Corporate Financial Management: ALL Stock Performance Analysis Report

VerifiedAdded on 2022/10/09

|10

|1183

|85

Report

AI Summary

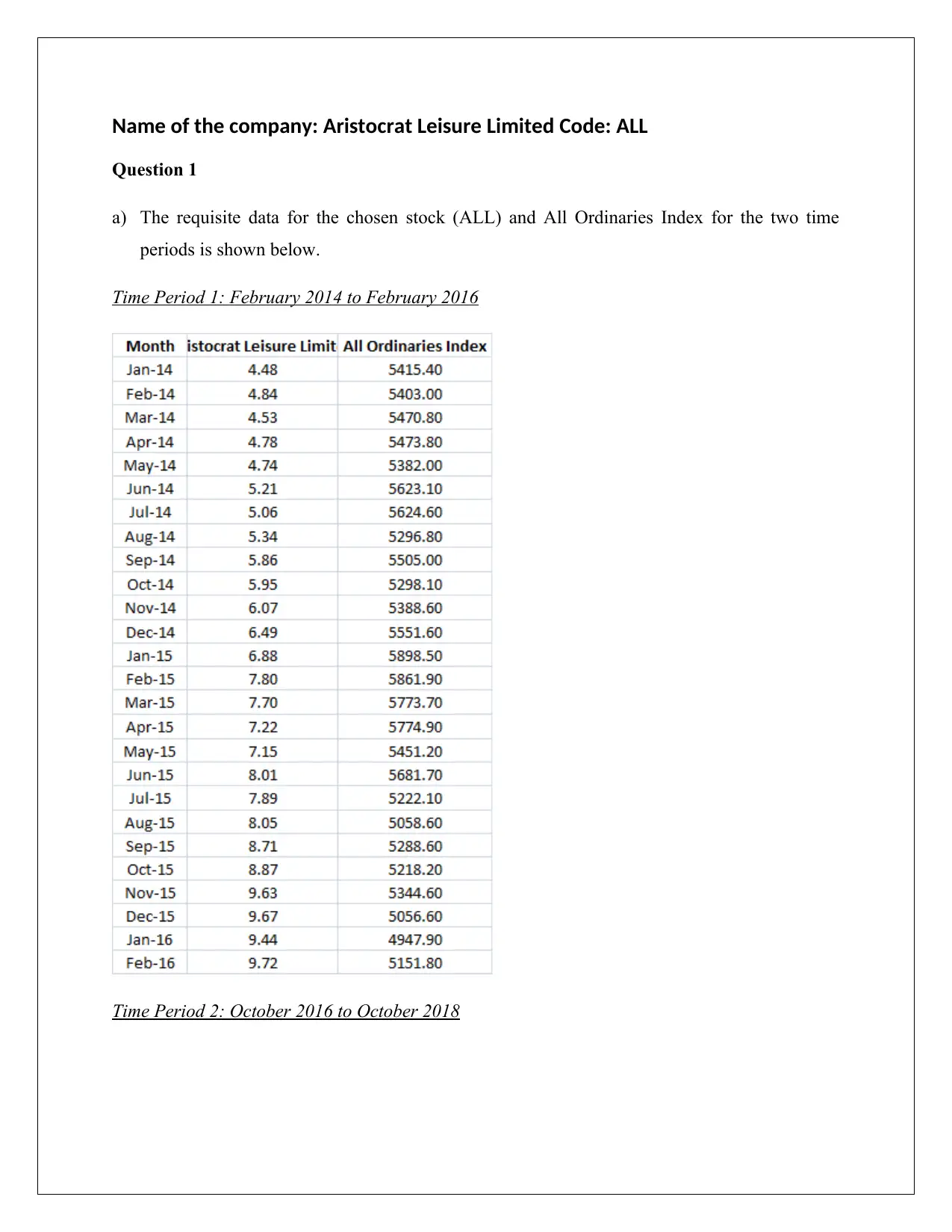

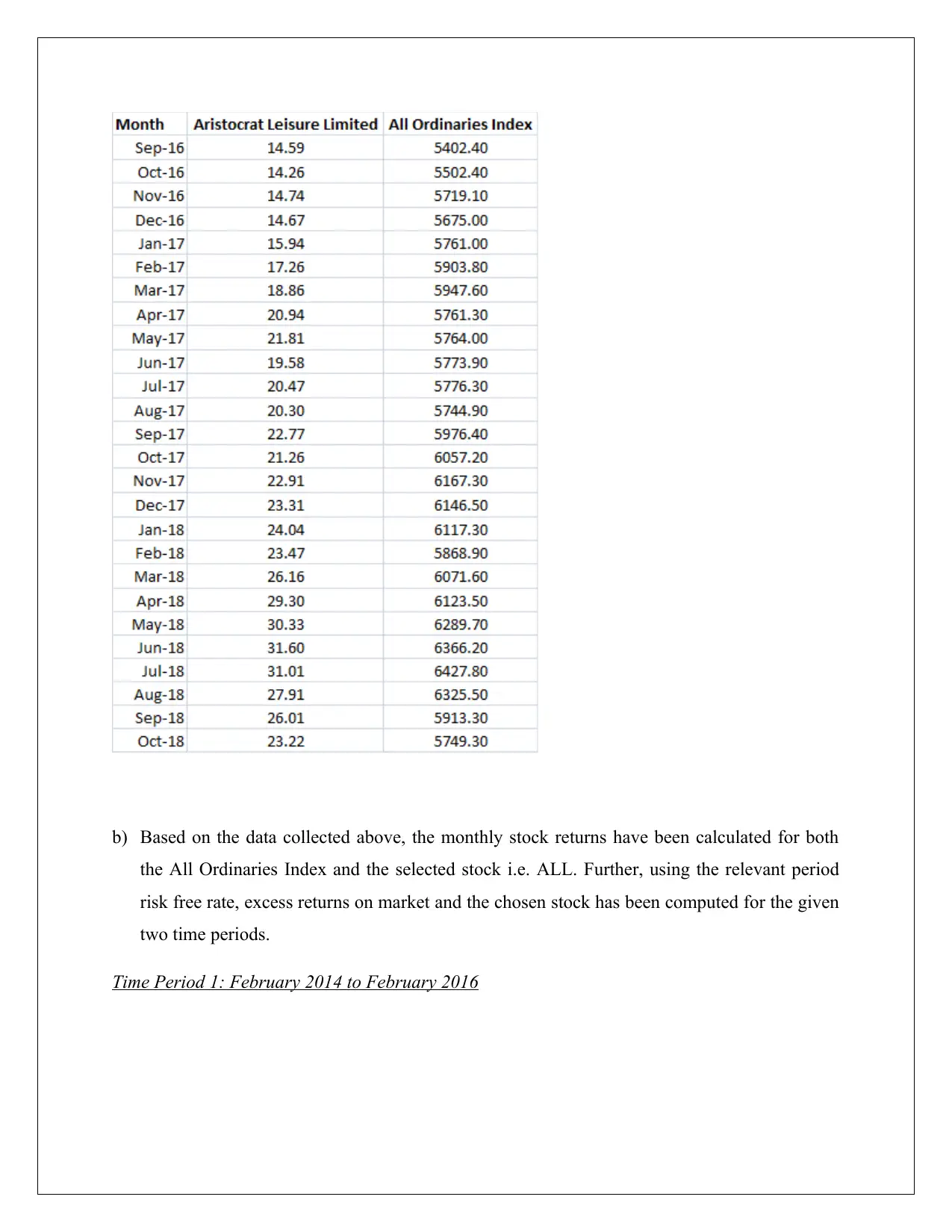

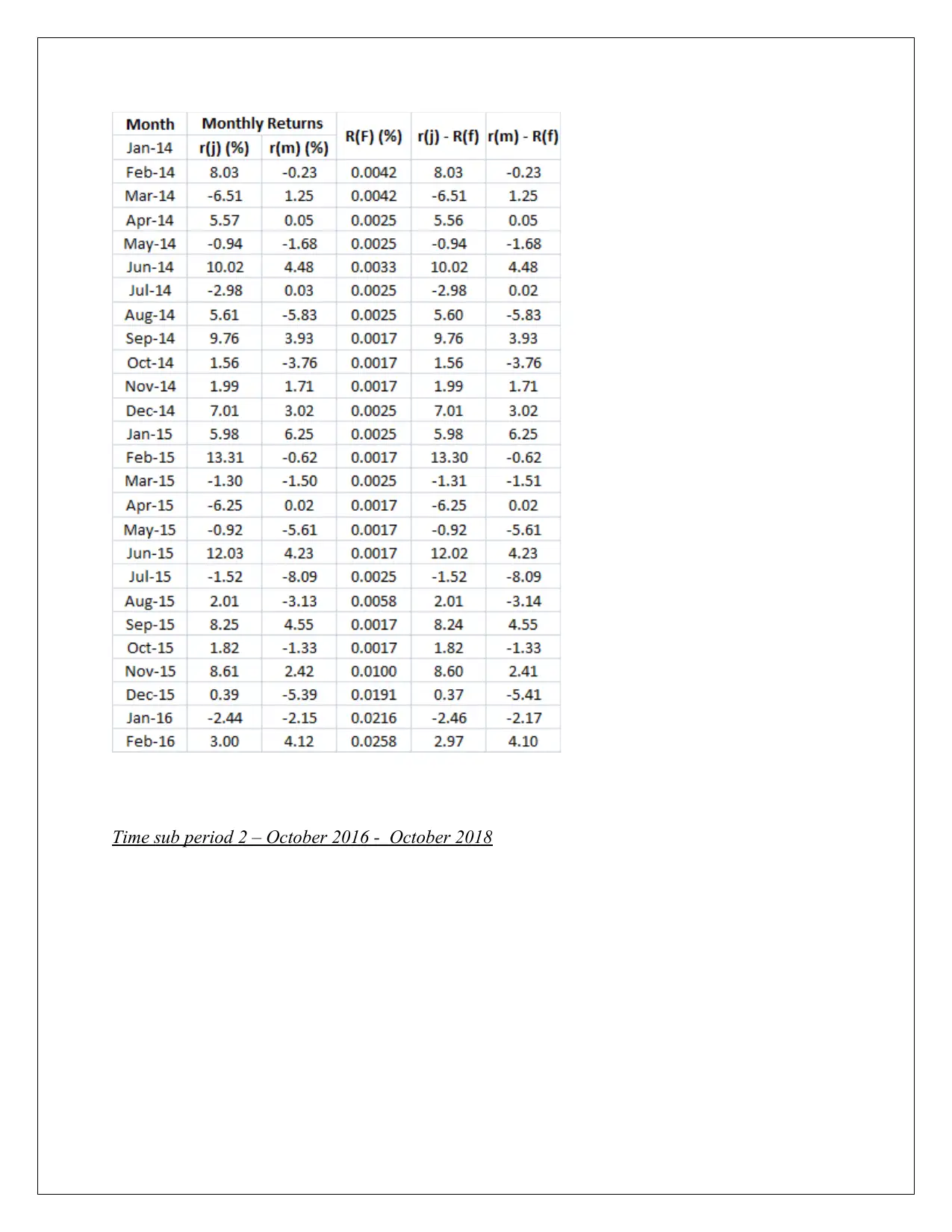

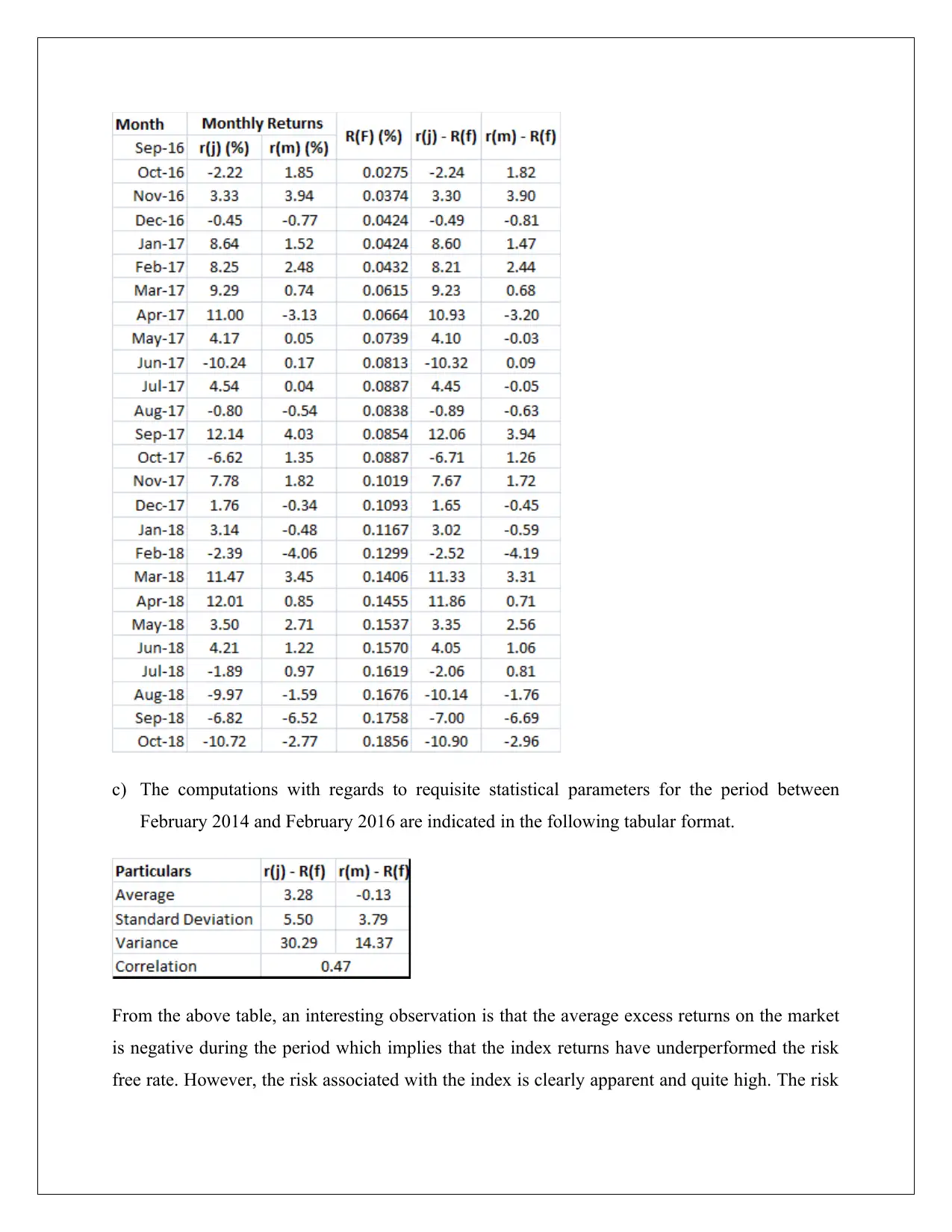

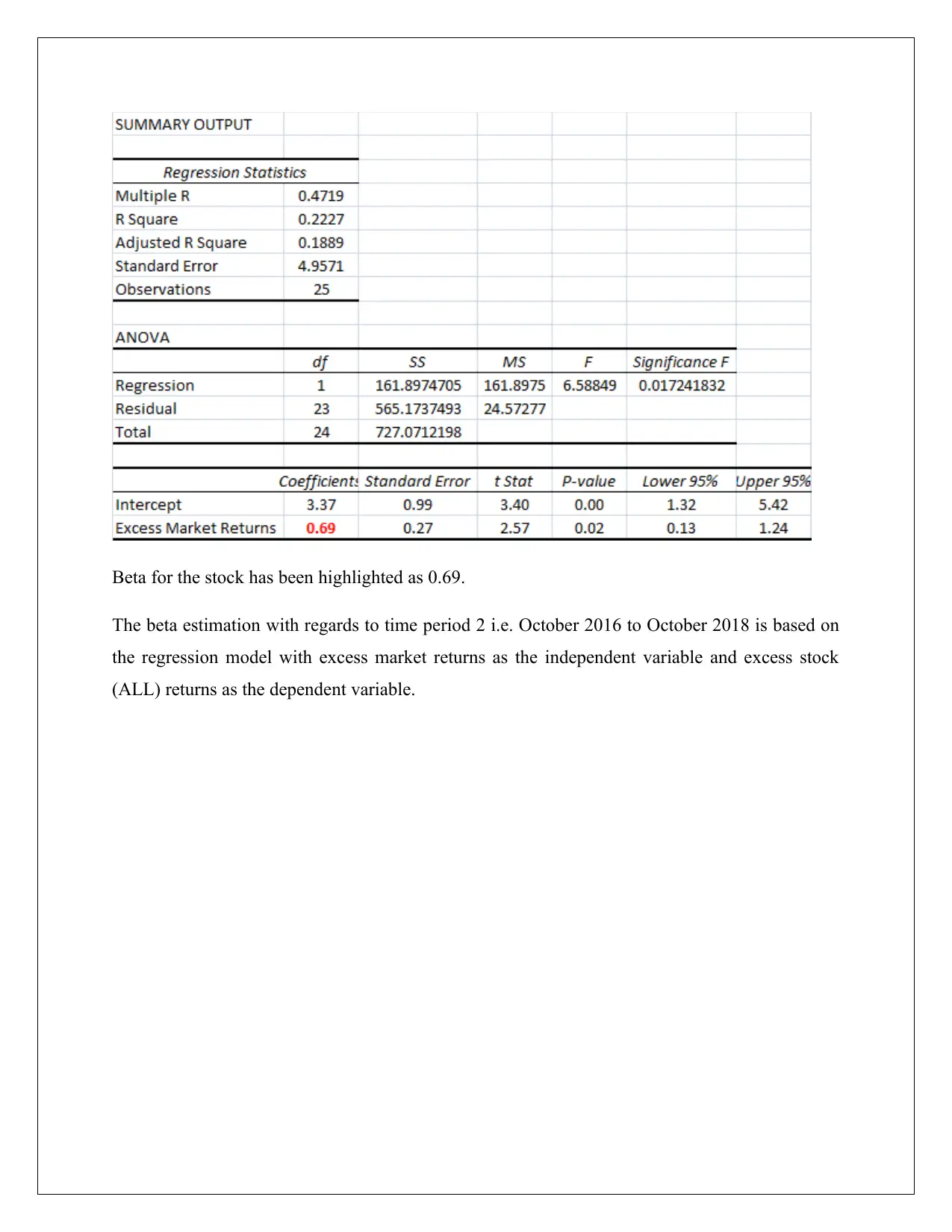

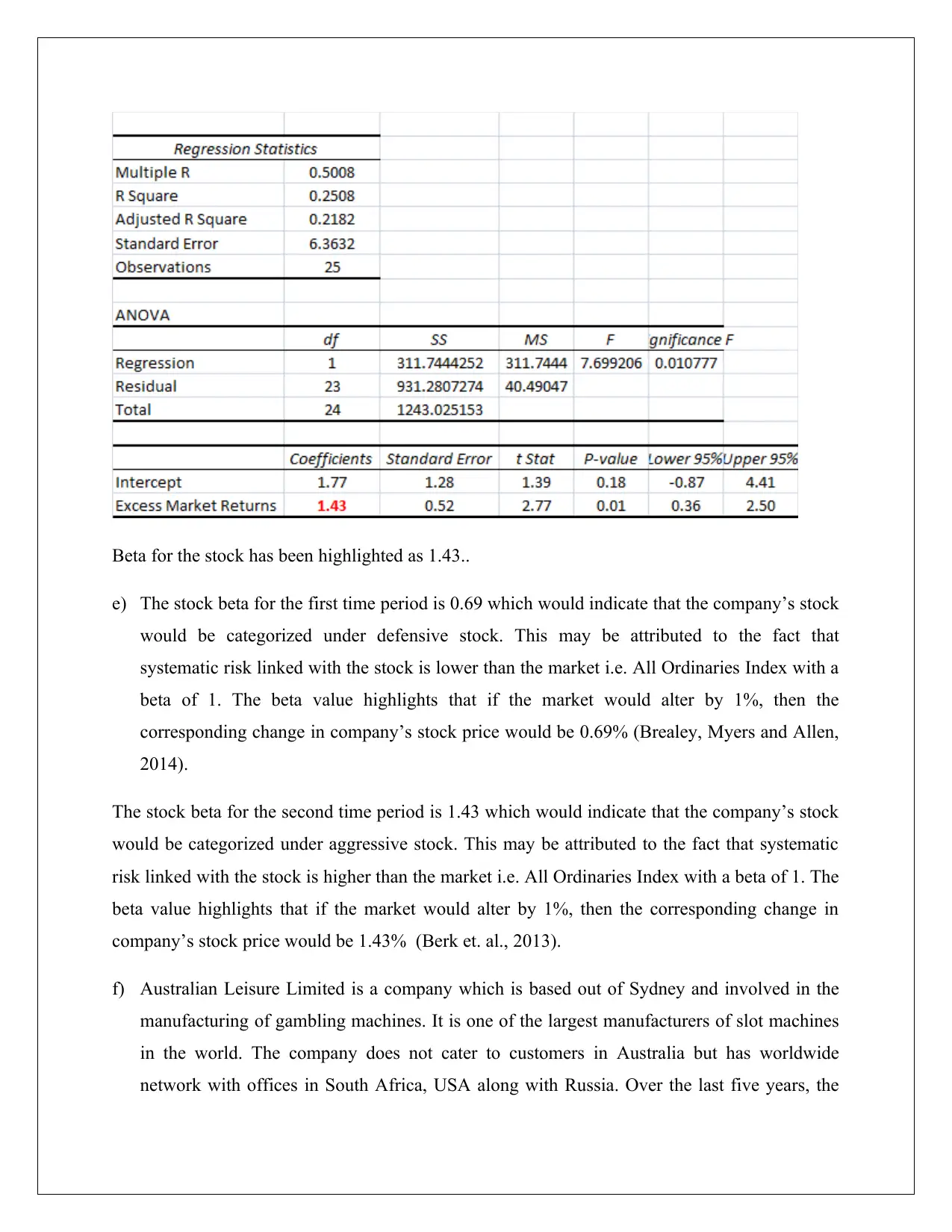

This report presents a financial analysis of Aristocrat Leisure Limited (ALL) stock, examining its performance over two distinct time periods: February 2014 to February 2016 and October 2016 to October 2018. The analysis includes the calculation of monthly stock returns, excess returns, and statistical parameters such as mean, standard deviation, variance, and correlation coefficients for both the stock and the All Ordinaries Index. The report also estimates the beta for the stock in both periods, categorizing the stock as defensive in the first period and aggressive in the second. The report discusses the implications of these beta values and the limitations of the Capital Asset Pricing Model (CAPM) in accurately capturing risk, especially the presence of unsystematic risk. The findings highlight the importance of considering multi-factor models for a more precise estimation of expected stock returns, due to the shortcomings of CAPM assumptions. The report concludes with references to support the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.