Groupe Ariel S.A. Case: Parity Conditions and Cross-Border Valuation

VerifiedAdded on 2023/05/29

|19

|3621

|65

Case Study

AI Summary

This case study analyzes the financial feasibility of Groupe Ariel S.A.'s expansion project in Mexico, focusing on the valuation of a recycling equipment investment. The analysis involves calculating the Net Present Value (NPV) of the project using incremental cash flows in both pesos and Euros, considering factors like inflation rates in Mexico and France, exchange rate fluctuations, and the company's hurdle rate. The student's solution presents two different approaches to calculate the NPV: one converting the net cash flow from Peso to Euro and the other converting each cash flow. The case study highlights the importance of understanding parity conditions and their impact on cross-border valuations, comparing the results of the two methods and providing insights into which approach is most appropriate for making sound financial decisions. The analysis also includes detailed calculations of hurdle rates, discount factors, and present values, providing a comprehensive understanding of the project's financial viability. The document showcases a student's application of financial principles to a real-world business scenario, demonstrating their ability to evaluate investment proposals in an international context.

International Finance Management

Case Analysis

“Groupe Ariel S.A.: Parity Conditions and Cross-Border Valuation”

Groupe Ariel is a worldwide manufacturer of many equipment like printer,

copies, fax, machines, and other equipment producing document. Groupe

Ariel also provides various consulting services to outside people. The

company after sales service revenue forms a big portion and near to almost

18 percent of the total revenue. In 2008 the company did witness low

profitability and sales due to worldwide recession and it similar situation

was prevalent all over the industry, but the main advantage point of the

company is its growth comparison to several emerging market like that of

Russia, china and India. The company had been a global firm for years but

did not grow violently into the emerging market. The company captured

the international market through its subsidiaries which generally ran

medium sized factories in which generally printers, copiers and other

products were manufactured to suit the local need of the people around.

The company conducted its business in 28 different countries around the

globe with operations such as manufacturing, small research labs, as well

as engaged in sales and other activities. The Company subsidiaries had

recorded half of the Ariel sales and had earned slightly less than 40 percent

of the pre-tax income.

Ariel always competed in a strong market and mostly competitors of the

company is the multinational company and few have even developed

there after sales service higher the level compared to Ariel business.

Case Analysis

“Groupe Ariel S.A.: Parity Conditions and Cross-Border Valuation”

Groupe Ariel is a worldwide manufacturer of many equipment like printer,

copies, fax, machines, and other equipment producing document. Groupe

Ariel also provides various consulting services to outside people. The

company after sales service revenue forms a big portion and near to almost

18 percent of the total revenue. In 2008 the company did witness low

profitability and sales due to worldwide recession and it similar situation

was prevalent all over the industry, but the main advantage point of the

company is its growth comparison to several emerging market like that of

Russia, china and India. The company had been a global firm for years but

did not grow violently into the emerging market. The company captured

the international market through its subsidiaries which generally ran

medium sized factories in which generally printers, copiers and other

products were manufactured to suit the local need of the people around.

The company conducted its business in 28 different countries around the

globe with operations such as manufacturing, small research labs, as well

as engaged in sales and other activities. The Company subsidiaries had

recorded half of the Ariel sales and had earned slightly less than 40 percent

of the pre-tax income.

Ariel always competed in a strong market and mostly competitors of the

company is the multinational company and few have even developed

there after sales service higher the level compared to Ariel business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

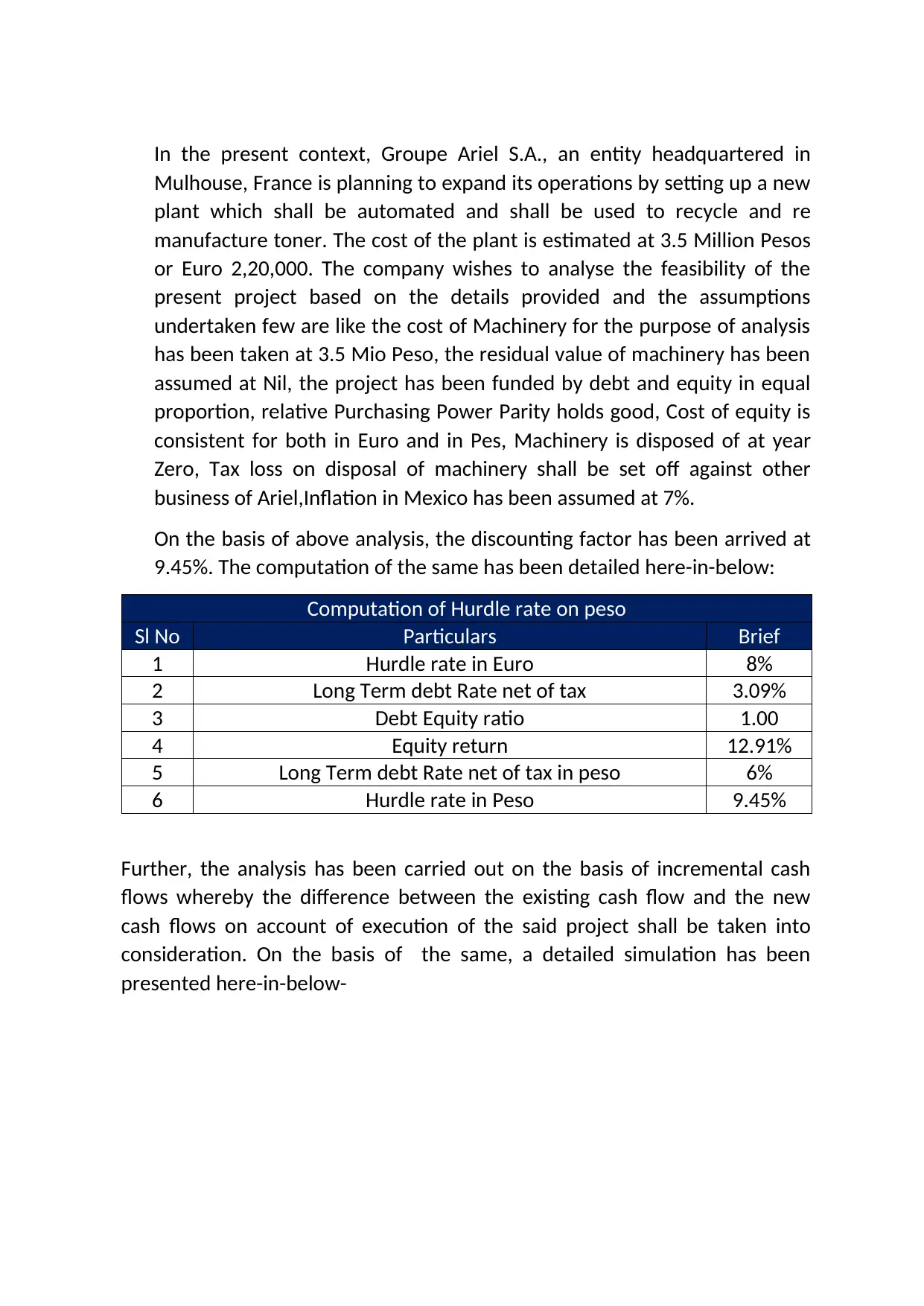

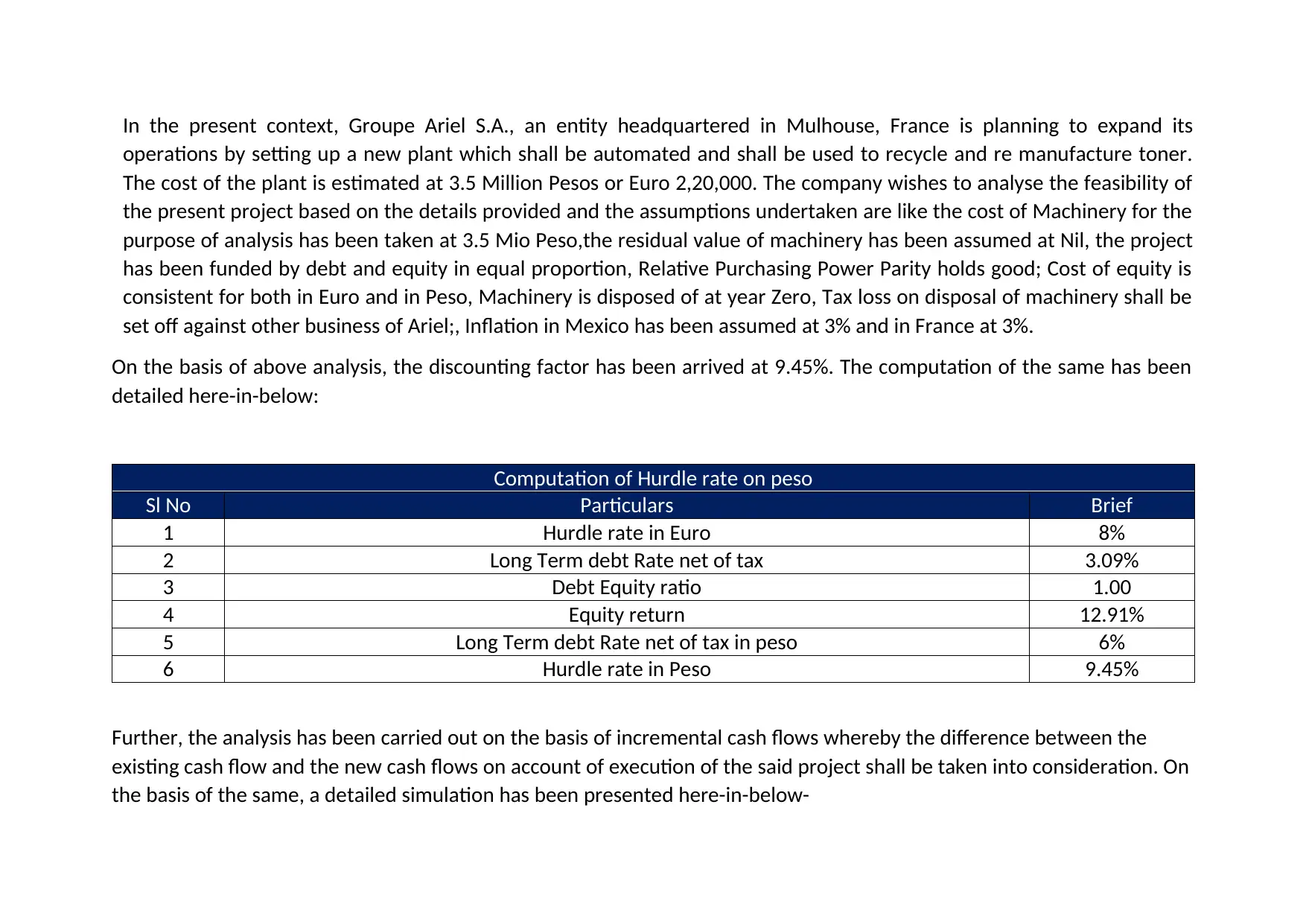

In the present context, Groupe Ariel S.A., an entity headquartered in

Mulhouse, France is planning to expand its operations by setting up a new

plant which shall be automated and shall be used to recycle and re

manufacture toner. The cost of the plant is estimated at 3.5 Million Pesos

or Euro 2,20,000. The company wishes to analyse the feasibility of the

present project based on the details provided and the assumptions

undertaken few are like the cost of Machinery for the purpose of analysis

has been taken at 3.5 Mio Peso, the residual value of machinery has been

assumed at Nil, the project has been funded by debt and equity in equal

proportion, relative Purchasing Power Parity holds good, Cost of equity is

consistent for both in Euro and in Pes, Machinery is disposed of at year

Zero, Tax loss on disposal of machinery shall be set off against other

business of Ariel,Inflation in Mexico has been assumed at 7%.

On the basis of above analysis, the discounting factor has been arrived at

9.45%. The computation of the same has been detailed here-in-below:

Computation of Hurdle rate on peso

Sl No Particulars Brief

1 Hurdle rate in Euro 8%

2 Long Term debt Rate net of tax 3.09%

3 Debt Equity ratio 1.00

4 Equity return 12.91%

5 Long Term debt Rate net of tax in peso 6%

6 Hurdle rate in Peso 9.45%

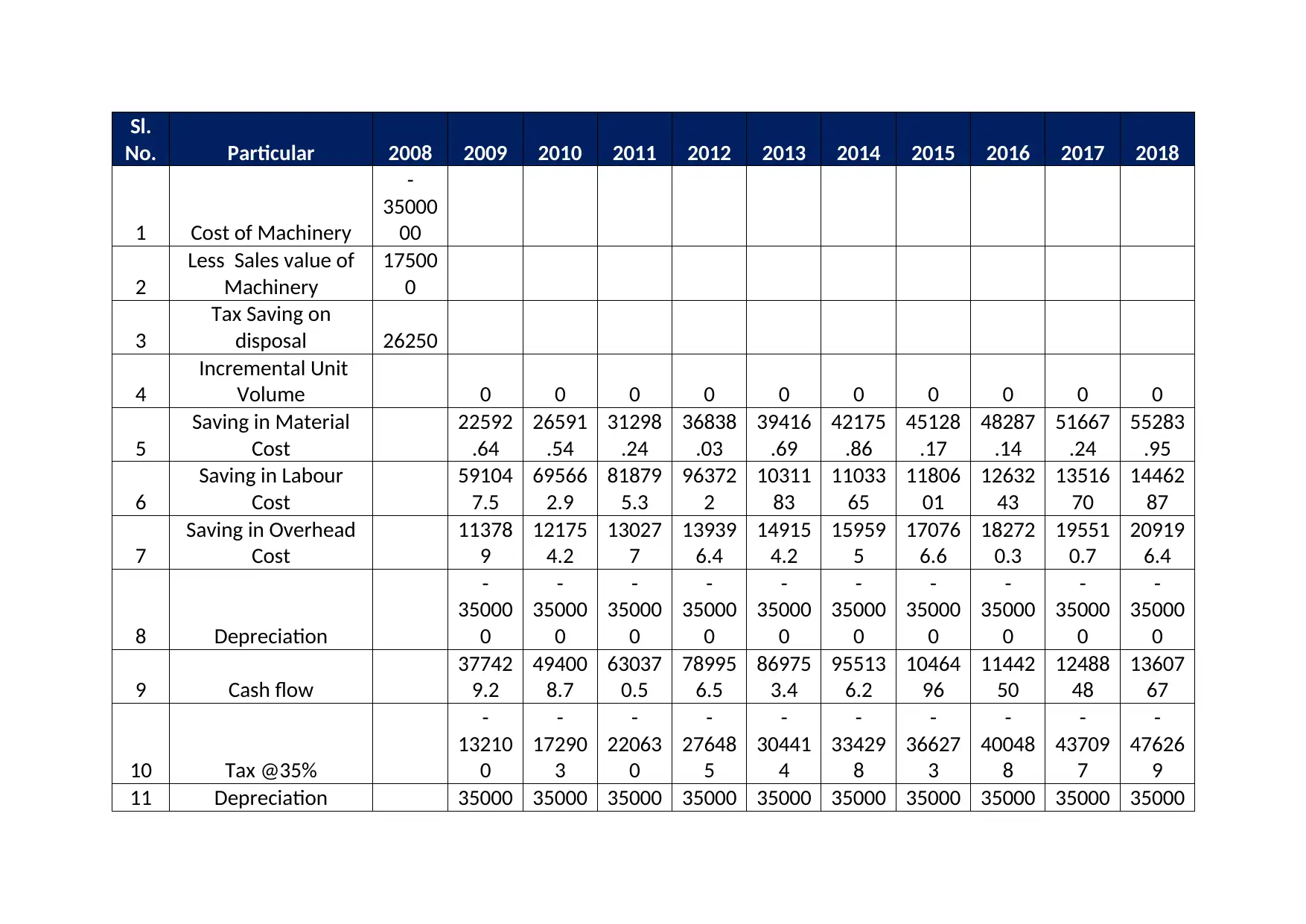

Further, the analysis has been carried out on the basis of incremental cash

flows whereby the difference between the existing cash flow and the new

cash flows on account of execution of the said project shall be taken into

consideration. On the basis of the same, a detailed simulation has been

presented here-in-below-

Mulhouse, France is planning to expand its operations by setting up a new

plant which shall be automated and shall be used to recycle and re

manufacture toner. The cost of the plant is estimated at 3.5 Million Pesos

or Euro 2,20,000. The company wishes to analyse the feasibility of the

present project based on the details provided and the assumptions

undertaken few are like the cost of Machinery for the purpose of analysis

has been taken at 3.5 Mio Peso, the residual value of machinery has been

assumed at Nil, the project has been funded by debt and equity in equal

proportion, relative Purchasing Power Parity holds good, Cost of equity is

consistent for both in Euro and in Pes, Machinery is disposed of at year

Zero, Tax loss on disposal of machinery shall be set off against other

business of Ariel,Inflation in Mexico has been assumed at 7%.

On the basis of above analysis, the discounting factor has been arrived at

9.45%. The computation of the same has been detailed here-in-below:

Computation of Hurdle rate on peso

Sl No Particulars Brief

1 Hurdle rate in Euro 8%

2 Long Term debt Rate net of tax 3.09%

3 Debt Equity ratio 1.00

4 Equity return 12.91%

5 Long Term debt Rate net of tax in peso 6%

6 Hurdle rate in Peso 9.45%

Further, the analysis has been carried out on the basis of incremental cash

flows whereby the difference between the existing cash flow and the new

cash flows on account of execution of the said project shall be taken into

consideration. On the basis of the same, a detailed simulation has been

presented here-in-below-

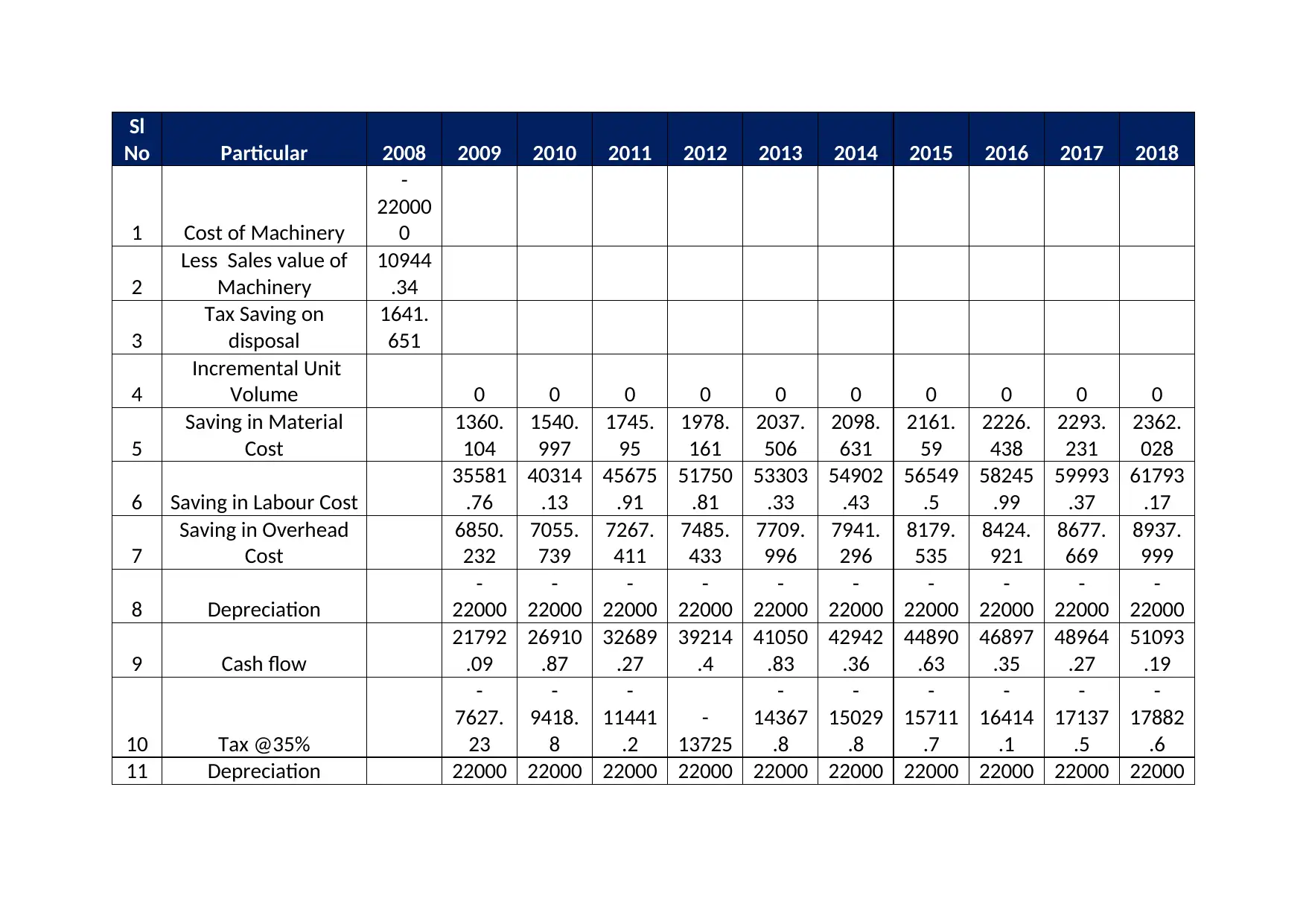

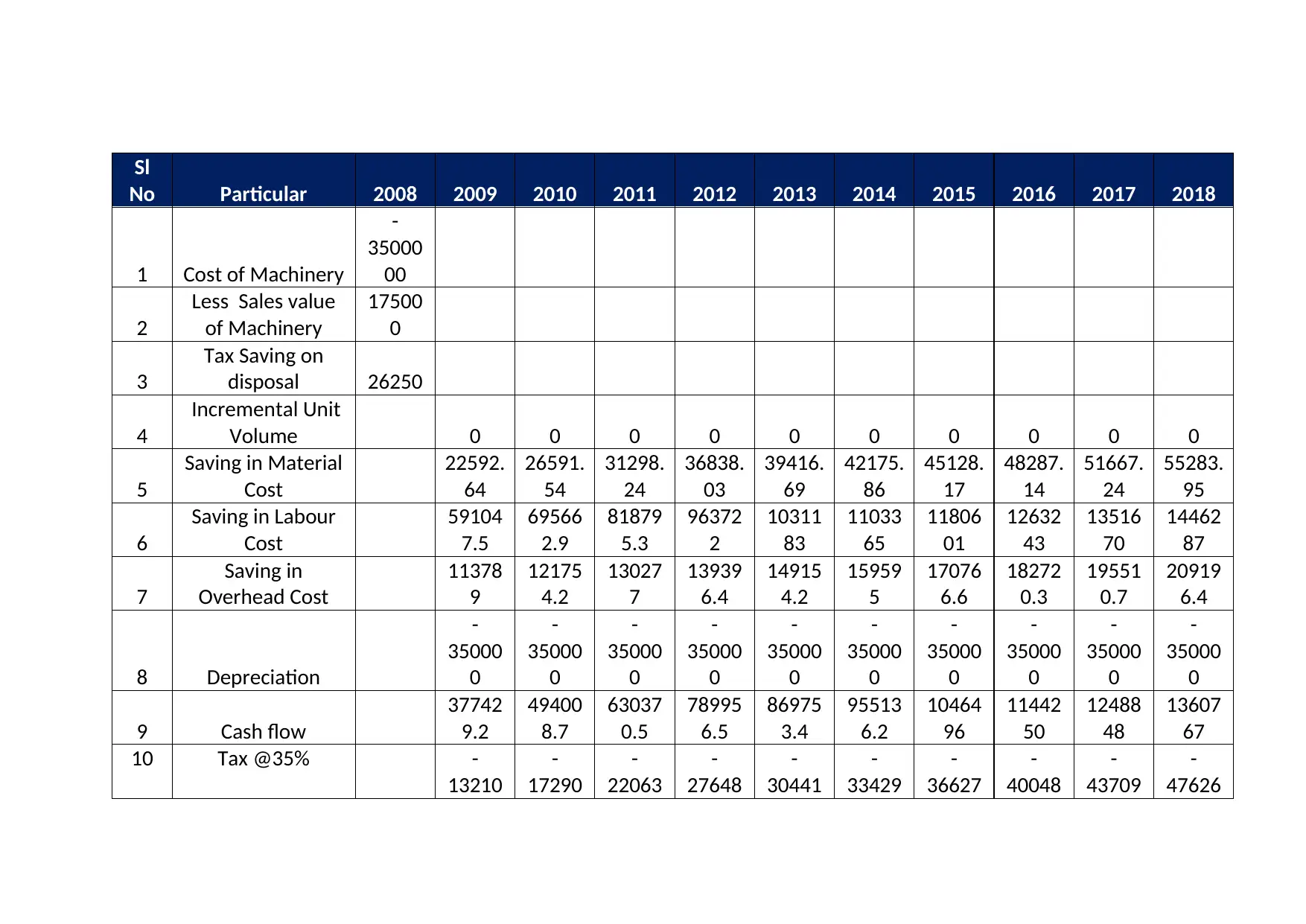

Sl.

No. Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery

-

35000

00

2

Less Sales value of

Machinery

17500

0

3

Tax Saving on

disposal 26250

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

22592

.64

26591

.54

31298

.24

36838

.03

39416

.69

42175

.86

45128

.17

48287

.14

51667

.24

55283

.95

6

Saving in Labour

Cost

59104

7.5

69566

2.9

81879

5.3

96372

2

10311

83

11033

65

11806

01

12632

43

13516

70

14462

87

7

Saving in Overhead

Cost

11378

9

12175

4.2

13027

7

13939

6.4

14915

4.2

15959

5

17076

6.6

18272

0.3

19551

0.7

20919

6.4

8 Depreciation

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

9 Cash flow

37742

9.2

49400

8.7

63037

0.5

78995

6.5

86975

3.4

95513

6.2

10464

96

11442

50

12488

48

13607

67

10 Tax @35%

-

13210

0

-

17290

3

-

22063

0

-

27648

5

-

30441

4

-

33429

8

-

36627

3

-

40048

8

-

43709

7

-

47626

9

11 Depreciation 35000 35000 35000 35000 35000 35000 35000 35000 35000 35000

No. Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery

-

35000

00

2

Less Sales value of

Machinery

17500

0

3

Tax Saving on

disposal 26250

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

22592

.64

26591

.54

31298

.24

36838

.03

39416

.69

42175

.86

45128

.17

48287

.14

51667

.24

55283

.95

6

Saving in Labour

Cost

59104

7.5

69566

2.9

81879

5.3

96372

2

10311

83

11033

65

11806

01

12632

43

13516

70

14462

87

7

Saving in Overhead

Cost

11378

9

12175

4.2

13027

7

13939

6.4

14915

4.2

15959

5

17076

6.6

18272

0.3

19551

0.7

20919

6.4

8 Depreciation

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

9 Cash flow

37742

9.2

49400

8.7

63037

0.5

78995

6.5

86975

3.4

95513

6.2

10464

96

11442

50

12488

48

13607

67

10 Tax @35%

-

13210

0

-

17290

3

-

22063

0

-

27648

5

-

30441

4

-

33429

8

-

36627

3

-

40048

8

-

43709

7

-

47626

9

11 Depreciation 35000 35000 35000 35000 35000 35000 35000 35000 35000 35000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 0 0 0 0 0 0 0 0 0

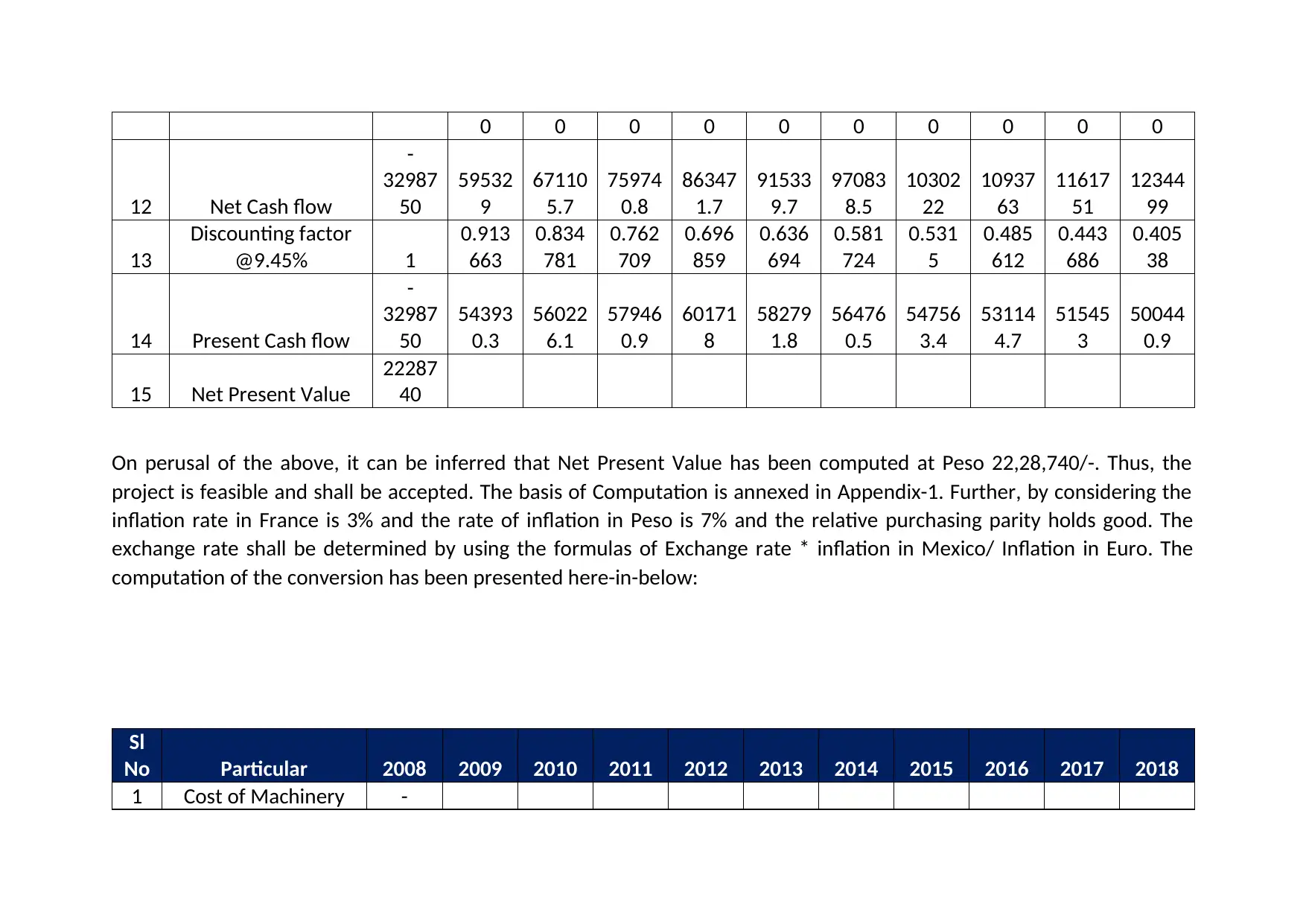

12 Net Cash flow

-

32987

50

59532

9

67110

5.7

75974

0.8

86347

1.7

91533

9.7

97083

8.5

10302

22

10937

63

11617

51

12344

99

13

Discounting factor

@9.45% 1

0.913

663

0.834

781

0.762

709

0.696

859

0.636

694

0.581

724

0.531

5

0.485

612

0.443

686

0.405

38

14 Present Cash flow

-

32987

50

54393

0.3

56022

6.1

57946

0.9

60171

8

58279

1.8

56476

0.5

54756

3.4

53114

4.7

51545

3

50044

0.9

15 Net Present Value

22287

40

On perusal of the above, it can be inferred that Net Present Value has been computed at Peso 22,28,740/-. Thus, the

project is feasible and shall be accepted. The basis of Computation is annexed in Appendix-1. Further, by considering the

inflation rate in France is 3% and the rate of inflation in Peso is 7% and the relative purchasing parity holds good. The

exchange rate shall be determined by using the formulas of Exchange rate * inflation in Mexico/ Inflation in Euro. The

computation of the conversion has been presented here-in-below:

Sl

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery -

12 Net Cash flow

-

32987

50

59532

9

67110

5.7

75974

0.8

86347

1.7

91533

9.7

97083

8.5

10302

22

10937

63

11617

51

12344

99

13

Discounting factor

@9.45% 1

0.913

663

0.834

781

0.762

709

0.696

859

0.636

694

0.581

724

0.531

5

0.485

612

0.443

686

0.405

38

14 Present Cash flow

-

32987

50

54393

0.3

56022

6.1

57946

0.9

60171

8

58279

1.8

56476

0.5

54756

3.4

53114

4.7

51545

3

50044

0.9

15 Net Present Value

22287

40

On perusal of the above, it can be inferred that Net Present Value has been computed at Peso 22,28,740/-. Thus, the

project is feasible and shall be accepted. The basis of Computation is annexed in Appendix-1. Further, by considering the

inflation rate in France is 3% and the rate of inflation in Peso is 7% and the relative purchasing parity holds good. The

exchange rate shall be determined by using the formulas of Exchange rate * inflation in Mexico/ Inflation in Euro. The

computation of the conversion has been presented here-in-below:

Sl

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

35000

00

2

Less Sales value of

Machinery

17500

0

3

Tax Saving on

disposal 26250

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

22592

.64

26591

.54

31298

.24

36838

.03

39416

.69

42175

.86

45128

.17

48287

.14

51667

.24

55283

.95

6

Saving in Labour

Cost

59104

7.5

69566

2.9

81879

5.3

96372

2

10311

83

11033

65

11806

01

12632

43

13516

70

14462

87

7

Saving in Overhead

Cost

11378

9

12175

4.2

13027

7

13939

6.4

14915

4.2

15959

5

17076

6.6

18272

0.3

19551

0.7

20919

6.4

8 Depreciation

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

9 Cash flow

37742

9.2

49400

8.7

63037

0.5

78995

6.5

86975

3.4

95513

6.2

10464

96

11442

50

12488

48

13607

67

10 Tax @35%

-

13210

0

-

17290

3

-

22063

0

-

27648

5

-

30441

4

-

33429

8

-

36627

3

-

40048

8

-

43709

7

-

47626

9

11 Depreciation

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

12 Net Cash flow -

32987

59532

9

67110

5.7

75974

0.8

86347

1.7

91533

9.7

97083

8.5

10302

22

10937

63

11617

51

12344

99

00

2

Less Sales value of

Machinery

17500

0

3

Tax Saving on

disposal 26250

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

22592

.64

26591

.54

31298

.24

36838

.03

39416

.69

42175

.86

45128

.17

48287

.14

51667

.24

55283

.95

6

Saving in Labour

Cost

59104

7.5

69566

2.9

81879

5.3

96372

2

10311

83

11033

65

11806

01

12632

43

13516

70

14462

87

7

Saving in Overhead

Cost

11378

9

12175

4.2

13027

7

13939

6.4

14915

4.2

15959

5

17076

6.6

18272

0.3

19551

0.7

20919

6.4

8 Depreciation

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

9 Cash flow

37742

9.2

49400

8.7

63037

0.5

78995

6.5

86975

3.4

95513

6.2

10464

96

11442

50

12488

48

13607

67

10 Tax @35%

-

13210

0

-

17290

3

-

22063

0

-

27648

5

-

30441

4

-

33429

8

-

36627

3

-

40048

8

-

43709

7

-

47626

9

11 Depreciation

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

35000

0

12 Net Cash flow -

32987

59532

9

67110

5.7

75974

0.8

86347

1.7

91533

9.7

97083

8.5

10302

22

10937

63

11617

51

12344

99

50

13

Discounting factor

@9.45% 1

0.913

663

0.834

781

0.762

709

0.696

859

0.636

694

0.581

724

0.531

5

0.485

612

0.443

686

0.405

38

14 Present Cash flow

-

32987

50

54393

0.3

56022

6.1

57946

0.9

60171

8

58279

1.8

56476

0.5

54756

3.4

53114

4.7

51545

3

50044

0.9

15 Net Present Value

22287

40

16

Net Cash flow in

Peso

-

32987

50

59532

9

67110

5.7

75974

0.8

86347

1.7

91533

9.7

97083

8.5

10302

22

10937

63

11617

51

12344

99

17 Peso/ Euro 15.99

16.61

097

17.25

606

17.92

62

18.62

236

19.34

556

20.09

684

20.87

73

21.68

807

22.53

032

23.40

529

18

Discounting factor

@9.45% 1

0.913

659

0.834

773

0.762

698

0.696

846

0.636

68

0.581

708

0.531

483

0.485

595

0.443

668

0.405

361

19 Present Cash flow

-

20630

1

32745

.09

32465

.18

32324

.37 32311

30124

.67

28101

.18

26226

.85

24489

.29

22877

.25

21380

.56

20 Net Present Value

76744

.62

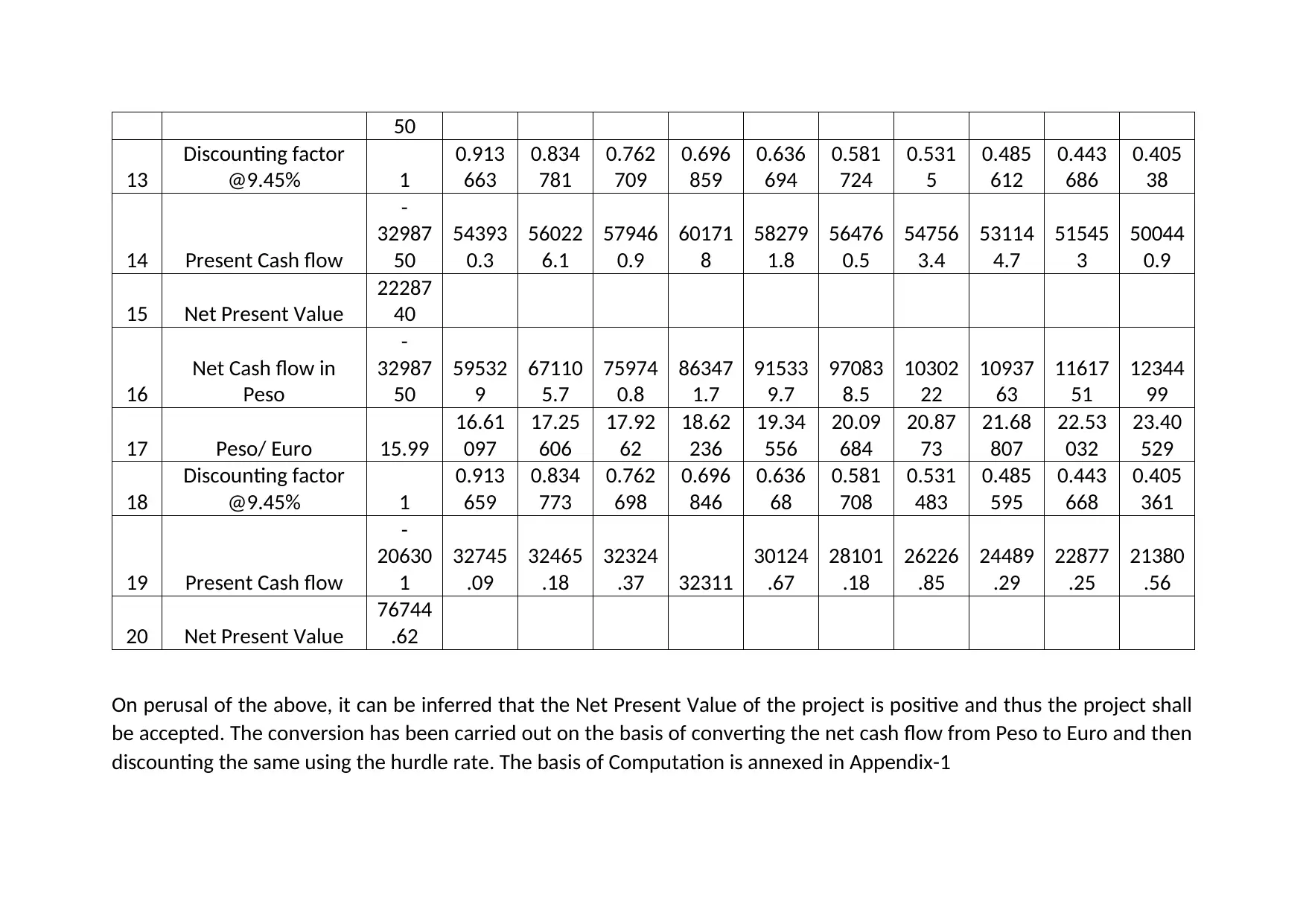

On perusal of the above, it can be inferred that the Net Present Value of the project is positive and thus the project shall

be accepted. The conversion has been carried out on the basis of converting the net cash flow from Peso to Euro and then

discounting the same using the hurdle rate. The basis of Computation is annexed in Appendix-1

13

Discounting factor

@9.45% 1

0.913

663

0.834

781

0.762

709

0.696

859

0.636

694

0.581

724

0.531

5

0.485

612

0.443

686

0.405

38

14 Present Cash flow

-

32987

50

54393

0.3

56022

6.1

57946

0.9

60171

8

58279

1.8

56476

0.5

54756

3.4

53114

4.7

51545

3

50044

0.9

15 Net Present Value

22287

40

16

Net Cash flow in

Peso

-

32987

50

59532

9

67110

5.7

75974

0.8

86347

1.7

91533

9.7

97083

8.5

10302

22

10937

63

11617

51

12344

99

17 Peso/ Euro 15.99

16.61

097

17.25

606

17.92

62

18.62

236

19.34

556

20.09

684

20.87

73

21.68

807

22.53

032

23.40

529

18

Discounting factor

@9.45% 1

0.913

659

0.834

773

0.762

698

0.696

846

0.636

68

0.581

708

0.531

483

0.485

595

0.443

668

0.405

361

19 Present Cash flow

-

20630

1

32745

.09

32465

.18

32324

.37 32311

30124

.67

28101

.18

26226

.85

24489

.29

22877

.25

21380

.56

20 Net Present Value

76744

.62

On perusal of the above, it can be inferred that the Net Present Value of the project is positive and thus the project shall

be accepted. The conversion has been carried out on the basis of converting the net cash flow from Peso to Euro and then

discounting the same using the hurdle rate. The basis of Computation is annexed in Appendix-1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the present context, Groupe Ariel S.A., an entity headquartered in Mulhouse, France is planning to expand its

operations by setting up a new plant which shall be automated and shall be used to recycle and re manufacture toner. The

cost of the plant is estimated at 3.5 Million Pesos or Euro 2,20,000. The company wishes to analyse the feasibility of the

present project based on the details provided and the assumptions undertaken are listed as, The cost of Machinery for the

purpose of analysis has been taken at Euro 2,20,000, The residual value of machinery has been assumed at Nil; The project

has been funded by debt and equity in equal proportion; Relative Purchasing Power Parity holds good; Cost of equity is

consistent for both in Euro and in Peso, Machinery is disposed of at year Zero; Tax loss on disposal of machinery shall be

set off against other business of Ariel; Inflation in Mexico has been assumed at 7% and in France at 3%.

The computation of the same has been detailed here-in-below:

operations by setting up a new plant which shall be automated and shall be used to recycle and re manufacture toner. The

cost of the plant is estimated at 3.5 Million Pesos or Euro 2,20,000. The company wishes to analyse the feasibility of the

present project based on the details provided and the assumptions undertaken are listed as, The cost of Machinery for the

purpose of analysis has been taken at Euro 2,20,000, The residual value of machinery has been assumed at Nil; The project

has been funded by debt and equity in equal proportion; Relative Purchasing Power Parity holds good; Cost of equity is

consistent for both in Euro and in Peso, Machinery is disposed of at year Zero; Tax loss on disposal of machinery shall be

set off against other business of Ariel; Inflation in Mexico has been assumed at 7% and in France at 3%.

The computation of the same has been detailed here-in-below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sl

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery

-

22000

0

2

Less Sales value of

Machinery

10944

.34

3

Tax Saving on

disposal

1641.

651

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

1360.

104

1540.

997

1745.

95

1978.

161

2037.

506

2098.

631

2161.

59

2226.

438

2293.

231

2362.

028

6 Saving in Labour Cost

35581

.76

40314

.13

45675

.91

51750

.81

53303

.33

54902

.43

56549

.5

58245

.99

59993

.37

61793

.17

7

Saving in Overhead

Cost

6850.

232

7055.

739

7267.

411

7485.

433

7709.

996

7941.

296

8179.

535

8424.

921

8677.

669

8937.

999

8 Depreciation

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

9 Cash flow

21792

.09

26910

.87

32689

.27

39214

.4

41050

.83

42942

.36

44890

.63

46897

.35

48964

.27

51093

.19

10 Tax @35%

-

7627.

23

-

9418.

8

-

11441

.2

-

13725

-

14367

.8

-

15029

.8

-

15711

.7

-

16414

.1

-

17137

.5

-

17882

.6

11 Depreciation 22000 22000 22000 22000 22000 22000 22000 22000 22000 22000

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery

-

22000

0

2

Less Sales value of

Machinery

10944

.34

3

Tax Saving on

disposal

1641.

651

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

1360.

104

1540.

997

1745.

95

1978.

161

2037.

506

2098.

631

2161.

59

2226.

438

2293.

231

2362.

028

6 Saving in Labour Cost

35581

.76

40314

.13

45675

.91

51750

.81

53303

.33

54902

.43

56549

.5

58245

.99

59993

.37

61793

.17

7

Saving in Overhead

Cost

6850.

232

7055.

739

7267.

411

7485.

433

7709.

996

7941.

296

8179.

535

8424.

921

8677.

669

8937.

999

8 Depreciation

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

-

22000

9 Cash flow

21792

.09

26910

.87

32689

.27

39214

.4

41050

.83

42942

.36

44890

.63

46897

.35

48964

.27

51093

.19

10 Tax @35%

-

7627.

23

-

9418.

8

-

11441

.2

-

13725

-

14367

.8

-

15029

.8

-

15711

.7

-

16414

.1

-

17137

.5

-

17882

.6

11 Depreciation 22000 22000 22000 22000 22000 22000 22000 22000 22000 22000

Sl

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

12 Net Cash flow

-

20741

4

36164

.86

39492

.06

43248

.03

47489

.36

48683

.04

49912

.53

51178

.91

52483

.28

53826

.77

55210

.58

13

Discounting factor

@8% 1

0.925

926

0.857

339

0.793

832

0.735

03

0.680

583

0.630

17

0.583

49

0.540

269

0.500

249

0.463

193

14 Present Cash flow

-

20741

4

33485

.98

33858

.08

34331

.68

34906

.1

33132

.86

31453

.36

29862

.4

28355

.08

26926

.79

25573

.18

15 Net Present Value

10447

1.5

On perusal of the above, it can be inferred that the Net Present Value of the project is positive and thus the project shall

be accepted. The conversion has been carried out on the basis of converting the each and every cash inflow and outflow

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

12 Net Cash flow

-

20741

4

36164

.86

39492

.06

43248

.03

47489

.36

48683

.04

49912

.53

51178

.91

52483

.28

53826

.77

55210

.58

13

Discounting factor

@8% 1

0.925

926

0.857

339

0.793

832

0.735

03

0.680

583

0.630

17

0.583

49

0.540

269

0.500

249

0.463

193

14 Present Cash flow

-

20741

4

33485

.98

33858

.08

34331

.68

34906

.1

33132

.86

31453

.36

29862

.4

28355

.08

26926

.79

25573

.18

15 Net Present Value

10447

1.5

On perusal of the above, it can be inferred that the Net Present Value of the project is positive and thus the project shall

be accepted. The conversion has been carried out on the basis of converting the each and every cash inflow and outflow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

from Peso to Euro and then discounting the same using the hurdle rate. The basis of Computation is annexed in Appendix-

1

The Net Present Value under both the solutions differ on account of the following reasons like under the first solution only

the net cash flow has been converted from Peso and Euro while under second solution all the cash flows have been

converted from Peso to Euro., The rate of Discounting used under solution 1 is 9.45% and the rate of discounting used in

solution 2 is 8% on account of difference in rate of debt under both the solution; The cost of machinery is different under

both the scenario.

Arnaud Martin should rely on Model 1 as the project shall be commission in Mexico and thus, he shall initially focus on the

profitability or feasibility of the project under the Mexican Currency i.e. Peso. Thus, Mr. Martin shall rely on Peso data and

compute the Net Present Value on the basis of same and convert net cash flows on the basis of forecasted currency

assuming relative purchasing parity holds good as provided in Solution above. Further, the Mr. Martin as an alternative

discount the converted cash flows with Euro hurdle rate instead of computed peso rate.

1

The Net Present Value under both the solutions differ on account of the following reasons like under the first solution only

the net cash flow has been converted from Peso and Euro while under second solution all the cash flows have been

converted from Peso to Euro., The rate of Discounting used under solution 1 is 9.45% and the rate of discounting used in

solution 2 is 8% on account of difference in rate of debt under both the solution; The cost of machinery is different under

both the scenario.

Arnaud Martin should rely on Model 1 as the project shall be commission in Mexico and thus, he shall initially focus on the

profitability or feasibility of the project under the Mexican Currency i.e. Peso. Thus, Mr. Martin shall rely on Peso data and

compute the Net Present Value on the basis of same and convert net cash flows on the basis of forecasted currency

assuming relative purchasing parity holds good as provided in Solution above. Further, the Mr. Martin as an alternative

discount the converted cash flows with Euro hurdle rate instead of computed peso rate.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In the present context, Groupe Ariel S.A., an entity headquartered in Mulhouse, France is planning to expand its

operations by setting up a new plant which shall be automated and shall be used to recycle and re manufacture toner.

The cost of the plant is estimated at 3.5 Million Pesos or Euro 2,20,000. The company wishes to analyse the feasibility of

the present project based on the details provided and the assumptions undertaken are like the cost of Machinery for the

purpose of analysis has been taken at 3.5 Mio Peso,the residual value of machinery has been assumed at Nil, the project

has been funded by debt and equity in equal proportion, Relative Purchasing Power Parity holds good; Cost of equity is

consistent for both in Euro and in Peso, Machinery is disposed of at year Zero, Tax loss on disposal of machinery shall be

set off against other business of Ariel;, Inflation in Mexico has been assumed at 3% and in France at 3%.

On the basis of above analysis, the discounting factor has been arrived at 9.45%. The computation of the same has been

detailed here-in-below:

Computation of Hurdle rate on peso

Sl No Particulars Brief

1 Hurdle rate in Euro 8%

2 Long Term debt Rate net of tax 3.09%

3 Debt Equity ratio 1.00

4 Equity return 12.91%

5 Long Term debt Rate net of tax in peso 6%

6 Hurdle rate in Peso 9.45%

Further, the analysis has been carried out on the basis of incremental cash flows whereby the difference between the

existing cash flow and the new cash flows on account of execution of the said project shall be taken into consideration. On

the basis of the same, a detailed simulation has been presented here-in-below-

operations by setting up a new plant which shall be automated and shall be used to recycle and re manufacture toner.

The cost of the plant is estimated at 3.5 Million Pesos or Euro 2,20,000. The company wishes to analyse the feasibility of

the present project based on the details provided and the assumptions undertaken are like the cost of Machinery for the

purpose of analysis has been taken at 3.5 Mio Peso,the residual value of machinery has been assumed at Nil, the project

has been funded by debt and equity in equal proportion, Relative Purchasing Power Parity holds good; Cost of equity is

consistent for both in Euro and in Peso, Machinery is disposed of at year Zero, Tax loss on disposal of machinery shall be

set off against other business of Ariel;, Inflation in Mexico has been assumed at 3% and in France at 3%.

On the basis of above analysis, the discounting factor has been arrived at 9.45%. The computation of the same has been

detailed here-in-below:

Computation of Hurdle rate on peso

Sl No Particulars Brief

1 Hurdle rate in Euro 8%

2 Long Term debt Rate net of tax 3.09%

3 Debt Equity ratio 1.00

4 Equity return 12.91%

5 Long Term debt Rate net of tax in peso 6%

6 Hurdle rate in Peso 9.45%

Further, the analysis has been carried out on the basis of incremental cash flows whereby the difference between the

existing cash flow and the new cash flows on account of execution of the said project shall be taken into consideration. On

the basis of the same, a detailed simulation has been presented here-in-below-

Sl

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery

-

35000

00

2

Less Sales value

of Machinery

17500

0

3

Tax Saving on

disposal 26250

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

22592.

64

26591.

54

31298.

24

36838.

03

39416.

69

42175.

86

45128.

17

48287.

14

51667.

24

55283.

95

6

Saving in Labour

Cost

59104

7.5

69566

2.9

81879

5.3

96372

2

10311

83

11033

65

11806

01

12632

43

13516

70

14462

87

7

Saving in

Overhead Cost

11378

9

12175

4.2

13027

7

13939

6.4

14915

4.2

15959

5

17076

6.6

18272

0.3

19551

0.7

20919

6.4

8 Depreciation

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

9 Cash flow

37742

9.2

49400

8.7

63037

0.5

78995

6.5

86975

3.4

95513

6.2

10464

96

11442

50

12488

48

13607

67

10 Tax @35% -

13210

-

17290

-

22063

-

27648

-

30441

-

33429

-

36627

-

40048

-

43709

-

47626

No Particular 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

1 Cost of Machinery

-

35000

00

2

Less Sales value

of Machinery

17500

0

3

Tax Saving on

disposal 26250

4

Incremental Unit

Volume 0 0 0 0 0 0 0 0 0 0

5

Saving in Material

Cost

22592.

64

26591.

54

31298.

24

36838.

03

39416.

69

42175.

86

45128.

17

48287.

14

51667.

24

55283.

95

6

Saving in Labour

Cost

59104

7.5

69566

2.9

81879

5.3

96372

2

10311

83

11033

65

11806

01

12632

43

13516

70

14462

87

7

Saving in

Overhead Cost

11378

9

12175

4.2

13027

7

13939

6.4

14915

4.2

15959

5

17076

6.6

18272

0.3

19551

0.7

20919

6.4

8 Depreciation

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

-

35000

0

9 Cash flow

37742

9.2

49400

8.7

63037

0.5

78995

6.5

86975

3.4

95513

6.2

10464

96

11442

50

12488

48

13607

67

10 Tax @35% -

13210

-

17290

-

22063

-

27648

-

30441

-

33429

-

36627

-

40048

-

43709

-

47626

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.