Analysis of Auditing Standards (ASA 701 & 570) in the Mining Sector

VerifiedAdded on 2022/08/27

|19

|2772

|29

Report

AI Summary

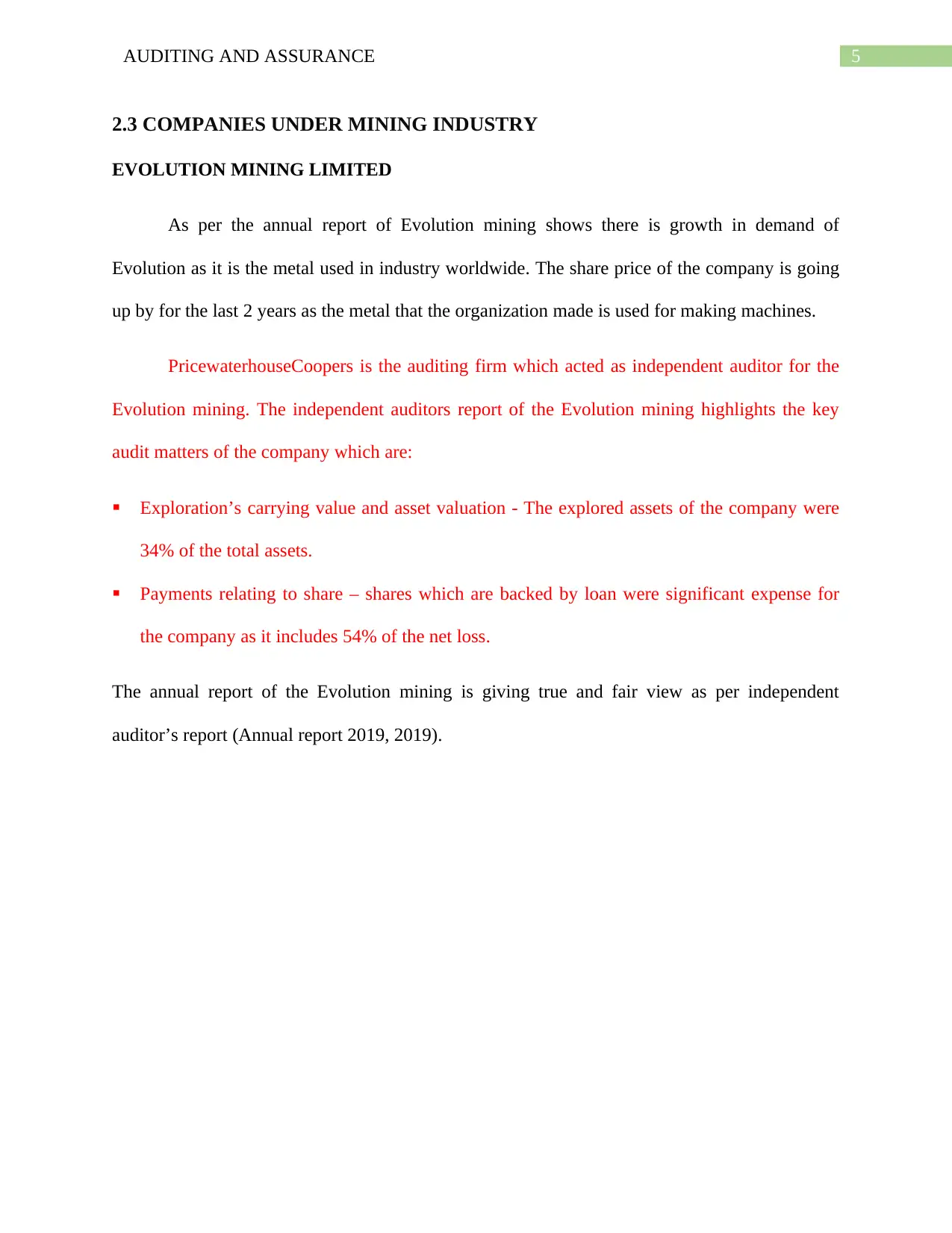

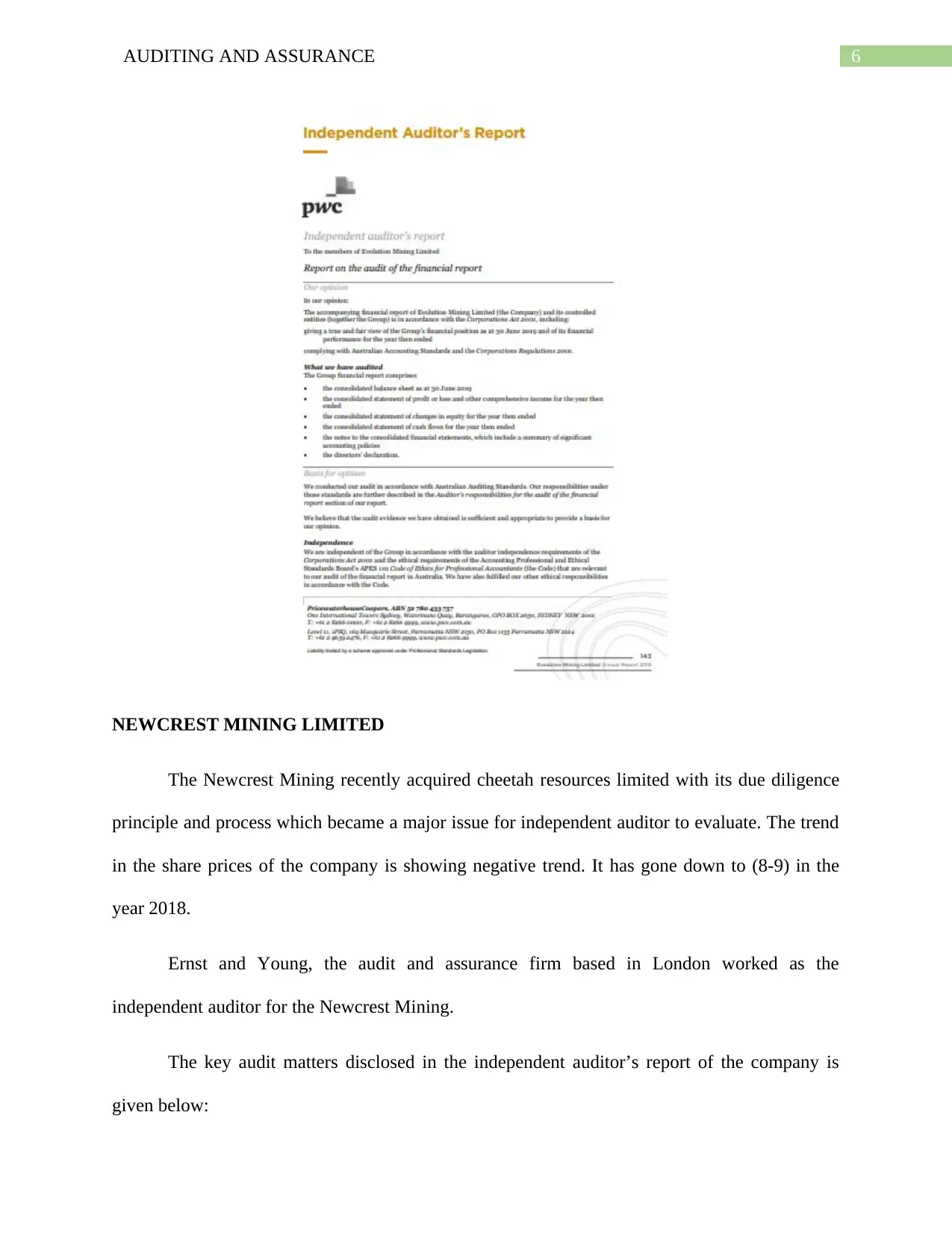

This report provides an in-depth analysis of the Auditing and Assurance Standards Board (AUASB) and its role in revising auditing standards, specifically focusing on ASA 701 and ASA 570. The study evaluates the significance of key audit matters (KAM) and the concept of going concern within independent auditor reports. The report uses examples of four ASX-listed mining companies to illustrate how ASA 701 and ASA 570 have been applied by independent auditors, highlighting the impact of these standards on financial reporting transparency. The analysis includes a comparison of auditing practices before and after the implementation of these revised standards, particularly concerning KAM communication and going concern assessments. The report concludes by emphasizing the importance of a dedicated section for KAM in auditor reports and its significant aspects, contributing to improved financial reporting and transparency.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.