ACC303 - Armour Energy Limited: Conceptual Framework Compliance Report

VerifiedAdded on 2023/05/31

|20

|2819

|114

Report

AI Summary

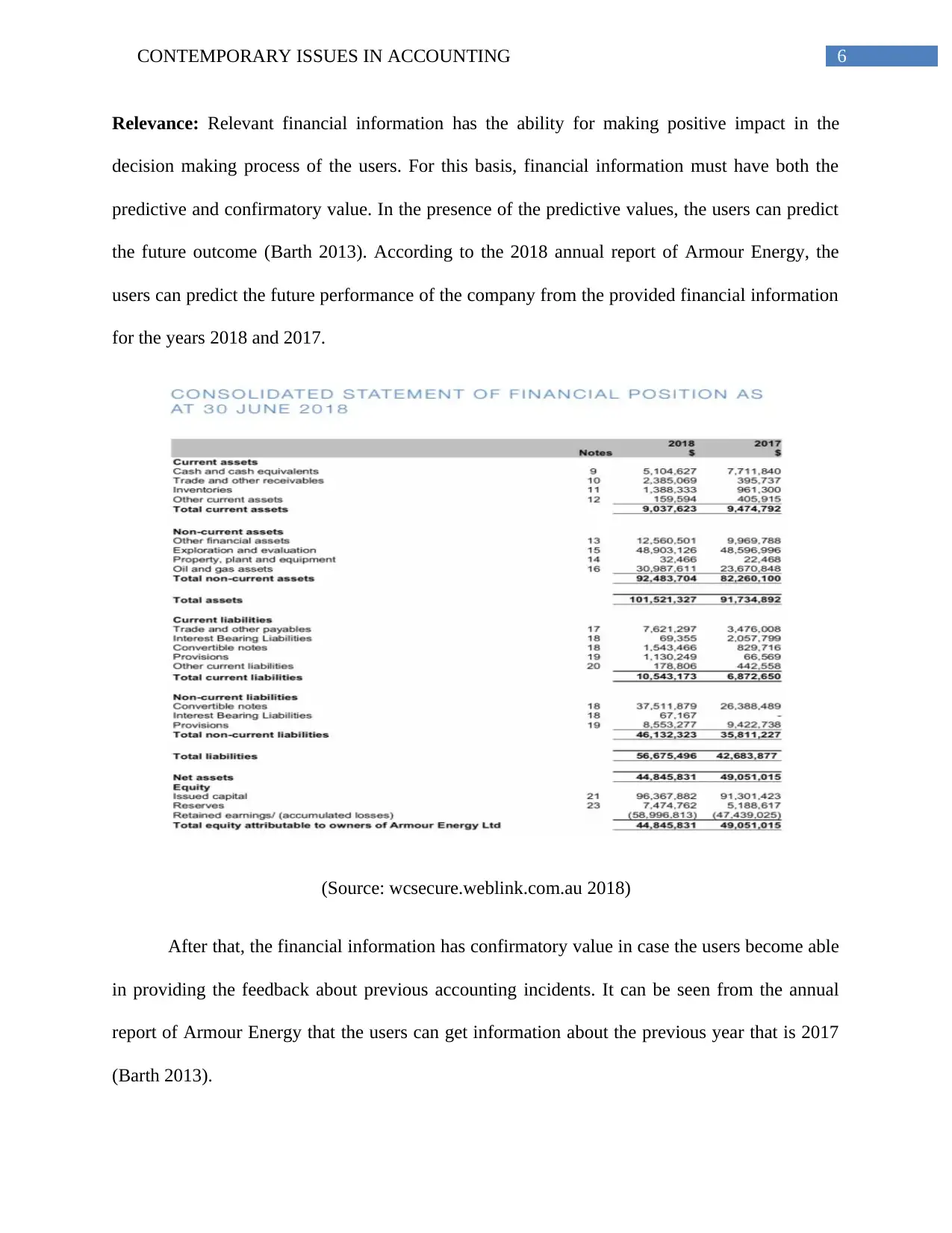

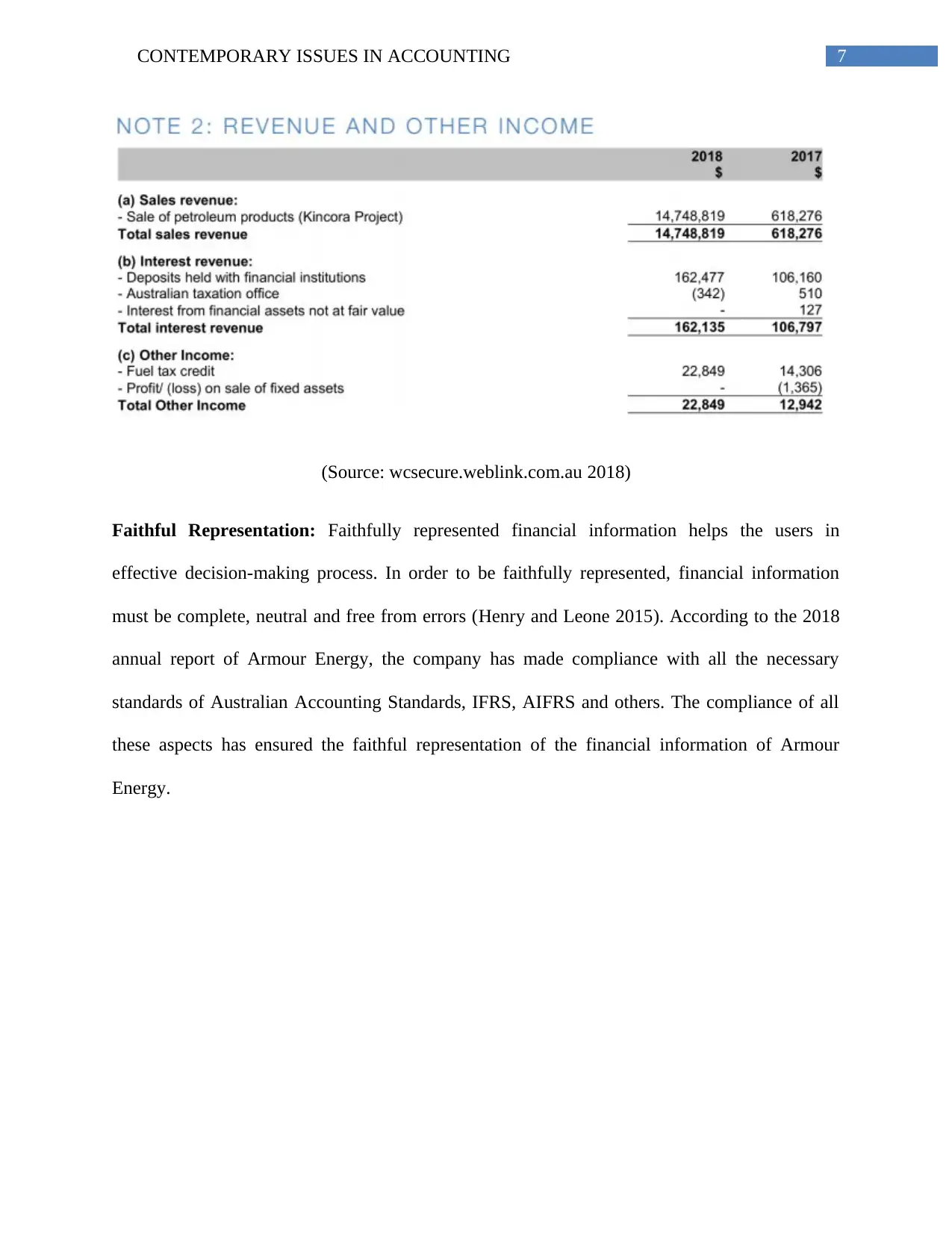

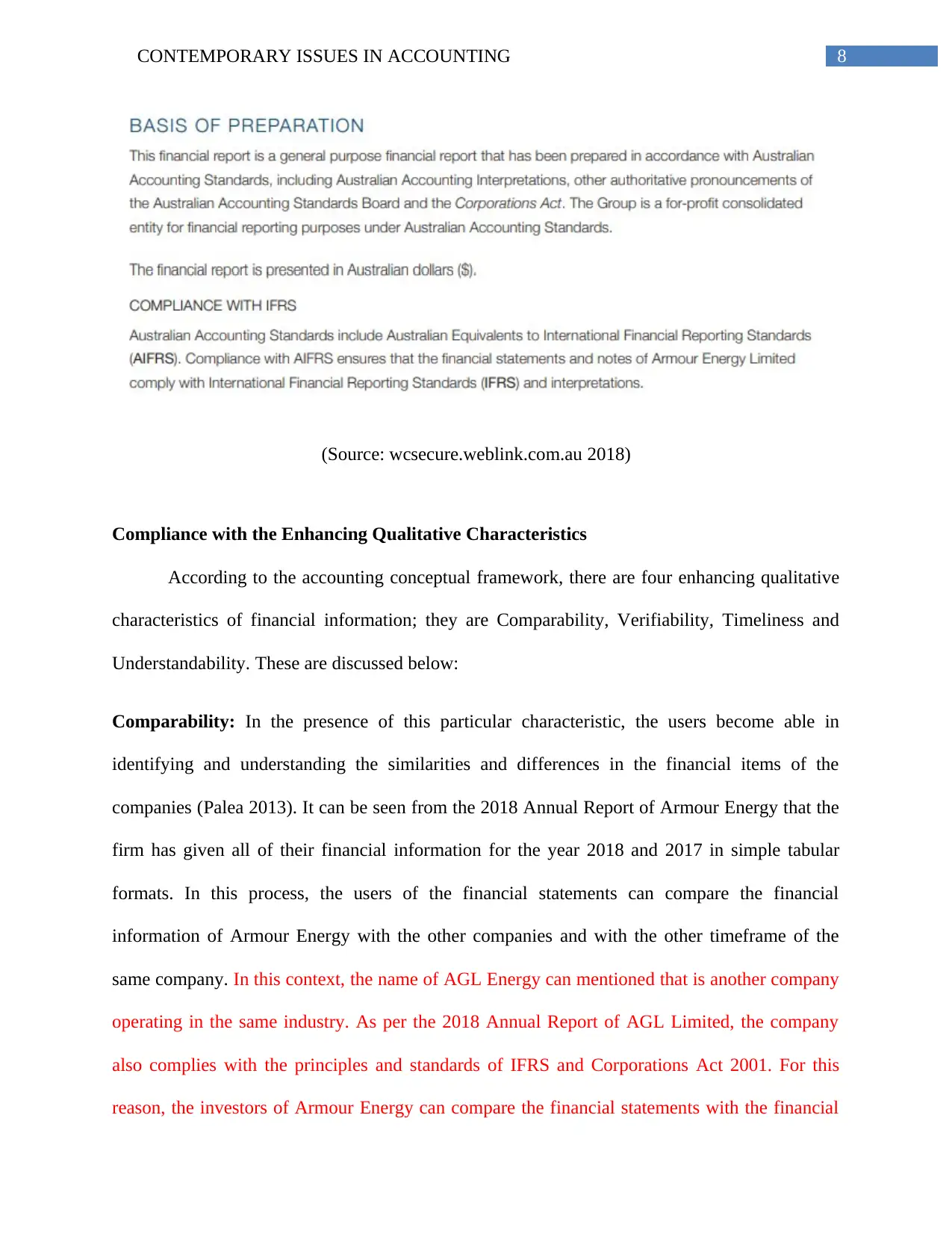

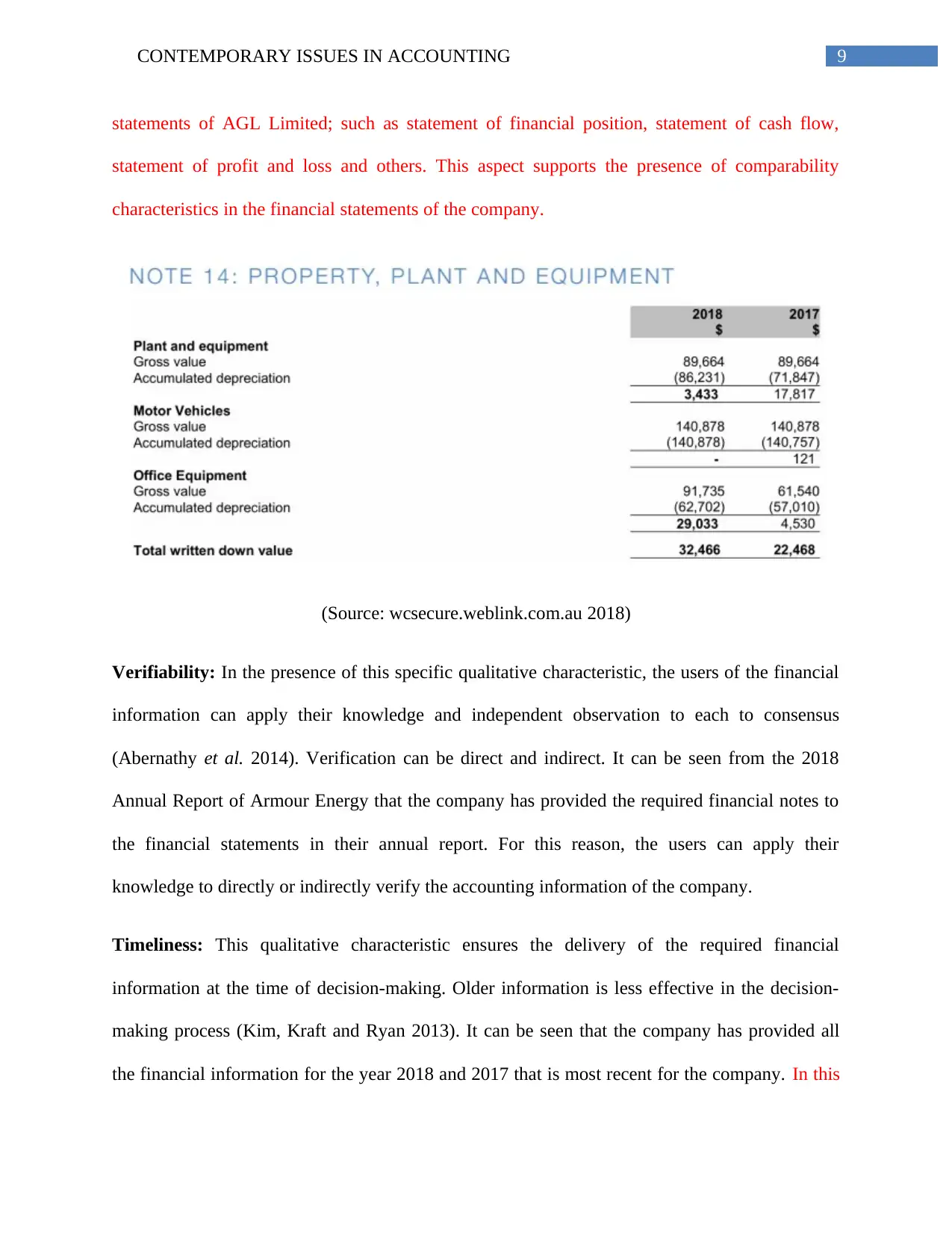

This report provides a comprehensive analysis of Armour Energy's compliance with the conceptual framework, focusing on measurement requirements and qualitative characteristics. It evaluates the company's adherence to historical cost and fair value measurements, as well as its compliance with fundamental qualities like relevance and faithful representation, and enhancing qualities such as comparability, verifiability, timeliness, and understandability. The report further assesses the credibility of Armour Energy's financial statements for decision-making purposes, examining whether the statements provide adequate information about the company's financial position, changes in economic resources, and cash flow. Finally, the report considers whether users need more than basic accounting knowledge to analyze the company's financial statements, concluding that the company presents information in a clear and understandable format while adhering to relevant accounting standards and principles.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.