BUAD 264 - Managerial Accounting: Master Budget for Archie-Boy Corp.

VerifiedAdded on 2022/08/27

|9

|1148

|29

Homework Assignment

AI Summary

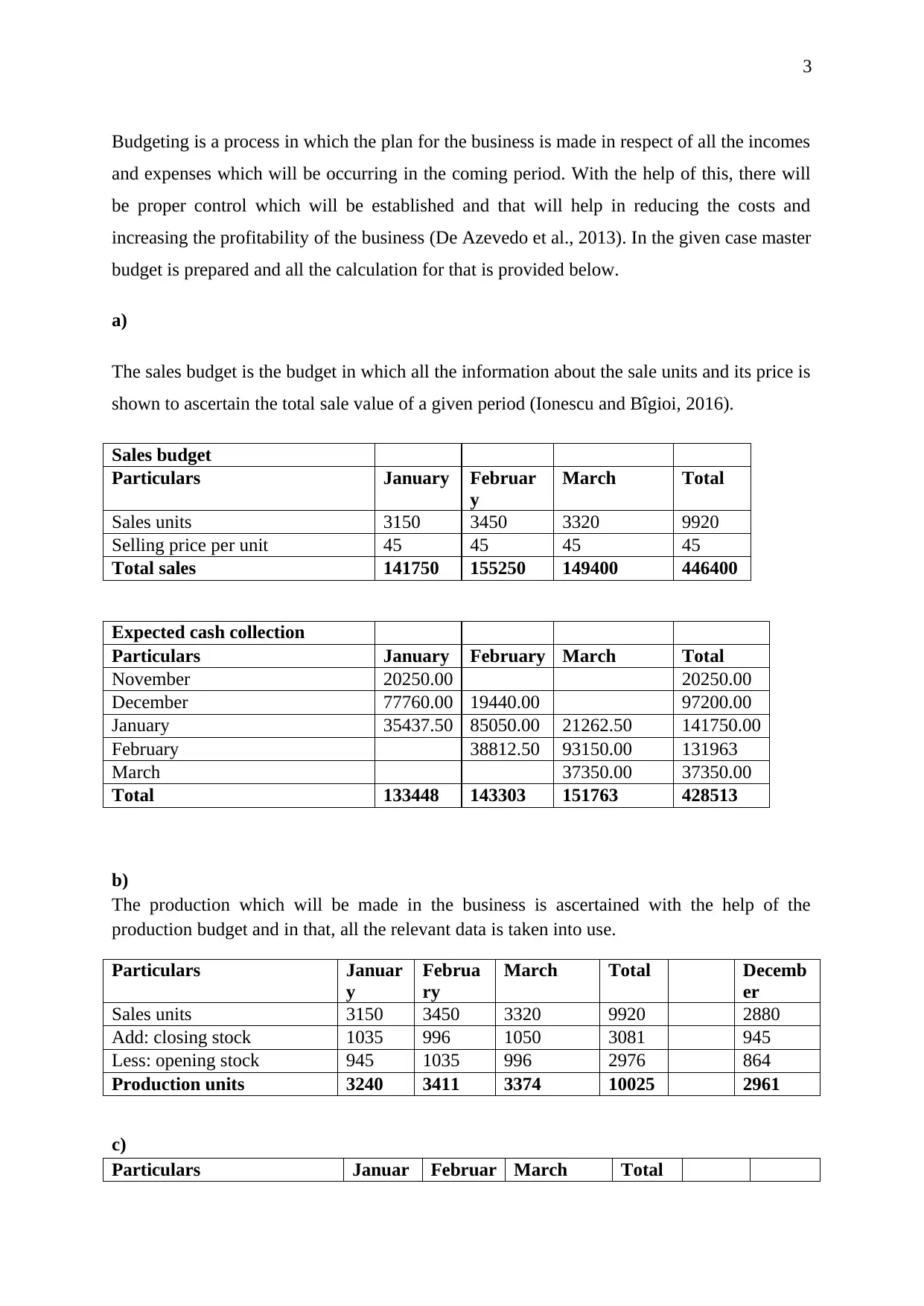

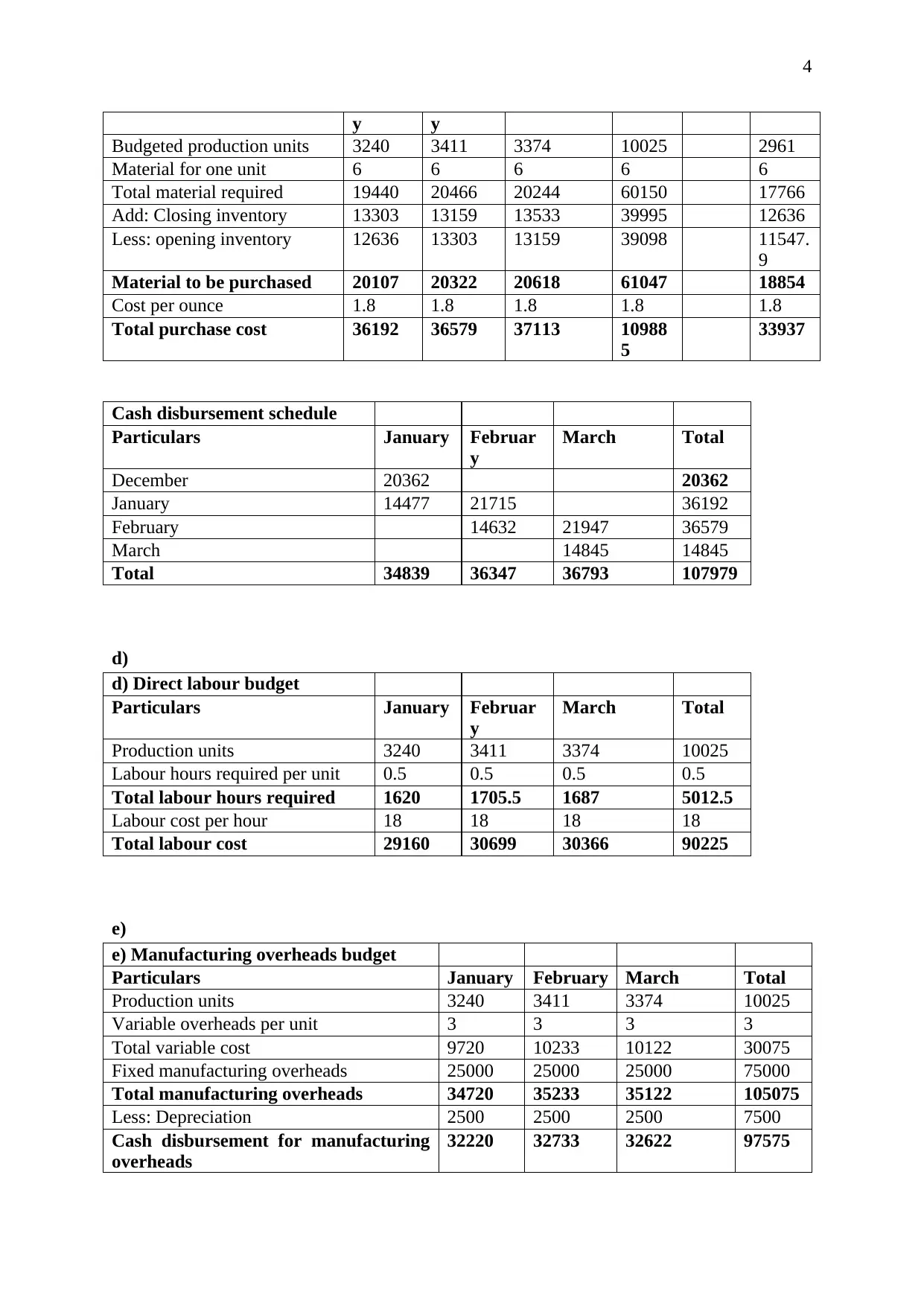

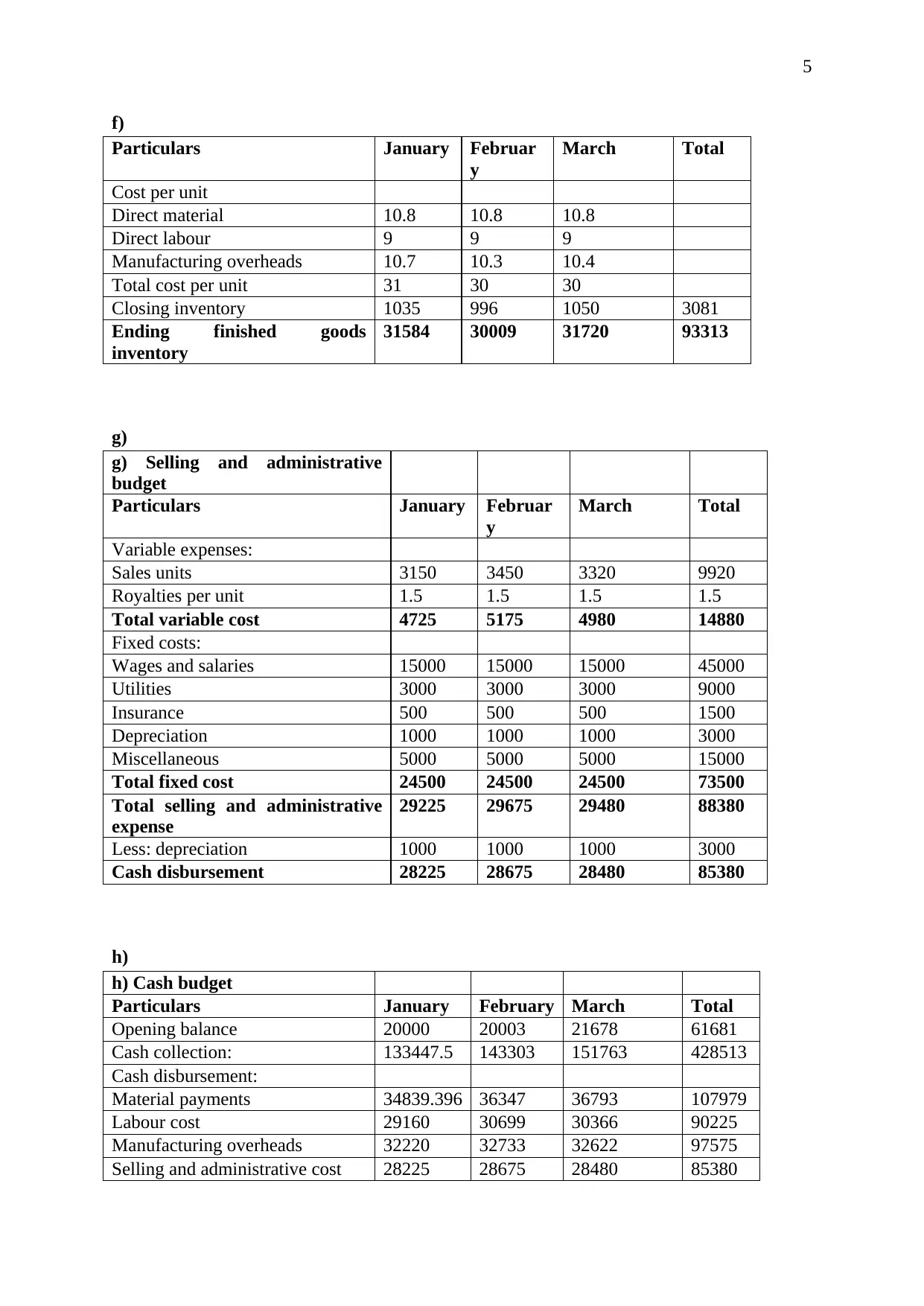

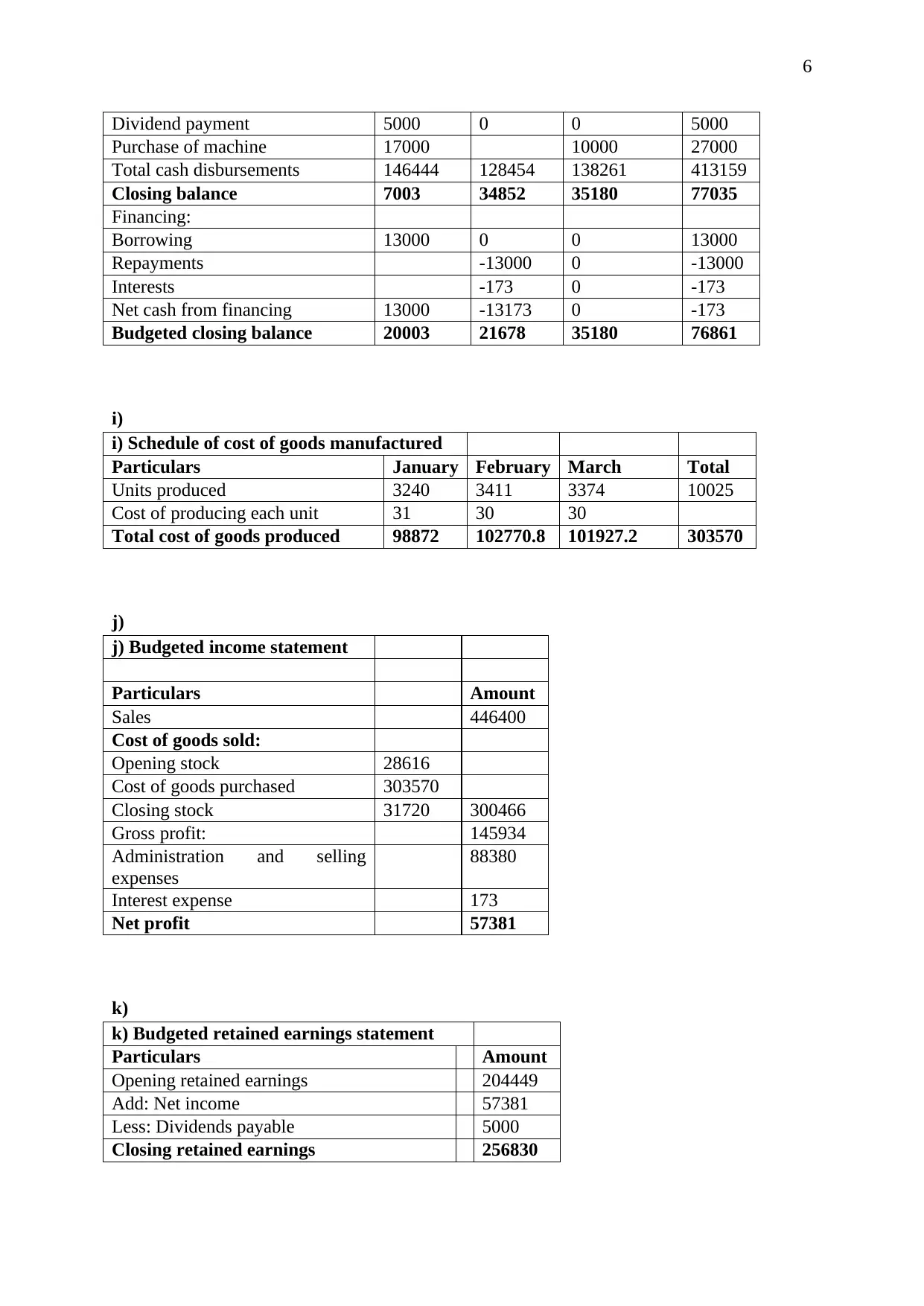

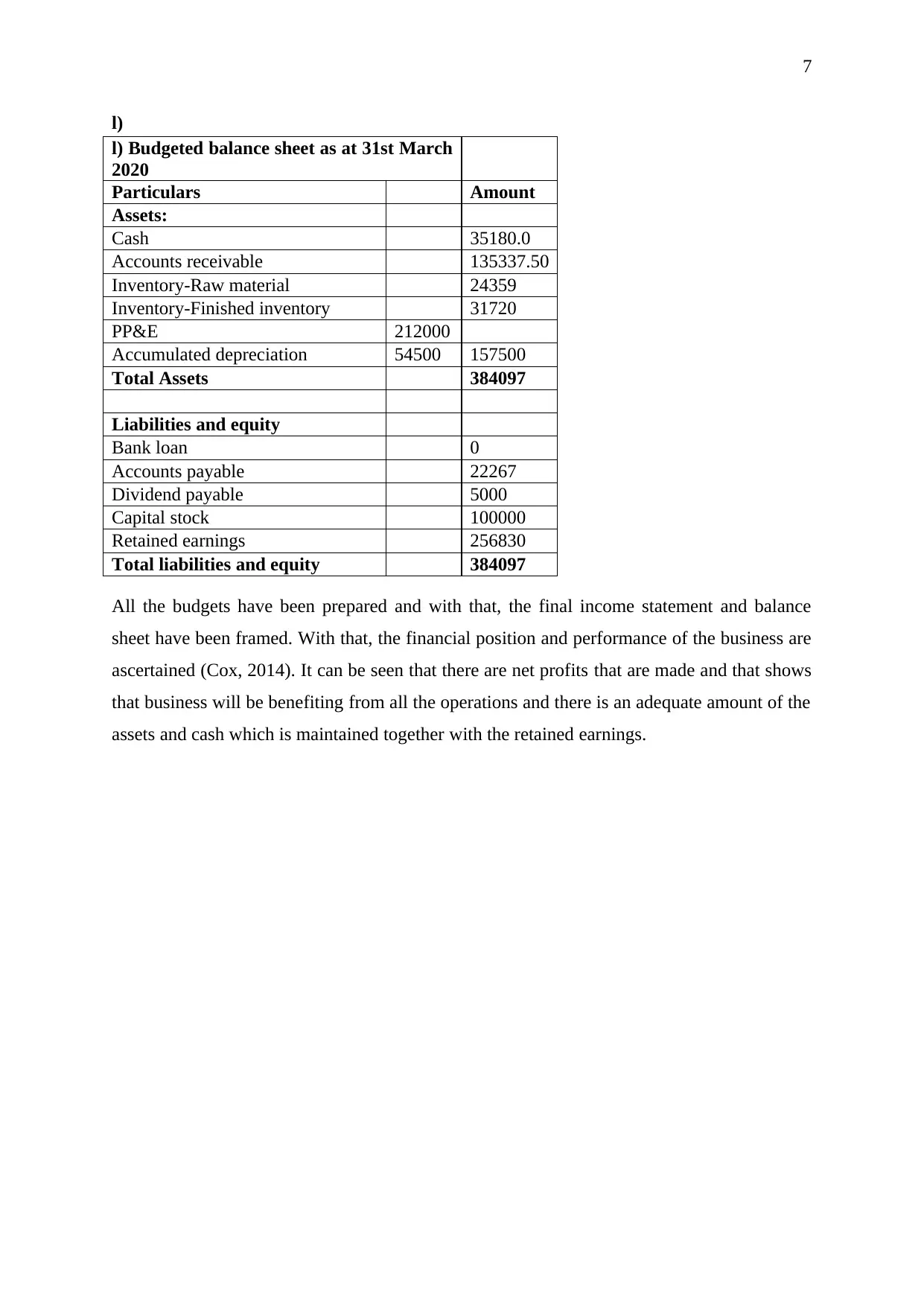

This assignment presents a comprehensive master budget for Archie-Boy Dog Toy Corp., prepared for the quarter ending March 31st, 2020. The budget includes detailed calculations for the sales budget, production budget, direct materials budget, direct labor budget, manufacturing overhead budget, selling and administrative budget, and cash budget. The solution meticulously outlines the expected cash collections, production units, material purchases, labor costs, and overhead expenses. Furthermore, it incorporates the schedule of cost of goods manufactured, the budgeted income statement, the budgeted retained earnings statement, and the budgeted balance sheet. The assignment demonstrates the preparation of these financial statements based on the provided sales data, inventory policies, and cost information, providing a complete overview of the company's financial performance and position during the budgeted period. All calculations are included, demonstrating the interrelation of the various budget components and their impact on the final financial statements.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.