HA3032 Audit Program for Asia Pacific Digital Limited - HIHE.

VerifiedAdded on 2023/06/04

|10

|661

|446

Report

AI Summary

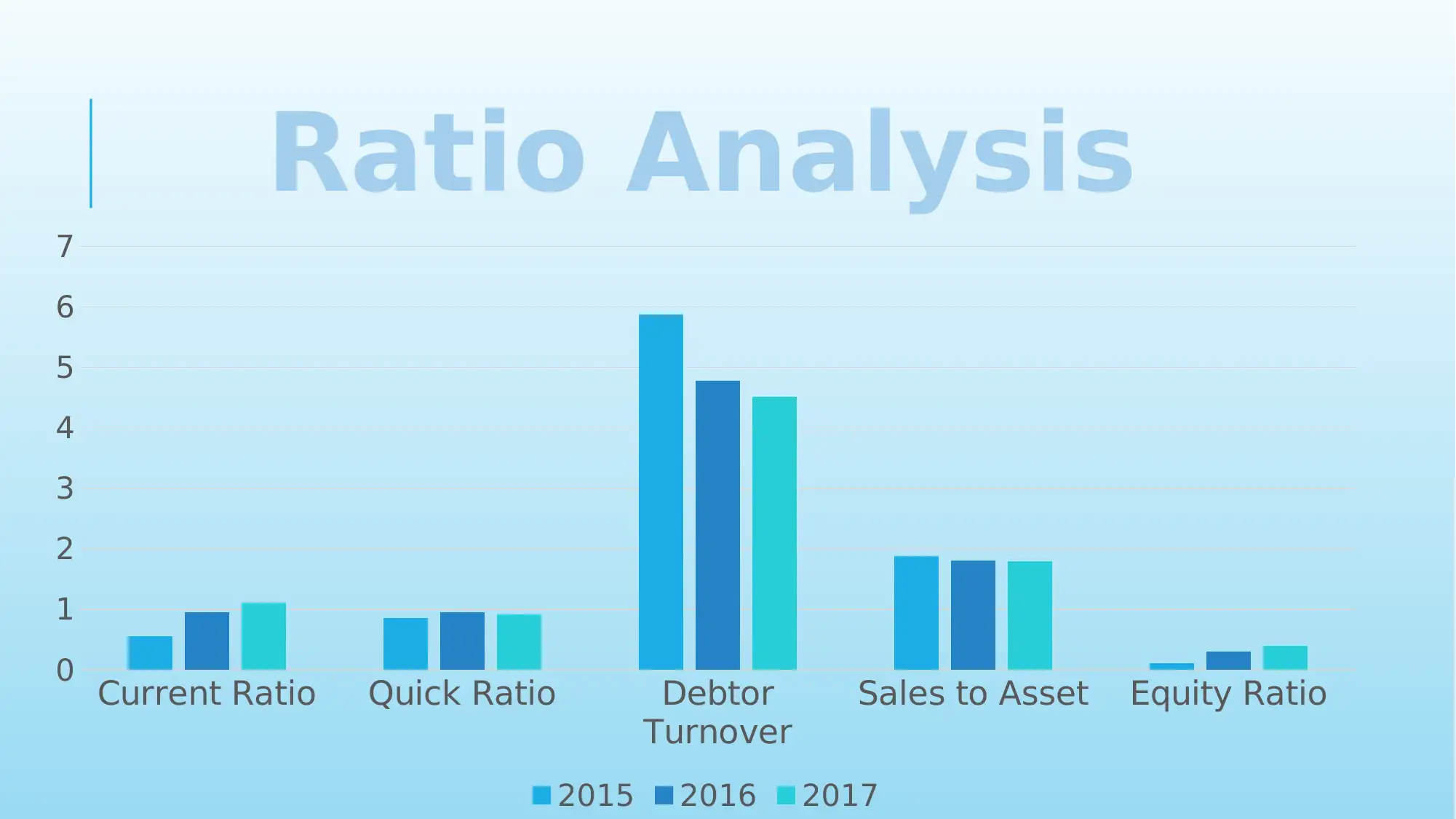

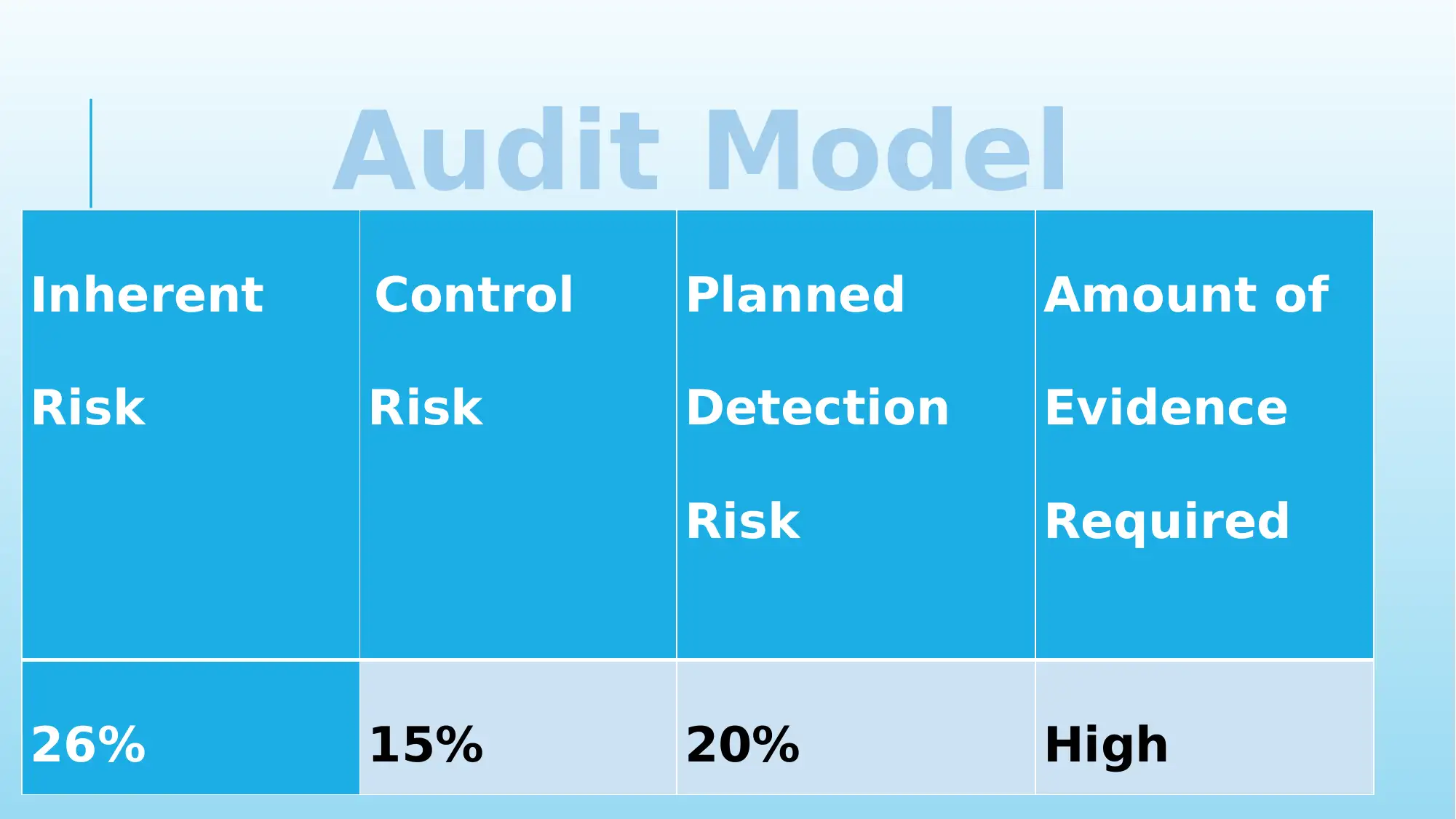

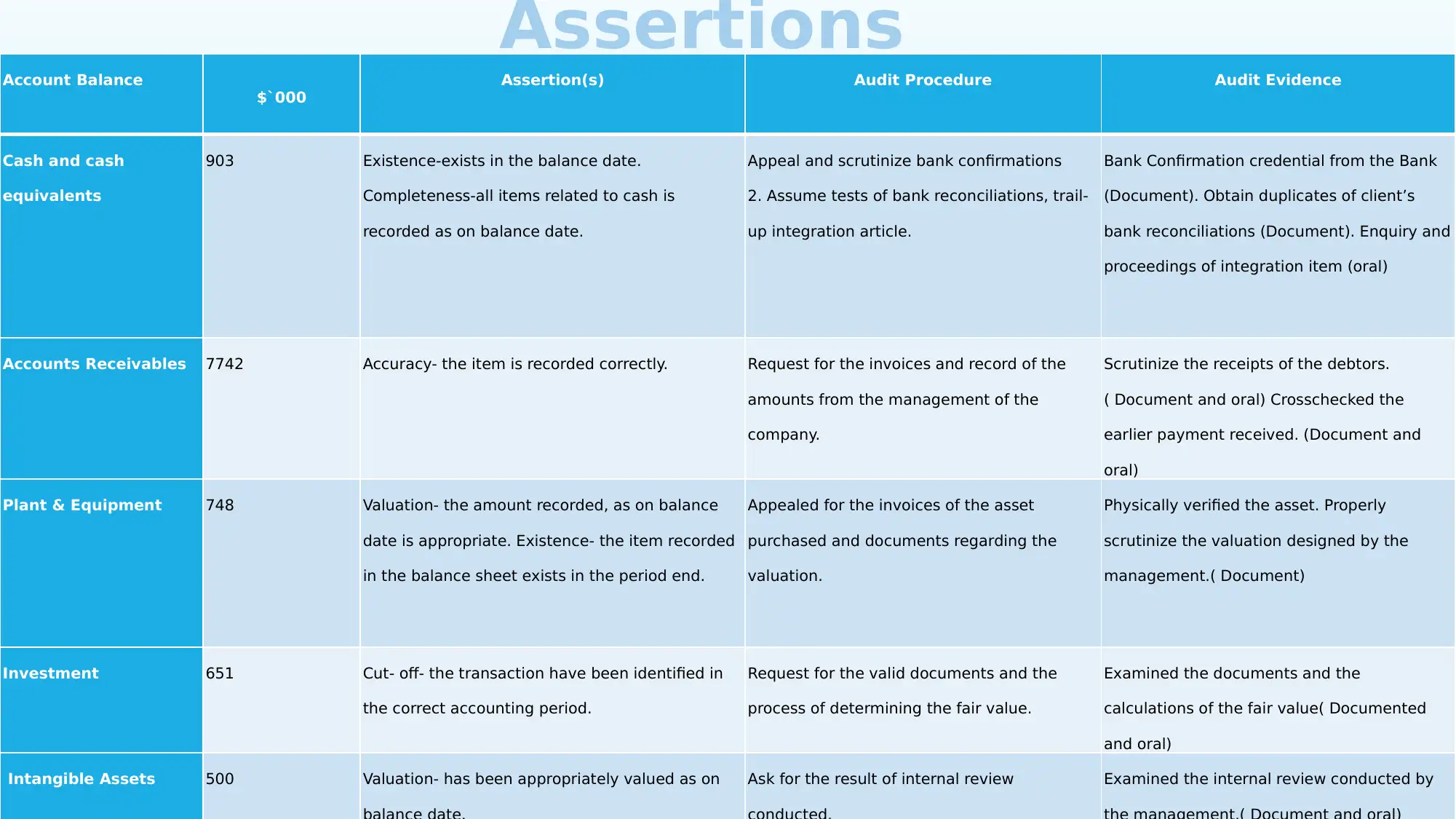

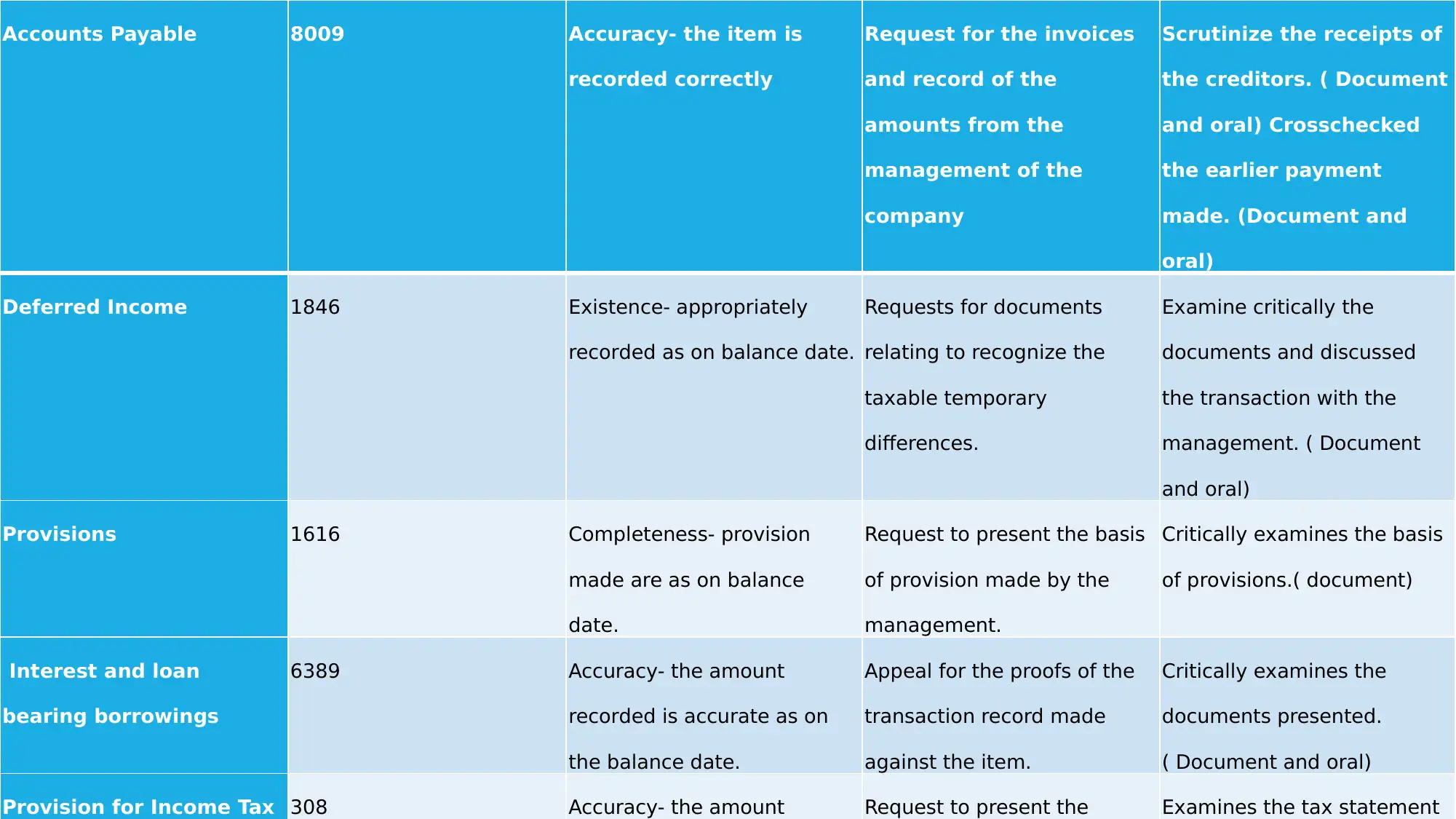

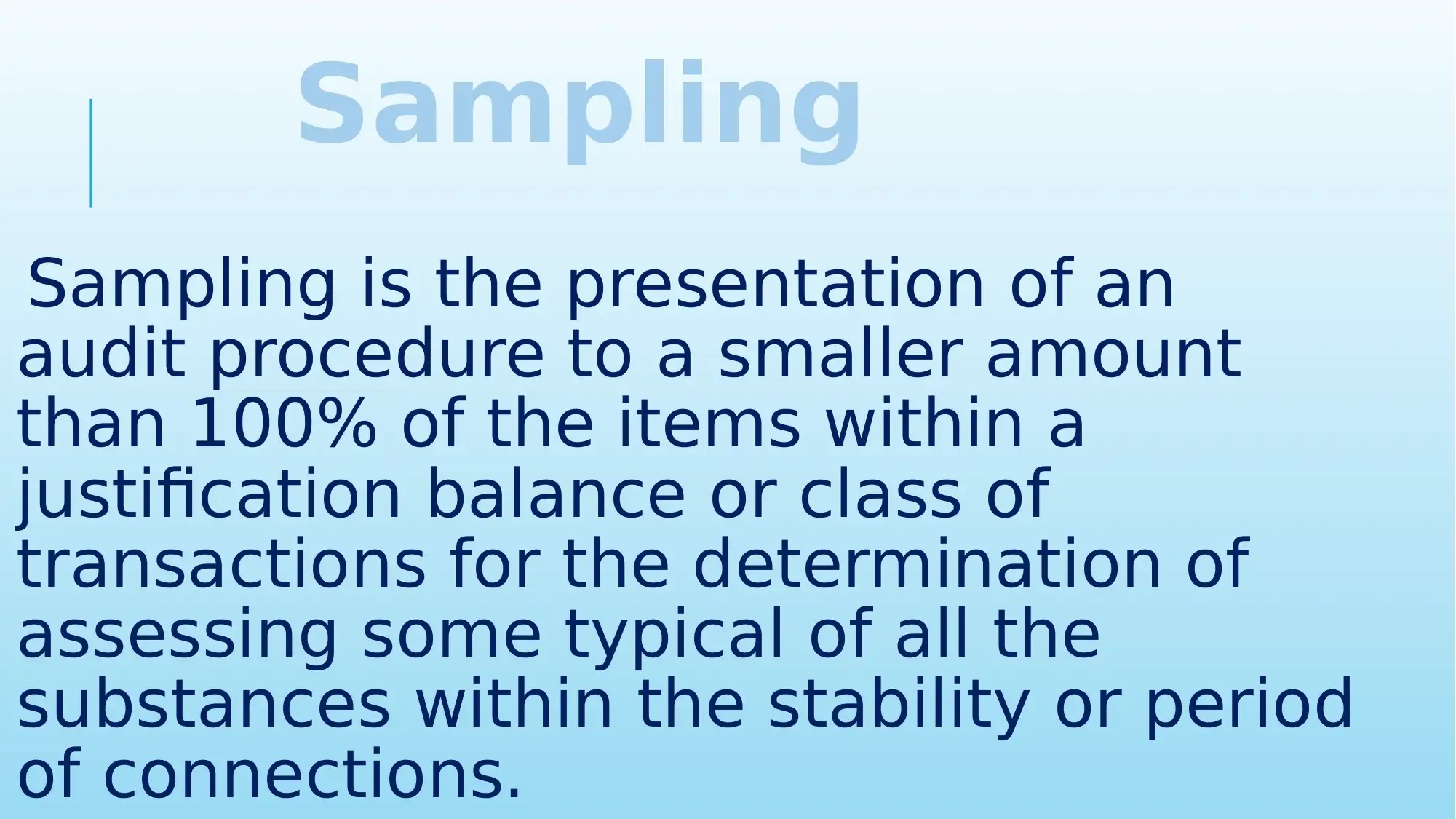

This report outlines an audit program for Asia Pacific Digital Limited, addressing key business risks such as compliance and financial risks, including interest rate, foreign exchange, and liquidity risks. It includes a ratio analysis covering current ratio, quick ratio, debtor turnover, sales to asset ratio, and equity ratio for the years 2015-2017. The audit model details inherent risk, control risk, planned detection risk, and the required evidence. Overall materiality is set at $455180 to identify misstatements. Assertions for account balances, including cash, accounts receivable, plant & equipment, intangible assets, accounts payable, deferred income, provisions, and income tax, are examined with corresponding audit procedures and evidence. The document concludes with a brief explanation of sampling within the audit process.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.