Architecture Design Technology Report: Payment and Depreciation

VerifiedAdded on 2020/05/16

|25

|4919

|100

Report

AI Summary

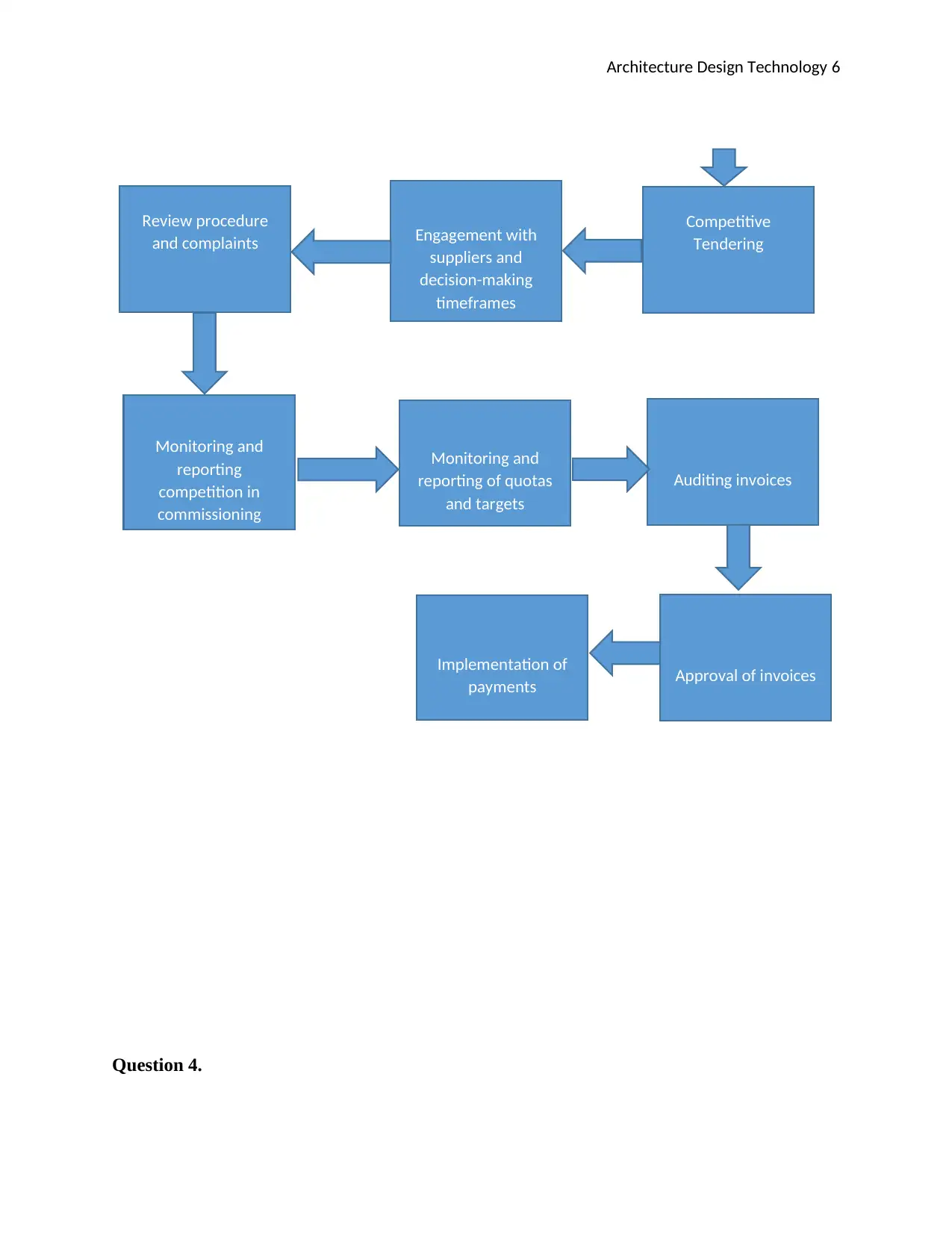

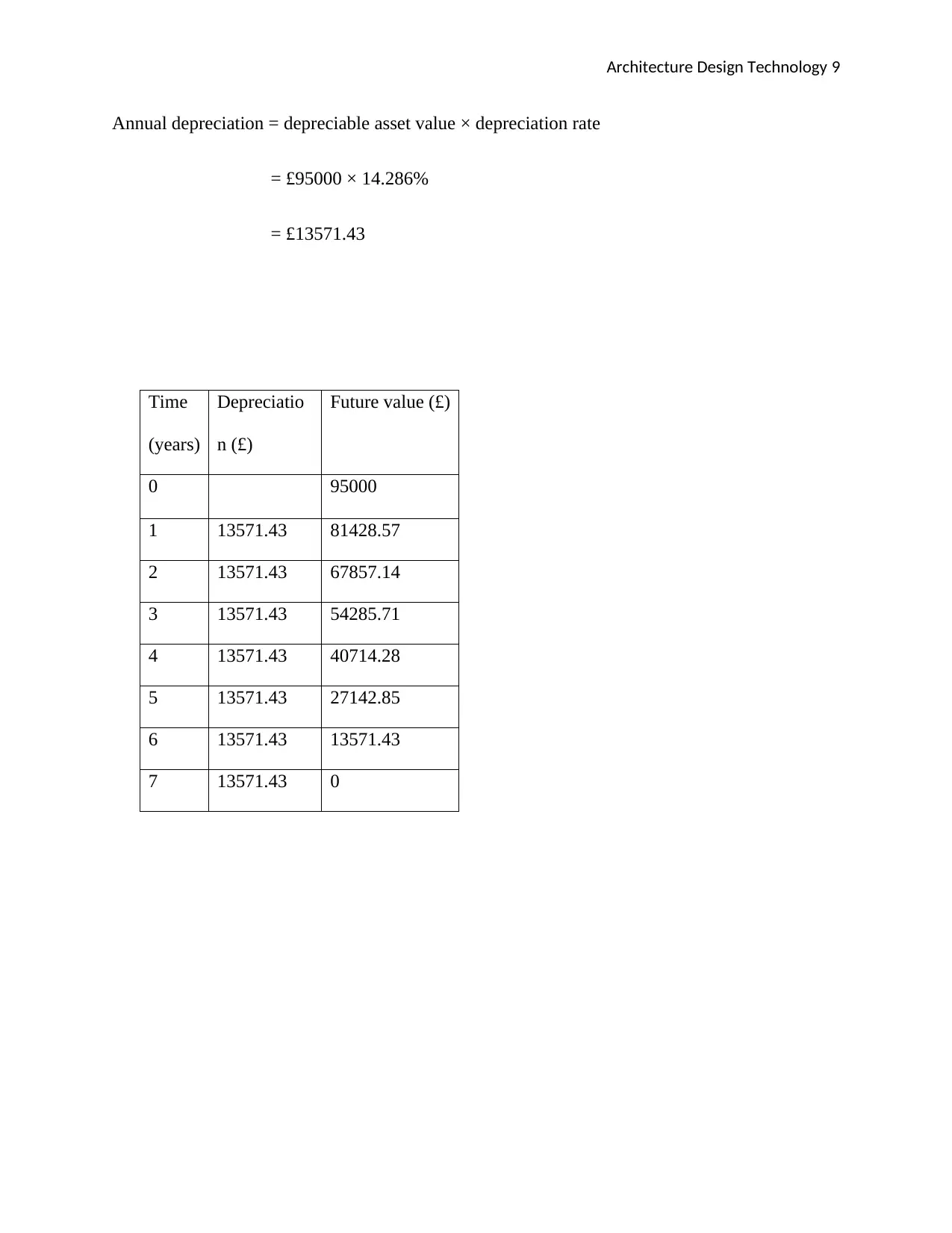

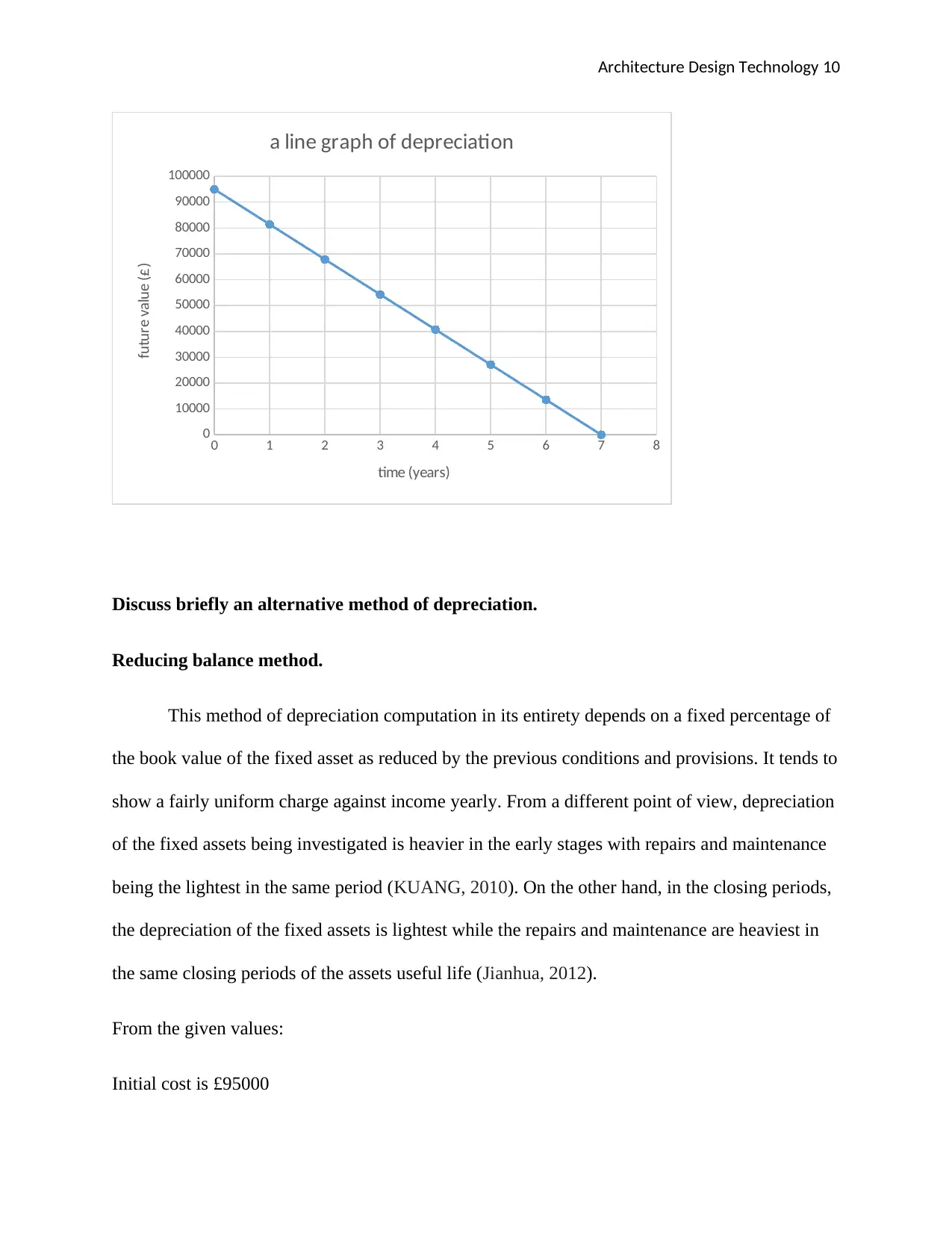

This report delves into the financial aspects of architecture design technology, covering key areas such as payment methods, depreciation techniques, and tendering processes. It begins by discussing the financial benefits of regular contractor payments and the importance of retention, outlining reasons for holding back funds on behalf of the client. The report then explores various methods of valuing works for payment, including DCF analysis and comparable company analysis. A practical calculation of an interim certificate is provided, followed by a detailed flowchart illustrating the procedure for obtaining quotes, commissioning suppliers, and making payments. The report further analyzes depreciation methods, specifically focusing on the straight-line method for a JCB, with graphical results and a discussion of the reducing balance method as an alternative. Finally, it examines the PQQ process, highlighting its importance and benefits, and contrasts competitive pricing with negotiated tendering, outlining their respective advantages. This comprehensive analysis provides valuable insights into the financial management of construction projects.

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.