Auditing Standard ASA 315: Governance Issues in Commonwealth Bank

VerifiedAdded on 2023/06/08

|14

|3065

|82

Report

AI Summary

This report provides an analysis of auditing governance, focusing on ASA 315 and the governance issues within the Commonwealth Bank. It discusses the auditor's responsibility in reviewing client governance, key governance issues identified by ASIC, and recommendations for improvement. The report covers topics such as ineffective board oversight, risk management frameworks, and ethical decision-making using the American Accounting Association model. Additionally, it addresses the impact of statutory caps on auditor liability. This document is available on Desklib, a platform providing students with a range of study tools and solved assignments.

Running head: AUDITING

Auditing

Name of the Student

Name of the University

Author’s Note

Auditing

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................7

Answer to Question 3......................................................................................................................9

References......................................................................................................................................11

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2......................................................................................................................7

Answer to Question 3......................................................................................................................9

References......................................................................................................................................11

2AUDITING

Answer to Question 1

Executive Summary

The analysis of different sections of ASA 15 states that the auditors are needed to gain

understanding as well as information about some of the major factors of the audit client like

industry nature, governance mechanism, internal control, processes to implement accounting

policies and others. The analysis of Commonwealth Bank issues states that the main governance

issues in the bank are ineffective oversight of the board, lack of urgency in resolving issues,

ineffective risk management framework and others. As a recommendation, the bank is needed to

establish effective governance mechanism along with effective risk management framework.

Answer to Question 1

Executive Summary

The analysis of different sections of ASA 15 states that the auditors are needed to gain

understanding as well as information about some of the major factors of the audit client like

industry nature, governance mechanism, internal control, processes to implement accounting

policies and others. The analysis of Commonwealth Bank issues states that the main governance

issues in the bank are ineffective oversight of the board, lack of urgency in resolving issues,

ineffective risk management framework and others. As a recommendation, the bank is needed to

establish effective governance mechanism along with effective risk management framework.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

Introduction

At the time to conduct the audit operations, the auditors are needed to take into

consideration all the relevant factors and one of them is the governance mechanism in client. In

Australia, the presence of ASA 315 can be seen that contains all the standards and principles for

the auditors to consider the governance of the audit clients. The main aim of this report is the

analysis of the responsibility of the auditors to review the governance of the audit client by

considering ASA 15. The next part of the report includes the analysis of the key governance

issues in Commonwealth Bank along with ASIC recommendation.

Discussion

At the time of the auditing process, the auditors should take into account the governance

mechanism of the clients. For this purpose, they are needed to follow the principles of Auditing

Standard ASA 315 Understanding the Entity and Its Environment and Assessing the Risks of

Material Misstatement as it provides the auditors with the required steps to review the

governance mechanism of the clients (apesb.org.au, 2018). This section is considered as a major

aspect for the auditors as they are needed to follow these guidelines while conducting the audit

operations. The main parts of this regulation are discussed below:

According to the standards of ASA 315, the auditors are responsible for gaining

understanding about some of the major factors of the clients like industry nature, major

regulatory bodies and other external factors such as financial reporting framework and others. In

addition, the auditors should gain information some other aspects like business operations of the

client, ownership structure, investment types and the available financial resources of the clients.

Most important, the auditors need to gain such information that helps them in understanding

Introduction

At the time to conduct the audit operations, the auditors are needed to take into

consideration all the relevant factors and one of them is the governance mechanism in client. In

Australia, the presence of ASA 315 can be seen that contains all the standards and principles for

the auditors to consider the governance of the audit clients. The main aim of this report is the

analysis of the responsibility of the auditors to review the governance of the audit client by

considering ASA 15. The next part of the report includes the analysis of the key governance

issues in Commonwealth Bank along with ASIC recommendation.

Discussion

At the time of the auditing process, the auditors should take into account the governance

mechanism of the clients. For this purpose, they are needed to follow the principles of Auditing

Standard ASA 315 Understanding the Entity and Its Environment and Assessing the Risks of

Material Misstatement as it provides the auditors with the required steps to review the

governance mechanism of the clients (apesb.org.au, 2018). This section is considered as a major

aspect for the auditors as they are needed to follow these guidelines while conducting the audit

operations. The main parts of this regulation are discussed below:

According to the standards of ASA 315, the auditors are responsible for gaining

understanding about some of the major factors of the clients like industry nature, major

regulatory bodies and other external factors such as financial reporting framework and others. In

addition, the auditors should gain information some other aspects like business operations of the

client, ownership structure, investment types and the available financial resources of the clients.

Most important, the auditors need to gain such information that helps them in understanding

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

about the client’s processes to select and apply accounting policies along with their

appropriateness with the client’s business operations (Xu et al., 2013). All these aspects are

required for the auditors for the preliminary stage of the audit operations in order to obtain

information about the major activities of the audit clients.

This particular standard of ASA 315 puts the obligation on the auditors to understand the

implementation process of internal control of the audit client so that they become able in making

judgment on the appropriateness of this control with the business risks. While gaining

understanding about the internal control of the audit clients, they should also consider the

internal control design process. On the overall basis, it can be said that ASA 315 makes the

auditors obliged in gaining all the information about all the dimensions of the internal control of

the audit clients (Rahman, 2013). In this process, it is needed for the auditors to take into account

the evaluation process of the staffs that are responsible for the implementation of effective

governance. Information about all these factors helps the auditors to understand the fact that

whether the culture of honesty as well as ethical behavior is present in the client’s business.

According to the standards of ASA 315, in the process of the review of the client’s

internal governance, it is responsible for the auditors to obtain understanding about the fact that

whether the employed governance procedures are appropriate for identifying the financial

reporting related risks of the companies (Sanderson, 2014). In this process, the main roles of the

auditors can be found in the process of risk estimation and the process of risk assessment as the

results of these assessments and identification is needed for the formulation of apposite auditing

strategies. Apart from all these, ASA 315 also puts the obligation on the auditors for obtaining

information about the internal information system within the organizations along with its role

towards the process of financial reporting of the audit clients. On the overall basis, ASA 315 puts

about the client’s processes to select and apply accounting policies along with their

appropriateness with the client’s business operations (Xu et al., 2013). All these aspects are

required for the auditors for the preliminary stage of the audit operations in order to obtain

information about the major activities of the audit clients.

This particular standard of ASA 315 puts the obligation on the auditors to understand the

implementation process of internal control of the audit client so that they become able in making

judgment on the appropriateness of this control with the business risks. While gaining

understanding about the internal control of the audit clients, they should also consider the

internal control design process. On the overall basis, it can be said that ASA 315 makes the

auditors obliged in gaining all the information about all the dimensions of the internal control of

the audit clients (Rahman, 2013). In this process, it is needed for the auditors to take into account

the evaluation process of the staffs that are responsible for the implementation of effective

governance. Information about all these factors helps the auditors to understand the fact that

whether the culture of honesty as well as ethical behavior is present in the client’s business.

According to the standards of ASA 315, in the process of the review of the client’s

internal governance, it is responsible for the auditors to obtain understanding about the fact that

whether the employed governance procedures are appropriate for identifying the financial

reporting related risks of the companies (Sanderson, 2014). In this process, the main roles of the

auditors can be found in the process of risk estimation and the process of risk assessment as the

results of these assessments and identification is needed for the formulation of apposite auditing

strategies. Apart from all these, ASA 315 also puts the obligation on the auditors for obtaining

information about the internal information system within the organizations along with its role

towards the process of financial reporting of the audit clients. On the overall basis, ASA 315 puts

5AUDITING

the obligation on the auditors for reviewing all aspects of governance and internal control of the

audit clients (Margret & Hoque, 2016).

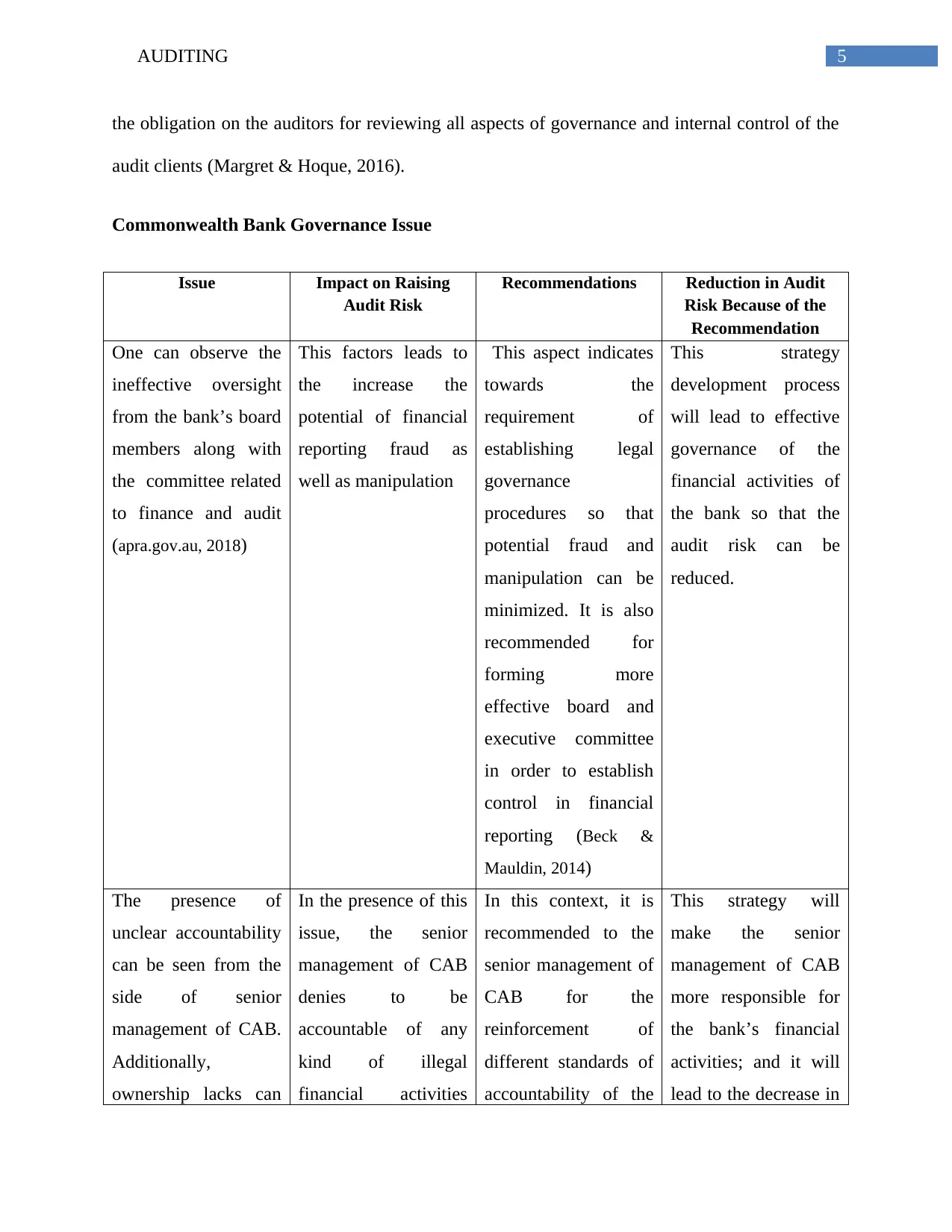

Commonwealth Bank Governance Issue

Issue Impact on Raising

Audit Risk

Recommendations Reduction in Audit

Risk Because of the

Recommendation

One can observe the

ineffective oversight

from the bank’s board

members along with

the committee related

to finance and audit

(apra.gov.au, 2018)

This factors leads to

the increase the

potential of financial

reporting fraud as

well as manipulation

This aspect indicates

towards the

requirement of

establishing legal

governance

procedures so that

potential fraud and

manipulation can be

minimized. It is also

recommended for

forming more

effective board and

executive committee

in order to establish

control in financial

reporting (Beck &

Mauldin, 2014)

This strategy

development process

will lead to effective

governance of the

financial activities of

the bank so that the

audit risk can be

reduced.

The presence of

unclear accountability

can be seen from the

side of senior

management of CAB.

Additionally,

ownership lacks can

In the presence of this

issue, the senior

management of CAB

denies to be

accountable of any

kind of illegal

financial activities

In this context, it is

recommended to the

senior management of

CAB for the

reinforcement of

different standards of

accountability of the

This strategy will

make the senior

management of CAB

more responsible for

the bank’s financial

activities; and it will

lead to the decrease in

the obligation on the auditors for reviewing all aspects of governance and internal control of the

audit clients (Margret & Hoque, 2016).

Commonwealth Bank Governance Issue

Issue Impact on Raising

Audit Risk

Recommendations Reduction in Audit

Risk Because of the

Recommendation

One can observe the

ineffective oversight

from the bank’s board

members along with

the committee related

to finance and audit

(apra.gov.au, 2018)

This factors leads to

the increase the

potential of financial

reporting fraud as

well as manipulation

This aspect indicates

towards the

requirement of

establishing legal

governance

procedures so that

potential fraud and

manipulation can be

minimized. It is also

recommended for

forming more

effective board and

executive committee

in order to establish

control in financial

reporting (Beck &

Mauldin, 2014)

This strategy

development process

will lead to effective

governance of the

financial activities of

the bank so that the

audit risk can be

reduced.

The presence of

unclear accountability

can be seen from the

side of senior

management of CAB.

Additionally,

ownership lacks can

In the presence of this

issue, the senior

management of CAB

denies to be

accountable of any

kind of illegal

financial activities

In this context, it is

recommended to the

senior management of

CAB for the

reinforcement of

different standards of

accountability of the

This strategy will

make the senior

management of CAB

more responsible for

the bank’s financial

activities; and it will

lead to the decrease in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

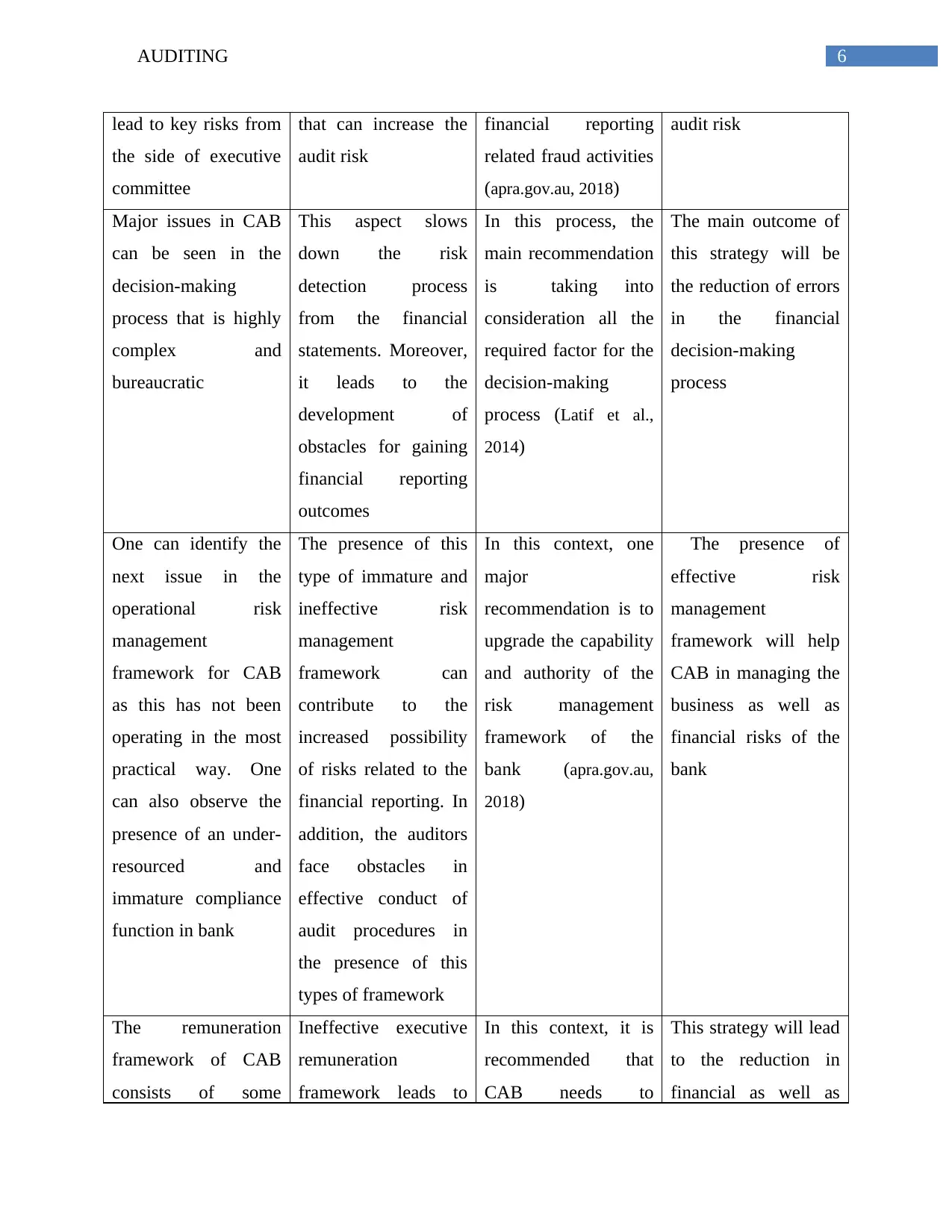

6AUDITING

lead to key risks from

the side of executive

committee

that can increase the

audit risk

financial reporting

related fraud activities

(apra.gov.au, 2018)

audit risk

Major issues in CAB

can be seen in the

decision-making

process that is highly

complex and

bureaucratic

This aspect slows

down the risk

detection process

from the financial

statements. Moreover,

it leads to the

development of

obstacles for gaining

financial reporting

outcomes

In this process, the

main recommendation

is taking into

consideration all the

required factor for the

decision-making

process (Latif et al.,

2014)

The main outcome of

this strategy will be

the reduction of errors

in the financial

decision-making

process

One can identify the

next issue in the

operational risk

management

framework for CAB

as this has not been

operating in the most

practical way. One

can also observe the

presence of an under-

resourced and

immature compliance

function in bank

The presence of this

type of immature and

ineffective risk

management

framework can

contribute to the

increased possibility

of risks related to the

financial reporting. In

addition, the auditors

face obstacles in

effective conduct of

audit procedures in

the presence of this

types of framework

In this context, one

major

recommendation is to

upgrade the capability

and authority of the

risk management

framework of the

bank (apra.gov.au,

2018)

The presence of

effective risk

management

framework will help

CAB in managing the

business as well as

financial risks of the

bank

The remuneration

framework of CAB

consists of some

Ineffective executive

remuneration

framework leads to

In this context, it is

recommended that

CAB needs to

This strategy will lead

to the reduction in

financial as well as

lead to key risks from

the side of executive

committee

that can increase the

audit risk

financial reporting

related fraud activities

(apra.gov.au, 2018)

audit risk

Major issues in CAB

can be seen in the

decision-making

process that is highly

complex and

bureaucratic

This aspect slows

down the risk

detection process

from the financial

statements. Moreover,

it leads to the

development of

obstacles for gaining

financial reporting

outcomes

In this process, the

main recommendation

is taking into

consideration all the

required factor for the

decision-making

process (Latif et al.,

2014)

The main outcome of

this strategy will be

the reduction of errors

in the financial

decision-making

process

One can identify the

next issue in the

operational risk

management

framework for CAB

as this has not been

operating in the most

practical way. One

can also observe the

presence of an under-

resourced and

immature compliance

function in bank

The presence of this

type of immature and

ineffective risk

management

framework can

contribute to the

increased possibility

of risks related to the

financial reporting. In

addition, the auditors

face obstacles in

effective conduct of

audit procedures in

the presence of this

types of framework

In this context, one

major

recommendation is to

upgrade the capability

and authority of the

risk management

framework of the

bank (apra.gov.au,

2018)

The presence of

effective risk

management

framework will help

CAB in managing the

business as well as

financial risks of the

bank

The remuneration

framework of CAB

consists of some

Ineffective executive

remuneration

framework leads to

In this context, it is

recommended that

CAB needs to

This strategy will lead

to the reduction in

financial as well as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

major issues that has

made the

remuneration

framework ineffective

the development of

audit as well as

financial risks in the

process of financial

reporting

consider the

implementation of an

effective executive

remuneration

framework that will

comply with all the

required regulations

and policies (Guénin-

Paracini, Malsch &

Paillé, 2014)

audit risks

major issues that has

made the

remuneration

framework ineffective

the development of

audit as well as

financial risks in the

process of financial

reporting

consider the

implementation of an

effective executive

remuneration

framework that will

comply with all the

required regulations

and policies (Guénin-

Paracini, Malsch &

Paillé, 2014)

audit risks

8AUDITING

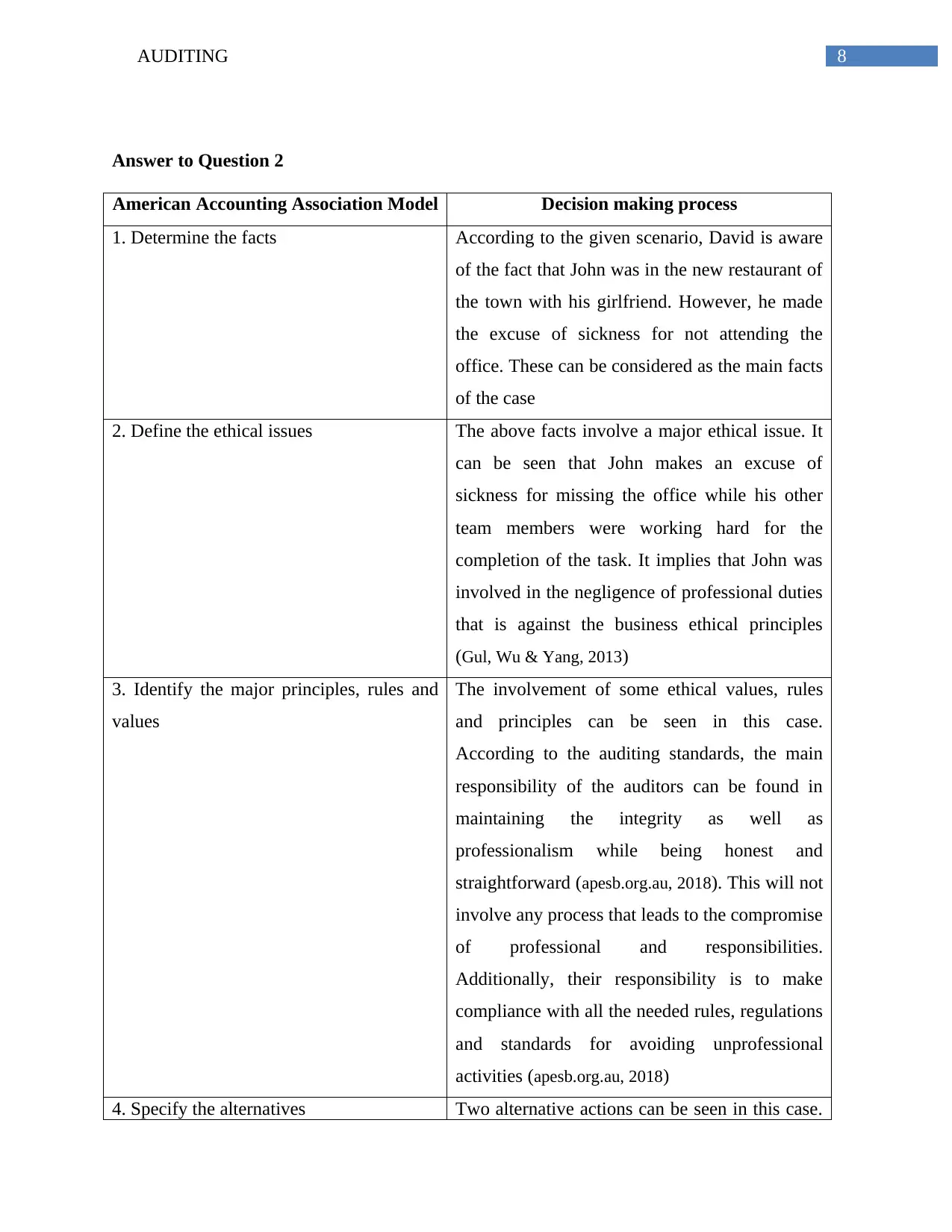

Answer to Question 2

American Accounting Association Model Decision making process

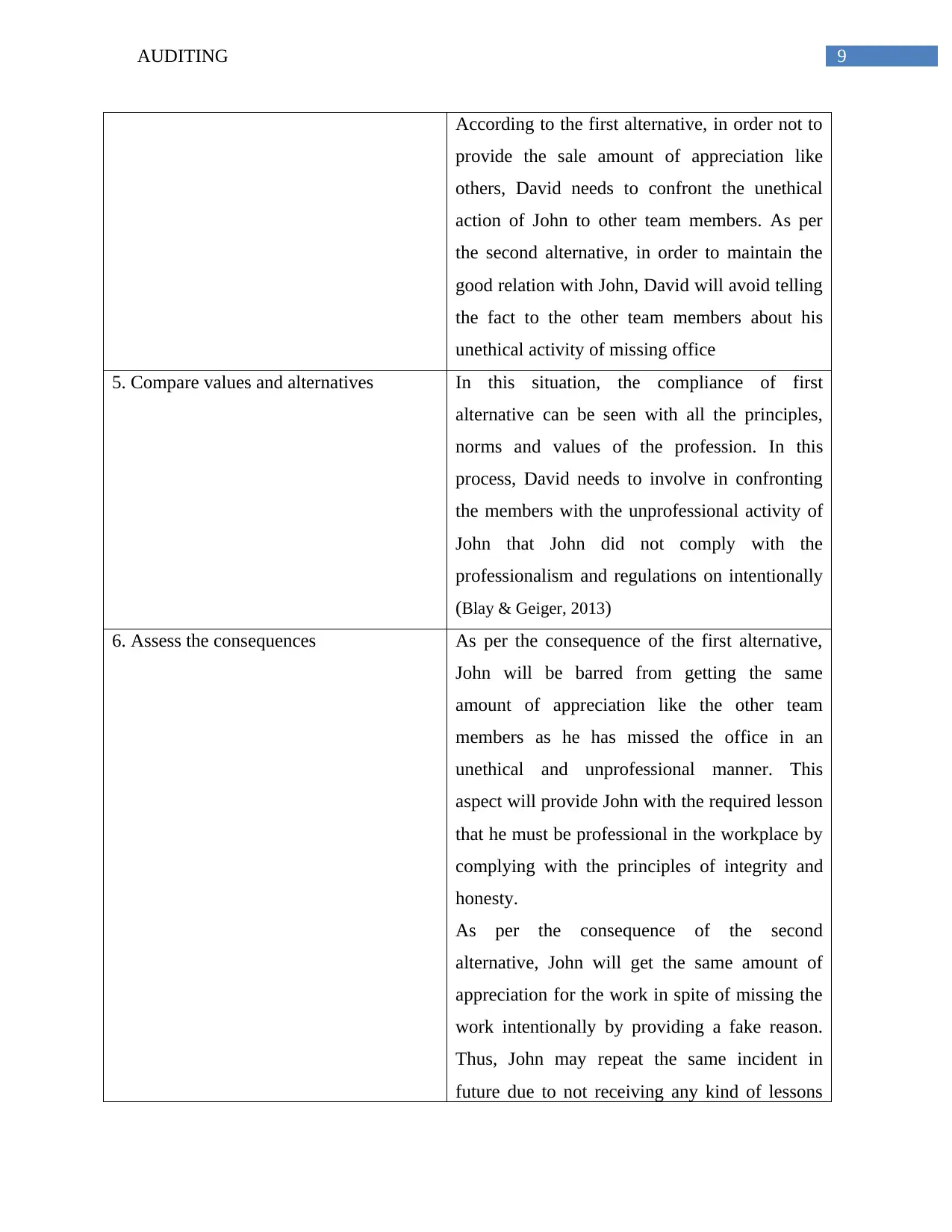

1. Determine the facts According to the given scenario, David is aware

of the fact that John was in the new restaurant of

the town with his girlfriend. However, he made

the excuse of sickness for not attending the

office. These can be considered as the main facts

of the case

2. Define the ethical issues The above facts involve a major ethical issue. It

can be seen that John makes an excuse of

sickness for missing the office while his other

team members were working hard for the

completion of the task. It implies that John was

involved in the negligence of professional duties

that is against the business ethical principles

(Gul, Wu & Yang, 2013)

3. Identify the major principles, rules and

values

The involvement of some ethical values, rules

and principles can be seen in this case.

According to the auditing standards, the main

responsibility of the auditors can be found in

maintaining the integrity as well as

professionalism while being honest and

straightforward (apesb.org.au, 2018). This will not

involve any process that leads to the compromise

of professional and responsibilities.

Additionally, their responsibility is to make

compliance with all the needed rules, regulations

and standards for avoiding unprofessional

activities (apesb.org.au, 2018)

4. Specify the alternatives Two alternative actions can be seen in this case.

Answer to Question 2

American Accounting Association Model Decision making process

1. Determine the facts According to the given scenario, David is aware

of the fact that John was in the new restaurant of

the town with his girlfriend. However, he made

the excuse of sickness for not attending the

office. These can be considered as the main facts

of the case

2. Define the ethical issues The above facts involve a major ethical issue. It

can be seen that John makes an excuse of

sickness for missing the office while his other

team members were working hard for the

completion of the task. It implies that John was

involved in the negligence of professional duties

that is against the business ethical principles

(Gul, Wu & Yang, 2013)

3. Identify the major principles, rules and

values

The involvement of some ethical values, rules

and principles can be seen in this case.

According to the auditing standards, the main

responsibility of the auditors can be found in

maintaining the integrity as well as

professionalism while being honest and

straightforward (apesb.org.au, 2018). This will not

involve any process that leads to the compromise

of professional and responsibilities.

Additionally, their responsibility is to make

compliance with all the needed rules, regulations

and standards for avoiding unprofessional

activities (apesb.org.au, 2018)

4. Specify the alternatives Two alternative actions can be seen in this case.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

According to the first alternative, in order not to

provide the sale amount of appreciation like

others, David needs to confront the unethical

action of John to other team members. As per

the second alternative, in order to maintain the

good relation with John, David will avoid telling

the fact to the other team members about his

unethical activity of missing office

5. Compare values and alternatives In this situation, the compliance of first

alternative can be seen with all the principles,

norms and values of the profession. In this

process, David needs to involve in confronting

the members with the unprofessional activity of

John that John did not comply with the

professionalism and regulations on intentionally

(Blay & Geiger, 2013)

6. Assess the consequences As per the consequence of the first alternative,

John will be barred from getting the same

amount of appreciation like the other team

members as he has missed the office in an

unethical and unprofessional manner. This

aspect will provide John with the required lesson

that he must be professional in the workplace by

complying with the principles of integrity and

honesty.

As per the consequence of the second

alternative, John will get the same amount of

appreciation for the work in spite of missing the

work intentionally by providing a fake reason.

Thus, John may repeat the same incident in

future due to not receiving any kind of lessons

According to the first alternative, in order not to

provide the sale amount of appreciation like

others, David needs to confront the unethical

action of John to other team members. As per

the second alternative, in order to maintain the

good relation with John, David will avoid telling

the fact to the other team members about his

unethical activity of missing office

5. Compare values and alternatives In this situation, the compliance of first

alternative can be seen with all the principles,

norms and values of the profession. In this

process, David needs to involve in confronting

the members with the unprofessional activity of

John that John did not comply with the

professionalism and regulations on intentionally

(Blay & Geiger, 2013)

6. Assess the consequences As per the consequence of the first alternative,

John will be barred from getting the same

amount of appreciation like the other team

members as he has missed the office in an

unethical and unprofessional manner. This

aspect will provide John with the required lesson

that he must be professional in the workplace by

complying with the principles of integrity and

honesty.

As per the consequence of the second

alternative, John will get the same amount of

appreciation for the work in spite of missing the

work intentionally by providing a fake reason.

Thus, John may repeat the same incident in

future due to not receiving any kind of lessons

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

(Pizzini, Lin & Ziegenfuss, 2014)

7. Make your decision Based on the above discussion, the appropriate

ethical decision will be the adoption of the first

alternative that is related to confront the

unethical action of John to the other team

members of the group

Answer to Question 3

It needs to be mentioned that the incorporation of the statutory cap of the auditors has

major impact on the process to limit the liability of the auditors. According to this statutory cap,

there are some alternative liability arrangements for the auditors. According to the first

agreement, at the time of the filing of claim by an injured party against specific tortfeasors, they

are given with the authority to collect all the damages from the remaining tortfeasors

(Samsonova-Taddei & Humphrey, 2015). As per this particular arrangement, it is the authority

for the injured parties in claiming all the damages from the auditors when there is presence of

misinterpretation in the company financial statements. However, the injured parties will be able

to avail this option in case of the presence of responsibility related to damages by the additional

tortfeasors. This arrangement puts the obligation on the auditors in providing full compensation

or a greater share of the compensation as per his/her level of fault. Hence, the injured party has

not right to increase the amount of the compensation. However, as per this regulation, it is not

the obligation on the auditors for the payment of compensation that is not appropriate with the

auditors’ level of fault (Philipsen, 2014). The applicability of this arrangement can be seen when

the remaining tortfeasors are unable to pay their part of damage. According to these regulations,

the injured party bears the greatest proportion of risk as compared to the auditors and the

(Pizzini, Lin & Ziegenfuss, 2014)

7. Make your decision Based on the above discussion, the appropriate

ethical decision will be the adoption of the first

alternative that is related to confront the

unethical action of John to the other team

members of the group

Answer to Question 3

It needs to be mentioned that the incorporation of the statutory cap of the auditors has

major impact on the process to limit the liability of the auditors. According to this statutory cap,

there are some alternative liability arrangements for the auditors. According to the first

agreement, at the time of the filing of claim by an injured party against specific tortfeasors, they

are given with the authority to collect all the damages from the remaining tortfeasors

(Samsonova-Taddei & Humphrey, 2015). As per this particular arrangement, it is the authority

for the injured parties in claiming all the damages from the auditors when there is presence of

misinterpretation in the company financial statements. However, the injured parties will be able

to avail this option in case of the presence of responsibility related to damages by the additional

tortfeasors. This arrangement puts the obligation on the auditors in providing full compensation

or a greater share of the compensation as per his/her level of fault. Hence, the injured party has

not right to increase the amount of the compensation. However, as per this regulation, it is not

the obligation on the auditors for the payment of compensation that is not appropriate with the

auditors’ level of fault (Philipsen, 2014). The applicability of this arrangement can be seen when

the remaining tortfeasors are unable to pay their part of damage. According to these regulations,

the injured party bears the greatest proportion of risk as compared to the auditors and the

11AUDITING

tortfeasors. Thus, the whole discussion indicates towards the reduced amount of liability for the

auditors.

The third arrangement involves in the establishment of a compensation cap. According to

this arrangement, the presence of a maximum amount of cap can be seen for the amount of

compensation. As per the regulation of this arrangement, when the auditors’ share in the

compensation equals or exceeds the equivalent cap, one does not have the authority in charging

more compensation that the set cap to the auditors (Eyal, 2013). The applicability of this rule can

also be seen at the time of the inability of other tortfeasors to pay their part of compensation. For

this reason, the authority lies with the injured party to collect the compensation when it does not

cross the previously set cap. Thus, it can be seen from the above discussion that the specific

arrangements under cap system play an integral part in order to reduce the auditors’ liability at

the time to conduct the audit operations.

tortfeasors. Thus, the whole discussion indicates towards the reduced amount of liability for the

auditors.

The third arrangement involves in the establishment of a compensation cap. According to

this arrangement, the presence of a maximum amount of cap can be seen for the amount of

compensation. As per the regulation of this arrangement, when the auditors’ share in the

compensation equals or exceeds the equivalent cap, one does not have the authority in charging

more compensation that the set cap to the auditors (Eyal, 2013). The applicability of this rule can

also be seen at the time of the inability of other tortfeasors to pay their part of compensation. For

this reason, the authority lies with the injured party to collect the compensation when it does not

cross the previously set cap. Thus, it can be seen from the above discussion that the specific

arrangements under cap system play an integral part in order to reduce the auditors’ liability at

the time to conduct the audit operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.