ACC707: Key Audit Matters ASA 701 in Independent Auditor's Report

VerifiedAdded on 2023/06/12

|15

|3111

|232

Report

AI Summary

This report analyzes Auditing Standard ASA 701, focusing on Communicating Key Audit Matters in the Independent Auditor’s Report, developed in response to the global financial crisis and shareholder demands for more transparency. It examines the rationale behind ASA 701, its core requirements, and its impact on disclosing potential issues like the Going Concern assumption. The analysis includes a review of the annual reports of TPG Telecom Limited and Telstra Corporation, both listed on the Australian Stock Exchange, to assess how their auditors have implemented the standard, particularly in areas like revenue recognition and goodwill valuation. The report concludes by emphasizing the importance of accurate and appropriate disclosure of key audit matters for investors and stakeholders.

Audit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 22nd May 2018.

[Type here]

By student name

Professor

University

Date: 22nd May 2018.

[Type here]

2

Executive Summary

Here, Accounting and Auditing Standards Board, which issued one of the standards on Communicating

Key Audit Matters (SA 701), has been analysed in detail and along with the same, discussion on various

aspects of the mentioned standard has also been stated here. Audit report is one of the most critical

record that the company is required to submit and hence it is essential all that is stated and related to

the company must be accurately mentioned. Required topics that the auditor is required to intimate has

also been mentioned. Conclusions has been drawn and some sections from the annual reports of 2

companies has also been analysed and checked to look as to the way, they have been reporting

important topics in their audit report.

[Type here]

Executive Summary

Here, Accounting and Auditing Standards Board, which issued one of the standards on Communicating

Key Audit Matters (SA 701), has been analysed in detail and along with the same, discussion on various

aspects of the mentioned standard has also been stated here. Audit report is one of the most critical

record that the company is required to submit and hence it is essential all that is stated and related to

the company must be accurately mentioned. Required topics that the auditor is required to intimate has

also been mentioned. Conclusions has been drawn and some sections from the annual reports of 2

companies has also been analysed and checked to look as to the way, they have been reporting

important topics in their audit report.

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTENTS:

Introduction...........…………………………………………………………………..........…...4

Analysis.......................………………........................................................................................6

Conclusion.......................………………...................................................................................10

References......................……………….....................................................................................11

[Type here]

CONTENTS:

Introduction...........…………………………………………………………………..........…...4

Analysis.......................………………........................................................................................6

Conclusion.......................………………...................................................................................10

References......................……………….....................................................................................11

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

In the Independent Auditor’s Report, the Auditing Standard ASA 701 which discusses on Communicating

Key Audit Matters explains important issues that the auditor is required to mention in his audit report.

Some transactions have a material impact on company and it is important all such aspects needs to be

clearly disclosed in the audit report. This standard asks the auditor to check and verify the important,

significant and critical areas which might have a material impact on the entity and therefore, might pose

a problem if not properly audited (Kuhn & Morris, 2016). For the investors of the company, the audit

report is essential as they rely on it to take appropriate resolutions associated with the business. All

these standards have been prepared on the basis of IFRS and comply with the same and are generally

released by the Auditing and Assurance Standards Board (AUASB). The auditor needs to abode with the

given standards and prepare the audit report on the basis of the same, only then it meets the

requirements of the interested stakeholders. This standard is also aimed at enhancing the qualitative

characteristics of the audit. These standards are framed in such a manner as to assist the auditor in the

given circumstances and to discuss the key issues with those charged in governance post which the audit

report is being prepared (Heminway, 2017). The detailed description and contents of the given standard

has been mentioned below. The important characteristics of this standard comprise the points given

below-

The auditor is required to list down all the essential topics that are to be disclosed in the

financials of the listed company. They are also required to take important resolution and reflect

all the important topics and look upon it such that there are no material misstatements in the

financials of the organisation. This is a mandatory requirement that while auditing the listed

companies, the auditors need to comply with the given standard while preparation of the

respective audit report.

In cases where the unlisted company is being involved, the auditor by himself decides what all

topics are essential and are they required to be incorporated in the annual reports. It is not a

mandatory requirement as it completely depends upon the auditor if they want to incorporate

the same or not (Chron, 2017).

Some necessary topics which the auditors are required to abide by and comply at the time when

they are assuming the inclusion of key audit matters in the report are listed below-

[Type here]

Introduction

In the Independent Auditor’s Report, the Auditing Standard ASA 701 which discusses on Communicating

Key Audit Matters explains important issues that the auditor is required to mention in his audit report.

Some transactions have a material impact on company and it is important all such aspects needs to be

clearly disclosed in the audit report. This standard asks the auditor to check and verify the important,

significant and critical areas which might have a material impact on the entity and therefore, might pose

a problem if not properly audited (Kuhn & Morris, 2016). For the investors of the company, the audit

report is essential as they rely on it to take appropriate resolutions associated with the business. All

these standards have been prepared on the basis of IFRS and comply with the same and are generally

released by the Auditing and Assurance Standards Board (AUASB). The auditor needs to abode with the

given standards and prepare the audit report on the basis of the same, only then it meets the

requirements of the interested stakeholders. This standard is also aimed at enhancing the qualitative

characteristics of the audit. These standards are framed in such a manner as to assist the auditor in the

given circumstances and to discuss the key issues with those charged in governance post which the audit

report is being prepared (Heminway, 2017). The detailed description and contents of the given standard

has been mentioned below. The important characteristics of this standard comprise the points given

below-

The auditor is required to list down all the essential topics that are to be disclosed in the

financials of the listed company. They are also required to take important resolution and reflect

all the important topics and look upon it such that there are no material misstatements in the

financials of the organisation. This is a mandatory requirement that while auditing the listed

companies, the auditors need to comply with the given standard while preparation of the

respective audit report.

In cases where the unlisted company is being involved, the auditor by himself decides what all

topics are essential and are they required to be incorporated in the annual reports. It is not a

mandatory requirement as it completely depends upon the auditor if they want to incorporate

the same or not (Chron, 2017).

Some necessary topics which the auditors are required to abide by and comply at the time when

they are assuming the inclusion of key audit matters in the report are listed below-

[Type here]

5

In case there are such domains and areas which are very vulnerable to pose a risk on the

company, the auditor is required to look into the same if they would significantly have an

influence on the decisions of the stakeholders and are significant by nature. The auditor is

required to include these matters in the audit report and along with the individual judgement of

the auditor so that the users of the financial statements are also aware of the views of the

auditor (Goldmann, 2016).

There are different matters that are cited to those charged with governance of the organisation

and in case the auditor realises any matter that is necessary he can report that in his audit

report of the company.

The auditor should specifically check those areas in which the management’s estimation and

decisions along with the assumptions are being involved as these areas may be quite vulnerable.

Hence, this is what should be determined by the auditor when they are dealing with the

company.

This standard further shows the way and the procedure in which the auditor shall explain the

important matters that may have an impact on the company. Appropriate analysis is required

before the same is reported in the audit report. Also disclosure needs to be made as to why that

has been presumed to be important enough to be shown in the audit report.

It is also necessary that appropriate and sufficient disclosures are being made in the audit report

of the company so that in case any modifications are required, then the same could be applied

immediately. The logic is that auditor should have appropriate skill and professional

competence which they can apply while preparing the audit report (Das, 2017).

There may be few cases, where the important and critical matters may still not be considered

and reported in the audit report, then in such a scenario, the auditor is should also disclose the

grounds and basis on which such item has not been recorded. The management of the company

needs to ensure that the auditor is having adequate experience and they are stating and

applying the same while preparing the audit report (Farmer, 2018).

This standard gives all the required steps which the auditor should abide by and adhere to so that

the long term perspective of the company can be built through the study of the audit report. The

investors can look into those important matters and determine if they should be investing in the

[Type here]

In case there are such domains and areas which are very vulnerable to pose a risk on the

company, the auditor is required to look into the same if they would significantly have an

influence on the decisions of the stakeholders and are significant by nature. The auditor is

required to include these matters in the audit report and along with the individual judgement of

the auditor so that the users of the financial statements are also aware of the views of the

auditor (Goldmann, 2016).

There are different matters that are cited to those charged with governance of the organisation

and in case the auditor realises any matter that is necessary he can report that in his audit

report of the company.

The auditor should specifically check those areas in which the management’s estimation and

decisions along with the assumptions are being involved as these areas may be quite vulnerable.

Hence, this is what should be determined by the auditor when they are dealing with the

company.

This standard further shows the way and the procedure in which the auditor shall explain the

important matters that may have an impact on the company. Appropriate analysis is required

before the same is reported in the audit report. Also disclosure needs to be made as to why that

has been presumed to be important enough to be shown in the audit report.

It is also necessary that appropriate and sufficient disclosures are being made in the audit report

of the company so that in case any modifications are required, then the same could be applied

immediately. The logic is that auditor should have appropriate skill and professional

competence which they can apply while preparing the audit report (Das, 2017).

There may be few cases, where the important and critical matters may still not be considered

and reported in the audit report, then in such a scenario, the auditor is should also disclose the

grounds and basis on which such item has not been recorded. The management of the company

needs to ensure that the auditor is having adequate experience and they are stating and

applying the same while preparing the audit report (Farmer, 2018).

This standard gives all the required steps which the auditor should abide by and adhere to so that

the long term perspective of the company can be built through the study of the audit report. The

investors can look into those important matters and determine if they should be investing in the

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

company or not. The key matters which are enlisted shows an insight into the complete business of

the company and hence it is essential that it should be shown with utmost accuracy and

appropriateness so that the end user does not suffers on account of the company or the auditor.

Importance of the new standard

This new standard has been introduced by the AASB in place of the standard ASA 570 (ISA 570)

Going Concern. It is a case that shows that the company will be operating for infinite time and they

have no intention of shutting down their business in future to come. This is termed as the going

concern assumption. It is very essential as investors rely on it to make important decisions if they

want to invest in the company or not. So, this is the manner, the management of the company

operates. Going concern assumption can be at stake by many modifications that may happen in the

financials of the company on time to time basis (Bromwich & Scapens, 2016). The earlier standard

did not give appropriate disclosure relating to that but with the new standard this issue is resolved.

In case there is any such modifications, it would be stated in the key matters of auditing that will

influence the decisions of the investors of the company. The best part of this standard is that they

have given all the measures in details that may influence the going concern assumption of the

company in a way or the other. In case there is any problem, the auditor would be held responsible.

The auditor is required to continue professional scepticism in case there are any error on part of the

auditor it would result in disciplinary actions. So, this draws the auditor more accountable with their

work. The company wants to see that the stakeholders achieve their due from the company, they

are reliable on the company so all the measures should be charged towards them (Belton, 2017).

Analysis

The given standard has been discussed with the help of the annual reports of two companies, and

observing how the respective auditors have abided with the same while reporting these standards in

their respective audit reports. Important and critical matters that were shown in their annual report has

also been briefly discussed. The two companies that have been chosen here for analysis is TPG Telecom

Limited and Telstra Corporation. Both these companies are listed on Australian Stock Exchange and they

are pioneer companies in the telecom sector working out of Australia. The annual reports of both these

companies have been studied and examined.

[Type here]

company or not. The key matters which are enlisted shows an insight into the complete business of

the company and hence it is essential that it should be shown with utmost accuracy and

appropriateness so that the end user does not suffers on account of the company or the auditor.

Importance of the new standard

This new standard has been introduced by the AASB in place of the standard ASA 570 (ISA 570)

Going Concern. It is a case that shows that the company will be operating for infinite time and they

have no intention of shutting down their business in future to come. This is termed as the going

concern assumption. It is very essential as investors rely on it to make important decisions if they

want to invest in the company or not. So, this is the manner, the management of the company

operates. Going concern assumption can be at stake by many modifications that may happen in the

financials of the company on time to time basis (Bromwich & Scapens, 2016). The earlier standard

did not give appropriate disclosure relating to that but with the new standard this issue is resolved.

In case there is any such modifications, it would be stated in the key matters of auditing that will

influence the decisions of the investors of the company. The best part of this standard is that they

have given all the measures in details that may influence the going concern assumption of the

company in a way or the other. In case there is any problem, the auditor would be held responsible.

The auditor is required to continue professional scepticism in case there are any error on part of the

auditor it would result in disciplinary actions. So, this draws the auditor more accountable with their

work. The company wants to see that the stakeholders achieve their due from the company, they

are reliable on the company so all the measures should be charged towards them (Belton, 2017).

Analysis

The given standard has been discussed with the help of the annual reports of two companies, and

observing how the respective auditors have abided with the same while reporting these standards in

their respective audit reports. Important and critical matters that were shown in their annual report has

also been briefly discussed. The two companies that have been chosen here for analysis is TPG Telecom

Limited and Telstra Corporation. Both these companies are listed on Australian Stock Exchange and they

are pioneer companies in the telecom sector working out of Australia. The annual reports of both these

companies have been studied and examined.

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

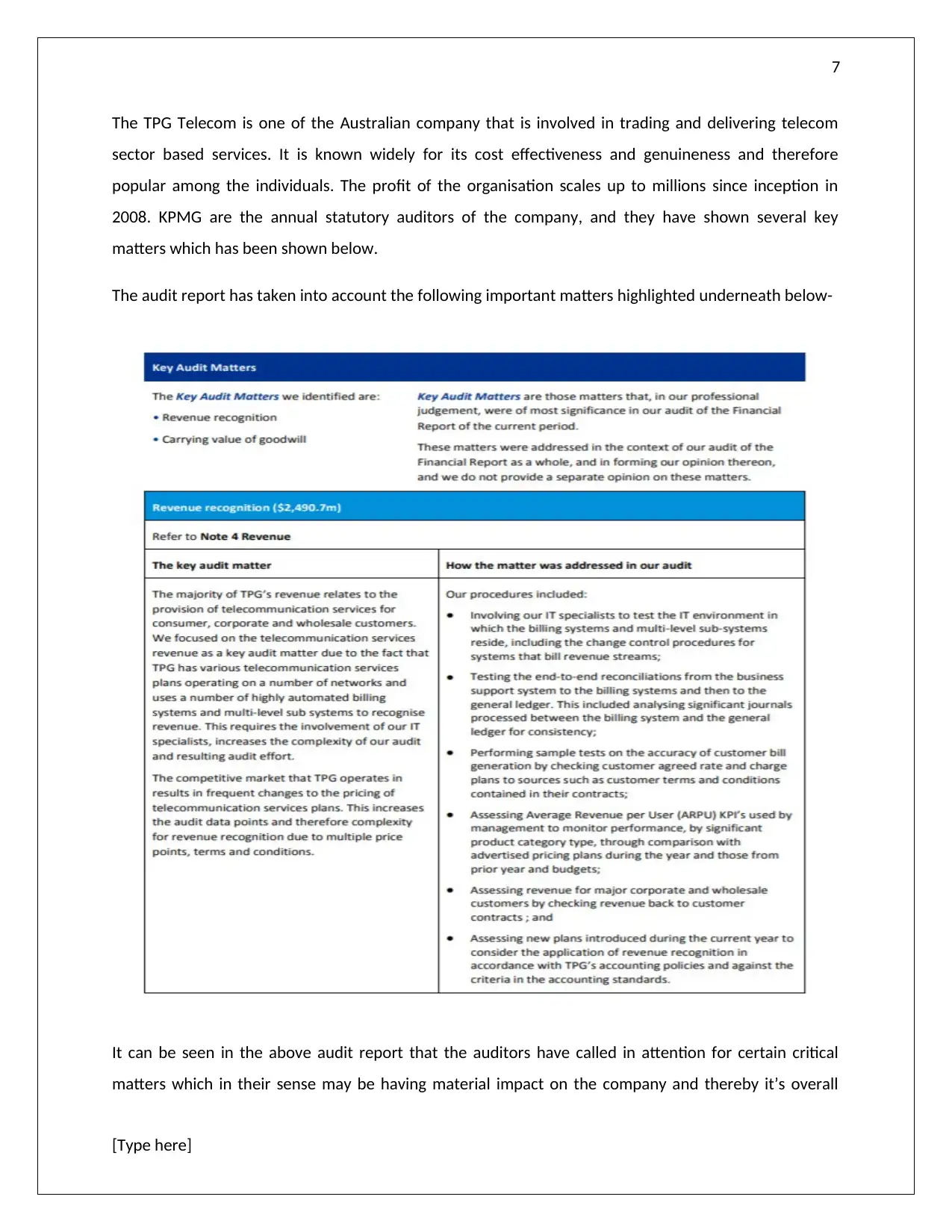

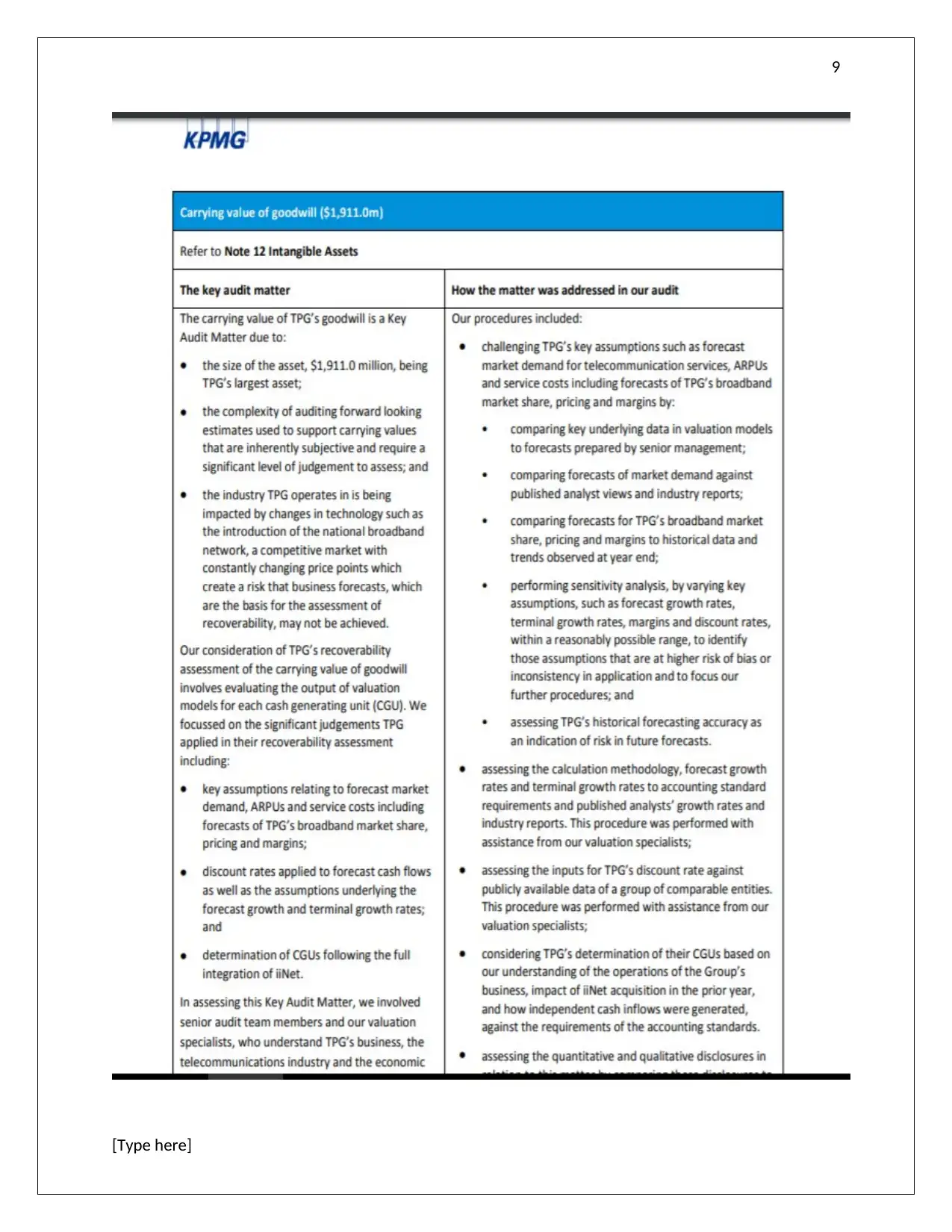

The TPG Telecom is one of the Australian company that is involved in trading and delivering telecom

sector based services. It is known widely for its cost effectiveness and genuineness and therefore

popular among the individuals. The profit of the organisation scales up to millions since inception in

2008. KPMG are the annual statutory auditors of the company, and they have shown several key

matters which has been shown below.

The audit report has taken into account the following important matters highlighted underneath below-

It can be seen in the above audit report that the auditors have called in attention for certain critical

matters which in their sense may be having material impact on the company and thereby it’s overall

[Type here]

The TPG Telecom is one of the Australian company that is involved in trading and delivering telecom

sector based services. It is known widely for its cost effectiveness and genuineness and therefore

popular among the individuals. The profit of the organisation scales up to millions since inception in

2008. KPMG are the annual statutory auditors of the company, and they have shown several key

matters which has been shown below.

The audit report has taken into account the following important matters highlighted underneath below-

It can be seen in the above audit report that the auditors have called in attention for certain critical

matters which in their sense may be having material impact on the company and thereby it’s overall

[Type here]

8

profitability. The main aspects that the auditor has focused upon is revenue recognition. In case of

telecom sector, a very unique method of revenue recognition is being followed which is inclusive of the

valuation aspects and a number of disclosure requirements. Since these companies mainly operate with

high usage of internet based services, they possess a high billing system and the entire gain is

distributed to separate domains. The auditor has also mentioned the appropriate methods which should

have been taken care off and basis which the audit has been done (Kangarluie & Aalizadeh, 2017). The

auditor has also stated the way and disclosed the method the valuation of goodwill which will be helpful

for the company. Therefore, we find that the auditors have given all the necessary disclosures on all

important and significant aspects and topics that may have a material impact on the company’s

financials and have adhered to the set standard. At present, the investors can verify and analyse as to

whether they should invest in the company or not, depending on the key audit matters being disclosed

as this gives a comprehensive snapshot of the company’s performance.

[Type here]

profitability. The main aspects that the auditor has focused upon is revenue recognition. In case of

telecom sector, a very unique method of revenue recognition is being followed which is inclusive of the

valuation aspects and a number of disclosure requirements. Since these companies mainly operate with

high usage of internet based services, they possess a high billing system and the entire gain is

distributed to separate domains. The auditor has also mentioned the appropriate methods which should

have been taken care off and basis which the audit has been done (Kangarluie & Aalizadeh, 2017). The

auditor has also stated the way and disclosed the method the valuation of goodwill which will be helpful

for the company. Therefore, we find that the auditors have given all the necessary disclosures on all

important and significant aspects and topics that may have a material impact on the company’s

financials and have adhered to the set standard. At present, the investors can verify and analyse as to

whether they should invest in the company or not, depending on the key audit matters being disclosed

as this gives a comprehensive snapshot of the company’s performance.

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

[Type here]

[Type here]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

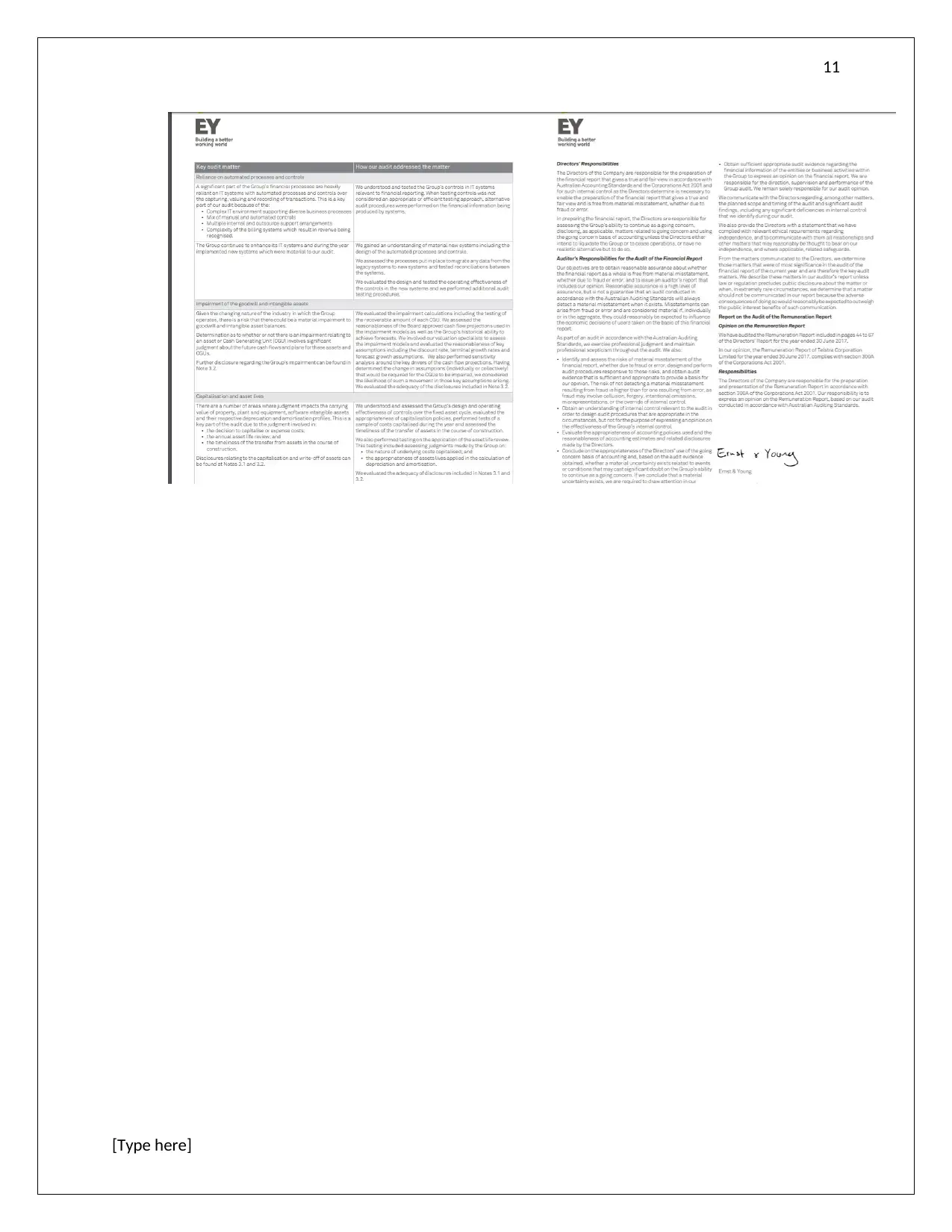

Telstra Corporation

It is the leader in the telecommunication sector in Australia and their financial statements are being

audited by EY. This company trades in mobile phones and tablets, internet and broadband services, sets

and constructs and maintains the telecom towers for the customers. It was setup in 2015 and from then

the company has been growing in terms of revenue. The important aspects have been mentioned in the

auditor’s report and emphasis has been given on the fact of going concern status of the company

(Goldmann, 2016). According to the accounting standard, the auditor shall check for all such domains

and areas that may have a material impact on the company’s financial position and status and will make

appropriate disclosures with regards to the same in the annual report. The necessary matters that were

mentioned in the audit report with respect to the above issues is how they are affect the company and

its growth. In case of Telstra, the key points that have been included in the audit report and on which

proper attention has been given have been listed below –

On the part of Telstra the usage of internet is quite high, and hence its valuation becomes

equally necessary. The auditor has examined the same and has disclosed how they have dealt

with the same.

Goodwill Impairment has been shown as one of another necessary matter by the auditor in his

report. Goodwill is one of the important part that will assist to conclude if the company is

operating better or not. It is all about the market valuation of the company.

Assets capitalization is another critical category that examines how the company is operating

and increasing the revenue. There are other methods in which valuation can be done and thus it

becomes essential to check if the company is following the correct method or not.

All that matters of key considerations have been clearly mentioned in the audit report of the

company. The auditors have also disclosed what the key issue was and how they have dealt with

the same during the course of the audit. From the above analysis, the investors can clearly

analyse and decide whether the company is doing good or not and whether or not to invest in

the company. Thus, these are some of the areas in which the auditor feels suspicious and thus

has covered them specifically in the audit report (Alexander, 2016).

[Type here]

Telstra Corporation

It is the leader in the telecommunication sector in Australia and their financial statements are being

audited by EY. This company trades in mobile phones and tablets, internet and broadband services, sets

and constructs and maintains the telecom towers for the customers. It was setup in 2015 and from then

the company has been growing in terms of revenue. The important aspects have been mentioned in the

auditor’s report and emphasis has been given on the fact of going concern status of the company

(Goldmann, 2016). According to the accounting standard, the auditor shall check for all such domains

and areas that may have a material impact on the company’s financial position and status and will make

appropriate disclosures with regards to the same in the annual report. The necessary matters that were

mentioned in the audit report with respect to the above issues is how they are affect the company and

its growth. In case of Telstra, the key points that have been included in the audit report and on which

proper attention has been given have been listed below –

On the part of Telstra the usage of internet is quite high, and hence its valuation becomes

equally necessary. The auditor has examined the same and has disclosed how they have dealt

with the same.

Goodwill Impairment has been shown as one of another necessary matter by the auditor in his

report. Goodwill is one of the important part that will assist to conclude if the company is

operating better or not. It is all about the market valuation of the company.

Assets capitalization is another critical category that examines how the company is operating

and increasing the revenue. There are other methods in which valuation can be done and thus it

becomes essential to check if the company is following the correct method or not.

All that matters of key considerations have been clearly mentioned in the audit report of the

company. The auditors have also disclosed what the key issue was and how they have dealt with

the same during the course of the audit. From the above analysis, the investors can clearly

analyse and decide whether the company is doing good or not and whether or not to invest in

the company. Thus, these are some of the areas in which the auditor feels suspicious and thus

has covered them specifically in the audit report (Alexander, 2016).

[Type here]

11

[Type here]

[Type here]

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.