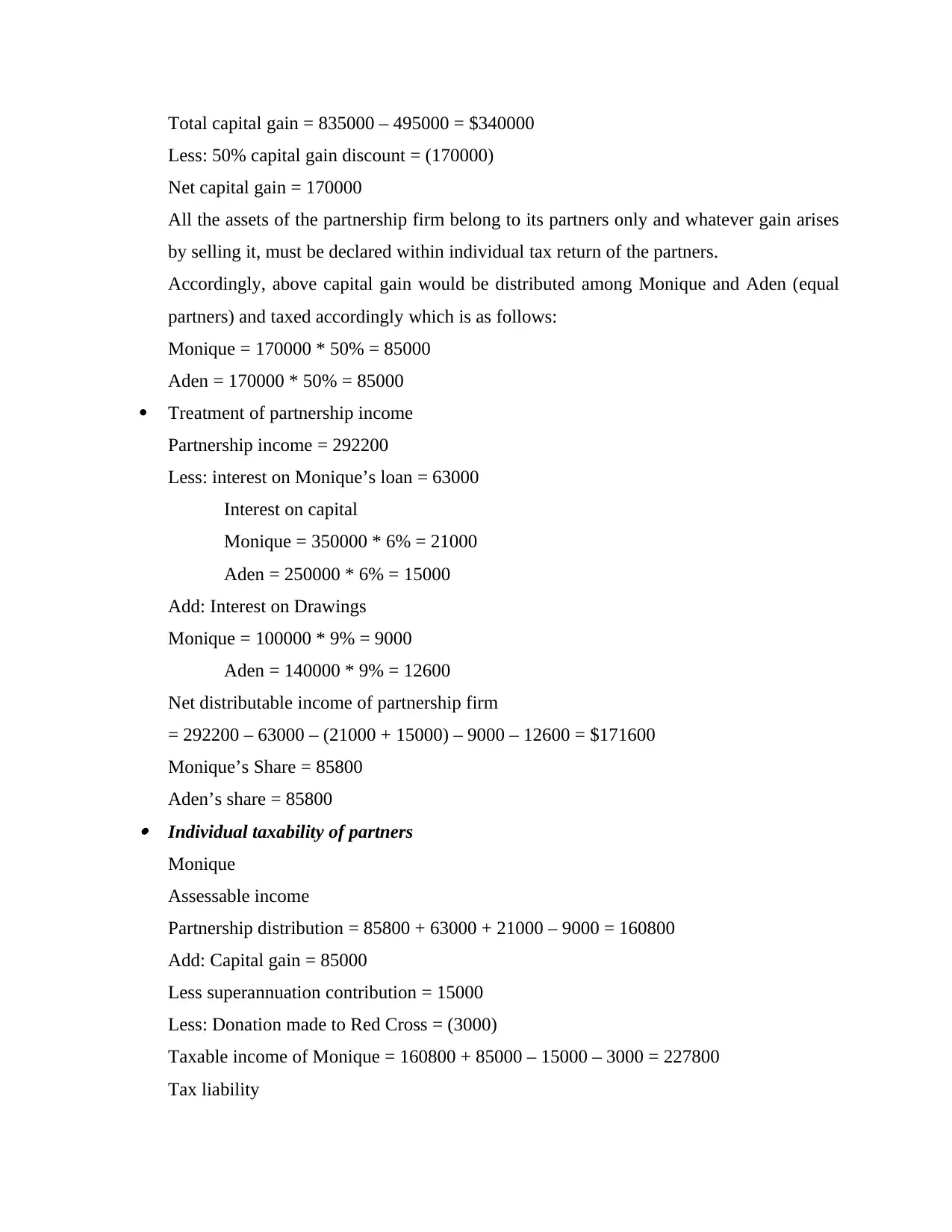

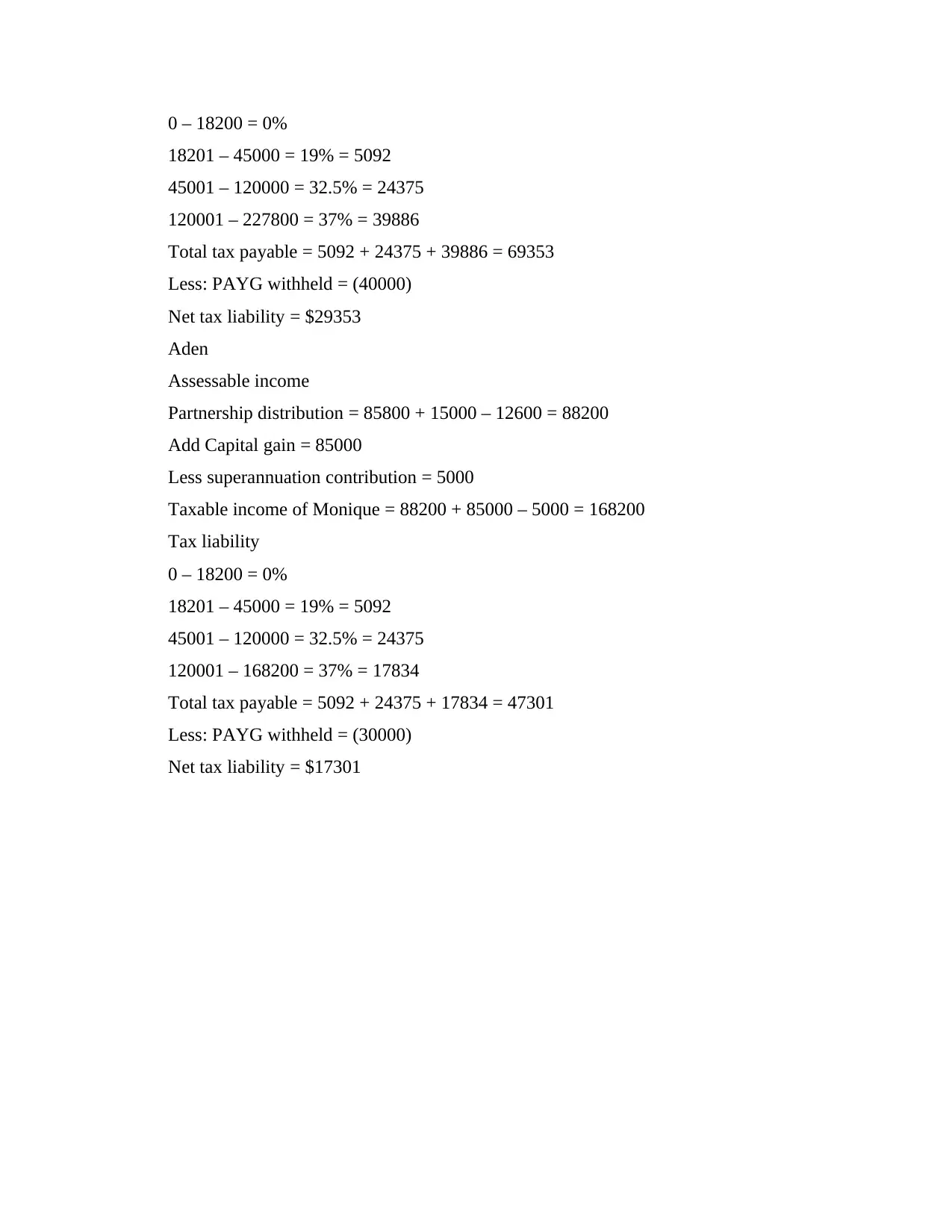

This document presents a comprehensive solution to an applied income tax assessment, focusing on the calculation of taxable income for a partnership and the individual tax liabilities of its partners, Monique and Aden. The assessment includes detailed calculations of assessable income, deductions, and net partnership income. It addresses specific items such as salary expenses, rent, bad debts, depreciation, and capital gains. The solution thoroughly analyzes the distribution of partnership income, considering interest on loans and drawings. Furthermore, it determines the individual taxable income for each partner, factoring in partnership distributions, capital gains, and other relevant deductions. The document then calculates the tax liability for each partner based on the provided tax brackets and PAYG withheld, concluding with the net tax payable or refundable for each individual. This solution demonstrates a clear understanding of tax principles and their application in a partnership scenario.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.