Analyzing the Impact of ASA 701 on Woolworths' Audit Report

VerifiedAdded on 2020/05/16

|13

|2264

|271

Report

AI Summary

This report examines the impact of ASA 701, focusing on the communication of key audit matters in independent auditor's reports, using Woolworths Limited's 2017 annual report as a case study. The report identifies key audit matters such as the exit of the home improvement business, the valuation of property, plant, and equipment for Big W, inventory provisions, rebates, and information technology systems. It analyzes areas of risk, including the Big W segment's performance and the complexity of IT systems, and discusses significant events and transactions affecting the audit, such as the decrease in the value of Big W's assets and the home improvement business exit. The report recommends clear accounting practices and transparency to aid auditors and investors, highlighting the increased transparency provided by ASA 701. The analysis aims to assess the influence of ASA 701 on financial reporting and provide a framework for evaluating companies within an industry.

1

IMPACT OF ASA 701 – COMMUNICATING KEY AUDIT

MATTERS IN THE INDEPENDENT AUDITORS REPORT

Student Name: Student ID:

1/21/2018

IMPACT OF ASA 701 – COMMUNICATING KEY AUDIT

MATTERS IN THE INDEPENDENT AUDITORS REPORT

Student Name: Student ID:

1/21/2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SYNOPSIS

EXECUTIVE SUMMARY

Impact of ASA 701 – Communicating key audit matters in the independent auditors report is title

of the report. The first major aim of the report is to identify whether the auditor of the selected

company has reported the key audit matters in its independent auditors report. The second major

aim of the report is to identify whether the key matters so reported in the independent auditors

report has the risk of material misstatement. The third major aim of the report is to identify any

significant event or transaction that has been taken place during the period of audit and whether

the same have any effect on the audit conducted by the independent auditor. The last major aim

of the report is to state whether these risks and transaction has affected the going concern

assumption of the company. With these aims, the report has been prepared into proper headings

and sub headings.

2

EXECUTIVE SUMMARY

Impact of ASA 701 – Communicating key audit matters in the independent auditors report is title

of the report. The first major aim of the report is to identify whether the auditor of the selected

company has reported the key audit matters in its independent auditors report. The second major

aim of the report is to identify whether the key matters so reported in the independent auditors

report has the risk of material misstatement. The third major aim of the report is to identify any

significant event or transaction that has been taken place during the period of audit and whether

the same have any effect on the audit conducted by the independent auditor. The last major aim

of the report is to state whether these risks and transaction has affected the going concern

assumption of the company. With these aims, the report has been prepared into proper headings

and sub headings.

2

EXECUTIVE SUMMARY................................................................................................................................ 2

INTRODUCTION............................................................................................................................................. 4

DETAILS OF COMPANY........................................................................................................................................ 4

SELECTED COMPANY.....................................................................................................................................................4

NATURE OF BUSINESS................................................................................................................................................... 5

NEW AUDITING STANDARD – 701....................................................................................................................... 5

REASON FOR DEVELOPMENT.......................................................................................................................................... 5

MEANING................................................................................................................................................................... 5

KEY AUDIT MATTERS LISTED................................................................................................................................ 6

EXIT OF HOME IMPROVEMENT........................................................................................................................................6

VALUE OF PROPERTY PLANT AND EQUIPMENT – BIG W......................................................................................................6

PROVISION OF INVENTORY.............................................................................................................................................6

REBATES.....................................................................................................................................................................7

INFORMATION TECHNOLOGY SYSTEMS..............................................................................................................................8

AREAS OF RISK.................................................................................................................................................... 9

SIGNIFICANT EVENT OR TRANSACTIONS AND ITS EFFECT ON AUDIT...................................................................10

RECOMMENDATION AND CONCLUSION............................................................................................................ 12

REFERENCES...................................................................................................................................................... 12

3

INTRODUCTION............................................................................................................................................. 4

DETAILS OF COMPANY........................................................................................................................................ 4

SELECTED COMPANY.....................................................................................................................................................4

NATURE OF BUSINESS................................................................................................................................................... 5

NEW AUDITING STANDARD – 701....................................................................................................................... 5

REASON FOR DEVELOPMENT.......................................................................................................................................... 5

MEANING................................................................................................................................................................... 5

KEY AUDIT MATTERS LISTED................................................................................................................................ 6

EXIT OF HOME IMPROVEMENT........................................................................................................................................6

VALUE OF PROPERTY PLANT AND EQUIPMENT – BIG W......................................................................................................6

PROVISION OF INVENTORY.............................................................................................................................................6

REBATES.....................................................................................................................................................................7

INFORMATION TECHNOLOGY SYSTEMS..............................................................................................................................8

AREAS OF RISK.................................................................................................................................................... 9

SIGNIFICANT EVENT OR TRANSACTIONS AND ITS EFFECT ON AUDIT...................................................................10

RECOMMENDATION AND CONCLUSION............................................................................................................ 12

REFERENCES...................................................................................................................................................... 12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The audit plays a very crucial role in depicting the financial health and position of any company

across the World. If there has been no provision for audit in statutes then the financial condition

of any company can never be depicted and the regulating authorities will not be able to track the

record of the company. In this report, the annual report of the company shall be analysed and

interpreted. The company selected for the purpose of the report is Woolworths Limited, being a

company listed in the Australian Stock Exchange. The annual report of the company for the year

ending 25th of June 2017 has been considered and has been analysed.

At first the detail of the company has been discussed then the importance of the new auditing

standard 701 has been discussed. After that, an independent auditors report has been analysed

with respect to the key audit matters reported therein as envisaged by the new auditing standard

number 701. Along with the key audit matters, the significant event and transaction if any

occurred during the period of audit has been discussed and detailed with regard to their likely

effect and impact on the audit of the company. Simultaneously matters have been discussed,

which are of risk and involves significant auditor and management judgment. At the last, the

summary has been given along with the recommendations on the basis of the results obtained.

, .

DETAILS OF COMPANY

Selected Company

The company that has been selected for the purpose of the report is M/s Woolworths Limited.

The company is listed in Australian Stock Exchange and is top 100 listed Corporation. Looking

back into the history of the company, the company has started its operations in the year of

nineteen hundred and twenty four.

4

The audit plays a very crucial role in depicting the financial health and position of any company

across the World. If there has been no provision for audit in statutes then the financial condition

of any company can never be depicted and the regulating authorities will not be able to track the

record of the company. In this report, the annual report of the company shall be analysed and

interpreted. The company selected for the purpose of the report is Woolworths Limited, being a

company listed in the Australian Stock Exchange. The annual report of the company for the year

ending 25th of June 2017 has been considered and has been analysed.

At first the detail of the company has been discussed then the importance of the new auditing

standard 701 has been discussed. After that, an independent auditors report has been analysed

with respect to the key audit matters reported therein as envisaged by the new auditing standard

number 701. Along with the key audit matters, the significant event and transaction if any

occurred during the period of audit has been discussed and detailed with regard to their likely

effect and impact on the audit of the company. Simultaneously matters have been discussed,

which are of risk and involves significant auditor and management judgment. At the last, the

summary has been given along with the recommendations on the basis of the results obtained.

, .

DETAILS OF COMPANY

Selected Company

The company that has been selected for the purpose of the report is M/s Woolworths Limited.

The company is listed in Australian Stock Exchange and is top 100 listed Corporation. Looking

back into the history of the company, the company has started its operations in the year of

nineteen hundred and twenty four.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nature of Business

The company is into the retail sector since its inception and has been regarded as the second

largest company in retail sector having the higher revenues. The company is into the retail chains

of departmental stores in Australia and New Zealand and deals in all type of products whether it

is fruit or vegetables or home décor or hotels. As per the annual report of the company for the

year ending 25th of June 2017, the company has its focus on major five important things –

customers, performance in food, generating revenue from drinks area, the hotel business shall

have more revenue and lastly becoming a best retailer by improving the processes and systems

installed in the company (Woolworths Limited official website, 2017)

NEW AUDITING STANDARD – 701

Reason for Development

The anew auditing standard 701 deals with the communication of the key audit matters in the

independent auditors report. The development of the standard has been invoked by the global

financial crisis which has been happened because of the major accounting flaws and

discrepancies that has been made by the management of the some companies. Like Lehman

Brothers, HIH Insurance, ABC Learning and One Tel. These companies are the example and the

reason of bringing the global financial crisis and have alarmed the regulating authorities by the

different class action suits so as to avoid the manipulative practices that have been adopted by

the aforementioned companies (Bajada and Trayler, 2010; Cordos and Fülöpa, 2015).

Meaning

As auditor plays fiduciary role in communicating the financial health and position of the

company to their stakeholders and the shareholders, it is the duty of the auditor to fairly disclose

and describe the true and fair view. Thus, in order to give more value to the auditor report, the

new standard has provided more transparency (AASB, 2015 and Thomson, 2008). The key audit

matters deals with the additional information which will have the valuable impact on the decision

of the investor. It will include those matters which in the view of the auditor’s professional

judgment are of significant importance in the audit of financial statements and thus required

5

The company is into the retail sector since its inception and has been regarded as the second

largest company in retail sector having the higher revenues. The company is into the retail chains

of departmental stores in Australia and New Zealand and deals in all type of products whether it

is fruit or vegetables or home décor or hotels. As per the annual report of the company for the

year ending 25th of June 2017, the company has its focus on major five important things –

customers, performance in food, generating revenue from drinks area, the hotel business shall

have more revenue and lastly becoming a best retailer by improving the processes and systems

installed in the company (Woolworths Limited official website, 2017)

NEW AUDITING STANDARD – 701

Reason for Development

The anew auditing standard 701 deals with the communication of the key audit matters in the

independent auditors report. The development of the standard has been invoked by the global

financial crisis which has been happened because of the major accounting flaws and

discrepancies that has been made by the management of the some companies. Like Lehman

Brothers, HIH Insurance, ABC Learning and One Tel. These companies are the example and the

reason of bringing the global financial crisis and have alarmed the regulating authorities by the

different class action suits so as to avoid the manipulative practices that have been adopted by

the aforementioned companies (Bajada and Trayler, 2010; Cordos and Fülöpa, 2015).

Meaning

As auditor plays fiduciary role in communicating the financial health and position of the

company to their stakeholders and the shareholders, it is the duty of the auditor to fairly disclose

and describe the true and fair view. Thus, in order to give more value to the auditor report, the

new standard has provided more transparency (AASB, 2015 and Thomson, 2008). The key audit

matters deals with the additional information which will have the valuable impact on the decision

of the investor. It will include those matters which in the view of the auditor’s professional

judgment are of significant importance in the audit of financial statements and thus required

5

significant management judgment. These have resulted the revision of auditing standard on

going concern (Masytoh O, 2010).

KEY AUDIT MATTERS LISTED

In the annual report of the company – Woolworths Limited for the period ending 25th of June

2017, the auditor has communicated five key audit matters in the independent auditors report.

These are as follows:

Exit of Home Improvement

The company has decided to discontinue the operations of the Home Improvement Business. In

this process, there have been major interrelated components which needs to be scrutinized and is

very much complex in nature due to which the auditor of the company has mentioned the same

as one of the key audit matter.

Value of Property Plant and Equipment – Big W

The carrying value of the Big W segment of the company has been arrived after deducting the

huge amount of the impairment. This is so because the results of the Big W have been

deteriorating on a yearly basis and the stage have come where the carrying value of the assets is

more than the recoverable amount. Thus, the company has charged an impairment of $35.3

million. It has been regarded as one of the key audit matters as the management of the company

has uses its own judgment for arriving at the recoverable amount using the future cash flows and

discounting the same at the capitalization rate.

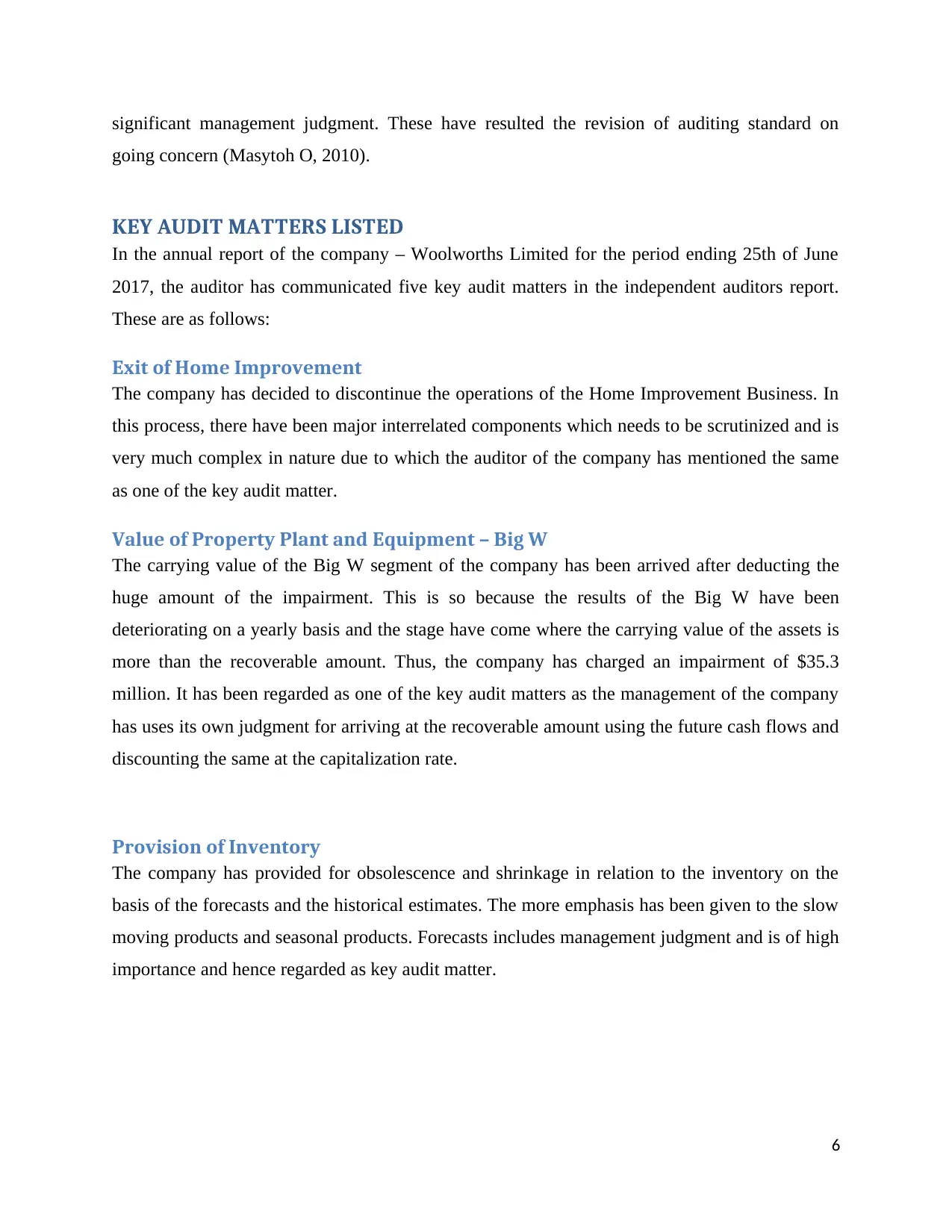

Provision of Inventory

The company has provided for obsolescence and shrinkage in relation to the inventory on the

basis of the forecasts and the historical estimates. The more emphasis has been given to the slow

moving products and seasonal products. Forecasts includes management judgment and is of high

importance and hence regarded as key audit matter.

6

going concern (Masytoh O, 2010).

KEY AUDIT MATTERS LISTED

In the annual report of the company – Woolworths Limited for the period ending 25th of June

2017, the auditor has communicated five key audit matters in the independent auditors report.

These are as follows:

Exit of Home Improvement

The company has decided to discontinue the operations of the Home Improvement Business. In

this process, there have been major interrelated components which needs to be scrutinized and is

very much complex in nature due to which the auditor of the company has mentioned the same

as one of the key audit matter.

Value of Property Plant and Equipment – Big W

The carrying value of the Big W segment of the company has been arrived after deducting the

huge amount of the impairment. This is so because the results of the Big W have been

deteriorating on a yearly basis and the stage have come where the carrying value of the assets is

more than the recoverable amount. Thus, the company has charged an impairment of $35.3

million. It has been regarded as one of the key audit matters as the management of the company

has uses its own judgment for arriving at the recoverable amount using the future cash flows and

discounting the same at the capitalization rate.

Provision of Inventory

The company has provided for obsolescence and shrinkage in relation to the inventory on the

basis of the forecasts and the historical estimates. The more emphasis has been given to the slow

moving products and seasonal products. Forecasts includes management judgment and is of high

importance and hence regarded as key audit matter.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

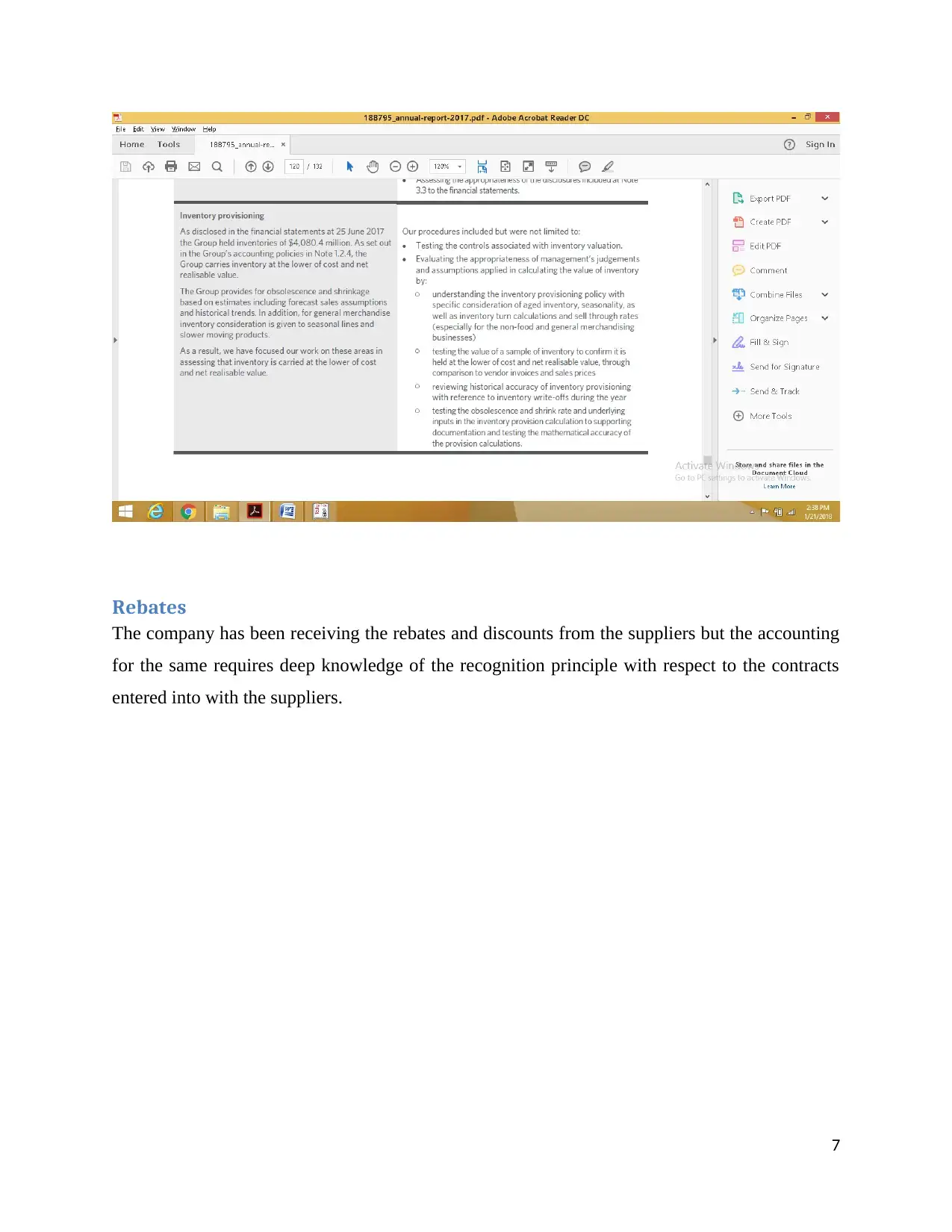

Rebates

The company has been receiving the rebates and discounts from the suppliers but the accounting

for the same requires deep knowledge of the recognition principle with respect to the contracts

entered into with the suppliers.

7

The company has been receiving the rebates and discounts from the suppliers but the accounting

for the same requires deep knowledge of the recognition principle with respect to the contracts

entered into with the suppliers.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

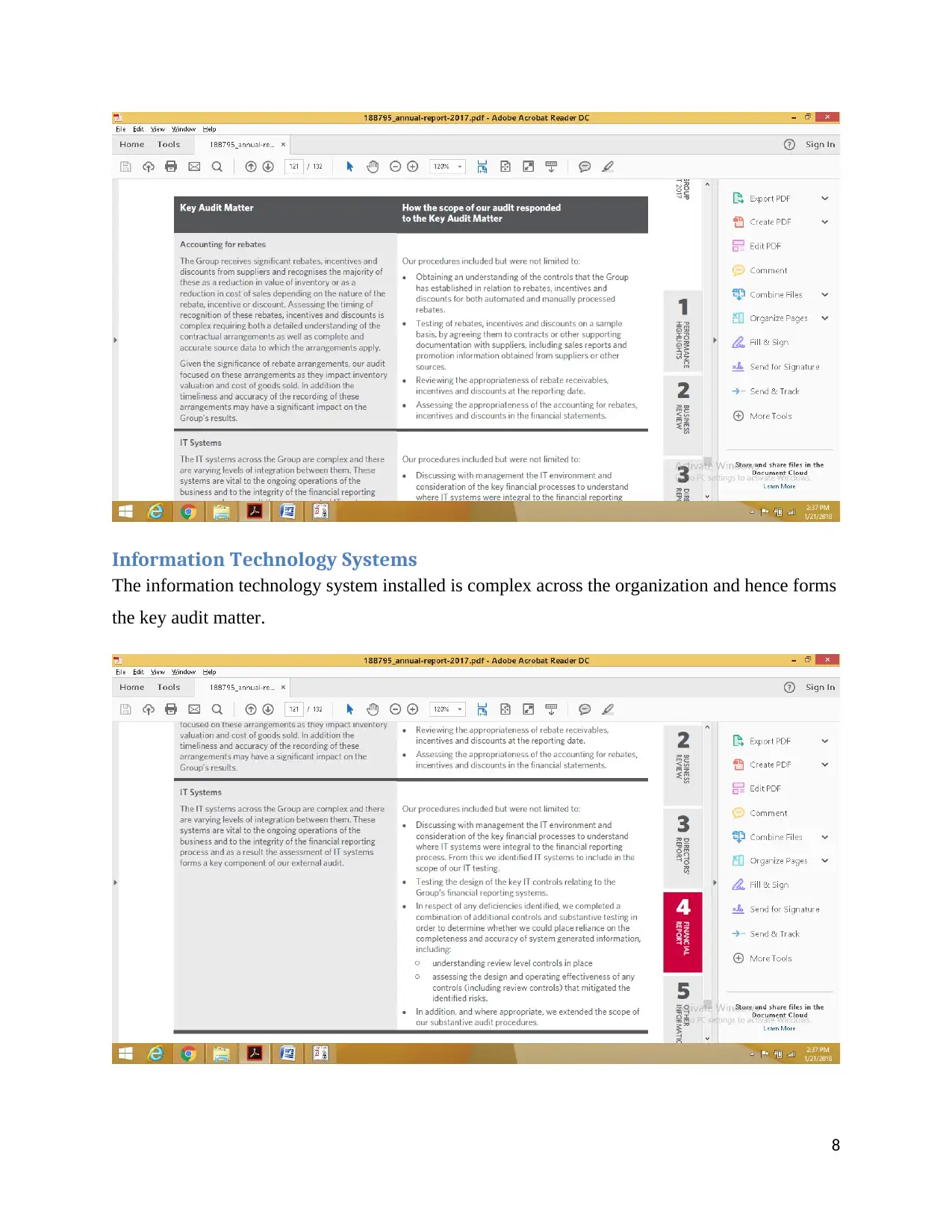

Information Technology Systems

The information technology system installed is complex across the organization and hence forms

the key audit matter.

8

The information technology system installed is complex across the organization and hence forms

the key audit matter.

8

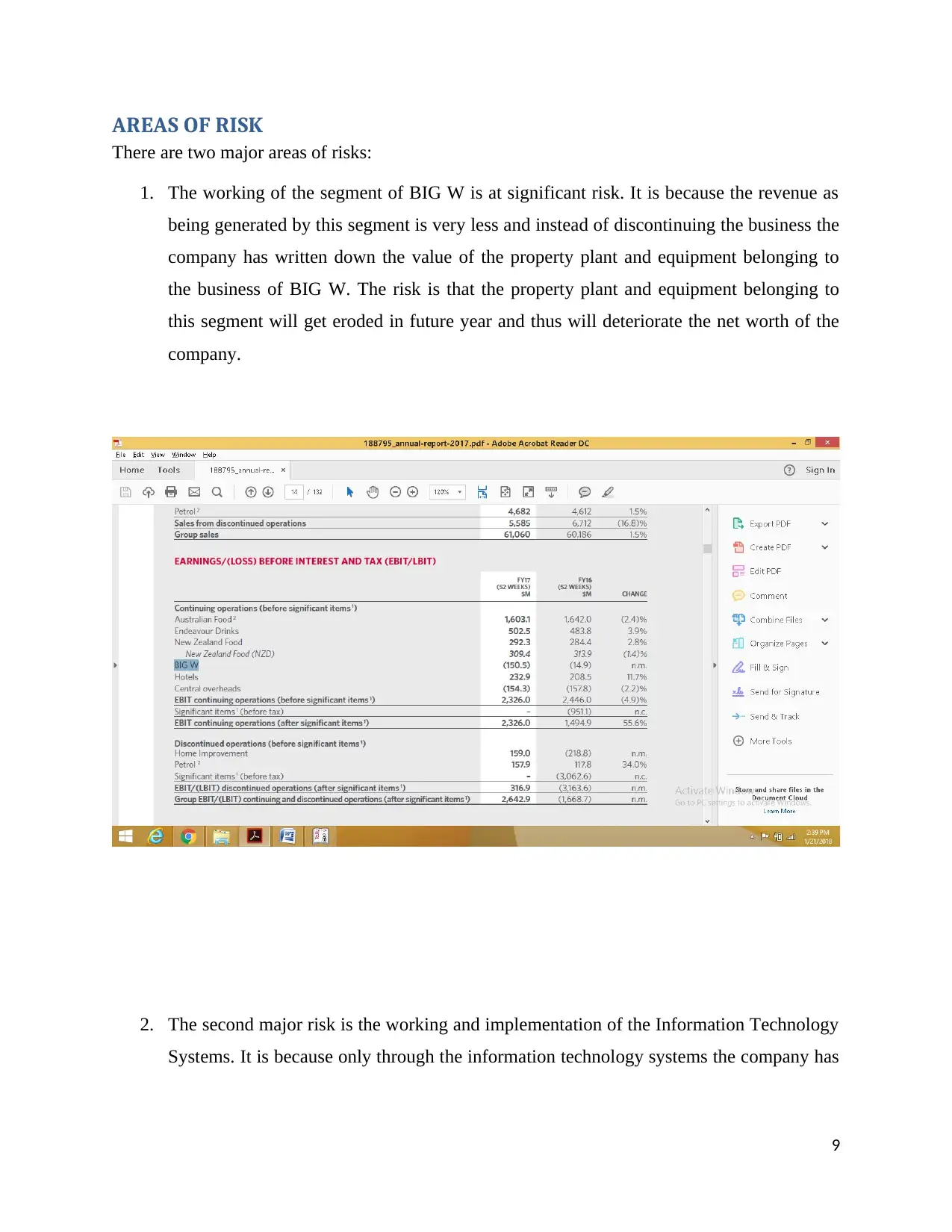

AREAS OF RISK

There are two major areas of risks:

1. The working of the segment of BIG W is at significant risk. It is because the revenue as

being generated by this segment is very less and instead of discontinuing the business the

company has written down the value of the property plant and equipment belonging to

the business of BIG W. The risk is that the property plant and equipment belonging to

this segment will get eroded in future year and thus will deteriorate the net worth of the

company.

2. The second major risk is the working and implementation of the Information Technology

Systems. It is because only through the information technology systems the company has

9

There are two major areas of risks:

1. The working of the segment of BIG W is at significant risk. It is because the revenue as

being generated by this segment is very less and instead of discontinuing the business the

company has written down the value of the property plant and equipment belonging to

the business of BIG W. The risk is that the property plant and equipment belonging to

this segment will get eroded in future year and thus will deteriorate the net worth of the

company.

2. The second major risk is the working and implementation of the Information Technology

Systems. It is because only through the information technology systems the company has

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

been working and if that is complex then it will be difficult for the next auditor and the

investors to rely on the controls placed by the company in this regard.

SIGNIFICANT EVENT OR TRANSACTIONS AND ITS EFFECT ON AUDIT

In accordance with the paragraph number nine of the auditing standard 701, following are the

major significant transaction that have occurred during the course of the audit and have the

relevant effect on the audit as described below (AASB, 2015):

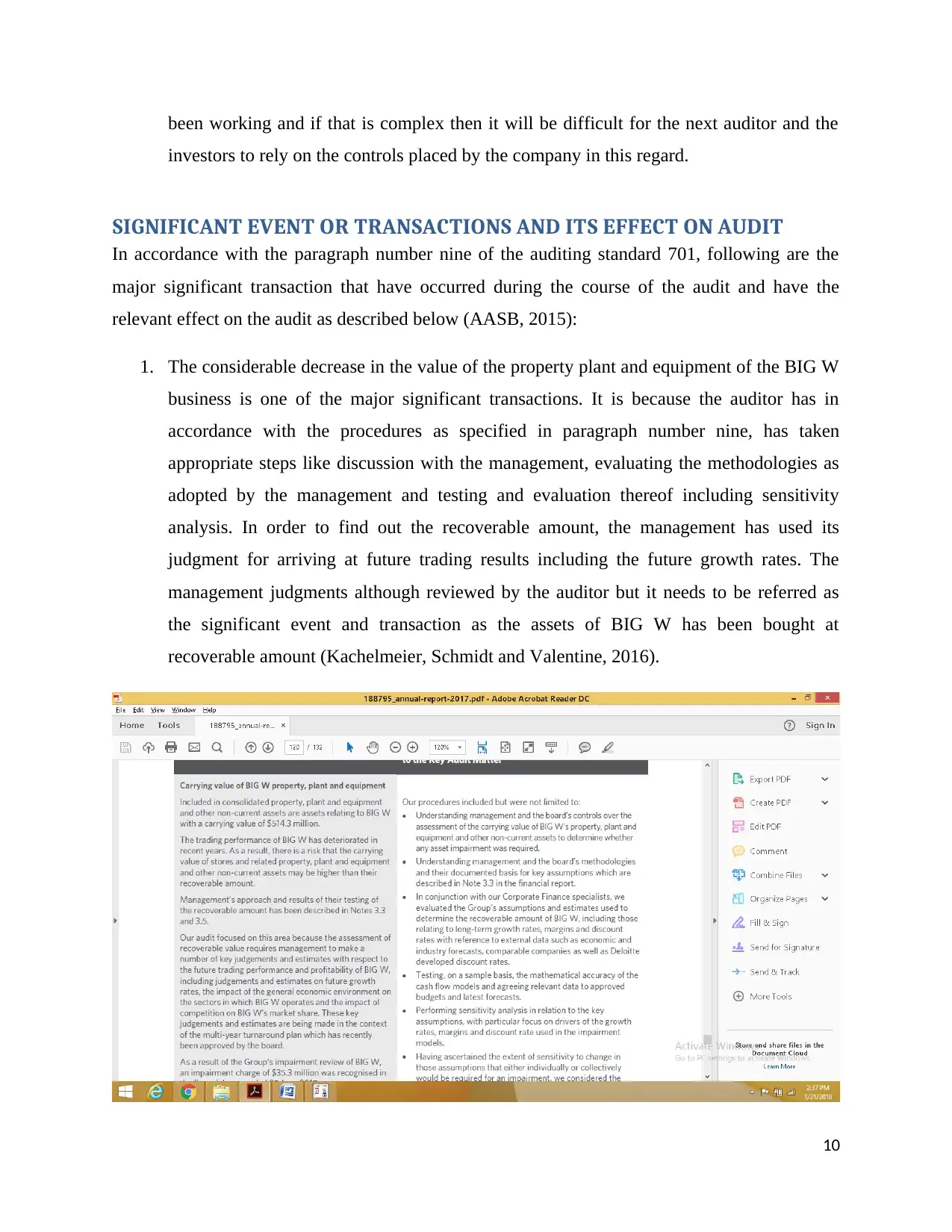

1. The considerable decrease in the value of the property plant and equipment of the BIG W

business is one of the major significant transactions. It is because the auditor has in

accordance with the procedures as specified in paragraph number nine, has taken

appropriate steps like discussion with the management, evaluating the methodologies as

adopted by the management and testing and evaluation thereof including sensitivity

analysis. In order to find out the recoverable amount, the management has used its

judgment for arriving at future trading results including the future growth rates. The

management judgments although reviewed by the auditor but it needs to be referred as

the significant event and transaction as the assets of BIG W has been bought at

recoverable amount (Kachelmeier, Schmidt and Valentine, 2016).

10

investors to rely on the controls placed by the company in this regard.

SIGNIFICANT EVENT OR TRANSACTIONS AND ITS EFFECT ON AUDIT

In accordance with the paragraph number nine of the auditing standard 701, following are the

major significant transaction that have occurred during the course of the audit and have the

relevant effect on the audit as described below (AASB, 2015):

1. The considerable decrease in the value of the property plant and equipment of the BIG W

business is one of the major significant transactions. It is because the auditor has in

accordance with the procedures as specified in paragraph number nine, has taken

appropriate steps like discussion with the management, evaluating the methodologies as

adopted by the management and testing and evaluation thereof including sensitivity

analysis. In order to find out the recoverable amount, the management has used its

judgment for arriving at future trading results including the future growth rates. The

management judgments although reviewed by the auditor but it needs to be referred as

the significant event and transaction as the assets of BIG W has been bought at

recoverable amount (Kachelmeier, Schmidt and Valentine, 2016).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

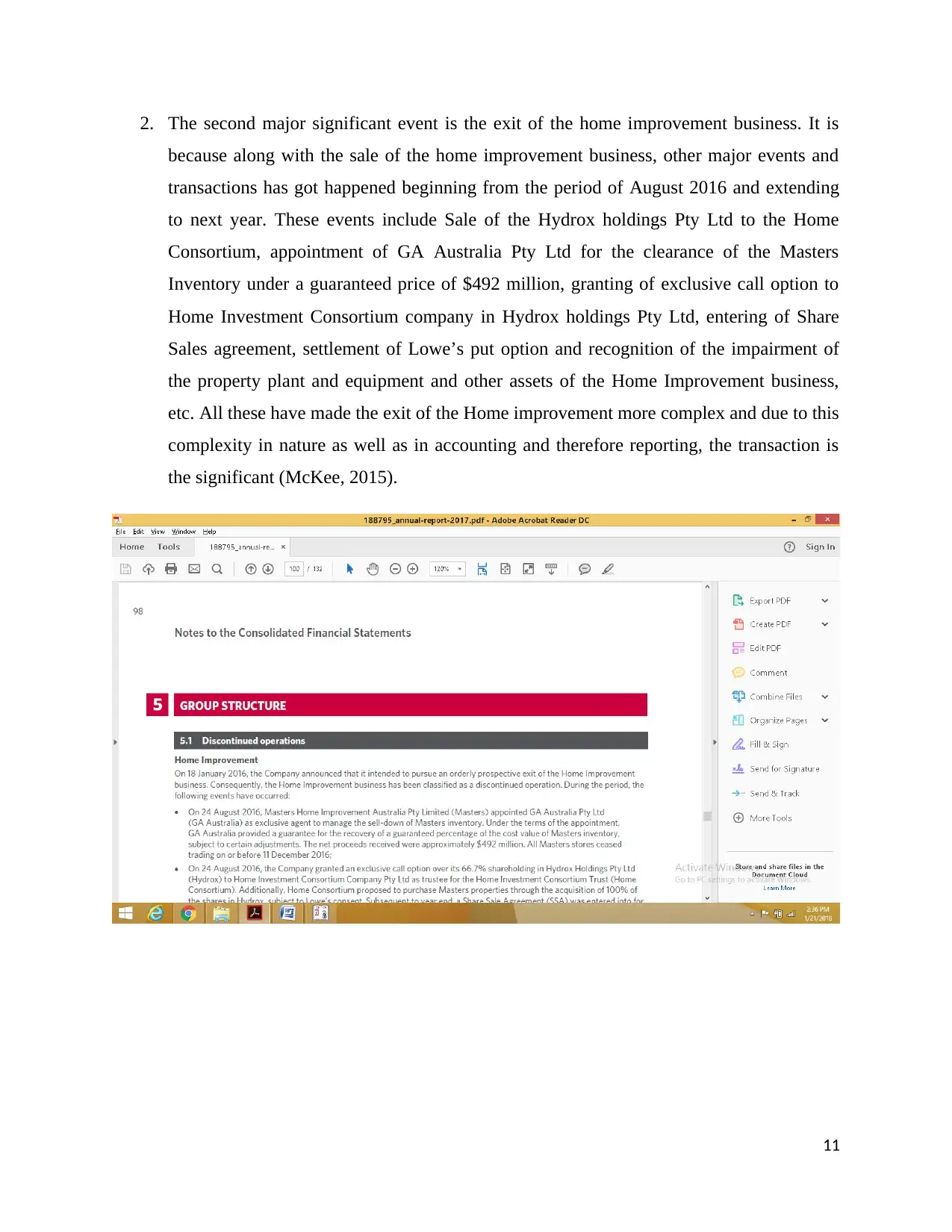

2. The second major significant event is the exit of the home improvement business. It is

because along with the sale of the home improvement business, other major events and

transactions has got happened beginning from the period of August 2016 and extending

to next year. These events include Sale of the Hydrox holdings Pty Ltd to the Home

Consortium, appointment of GA Australia Pty Ltd for the clearance of the Masters

Inventory under a guaranteed price of $492 million, granting of exclusive call option to

Home Investment Consortium company in Hydrox holdings Pty Ltd, entering of Share

Sales agreement, settlement of Lowe’s put option and recognition of the impairment of

the property plant and equipment and other assets of the Home Improvement business,

etc. All these have made the exit of the Home improvement more complex and due to this

complexity in nature as well as in accounting and therefore reporting, the transaction is

the significant (McKee, 2015).

11

because along with the sale of the home improvement business, other major events and

transactions has got happened beginning from the period of August 2016 and extending

to next year. These events include Sale of the Hydrox holdings Pty Ltd to the Home

Consortium, appointment of GA Australia Pty Ltd for the clearance of the Masters

Inventory under a guaranteed price of $492 million, granting of exclusive call option to

Home Investment Consortium company in Hydrox holdings Pty Ltd, entering of Share

Sales agreement, settlement of Lowe’s put option and recognition of the impairment of

the property plant and equipment and other assets of the Home Improvement business,

etc. All these have made the exit of the Home improvement more complex and due to this

complexity in nature as well as in accounting and therefore reporting, the transaction is

the significant (McKee, 2015).

11

RECOMMENDATION AND CONCLUSION

It is recommended for the company to employ the clear and best accounting practices so that

even the complex transactions and the event and the complex accounting can be understood by

the auditor in best manner so that true and fair view can be given.

The new auditing standard 701 has provided more and more transparency to the investors and

will provide the framework for the investors where they can evaluate different companies

performing in particular industry at one place. In the report, the auditor of the company has

mentioned the five key audit matters and relevant significant transaction and the event have

occurred. Although the company is the second largest company in the retail chain sector but the

systems that the company has employed in relation to accounting and management does not

commensurate with the business and thus to conclude the report the accounting treatment and

assumptions shall be carefully done and with transparency.

REFERENCES

AASB, (2015), “ASA 701, Communicating Key Audit Matters in the Independents Auditors

report”, available on http://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf

accessed at 21/01/2018.

Bajada, C. and Trayler, R., 2010. How Australia Survived the Global Financial Crisis. The

Financial and Economic Crises: An International Perspective, Edward Elgar: Cheltenham, UK

and Northampton, USA, pp.139-154.

Cordos, G.S. and Fülöpa, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting and Management Information Systems, 14(1), p.128.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2016. The disclaimer effect of disclosing

critical audit matters in the auditor’s report.

12

It is recommended for the company to employ the clear and best accounting practices so that

even the complex transactions and the event and the complex accounting can be understood by

the auditor in best manner so that true and fair view can be given.

The new auditing standard 701 has provided more and more transparency to the investors and

will provide the framework for the investors where they can evaluate different companies

performing in particular industry at one place. In the report, the auditor of the company has

mentioned the five key audit matters and relevant significant transaction and the event have

occurred. Although the company is the second largest company in the retail chain sector but the

systems that the company has employed in relation to accounting and management does not

commensurate with the business and thus to conclude the report the accounting treatment and

assumptions shall be carefully done and with transparency.

REFERENCES

AASB, (2015), “ASA 701, Communicating Key Audit Matters in the Independents Auditors

report”, available on http://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf

accessed at 21/01/2018.

Bajada, C. and Trayler, R., 2010. How Australia Survived the Global Financial Crisis. The

Financial and Economic Crises: An International Perspective, Edward Elgar: Cheltenham, UK

and Northampton, USA, pp.139-154.

Cordos, G.S. and Fülöpa, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting and Management Information Systems, 14(1), p.128.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2016. The disclaimer effect of disclosing

critical audit matters in the auditor’s report.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.