Comprehensive Audit Report and Analysis: Aristocrat Leisure Ltd

VerifiedAdded on 2022/08/26

|17

|3017

|22

Report

AI Summary

This report conducts an audit framework analysis of Aristocrat Leisure Ltd., examining the company's activities, financial aspects, and associated risks. It delves into the inherent risks, control risks, and detection risks within the audit process, emphasizing potential material misstatements. The report reviews the company's financial statements over three years, analyzing the impact of accounting standards like AASB 9, AASB 15, and AASB 16. It assesses business risks, including competitive, economic, legal, and foreign-exchange risks. The study also explores the impact of the control environment on audit planning and examines the composition of the company's equity, debt structure, income tax figures, and asset valuation. The analysis provides insights into the company's financial health and highlights key considerations for auditors and stakeholders.

Running Head: AUDITING

AUDITING

Name of the Student

Name of the University

Author Note

AUDITING

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Executive Summary

The purpose of this paper is to do audit framework of Aristocrat Leisure Ltd. The study is

supported by reviewing the annual reports of the three financial year of the company. It was

found that, various audit risks have been involved in the company audit process that has led

to misstatement of the company’s financial statement.

Executive Summary

The purpose of this paper is to do audit framework of Aristocrat Leisure Ltd. The study is

supported by reviewing the annual reports of the three financial year of the company. It was

found that, various audit risks have been involved in the company audit process that has led

to misstatement of the company’s financial statement.

2AUDITING

Table of Contents

Introduction................................................................................................................................3

Nature of Aristocrat Activities...................................................................................................3

Analytical Review of the Aristocrat Leisure Ltd.......................................................................3

Audit Risks.............................................................................................................................5

Business Risks........................................................................................................................6

Impact of Control Environment on Audit Planning...................................................................7

Composition of Company Equity...............................................................................................8

Conclusions..............................................................................................................................10

References................................................................................................................................11

Appendix..................................................................................................................................14

Table of Contents

Introduction................................................................................................................................3

Nature of Aristocrat Activities...................................................................................................3

Analytical Review of the Aristocrat Leisure Ltd.......................................................................3

Audit Risks.............................................................................................................................5

Business Risks........................................................................................................................6

Impact of Control Environment on Audit Planning...................................................................7

Composition of Company Equity...............................................................................................8

Conclusions..............................................................................................................................10

References................................................................................................................................11

Appendix..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

Introduction

This report provides the basic information’s related to auditing process of Aristocrat

limited. The first part of the paper has discussed on, the various risks associated with the

audit process of Aristocrat Leisure. The next part has viewed on the financial aspects of the

business on the basis of three financial year. The intense of this report is to do audit

frameworks associated with the Aristocrat Leisure.

Nature of Aristocrat Activities

Aristocrat Leisure is a leading producer of gaming related products. Most of the

products includes; gaming machines, digital games, casino management systems. The

company has more than 300 licensed business operations over 90 countries. The company is

a publicly traded company, listed in Australian Stock Exchange (Venkatadri et al., 2018).

VGT is an Aristocrat Company, which is a leading developer and manufacturer of casino

games in parts of Northern America. It has nearly 140 distributer locations in the country.

Aristocrat Leisure is head quartered in Sydney city of Australia. It also has a development

and marketing offices in South Africa and United States. The company is currently listed in

second position in manufacturing of slot machines of gaming technology. Trevor Croker is

the Chief Executive Officer of the Aristocrat group since, 2017. In the year 2017, the

company has entered in providing technologies for mobile gaming and acquired with big fish

Games, which is a largest mobile game developer. Plarium is the mobile gaming technology

that has gained a dedicated fan based reputation in terms of providing exceptional values.

Analytical Review of the Aristocrat Leisure Ltd

Risk Assessment

Introduction

This report provides the basic information’s related to auditing process of Aristocrat

limited. The first part of the paper has discussed on, the various risks associated with the

audit process of Aristocrat Leisure. The next part has viewed on the financial aspects of the

business on the basis of three financial year. The intense of this report is to do audit

frameworks associated with the Aristocrat Leisure.

Nature of Aristocrat Activities

Aristocrat Leisure is a leading producer of gaming related products. Most of the

products includes; gaming machines, digital games, casino management systems. The

company has more than 300 licensed business operations over 90 countries. The company is

a publicly traded company, listed in Australian Stock Exchange (Venkatadri et al., 2018).

VGT is an Aristocrat Company, which is a leading developer and manufacturer of casino

games in parts of Northern America. It has nearly 140 distributer locations in the country.

Aristocrat Leisure is head quartered in Sydney city of Australia. It also has a development

and marketing offices in South Africa and United States. The company is currently listed in

second position in manufacturing of slot machines of gaming technology. Trevor Croker is

the Chief Executive Officer of the Aristocrat group since, 2017. In the year 2017, the

company has entered in providing technologies for mobile gaming and acquired with big fish

Games, which is a largest mobile game developer. Plarium is the mobile gaming technology

that has gained a dedicated fan based reputation in terms of providing exceptional values.

Analytical Review of the Aristocrat Leisure Ltd

Risk Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

Risk Assessment of a company is done, by evaluating the inherent risk and control

risks associated by the business activity. This can be done by understanding the business and

its environment.

Regulatory Frameworks of Aristocrat Leisure Ltd

Aristocrat Leisure follows the statutory requirements of Australian Accounting

Standard rules, AASB 2 for reporting their share growth and remuneration on the basis of

shares to the shareholders (Thottoli, Thomas & Ahmed 2019). The financial Statements is

prepared according to the International Financial Reporting Standards (IFRS), International

Accounting Standards (IASB) and corporations Act 2001. The financial report is presented

on historical cost basis and the cost of assets & liabilities are measured on fair value. Certain

policies have been applied during the preparations. The overall accounting reporting is done

by following the ASSB 9, AASB 15, AASB 16 standards of Australian Accounting Standards

Boards.

AASB 9- This is an Australian accounting standards for the financial instruments.

This standard involves the measurements and recognition of the assets and liabilities

of the company. This involves the reformed approach for doing hedge accounting.

Aristocrat has reviewed this standard of accounting, to find the impact of new

expected loss model.

AASB 15- This is an accounting standard for finding the revenue generated from the

contracts with the customers. It is based on the principle that, revenue is only

recognised, if the goods & services are moved to the customers (Moorthy et al.,

2011). This accounting principle has replaced the standards of ASSB 118 and AASB

111 of the revenue and construction contracts. Aristocrat leisure group has mainly

focused on the revenue streams to identify the impact of this standard and develop a

Risk Assessment of a company is done, by evaluating the inherent risk and control

risks associated by the business activity. This can be done by understanding the business and

its environment.

Regulatory Frameworks of Aristocrat Leisure Ltd

Aristocrat Leisure follows the statutory requirements of Australian Accounting

Standard rules, AASB 2 for reporting their share growth and remuneration on the basis of

shares to the shareholders (Thottoli, Thomas & Ahmed 2019). The financial Statements is

prepared according to the International Financial Reporting Standards (IFRS), International

Accounting Standards (IASB) and corporations Act 2001. The financial report is presented

on historical cost basis and the cost of assets & liabilities are measured on fair value. Certain

policies have been applied during the preparations. The overall accounting reporting is done

by following the ASSB 9, AASB 15, AASB 16 standards of Australian Accounting Standards

Boards.

AASB 9- This is an Australian accounting standards for the financial instruments.

This standard involves the measurements and recognition of the assets and liabilities

of the company. This involves the reformed approach for doing hedge accounting.

Aristocrat has reviewed this standard of accounting, to find the impact of new

expected loss model.

AASB 15- This is an accounting standard for finding the revenue generated from the

contracts with the customers. It is based on the principle that, revenue is only

recognised, if the goods & services are moved to the customers (Moorthy et al.,

2011). This accounting principle has replaced the standards of ASSB 118 and AASB

111 of the revenue and construction contracts. Aristocrat leisure group has mainly

focused on the revenue streams to identify the impact of this standard and develop a

5AUDITING

new accounting policy. They have classified all the jackpot liability expenses, in

contra revenues, instead of listing in expenses.

AASB 16- This is an accounting standard for leases. This standard has removed the

lease classifications in operating and finance lease. The lease is listed in on-balance

liabilities on the balance sheet. Aristocrat Group has assessed the impact of this

accounting standard on the balance sheet (Ma et al., 2019).

Audit Risks

1. Inherent Risk

Material Misstatement- This is the information that is incorrect and can impact the

business decisions. The total revenue of Aristocrat Group is represented by using

system contracts and machine sales. This system contains multiple arrangements,

which is quiet a complex process. This is due to delayed customer services, delay in

settlements and other contractual arrangements with the customers. There is a risk

involved during the contractual arrangements with the customers and may result in

inventory related risks. This sales is not recognised in the annual financial report of

the company. This can result in material misstatement of the reported revenue in that

financial year. The investors can be triggered while making decisions to buy the

company stock. Cash and cash equivalent reported in the financial statement includes

cash on hand, deposits and bank overdrafts. A very highly liquidable investments,

having a short-term maturity of three months or less than this can readily converted

into cash. There can be a risk of change in the value of cash on hand.

Going Concern- Aristocrat Leisure has a social sustainability risks related to business

performance. Various risks is tangled in meeting the demands of the changing

preferences of the gaming features, creating a sustainable employee relations,

new accounting policy. They have classified all the jackpot liability expenses, in

contra revenues, instead of listing in expenses.

AASB 16- This is an accounting standard for leases. This standard has removed the

lease classifications in operating and finance lease. The lease is listed in on-balance

liabilities on the balance sheet. Aristocrat Group has assessed the impact of this

accounting standard on the balance sheet (Ma et al., 2019).

Audit Risks

1. Inherent Risk

Material Misstatement- This is the information that is incorrect and can impact the

business decisions. The total revenue of Aristocrat Group is represented by using

system contracts and machine sales. This system contains multiple arrangements,

which is quiet a complex process. This is due to delayed customer services, delay in

settlements and other contractual arrangements with the customers. There is a risk

involved during the contractual arrangements with the customers and may result in

inventory related risks. This sales is not recognised in the annual financial report of

the company. This can result in material misstatement of the reported revenue in that

financial year. The investors can be triggered while making decisions to buy the

company stock. Cash and cash equivalent reported in the financial statement includes

cash on hand, deposits and bank overdrafts. A very highly liquidable investments,

having a short-term maturity of three months or less than this can readily converted

into cash. There can be a risk of change in the value of cash on hand.

Going Concern- Aristocrat Leisure has a social sustainability risks related to business

performance. Various risks is tangled in meeting the demands of the changing

preferences of the gaming features, creating a sustainable employee relations,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

maintaining of diversity and inclusion in the work place and corporate governance

(Green, 2016).

2. Control Risk

This type of risk has been raised, when the financial statements are materially

misstated due to failure in the system control. The company has developed a third party

development partners for licensing the games. Their success depends on the reliable

partners on the basis of their existing content (Khattab, 2016). The group faces a risk in

expire during some instances. A new team similar to third party developers can be

developed to mitigate this type of risks. Eve, the data stored in the information technology

systems has the risk of cyber-attacks and security failures. This can result in disclosure of

any confidential information of the company. The above risks can be controlled by

making more and more investments, in the data management practices and cyber security

measures in order to respond towards these type of threats.

3. Detection Risks- The auditors of the Aristocrat Leisure have concluded that, the

financial report presented by the company, is giving a true and fair value of the actual

financial position of the business & is complied with the Australian Accounting

Standards and Corporation Regulation act 2001. They have concluded that, there are

no material misstatement involved in the financial statement. But, there is a managing

detection risk found in the financial statement. Material misstatement was found in

the process. Hence, Aristocrat has detection risks during the audit process. They have

only reviewed on the sample of their business transactions.

maintaining of diversity and inclusion in the work place and corporate governance

(Green, 2016).

2. Control Risk

This type of risk has been raised, when the financial statements are materially

misstated due to failure in the system control. The company has developed a third party

development partners for licensing the games. Their success depends on the reliable

partners on the basis of their existing content (Khattab, 2016). The group faces a risk in

expire during some instances. A new team similar to third party developers can be

developed to mitigate this type of risks. Eve, the data stored in the information technology

systems has the risk of cyber-attacks and security failures. This can result in disclosure of

any confidential information of the company. The above risks can be controlled by

making more and more investments, in the data management practices and cyber security

measures in order to respond towards these type of threats.

3. Detection Risks- The auditors of the Aristocrat Leisure have concluded that, the

financial report presented by the company, is giving a true and fair value of the actual

financial position of the business & is complied with the Australian Accounting

Standards and Corporation Regulation act 2001. They have concluded that, there are

no material misstatement involved in the financial statement. But, there is a managing

detection risk found in the financial statement. Material misstatement was found in

the process. Hence, Aristocrat has detection risks during the audit process. They have

only reviewed on the sample of their business transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

Business Risks

Business risks are the type of risks, which can prevent the Aristocrat Group in

achieving their objectives. The following business risks associated with Aristocrat Leisure

are:

1. Competitive Risk- There is an intensified competition in the gaming industry.

Innovations in products, reliability and price associated with the products, are

tremendously affecting the selling of the company’s products. Frequent product

innovations is necessary to compete with the emerging platforms and the

technologies. The group’s success is depended on the innovations of the new products

and investments in new skills & development process.

2. Economic risks- The demand for the products and services are continuously changing.

The demand depends on the favourable conditions of the gaming industry. There

could be possibility of decline in economic conditions of the Aristocrat Group. The

company can have an inadequate capital to finance their business operations. This can

result in economic risks of the business.

3. Legal Risks- Gaming Industries is subjected to government regulations requirements,

which includes license permission, documentations of various qualifications. There

can be possibility of change in regulations by the government. This could adversely

affect the business strategy and could have a negative impact on the business (Visser

& van Scheers 2018).

4. Foreign-exchange risks- The group operates across the world and could have an

impact on the risks related to currency exposures related to Dollar and Euro. This type

of risks may arise due to the commercial transactions of the debts and assets in the

form of foreign currency.

Business Risks

Business risks are the type of risks, which can prevent the Aristocrat Group in

achieving their objectives. The following business risks associated with Aristocrat Leisure

are:

1. Competitive Risk- There is an intensified competition in the gaming industry.

Innovations in products, reliability and price associated with the products, are

tremendously affecting the selling of the company’s products. Frequent product

innovations is necessary to compete with the emerging platforms and the

technologies. The group’s success is depended on the innovations of the new products

and investments in new skills & development process.

2. Economic risks- The demand for the products and services are continuously changing.

The demand depends on the favourable conditions of the gaming industry. There

could be possibility of decline in economic conditions of the Aristocrat Group. The

company can have an inadequate capital to finance their business operations. This can

result in economic risks of the business.

3. Legal Risks- Gaming Industries is subjected to government regulations requirements,

which includes license permission, documentations of various qualifications. There

can be possibility of change in regulations by the government. This could adversely

affect the business strategy and could have a negative impact on the business (Visser

& van Scheers 2018).

4. Foreign-exchange risks- The group operates across the world and could have an

impact on the risks related to currency exposures related to Dollar and Euro. This type

of risks may arise due to the commercial transactions of the debts and assets in the

form of foreign currency.

8AUDITING

Impact of Control Environment on Audit Planning

Control Environment is the foundation in which, the internal control of an

organisation is built in order to attain the strategic goal of the organisation (Kljucnikov et al.

2016). Looking into the internal control environment of Aristocrat group, it can be seen that,

the company has adopted Australian accounting standards and principle to do the accounting

process. The business structure and processes have been integrated and coordinated to

maintain the control process of the group (Williams & Hausman 2017). The board of

directors has satisfied in providing the non-audit services, for successful audit process in

compatible to the general standards of auditing. All the non-audit services are viewed by the

entire audit committee of the organisation in order to ensure the objectivity is successfully

achieved. Internal control of business structure has allowed the audit committee to make

decisions on various assignments. The audit process is committed to ethical values of the

society and the business. The company has applied APES 110 code of ethics for professional

accountants for successfully reviewing the audit frameworks and acting within the

management and decision-making capacity of the Company. The company has a charter of

audit independence that specifies that, various non-audit services cannot be performed by the

auditor of the company (Chen et al., 2017). Individual board of directors have individual

responsibilities to ensure that, the company objective is achieved within the corporate

governance. These controlled activities of a business can have a severe impact in the

business.

Composition of Company Equity

Ordinary shares are issued by the company, that has no par value and the shareholders

are allowed to participate in the dividends. The holders of these ordinary shares, are allowed

to vote do one vote on one shares during the company meetings. During the issue of new

shares, incremental costs are directly attributed to the shares and is showed as contributed

Impact of Control Environment on Audit Planning

Control Environment is the foundation in which, the internal control of an

organisation is built in order to attain the strategic goal of the organisation (Kljucnikov et al.

2016). Looking into the internal control environment of Aristocrat group, it can be seen that,

the company has adopted Australian accounting standards and principle to do the accounting

process. The business structure and processes have been integrated and coordinated to

maintain the control process of the group (Williams & Hausman 2017). The board of

directors has satisfied in providing the non-audit services, for successful audit process in

compatible to the general standards of auditing. All the non-audit services are viewed by the

entire audit committee of the organisation in order to ensure the objectivity is successfully

achieved. Internal control of business structure has allowed the audit committee to make

decisions on various assignments. The audit process is committed to ethical values of the

society and the business. The company has applied APES 110 code of ethics for professional

accountants for successfully reviewing the audit frameworks and acting within the

management and decision-making capacity of the Company. The company has a charter of

audit independence that specifies that, various non-audit services cannot be performed by the

auditor of the company (Chen et al., 2017). Individual board of directors have individual

responsibilities to ensure that, the company objective is achieved within the corporate

governance. These controlled activities of a business can have a severe impact in the

business.

Composition of Company Equity

Ordinary shares are issued by the company, that has no par value and the shareholders

are allowed to participate in the dividends. The holders of these ordinary shares, are allowed

to vote do one vote on one shares during the company meetings. During the issue of new

shares, incremental costs are directly attributed to the shares and is showed as contributed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

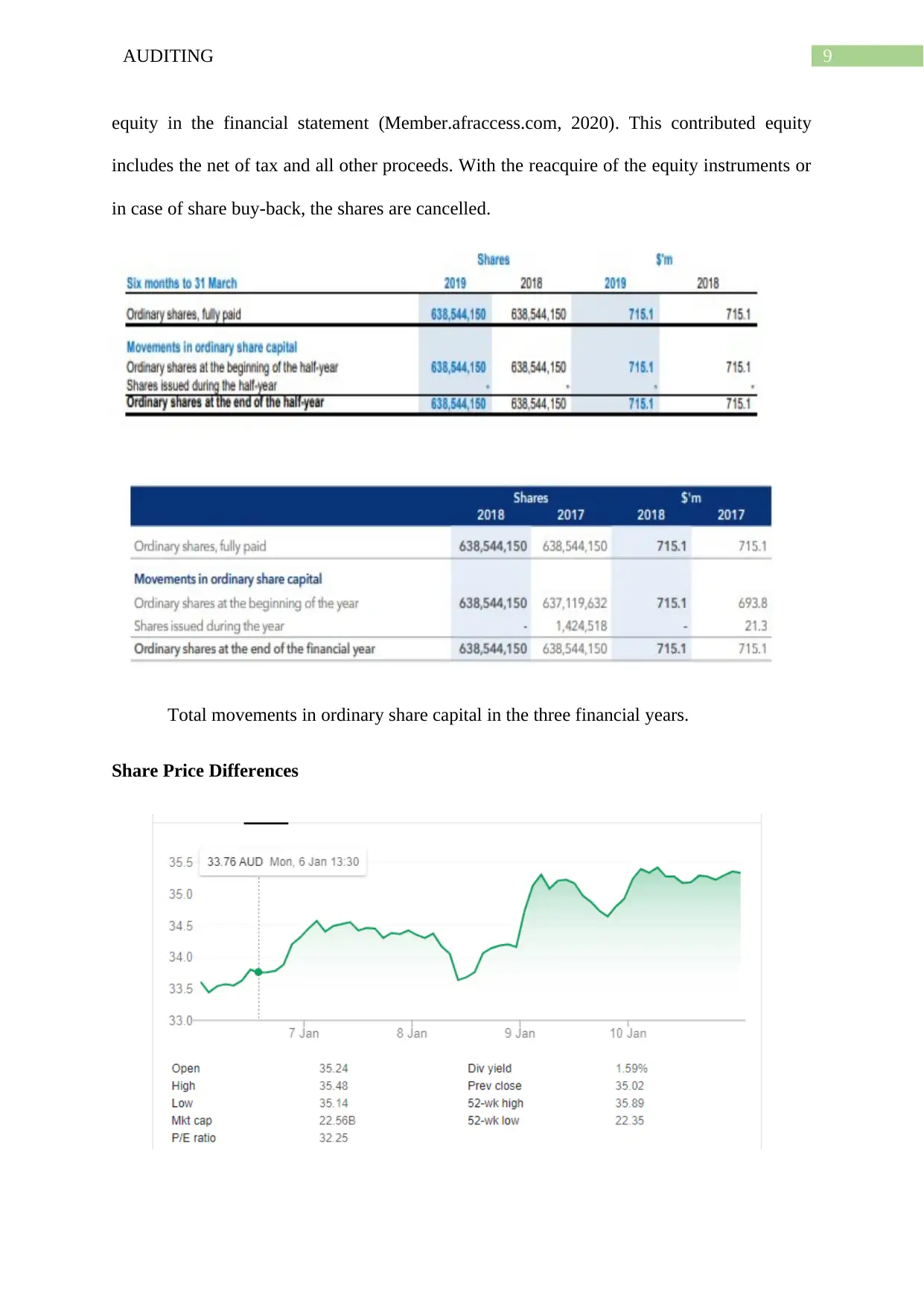

equity in the financial statement (Member.afraccess.com, 2020). This contributed equity

includes the net of tax and all other proceeds. With the reacquire of the equity instruments or

in case of share buy-back, the shares are cancelled.

Total movements in ordinary share capital in the three financial years.

Share Price Differences

equity in the financial statement (Member.afraccess.com, 2020). This contributed equity

includes the net of tax and all other proceeds. With the reacquire of the equity instruments or

in case of share buy-back, the shares are cancelled.

Total movements in ordinary share capital in the three financial years.

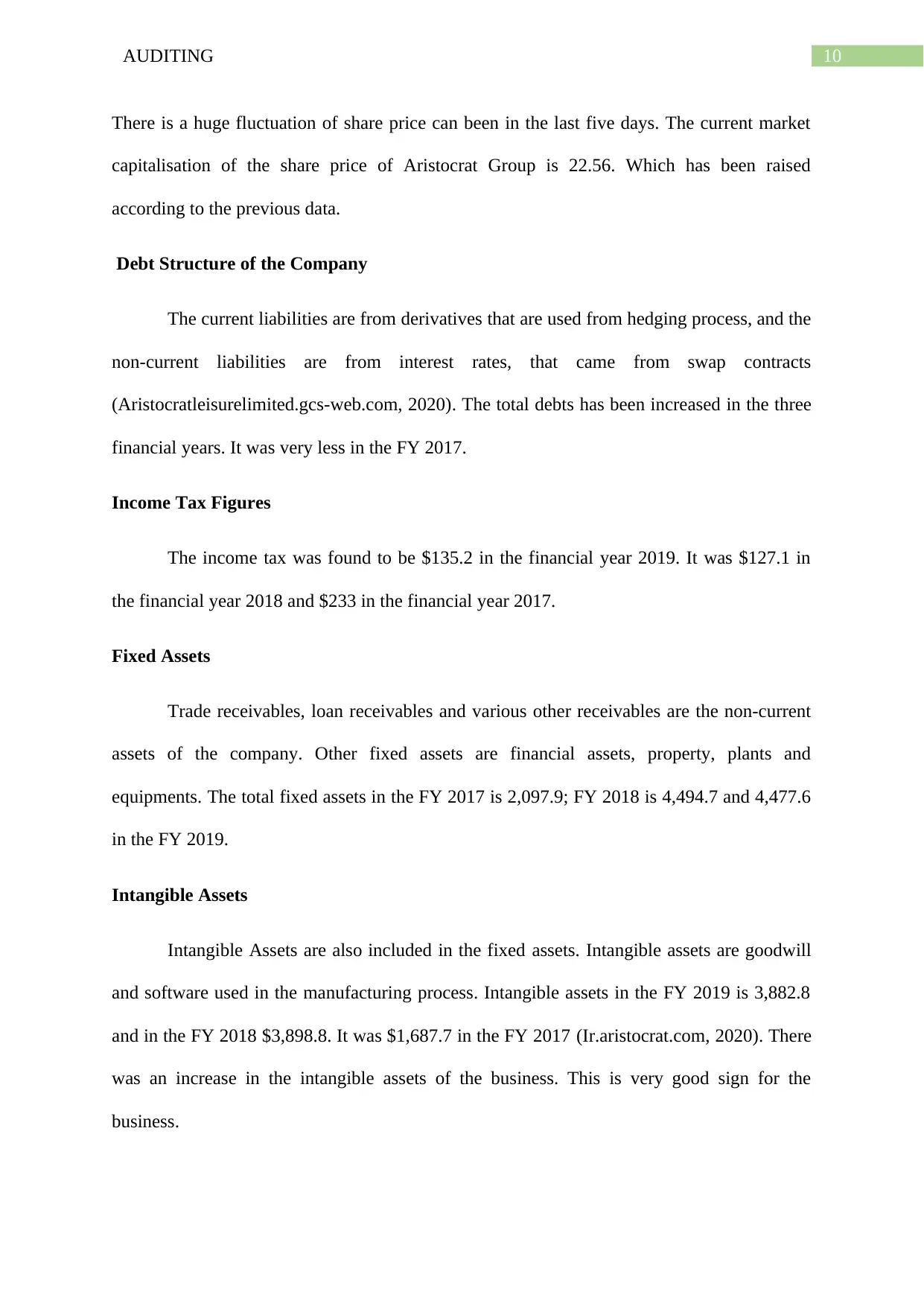

Share Price Differences

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

There is a huge fluctuation of share price can been in the last five days. The current market

capitalisation of the share price of Aristocrat Group is 22.56. Which has been raised

according to the previous data.

Debt Structure of the Company

The current liabilities are from derivatives that are used from hedging process, and the

non-current liabilities are from interest rates, that came from swap contracts

(Aristocratleisurelimited.gcs-web.com, 2020). The total debts has been increased in the three

financial years. It was very less in the FY 2017.

Income Tax Figures

The income tax was found to be $135.2 in the financial year 2019. It was $127.1 in

the financial year 2018 and $233 in the financial year 2017.

Fixed Assets

Trade receivables, loan receivables and various other receivables are the non-current

assets of the company. Other fixed assets are financial assets, property, plants and

equipments. The total fixed assets in the FY 2017 is 2,097.9; FY 2018 is 4,494.7 and 4,477.6

in the FY 2019.

Intangible Assets

Intangible Assets are also included in the fixed assets. Intangible assets are goodwill

and software used in the manufacturing process. Intangible assets in the FY 2019 is 3,882.8

and in the FY 2018 $3,898.8. It was $1,687.7 in the FY 2017 (Ir.aristocrat.com, 2020). There

was an increase in the intangible assets of the business. This is very good sign for the

business.

There is a huge fluctuation of share price can been in the last five days. The current market

capitalisation of the share price of Aristocrat Group is 22.56. Which has been raised

according to the previous data.

Debt Structure of the Company

The current liabilities are from derivatives that are used from hedging process, and the

non-current liabilities are from interest rates, that came from swap contracts

(Aristocratleisurelimited.gcs-web.com, 2020). The total debts has been increased in the three

financial years. It was very less in the FY 2017.

Income Tax Figures

The income tax was found to be $135.2 in the financial year 2019. It was $127.1 in

the financial year 2018 and $233 in the financial year 2017.

Fixed Assets

Trade receivables, loan receivables and various other receivables are the non-current

assets of the company. Other fixed assets are financial assets, property, plants and

equipments. The total fixed assets in the FY 2017 is 2,097.9; FY 2018 is 4,494.7 and 4,477.6

in the FY 2019.

Intangible Assets

Intangible Assets are also included in the fixed assets. Intangible assets are goodwill

and software used in the manufacturing process. Intangible assets in the FY 2019 is 3,882.8

and in the FY 2018 $3,898.8. It was $1,687.7 in the FY 2017 (Ir.aristocrat.com, 2020). There

was an increase in the intangible assets of the business. This is very good sign for the

business.

11AUDITING

Conclusions

Therefore, it can be deferred that, the audit process of aristocrat leisure has evolved

into various errors in the financial statement of the business. There were various audit risks

like inherent risks, control risks and defected risks involved in the audit process of the

Aristocrat Group.

Conclusions

Therefore, it can be deferred that, the audit process of aristocrat leisure has evolved

into various errors in the financial statement of the business. There were various audit risks

like inherent risks, control risks and defected risks involved in the audit process of the

Aristocrat Group.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.