Audit Planning and Internal Control: Arafura Resources Limited Report

VerifiedAdded on 2021/06/17

|18

|3563

|70

Report

AI Summary

This report provides a comprehensive audit analysis of Arafura Resources Limited, examining its financial statements, business transactions, and investment activities. It delves into the company's financial reporting practices, including compliance with AASB 101 and the use of analytical procedures over a three-year period. The report identifies material account balances, assesses relevant financial report assertions, and outlines audit work steps to mitigate risks. Furthermore, it includes a ratio analysis of liquidity, solvency, profitability, and efficiency, highlighting key financial trends and potential risks. The report also considers the company's investments in research and development, financing activities, and the role of internal controls in determining material account considerations. The audit focuses on evaluating the company's financial health and ensuring adherence to financial reporting standards and regulations. This report is contributed by a student and available on Desklib, a platform offering AI-powered study tools and resources for students, including past papers and solved assignments.

ARAFURA Resources Limited

Audit assurance and

practice

Audit Planning and Internal Control

Name of the Author

Audit assurance and

practice

Audit Planning and Internal Control

Name of the Author

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

With the changes in economic condition and increased complexity of the financial

reporting frameworks, every company needs to audit its financial statements with the

auditors. In this report, in order to conduct the audit and assurance, Arafura Resources

Limited has been taken into consideration. There are several financial tools and audit

assurance procedure have been taken which reflects that company has complied with all the

rules an regulation and established harmonization in domestic and international regulations.

With the changes in economic condition and increased complexity of the financial

reporting frameworks, every company needs to audit its financial statements with the

auditors. In this report, in order to conduct the audit and assurance, Arafura Resources

Limited has been taken into consideration. There are several financial tools and audit

assurance procedure have been taken which reflects that company has complied with all the

rules an regulation and established harmonization in domestic and international regulations.

Table of Contents

EXECUTIVE SUMMARY...........................................................................................................................1

Introduction...........................................................................................................................................3

Description of ARAFURA Resources Limited......................................................................................3

Understand the nature of the entity and its industry............................................................................3

Business Transactions of the company..............................................................................................3

Investments and investment activities..............................................................................................3

Financing and financing activities......................................................................................................3

Financial reporting practices..............................................................................................................4

Analytical procedures of the Statement of Financial Position and of Financial Performance over the

last three years......................................................................................................................................4

Consideration of the account balances are considered “material”.......................................................4

Ten different material account balances, five assets and five liabilities................................................6

List the relevant financial report assertions and explain why the selected assertions are applicable to

each account..........................................................................................................................................7

Comprehensive set of audit work steps for each material account balance.........................................8

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

EXECUTIVE SUMMARY...........................................................................................................................1

Introduction...........................................................................................................................................3

Description of ARAFURA Resources Limited......................................................................................3

Understand the nature of the entity and its industry............................................................................3

Business Transactions of the company..............................................................................................3

Investments and investment activities..............................................................................................3

Financing and financing activities......................................................................................................3

Financial reporting practices..............................................................................................................4

Analytical procedures of the Statement of Financial Position and of Financial Performance over the

last three years......................................................................................................................................4

Consideration of the account balances are considered “material”.......................................................4

Ten different material account balances, five assets and five liabilities................................................6

List the relevant financial report assertions and explain why the selected assertions are applicable to

each account..........................................................................................................................................7

Comprehensive set of audit work steps for each material account balance.........................................8

Conclusion.............................................................................................................................................8

References.............................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The substantive tests are the balances that are used to decrease the threats of the audit

risks. The internal control system helps to determine material consideration of account

balances. It is considered that Arafira Resources Limited has been taken into consideration to

evaluate whether company has been facing high loss in its business.

Description of ARAFURA Resources Limited

Arafira Resources Limited is the mineral extraction company which has been running

its business in Australia. This business has been planned to implement the rarest of the rare

minerals of earth. The main headquartered of company is in Perth, Western Australia. This

company is listed in the Australian Stock exchange (ARAFURA Resources Limited, 2017).

Understand the nature of the entity and its industry

Business Transactions of the company

It is evaluated that the auditors of the company are more worried about the over value

statement and less value in the books of statement. There are several test such as substantive

test, assertive test and audit program have been used to evaluate the business business

transaction of the company. The test balance is used to evaluate the balance of accounts

maintained in the business transactions.

With the business transactions of company is accompanied with the extraction of the rarest of

the rare minerals present on this earth. This company is the permanent supplier of

Neodymium and Praseodymium from the Noland which is the biggest project of company.

The busienss project of Company is situated in the northwest territory of Australia.

The mineral tenure project is secured by the three major extraction licenses which are applied

on four mineral leases (ARAFURA Resources Limited, 2017).

Investments and investment activities

In 2015, company had invested in the mineral production around $110,010. The payments for

extraction and evaluation amounted to $

The substantive tests are the balances that are used to decrease the threats of the audit

risks. The internal control system helps to determine material consideration of account

balances. It is considered that Arafira Resources Limited has been taken into consideration to

evaluate whether company has been facing high loss in its business.

Description of ARAFURA Resources Limited

Arafira Resources Limited is the mineral extraction company which has been running

its business in Australia. This business has been planned to implement the rarest of the rare

minerals of earth. The main headquartered of company is in Perth, Western Australia. This

company is listed in the Australian Stock exchange (ARAFURA Resources Limited, 2017).

Understand the nature of the entity and its industry

Business Transactions of the company

It is evaluated that the auditors of the company are more worried about the over value

statement and less value in the books of statement. There are several test such as substantive

test, assertive test and audit program have been used to evaluate the business business

transaction of the company. The test balance is used to evaluate the balance of accounts

maintained in the business transactions.

With the business transactions of company is accompanied with the extraction of the rarest of

the rare minerals present on this earth. This company is the permanent supplier of

Neodymium and Praseodymium from the Noland which is the biggest project of company.

The busienss project of Company is situated in the northwest territory of Australia.

The mineral tenure project is secured by the three major extraction licenses which are applied

on four mineral leases (ARAFURA Resources Limited, 2017).

Investments and investment activities

In 2015, company had invested in the mineral production around $110,010. The payments for

extraction and evaluation amounted to $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The payment for the extraction of mineral has being AUD $ 6,189,149 (ARAFURA

Resources Limited, 2017).

Company has invested $2,263,935 in its research and development department which

increase the long term benefit program of organization.

The net cash outflow from the investing activities of Arafura Resources Limited, $4,035,224

(ARAFURA Resources Limited, 2015).

In 2016, Arafura Resources Limited had invested capital of $523 in property, plant and

machinery. The current extraction of Arafura Resources Limited is to $4,072,639.

The expenses and investment of Arafura Resources Limited is $51,229 which eventually

increases the cash outflow of $1,608,469 (ARAFURA Resources Limited, 2016).

Arafura Resources Limited invested $55396 in 2017 in plants and machineries and deployed

more funds in its assets amounting to $3,364,107.

The current investment of Arafura Resources Limited in 2017 is $ 182500 as provision for

lease incentive in 2015 and $ 421,693 as lease investment (ARAFURA Resources Limited,

2017).

Financing and financing activities

In 2017, Company has increased its investment in research and development department

amounting to $6,764,740. On the other hand, the transaction cost is around $ $309,099 as

transaction costs of the shares

The total equity share of Arafura Resources Limited is $130,385,162 in 2015. The company

has increased its equity funding by $ 3.6 Million by using the investment of the institutional

investors (ARAFURA Resources Limited, 2017).

Financial reporting practices

Company has complied with the AASB 101 for the presentation of the financial

statement. It states that the company must ensure that its assets are accounted at their

recoverable amounts by using the assertion test and complied with the IAS 136. It implies

that the company has invested more capital in its current assets which will block high cost of

Resources Limited, 2017).

Company has invested $2,263,935 in its research and development department which

increase the long term benefit program of organization.

The net cash outflow from the investing activities of Arafura Resources Limited, $4,035,224

(ARAFURA Resources Limited, 2015).

In 2016, Arafura Resources Limited had invested capital of $523 in property, plant and

machinery. The current extraction of Arafura Resources Limited is to $4,072,639.

The expenses and investment of Arafura Resources Limited is $51,229 which eventually

increases the cash outflow of $1,608,469 (ARAFURA Resources Limited, 2016).

Arafura Resources Limited invested $55396 in 2017 in plants and machineries and deployed

more funds in its assets amounting to $3,364,107.

The current investment of Arafura Resources Limited in 2017 is $ 182500 as provision for

lease incentive in 2015 and $ 421,693 as lease investment (ARAFURA Resources Limited,

2017).

Financing and financing activities

In 2017, Company has increased its investment in research and development department

amounting to $6,764,740. On the other hand, the transaction cost is around $ $309,099 as

transaction costs of the shares

The total equity share of Arafura Resources Limited is $130,385,162 in 2015. The company

has increased its equity funding by $ 3.6 Million by using the investment of the institutional

investors (ARAFURA Resources Limited, 2017).

Financial reporting practices

Company has complied with the AASB 101 for the presentation of the financial

statement. It states that the company must ensure that its assets are accounted at their

recoverable amounts by using the assertion test and complied with the IAS 136. It implies

that the company has invested more capital in its current assets which will block high cost of

capital resulting in high cost of production. The company should deploy its funds from the

current assets to pay its current liabilities Arafura Resources Limited should increase the

overall turnover and transparency of its business if it wants to win over the market as

compared to other rivals by establishing harmonization in its domestic and international

reporting frameworks. Furthermore, financial assertions of the various material account

balances shall be executed. Lastly, the various steps of audit for each material account of the

company shall be designed. The accounts of company are audited by BDO audit (WA)

Private Limited (ARAFURA Resources Limited, 2017).

Analytical procedures of the Statement of Financial

Position and of Financial Performance over the last

three years

Ratio Analysis

Liquidity ratio

The liquidity ratio of company reflects that

company has maintained effective cash in its

business. The current ratio of company was

11.47 in 2015 which has increased to 12.70

in 2016. The quick ratio of company in 2015

is 12.70 which are already way too high and

company has also increased this ratio to

12.81 points in 2017.

Solvency ratio

The financial leverage of the company is

same in all the years viz. 2015, 2016 and

2017 i.e. 1.01 which is more than 0.5 which

is an ideal figure. The company has financed

more assets through its debt which are to be

repaid back. Larger debt loads makes the

company vulnerable during the economic

downturn. In case the company is not able to

make consistent interest payments, then the

investors are likely to lose confidence in it.

current assets to pay its current liabilities Arafura Resources Limited should increase the

overall turnover and transparency of its business if it wants to win over the market as

compared to other rivals by establishing harmonization in its domestic and international

reporting frameworks. Furthermore, financial assertions of the various material account

balances shall be executed. Lastly, the various steps of audit for each material account of the

company shall be designed. The accounts of company are audited by BDO audit (WA)

Private Limited (ARAFURA Resources Limited, 2017).

Analytical procedures of the Statement of Financial

Position and of Financial Performance over the last

three years

Ratio Analysis

Liquidity ratio

The liquidity ratio of company reflects that

company has maintained effective cash in its

business. The current ratio of company was

11.47 in 2015 which has increased to 12.70

in 2016. The quick ratio of company in 2015

is 12.70 which are already way too high and

company has also increased this ratio to

12.81 points in 2017.

Solvency ratio

The financial leverage of the company is

same in all the years viz. 2015, 2016 and

2017 i.e. 1.01 which is more than 0.5 which

is an ideal figure. The company has financed

more assets through its debt which are to be

repaid back. Larger debt loads makes the

company vulnerable during the economic

downturn. In case the company is not able to

make consistent interest payments, then the

investors are likely to lose confidence in it.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As a result, the share prices can go down

Profitability ratio

The profitability ratio shows company’s

ability to earn profit on the investment. Even

after new contracts have been entered, the

ratios have fallen; the reason may certainly

be the downfall in the prices due to high

competition and the severe downfall in the

mining industry. Even when the gold and

coal industries have seen a rise in the recent

year, but the iron industry remains at crash.

ARAFURA Resources Limited stands at the

risk to lose market share in the above

discussed industries due to heavy

competition or could lose the edge to bargain

for high lease income from the new potential

clients (Argenti, 2016).

Efficiency ratio

Anything that amounts to outflow or inflow

of cash is recorded. Income tax paid is an

item of cash flow statement and only

represents the amount of cash paid to the

income tax authorities for tax calls, be it for

current, previous or future periods. While,

the current tax expense relates to the tax

expense for current year itself (Arens, Elder,

and Mark, 2012).

Profitability ratio

The profitability ratio shows company’s

ability to earn profit on the investment. Even

after new contracts have been entered, the

ratios have fallen; the reason may certainly

be the downfall in the prices due to high

competition and the severe downfall in the

mining industry. Even when the gold and

coal industries have seen a rise in the recent

year, but the iron industry remains at crash.

ARAFURA Resources Limited stands at the

risk to lose market share in the above

discussed industries due to heavy

competition or could lose the edge to bargain

for high lease income from the new potential

clients (Argenti, 2016).

Efficiency ratio

Anything that amounts to outflow or inflow

of cash is recorded. Income tax paid is an

item of cash flow statement and only

represents the amount of cash paid to the

income tax authorities for tax calls, be it for

current, previous or future periods. While,

the current tax expense relates to the tax

expense for current year itself (Arens, Elder,

and Mark, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Consideration of the account balances are considered

“material”

The account balance material consideration are done to make the presentation accrues to the

share of total comprehensive income formulated by the continuing operations

The internal control system helps to determine material consideration of account balances. It

refers to the technique that is used by the organizations to ensure that the risk flying over the

entity can be mitigated. There are various accounts are considered as material which are as

follows

Receivables

Lease undertaken

Hire purchase

Machines

Investment in mining business

Creditors

Lease payment

Lease

Bank loan

The consideration of accounts as material account is determined on the basis of the flow of

cash as per requirement and the risk for the same (Argenti, 2016).

“material”

The account balance material consideration are done to make the presentation accrues to the

share of total comprehensive income formulated by the continuing operations

The internal control system helps to determine material consideration of account balances. It

refers to the technique that is used by the organizations to ensure that the risk flying over the

entity can be mitigated. There are various accounts are considered as material which are as

follows

Receivables

Lease undertaken

Hire purchase

Machines

Investment in mining business

Creditors

Lease payment

Lease

Bank loan

The consideration of accounts as material account is determined on the basis of the flow of

cash as per requirement and the risk for the same (Argenti, 2016).

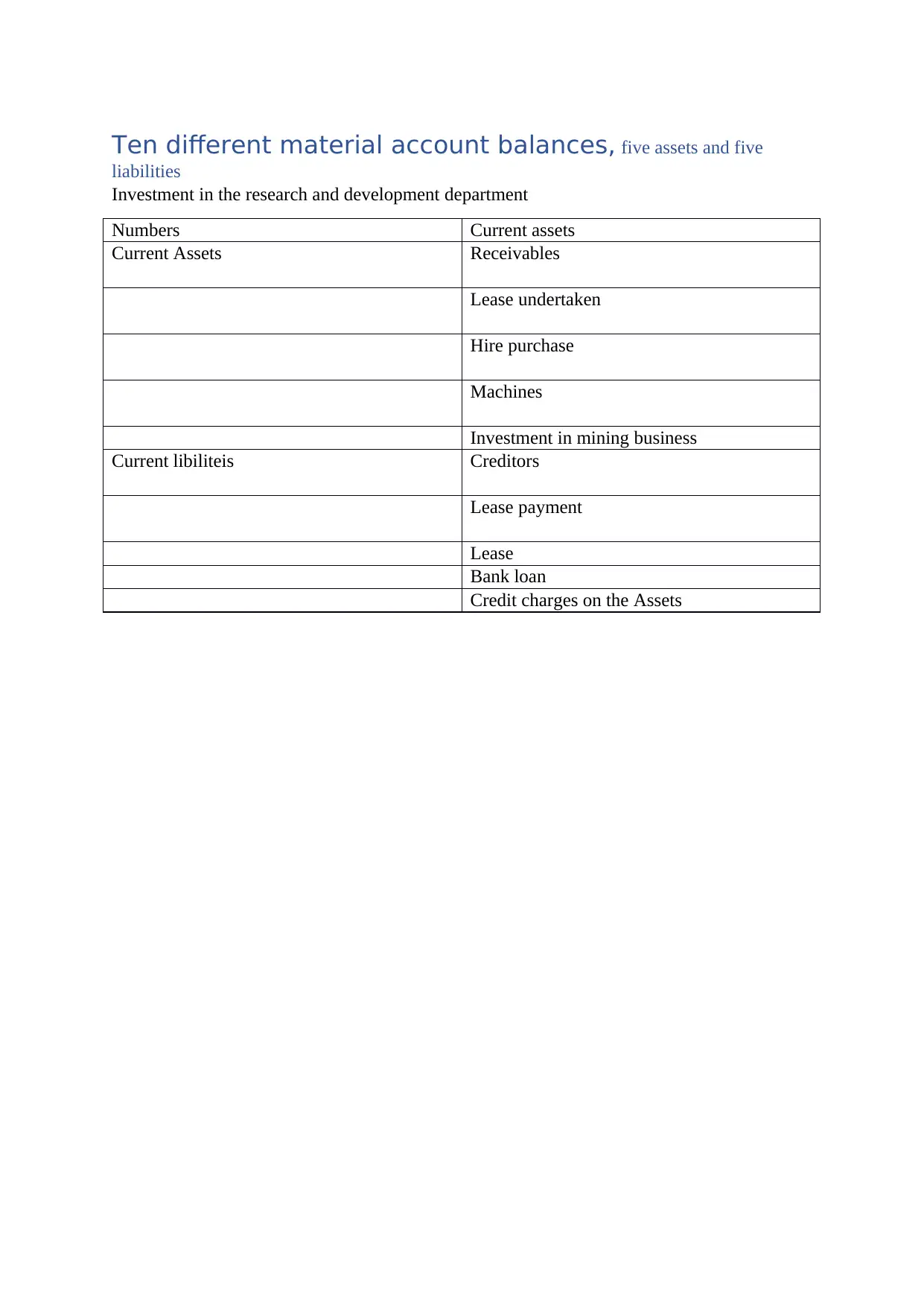

Ten different material account balances, five assets and five

liabilities

Investment in the research and development department

Numbers Current assets

Current Assets Receivables

Lease undertaken

Hire purchase

Machines

Investment in mining business

Current libiliteis Creditors

Lease payment

Lease

Bank loan

Credit charges on the Assets

liabilities

Investment in the research and development department

Numbers Current assets

Current Assets Receivables

Lease undertaken

Hire purchase

Machines

Investment in mining business

Current libiliteis Creditors

Lease payment

Lease

Bank loan

Credit charges on the Assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

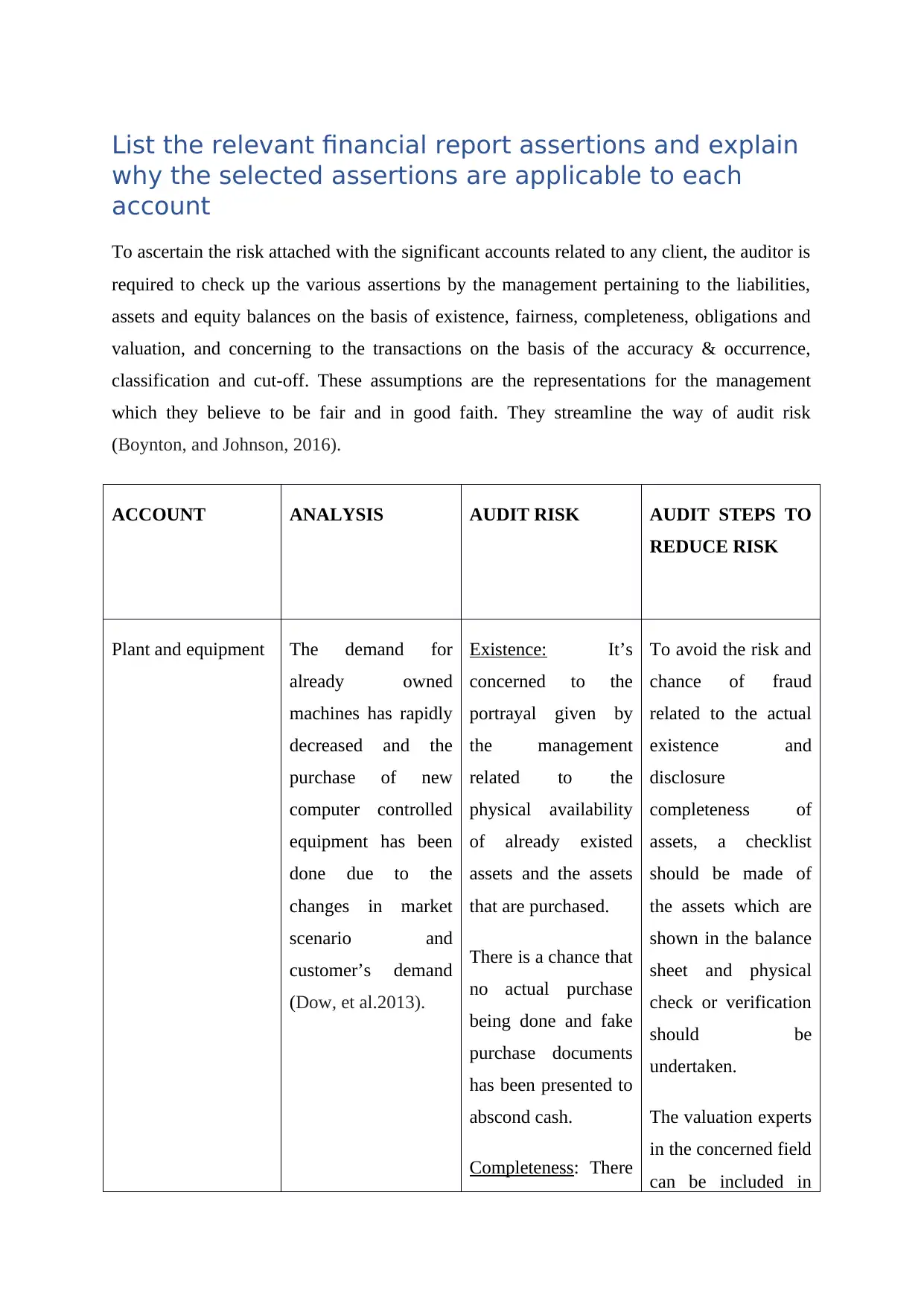

List the relevant financial report assertions and explain

why the selected assertions are applicable to each

account

To ascertain the risk attached with the significant accounts related to any client, the auditor is

required to check up the various assertions by the management pertaining to the liabilities,

assets and equity balances on the basis of existence, fairness, completeness, obligations and

valuation, and concerning to the transactions on the basis of the accuracy & occurrence,

classification and cut-off. These assumptions are the representations for the management

which they believe to be fair and in good faith. They streamline the way of audit risk

(Boynton, and Johnson, 2016).

ACCOUNT ANALYSIS AUDIT RISK AUDIT STEPS TO

REDUCE RISK

Plant and equipment The demand for

already owned

machines has rapidly

decreased and the

purchase of new

computer controlled

equipment has been

done due to the

changes in market

scenario and

customer’s demand

(Dow, et al.2013).

Existence: It’s

concerned to the

portrayal given by

the management

related to the

physical availability

of already existed

assets and the assets

that are purchased.

There is a chance that

no actual purchase

being done and fake

purchase documents

has been presented to

abscond cash.

Completeness: There

To avoid the risk and

chance of fraud

related to the actual

existence and

disclosure

completeness of

assets, a checklist

should be made of

the assets which are

shown in the balance

sheet and physical

check or verification

should be

undertaken.

The valuation experts

in the concerned field

can be included in

why the selected assertions are applicable to each

account

To ascertain the risk attached with the significant accounts related to any client, the auditor is

required to check up the various assertions by the management pertaining to the liabilities,

assets and equity balances on the basis of existence, fairness, completeness, obligations and

valuation, and concerning to the transactions on the basis of the accuracy & occurrence,

classification and cut-off. These assumptions are the representations for the management

which they believe to be fair and in good faith. They streamline the way of audit risk

(Boynton, and Johnson, 2016).

ACCOUNT ANALYSIS AUDIT RISK AUDIT STEPS TO

REDUCE RISK

Plant and equipment The demand for

already owned

machines has rapidly

decreased and the

purchase of new

computer controlled

equipment has been

done due to the

changes in market

scenario and

customer’s demand

(Dow, et al.2013).

Existence: It’s

concerned to the

portrayal given by

the management

related to the

physical availability

of already existed

assets and the assets

that are purchased.

There is a chance that

no actual purchase

being done and fake

purchase documents

has been presented to

abscond cash.

Completeness: There

To avoid the risk and

chance of fraud

related to the actual

existence and

disclosure

completeness of

assets, a checklist

should be made of

the assets which are

shown in the balance

sheet and physical

check or verification

should be

undertaken.

The valuation experts

in the concerned field

can be included in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is also a chance that

all the equipment

required to be

disclosing in the

balance sheet aren’t

done in real.

the valuation process

to get the correct

valuations. They may

help to ascertain the

correctness of

valuation in

ARAFURA

Resources Limited’s

context (Dow, et al…

2013).

Investment in mines

It leads to the result,

that many used and

huge mining

machines are lying

idle and motionless

in ARAFURA

Resources Limited’s

yard.

Valuation: Although

it may be possible

that the management

have represent the

correctly valued

assets and liabilities

but there may be

chances that the

improper valuation

has been adopted and

expressions have

been done for the

window dressing of

the figures of balance

sheet.

Any Discrepancy in

the existence or

disclosure of the

existence of the

assets is there, then it

shall be highlighted

automatically by a

cross verification of

the list with the

physical equipment

property.

Machine Finance

Liabilities

The liability which

becomes obligatory

for the management

for the purchase of

Completeness: There

a risk may be arises

that the liability on

the management to

To avoid the risk, the

documents related to

the purchase of both

old and new

all the equipment

required to be

disclosing in the

balance sheet aren’t

done in real.

the valuation process

to get the correct

valuations. They may

help to ascertain the

correctness of

valuation in

ARAFURA

Resources Limited’s

context (Dow, et al…

2013).

Investment in mines

It leads to the result,

that many used and

huge mining

machines are lying

idle and motionless

in ARAFURA

Resources Limited’s

yard.

Valuation: Although

it may be possible

that the management

have represent the

correctly valued

assets and liabilities

but there may be

chances that the

improper valuation

has been adopted and

expressions have

been done for the

window dressing of

the figures of balance

sheet.

Any Discrepancy in

the existence or

disclosure of the

existence of the

assets is there, then it

shall be highlighted

automatically by a

cross verification of

the list with the

physical equipment

property.

Machine Finance

Liabilities

The liability which

becomes obligatory

for the management

for the purchase of

Completeness: There

a risk may be arises

that the liability on

the management to

To avoid the risk, the

documents related to

the purchase of both

old and new

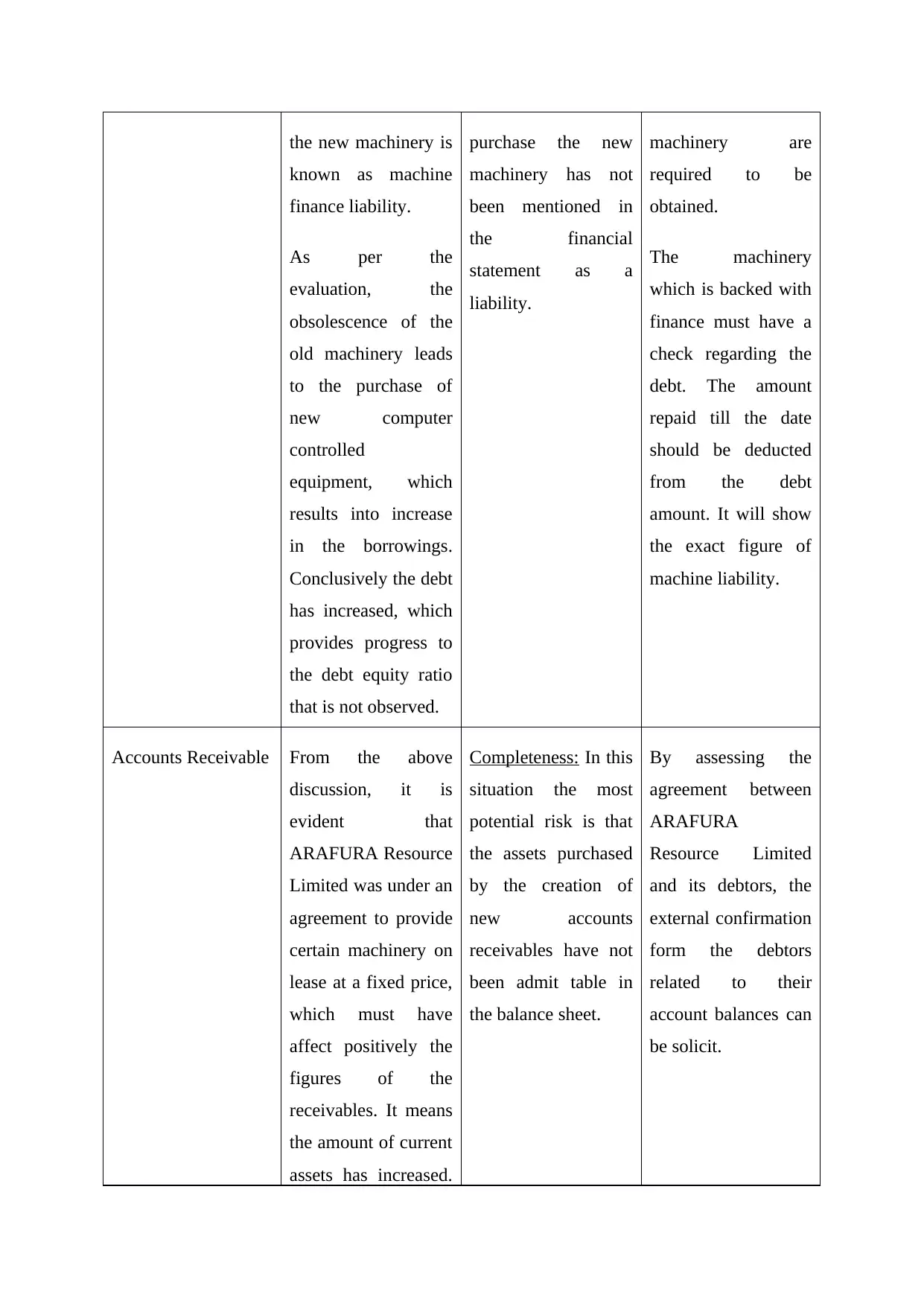

the new machinery is

known as machine

finance liability.

As per the

evaluation, the

obsolescence of the

old machinery leads

to the purchase of

new computer

controlled

equipment, which

results into increase

in the borrowings.

Conclusively the debt

has increased, which

provides progress to

the debt equity ratio

that is not observed.

purchase the new

machinery has not

been mentioned in

the financial

statement as a

liability.

machinery are

required to be

obtained.

The machinery

which is backed with

finance must have a

check regarding the

debt. The amount

repaid till the date

should be deducted

from the debt

amount. It will show

the exact figure of

machine liability.

Accounts Receivable From the above

discussion, it is

evident that

ARAFURA Resource

Limited was under an

agreement to provide

certain machinery on

lease at a fixed price,

which must have

affect positively the

figures of the

receivables. It means

the amount of current

assets has increased.

Completeness: In this

situation the most

potential risk is that

the assets purchased

by the creation of

new accounts

receivables have not

been admit table in

the balance sheet.

By assessing the

agreement between

ARAFURA

Resource Limited

and its debtors, the

external confirmation

form the debtors

related to their

account balances can

be solicit.

known as machine

finance liability.

As per the

evaluation, the

obsolescence of the

old machinery leads

to the purchase of

new computer

controlled

equipment, which

results into increase

in the borrowings.

Conclusively the debt

has increased, which

provides progress to

the debt equity ratio

that is not observed.

purchase the new

machinery has not

been mentioned in

the financial

statement as a

liability.

machinery are

required to be

obtained.

The machinery

which is backed with

finance must have a

check regarding the

debt. The amount

repaid till the date

should be deducted

from the debt

amount. It will show

the exact figure of

machine liability.

Accounts Receivable From the above

discussion, it is

evident that

ARAFURA Resource

Limited was under an

agreement to provide

certain machinery on

lease at a fixed price,

which must have

affect positively the

figures of the

receivables. It means

the amount of current

assets has increased.

Completeness: In this

situation the most

potential risk is that

the assets purchased

by the creation of

new accounts

receivables have not

been admit table in

the balance sheet.

By assessing the

agreement between

ARAFURA

Resource Limited

and its debtors, the

external confirmation

form the debtors

related to their

account balances can

be solicit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.