Comprehensive Financial Report on ASOS plc: AC4052 Accounting

VerifiedAdded on 2023/06/15

|13

|2314

|197

Report

AI Summary

This report provides a financial analysis of ASOS plc from 2018 to 2021, utilizing accounting ratios to evaluate the company's performance, liquidity, and financial structure. Section I includes an introduction and interpretation of profitability, operational, structure, and per-employee ratios, concluding that ASOS plc faces challenges in several areas. Section II presents the preparation of an income statement and balance sheet, identifies five key accounting concepts, and includes a statement of cash flow. A short memo to Mrs. Harma summarizes findings from the cash flow statement, highlighting concerns about operating activities and financing activities. The report references various books and journals to support its analysis and recommendations, offering a comprehensive overview of ASOS plc's financial standing during the specified period.

Financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Section I...........................................................................................................................................1

INTRODUCTION.......................................................................................................................1

Interpretation of ratios..................................................................................................................1

CONCLUSION............................................................................................................................3

Section II .........................................................................................................................................4

Question 1....................................................................................................................................4

Preparation of Income Statement.................................................................................................4

Preparation of Balance Sheet.......................................................................................................5

Identify Five Accounting concepts and explain their meaning...................................................6

Question 2....................................................................................................................................6

Preparation of statement of cash flow..........................................................................................6

Short Memo to Mrs. Harma.........................................................................................................7

REFERENCES................................................................................................................................9

Section I...........................................................................................................................................1

INTRODUCTION.......................................................................................................................1

Interpretation of ratios..................................................................................................................1

CONCLUSION............................................................................................................................3

Section II .........................................................................................................................................4

Question 1....................................................................................................................................4

Preparation of Income Statement.................................................................................................4

Preparation of Balance Sheet.......................................................................................................5

Identify Five Accounting concepts and explain their meaning...................................................6

Question 2....................................................................................................................................6

Preparation of statement of cash flow..........................................................................................6

Short Memo to Mrs. Harma.........................................................................................................7

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section I

INTRODUCTION

The fiscal ratios review of ASOS plc is described in the subsequent sections. The

comprehensive balancing statements and revenue account of ASOS PLC were used to calculate

finance indicators such as return on assets, net working capital, and working capital proportions

(Commerford, Hatfield and Houston, 2018). In addition, the study includes a detailed ratios

assessment of ASOS PLC's. The study's main goal is to describe and assess ASOS PLC's fiscal

situation. Asos plc is a global apparel retailer with locations all over the world. Its distinctive

selling point is its user-friendly open-source web application. Asos offers its consumers a highly

comprehensive consumer environment with a choice of well-curated 200 thousand items

acquired from the finest merchants all around the world. ASOS Designer, ASOS Limited, ASOS

4505, and Connivance are among some of the company's in-house clothing companies. Asos is a

customer-centric company which provides industry-leading services, as evidenced by its state-of-

the-art distribution centre in the United Kingdom, France, and the United States, as well as

relatively simple payments and distribution of goods methods. Asos plc owns 896 facilities in

160 nations that allows it to monitor ASOS clothing and cut completion and manufacturing

period. ASOS Designs, ASOS 4505, AsYou, and ASOS Luxury are among its well-known

products and brands. Factory workers trim, stitch, and polish ASOS branded items in the major

manufacturing locations that are subsequently transported to ASOS stores.

Interpretation of ratios

Profitability ratios

Return on Shareholders’ Funds- It can be said that the ratio is not at a satisfactory

position though it was in the year 2018 but it dropped drastically from 23.25 to 7.3 in the

year 2019, and was recouped back at around 17 percent in the year 2020 and 2021.

Return on Capital Employed- This ratio of the company is also not in a very good

position as it is declining since 2018 from 22.72 as it was 6.99 in 2019 and 12.52 and

9.39 in the year 2020 and 2021 which is not a good sign for the firm at all.

INTRODUCTION

The fiscal ratios review of ASOS plc is described in the subsequent sections. The

comprehensive balancing statements and revenue account of ASOS PLC were used to calculate

finance indicators such as return on assets, net working capital, and working capital proportions

(Commerford, Hatfield and Houston, 2018). In addition, the study includes a detailed ratios

assessment of ASOS PLC's. The study's main goal is to describe and assess ASOS PLC's fiscal

situation. Asos plc is a global apparel retailer with locations all over the world. Its distinctive

selling point is its user-friendly open-source web application. Asos offers its consumers a highly

comprehensive consumer environment with a choice of well-curated 200 thousand items

acquired from the finest merchants all around the world. ASOS Designer, ASOS Limited, ASOS

4505, and Connivance are among some of the company's in-house clothing companies. Asos is a

customer-centric company which provides industry-leading services, as evidenced by its state-of-

the-art distribution centre in the United Kingdom, France, and the United States, as well as

relatively simple payments and distribution of goods methods. Asos plc owns 896 facilities in

160 nations that allows it to monitor ASOS clothing and cut completion and manufacturing

period. ASOS Designs, ASOS 4505, AsYou, and ASOS Luxury are among its well-known

products and brands. Factory workers trim, stitch, and polish ASOS branded items in the major

manufacturing locations that are subsequently transported to ASOS stores.

Interpretation of ratios

Profitability ratios

Return on Shareholders’ Funds- It can be said that the ratio is not at a satisfactory

position though it was in the year 2018 but it dropped drastically from 23.25 to 7.3 in the

year 2019, and was recouped back at around 17 percent in the year 2020 and 2021.

Return on Capital Employed- This ratio of the company is also not in a very good

position as it is declining since 2018 from 22.72 as it was 6.99 in 2019 and 12.52 and

9.39 in the year 2020 and 2021 which is not a good sign for the firm at all.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Return on Total Assets- This ratio is also on a trend on declining as it was 10.13 in the

year 2018 and since then it is less than that as it was 2.66, 7.14, and 6.14 in the year 2019,

2020, and 2021 respectively (Fan and Chatterjee, 2018).

Profit margin- This ratio is in a better position as compared to in the year 2018 to 2021

though it declined from 4.22 to 1.21 in the year 2018 to 2019 but it rose again and were

standing at 4.35 and 4.53 in the year 2020 and 2021 respectively.

Gross margin- This ratio is also declining when we see it while taking the base year as

2018 as in that year the ratio was 51.18 while from the next three years that is 2019,

2020, and 2021 it was standing at 48.81, 47.42, and 45.43 respectively.

Operational ratios

Net Assets Turnover- This ratio also declined but the exception was the year 2019

where it rose as compared to the year 2018 as it rose from 5.38 to 5.78 respectively while

for both the year that is 2020 and 2021 the ratio was standing at 2.87 and 2.07

respectively (Kovalenko, 2019).

Fixed Assets Turnover- This ratio kept on declining since 2018 as it was standing at 4.8

in that year while it was 4.39 for the year 2019, 3.37 for the year 2020 and 2.95 for the

year 2021.

Interest Cover- This ratio shows a declining trend and that too very steeply as it was 511

in the year 2018 and it came down to 17.55 in the year 2019 which was down by a huge

margin and further it dropped to 15.96 and 14.42 in the year 2020 and 2021 respectively.

Stock Turnover- This ratio declined too except in the year 2020 as compared to the year

2018 as it was standing at 5.93 in the year 2018 while it rose to 6.13 in the year 2020

while for the rest of the year that is 2019 and 2021 it was down and was standing at 5.09

and 4.85 respectively.

Debtor Collection- This ratio is also not at a favourable position as it is increasing as it

was 2.13 in the year 2018 while it rose to 2.54 in the year 2019 while it came down a bit

in the year 2020 and was standing at 2.36 but again it rose and stood up at 3.88 in the

year 2021 (Sonnenberg, 2018).

Creditors Payment- This ratio can be said to be in a good position as it rose and was

standing at 14.8 in the year 2018 while it rose to 39.5 in the year 2020 but again it fell a

bit and stood up at 36.81 in the year 2021.

year 2018 and since then it is less than that as it was 2.66, 7.14, and 6.14 in the year 2019,

2020, and 2021 respectively (Fan and Chatterjee, 2018).

Profit margin- This ratio is in a better position as compared to in the year 2018 to 2021

though it declined from 4.22 to 1.21 in the year 2018 to 2019 but it rose again and were

standing at 4.35 and 4.53 in the year 2020 and 2021 respectively.

Gross margin- This ratio is also declining when we see it while taking the base year as

2018 as in that year the ratio was 51.18 while from the next three years that is 2019,

2020, and 2021 it was standing at 48.81, 47.42, and 45.43 respectively.

Operational ratios

Net Assets Turnover- This ratio also declined but the exception was the year 2019

where it rose as compared to the year 2018 as it rose from 5.38 to 5.78 respectively while

for both the year that is 2020 and 2021 the ratio was standing at 2.87 and 2.07

respectively (Kovalenko, 2019).

Fixed Assets Turnover- This ratio kept on declining since 2018 as it was standing at 4.8

in that year while it was 4.39 for the year 2019, 3.37 for the year 2020 and 2.95 for the

year 2021.

Interest Cover- This ratio shows a declining trend and that too very steeply as it was 511

in the year 2018 and it came down to 17.55 in the year 2019 which was down by a huge

margin and further it dropped to 15.96 and 14.42 in the year 2020 and 2021 respectively.

Stock Turnover- This ratio declined too except in the year 2020 as compared to the year

2018 as it was standing at 5.93 in the year 2018 while it rose to 6.13 in the year 2020

while for the rest of the year that is 2019 and 2021 it was down and was standing at 5.09

and 4.85 respectively.

Debtor Collection- This ratio is also not at a favourable position as it is increasing as it

was 2.13 in the year 2018 while it rose to 2.54 in the year 2019 while it came down a bit

in the year 2020 and was standing at 2.36 but again it rose and stood up at 3.88 in the

year 2021 (Sonnenberg, 2018).

Creditors Payment- This ratio can be said to be in a good position as it rose and was

standing at 14.8 in the year 2018 while it rose to 39.5 in the year 2020 but again it fell a

bit and stood up at 36.81 in the year 2021.

Structure ratios

Current ratio- This ratio is not at a satisfactory level in the year 2018 as it was only .9

but is increasing slowly and gradually which is a good sign for the company as it rose to

1.19 and 1.56 in the year 2020 and 2021 except for the year 2019 where it fell to .81.

Liquidity ratio- This ratio of the firm is also increasing except in the year 2019 when the

base is taken as 2018 as it was .17 in the year 2018 after which it fell to .11 in the year

2019 and after that it again rose to .57 and .75 in the year 2020 and 2021 respectively

(Suykens, De Rynck and Verschuere, 2019).

Gearing- This ratio is increasing significantly as compared to 2018 as it was just 2.32 at

that time and then it drastically rose to 20.88 in the year 2019 and then again it rose more

than twice times higher as it was in 2019 as was standing at 42.86 in the year 2020 and

85.13 in the year 2021.

Per employee ratios

Profit per employee- It rose in every year except in the year 2019 as it was 23910 in the

year 2018, 6961 in the year 2019, 37160 in the year 2020, and 58710 in the year 2021.

Turnover per employee- This ratio rose in every year as it was 566643 in the year 2018,

574869 in the year 2019, 853426 in the year 2020, and was 1296155 in the year 2021.

Salaries/Turnover- This ratio is on a declining mode since 2018 as it was 6.68 in that

year and then it was 6.58 in the year 2019, 5.61 in the year 2020, and 4.14 in the year

2021 (Zimon and Zimon, 2019).

CONCLUSION

It can be concluded that the firm which is ASOS plc is not doing well in the market in many

areas and thus it is very crucial as well as critical for the firm to keep a tab on its overall

activities so that it can find out the errors in the operation so that appropriate measures can be

taken in that context which can further help the firm to establish its market value in the industry

in which it is operating.

Current ratio- This ratio is not at a satisfactory level in the year 2018 as it was only .9

but is increasing slowly and gradually which is a good sign for the company as it rose to

1.19 and 1.56 in the year 2020 and 2021 except for the year 2019 where it fell to .81.

Liquidity ratio- This ratio of the firm is also increasing except in the year 2019 when the

base is taken as 2018 as it was .17 in the year 2018 after which it fell to .11 in the year

2019 and after that it again rose to .57 and .75 in the year 2020 and 2021 respectively

(Suykens, De Rynck and Verschuere, 2019).

Gearing- This ratio is increasing significantly as compared to 2018 as it was just 2.32 at

that time and then it drastically rose to 20.88 in the year 2019 and then again it rose more

than twice times higher as it was in 2019 as was standing at 42.86 in the year 2020 and

85.13 in the year 2021.

Per employee ratios

Profit per employee- It rose in every year except in the year 2019 as it was 23910 in the

year 2018, 6961 in the year 2019, 37160 in the year 2020, and 58710 in the year 2021.

Turnover per employee- This ratio rose in every year as it was 566643 in the year 2018,

574869 in the year 2019, 853426 in the year 2020, and was 1296155 in the year 2021.

Salaries/Turnover- This ratio is on a declining mode since 2018 as it was 6.68 in that

year and then it was 6.58 in the year 2019, 5.61 in the year 2020, and 4.14 in the year

2021 (Zimon and Zimon, 2019).

CONCLUSION

It can be concluded that the firm which is ASOS plc is not doing well in the market in many

areas and thus it is very crucial as well as critical for the firm to keep a tab on its overall

activities so that it can find out the errors in the operation so that appropriate measures can be

taken in that context which can further help the firm to establish its market value in the industry

in which it is operating.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section II

Question 1

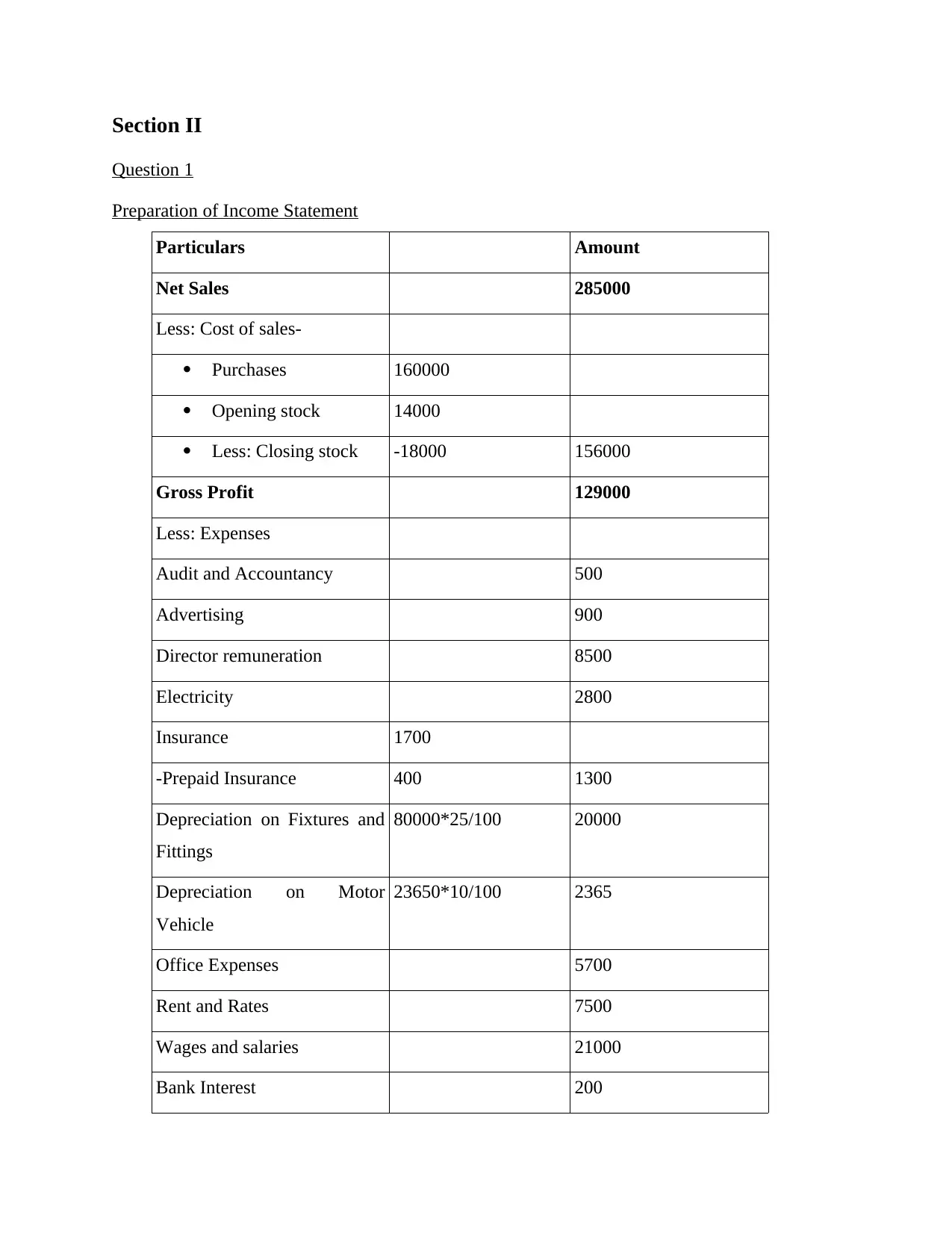

Preparation of Income Statement

Particulars Amount

Net Sales 285000

Less: Cost of sales-

Purchases 160000

Opening stock 14000

Less: Closing stock -18000 156000

Gross Profit 129000

Less: Expenses

Audit and Accountancy 500

Advertising 900

Director remuneration 8500

Electricity 2800

Insurance 1700

-Prepaid Insurance 400 1300

Depreciation on Fixtures and

Fittings

80000*25/100 20000

Depreciation on Motor

Vehicle

23650*10/100 2365

Office Expenses 5700

Rent and Rates 7500

Wages and salaries 21000

Bank Interest 200

Question 1

Preparation of Income Statement

Particulars Amount

Net Sales 285000

Less: Cost of sales-

Purchases 160000

Opening stock 14000

Less: Closing stock -18000 156000

Gross Profit 129000

Less: Expenses

Audit and Accountancy 500

Advertising 900

Director remuneration 8500

Electricity 2800

Insurance 1700

-Prepaid Insurance 400 1300

Depreciation on Fixtures and

Fittings

80000*25/100 20000

Depreciation on Motor

Vehicle

23650*10/100 2365

Office Expenses 5700

Rent and Rates 7500

Wages and salaries 21000

Bank Interest 200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

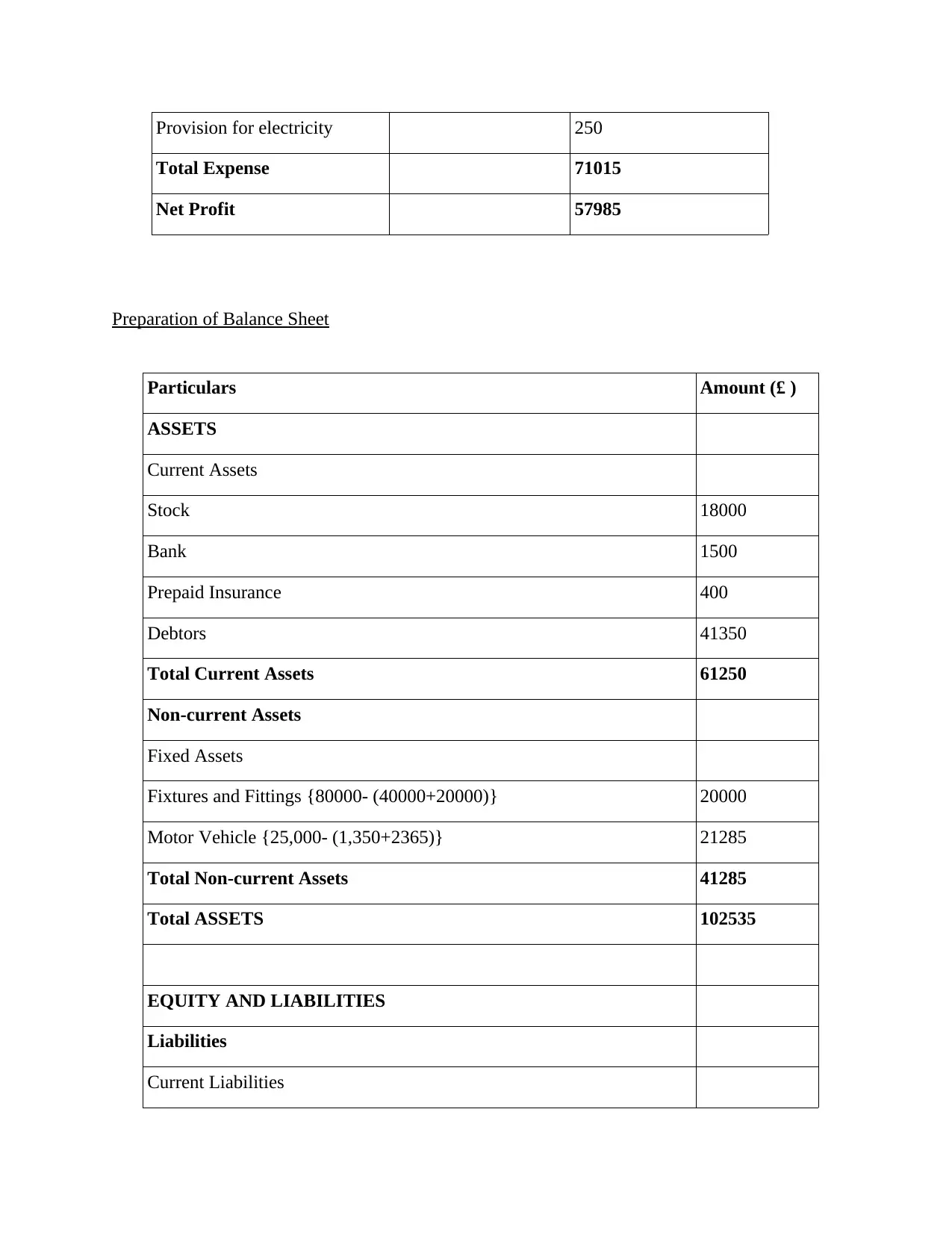

Provision for electricity 250

Total Expense 71015

Net Profit 57985

Preparation of Balance Sheet

Particulars Amount (£ )

ASSETS

Current Assets

Stock 18000

Bank 1500

Prepaid Insurance 400

Debtors 41350

Total Current Assets 61250

Non-current Assets

Fixed Assets

Fixtures and Fittings {80000- (40000+20000)} 20000

Motor Vehicle {25,000- (1,350+2365)} 21285

Total Non-current Assets 41285

Total ASSETS 102535

EQUITY AND LIABILITIES

Liabilities

Current Liabilities

Total Expense 71015

Net Profit 57985

Preparation of Balance Sheet

Particulars Amount (£ )

ASSETS

Current Assets

Stock 18000

Bank 1500

Prepaid Insurance 400

Debtors 41350

Total Current Assets 61250

Non-current Assets

Fixed Assets

Fixtures and Fittings {80000- (40000+20000)} 20000

Motor Vehicle {25,000- (1,350+2365)} 21285

Total Non-current Assets 41285

Total ASSETS 102535

EQUITY AND LIABILITIES

Liabilities

Current Liabilities

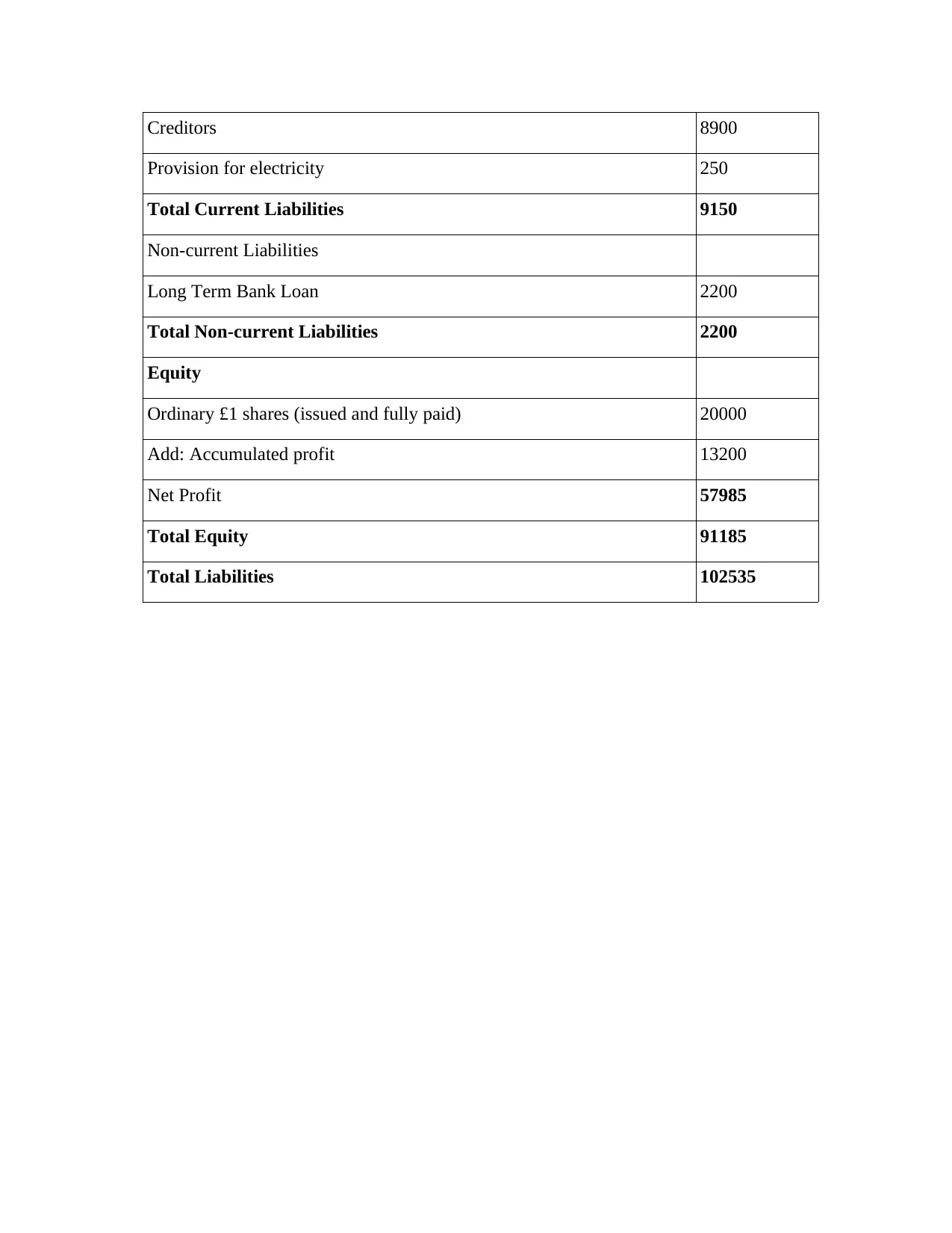

Creditors 8900

Provision for electricity 250

Total Current Liabilities 9150

Non-current Liabilities

Long Term Bank Loan 2200

Total Non-current Liabilities 2200

Equity

Ordinary £1 shares (issued and fully paid) 20000

Add: Accumulated profit 13200

Net Profit 57985

Total Equity 91185

Total Liabilities 102535

Provision for electricity 250

Total Current Liabilities 9150

Non-current Liabilities

Long Term Bank Loan 2200

Total Non-current Liabilities 2200

Equity

Ordinary £1 shares (issued and fully paid) 20000

Add: Accumulated profit 13200

Net Profit 57985

Total Equity 91185

Total Liabilities 102535

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

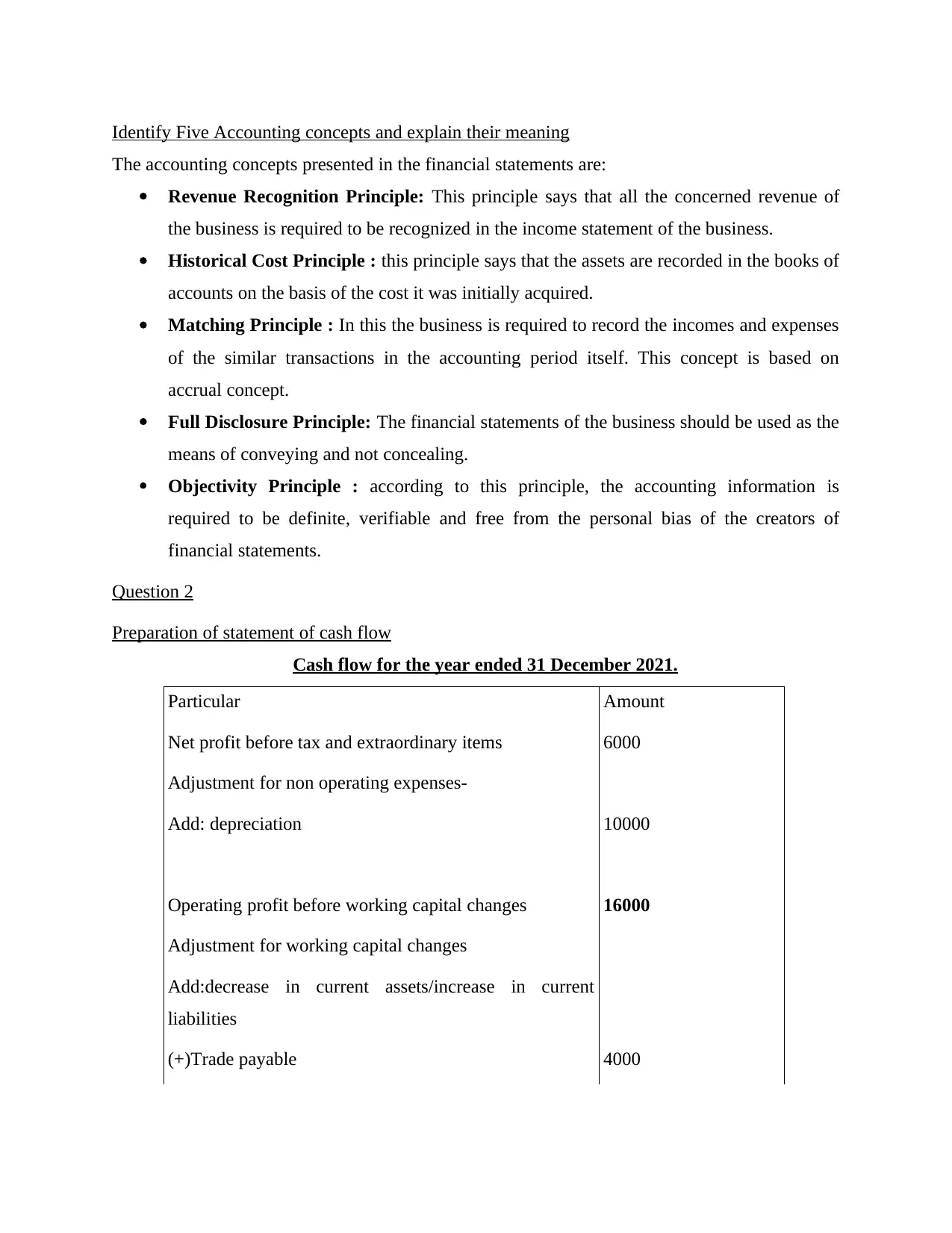

Identify Five Accounting concepts and explain their meaning

The accounting concepts presented in the financial statements are:

Revenue Recognition Principle: This principle says that all the concerned revenue of

the business is required to be recognized in the income statement of the business.

Historical Cost Principle : this principle says that the assets are recorded in the books of

accounts on the basis of the cost it was initially acquired.

Matching Principle : In this the business is required to record the incomes and expenses

of the similar transactions in the accounting period itself. This concept is based on

accrual concept.

Full Disclosure Principle: The financial statements of the business should be used as the

means of conveying and not concealing.

Objectivity Principle : according to this principle, the accounting information is

required to be definite, verifiable and free from the personal bias of the creators of

financial statements.

Question 2

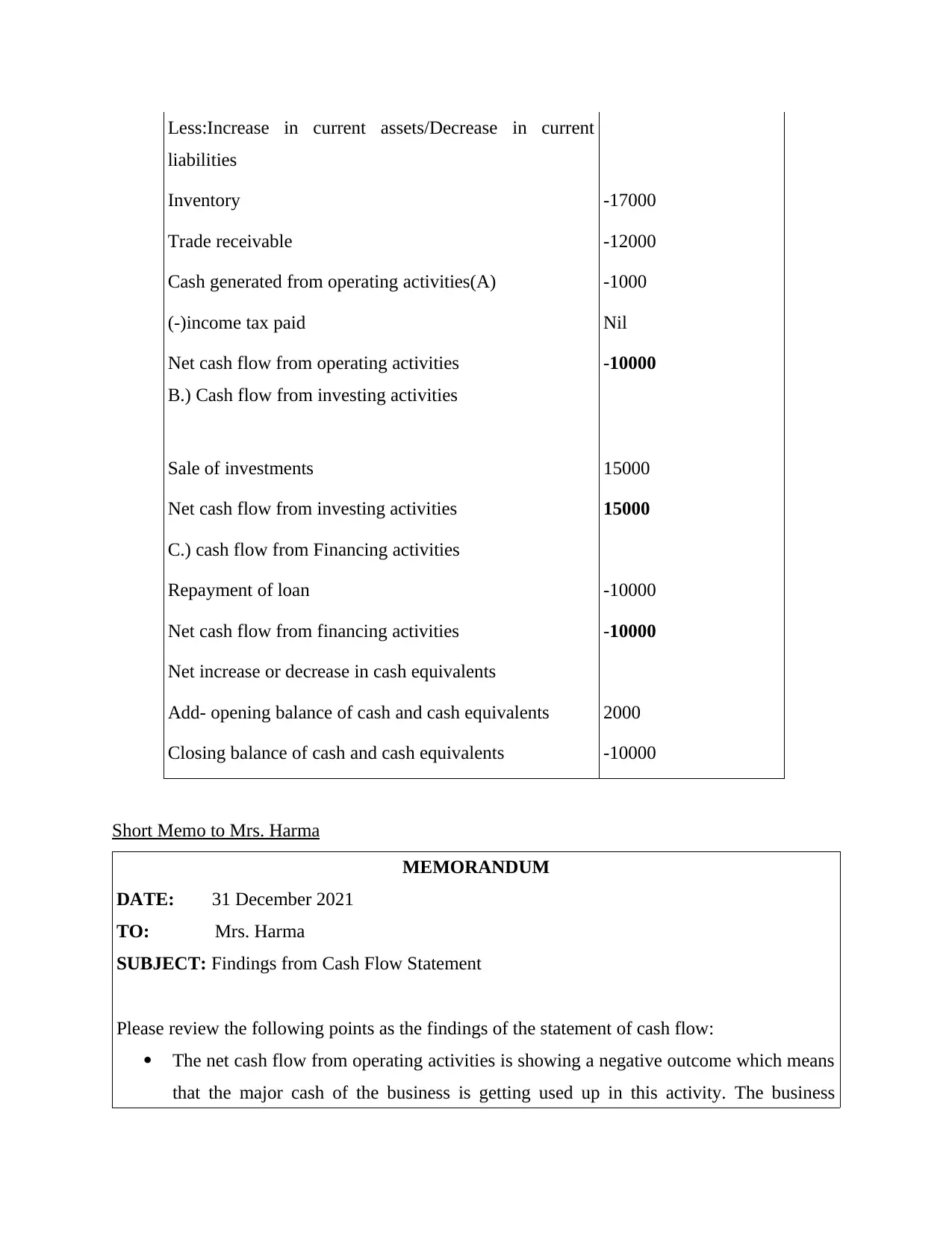

Preparation of statement of cash flow

Cash flow for the year ended 31 December 2021.

Particular Amount

Net profit before tax and extraordinary items 6000

Adjustment for non operating expenses-

Add: depreciation 10000

Operating profit before working capital changes 16000

Adjustment for working capital changes

Add:decrease in current assets/increase in current

liabilities

(+)Trade payable 4000

The accounting concepts presented in the financial statements are:

Revenue Recognition Principle: This principle says that all the concerned revenue of

the business is required to be recognized in the income statement of the business.

Historical Cost Principle : this principle says that the assets are recorded in the books of

accounts on the basis of the cost it was initially acquired.

Matching Principle : In this the business is required to record the incomes and expenses

of the similar transactions in the accounting period itself. This concept is based on

accrual concept.

Full Disclosure Principle: The financial statements of the business should be used as the

means of conveying and not concealing.

Objectivity Principle : according to this principle, the accounting information is

required to be definite, verifiable and free from the personal bias of the creators of

financial statements.

Question 2

Preparation of statement of cash flow

Cash flow for the year ended 31 December 2021.

Particular Amount

Net profit before tax and extraordinary items 6000

Adjustment for non operating expenses-

Add: depreciation 10000

Operating profit before working capital changes 16000

Adjustment for working capital changes

Add:decrease in current assets/increase in current

liabilities

(+)Trade payable 4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less:Increase in current assets/Decrease in current

liabilities

Inventory -17000

Trade receivable -12000

Cash generated from operating activities(A) -1000

(-)income tax paid Nil

Net cash flow from operating activities

B.) Cash flow from investing activities

-10000

Sale of investments 15000

Net cash flow from investing activities 15000

C.) cash flow from Financing activities

Repayment of loan -10000

Net cash flow from financing activities -10000

Net increase or decrease in cash equivalents

Add- opening balance of cash and cash equivalents 2000

Closing balance of cash and cash equivalents -10000

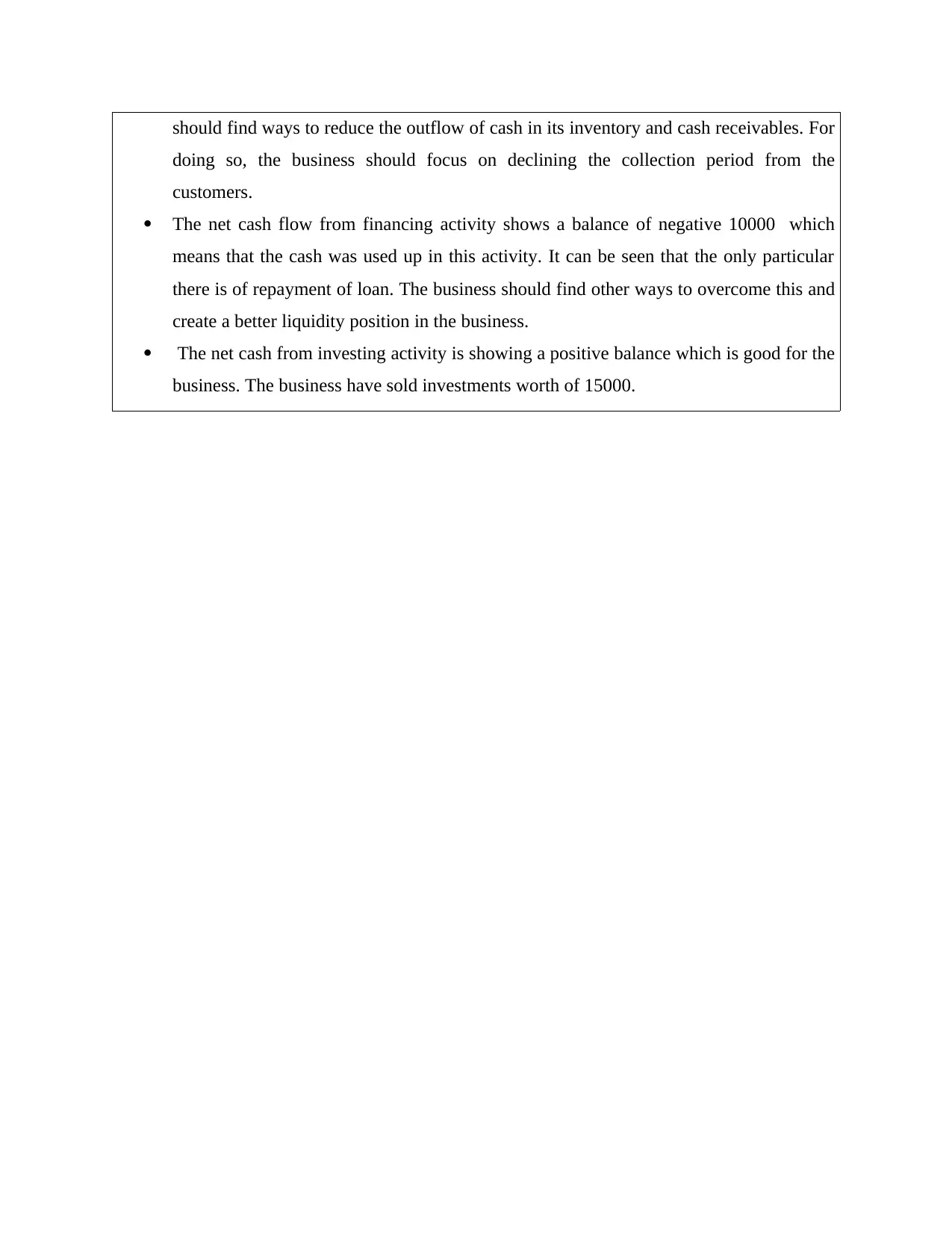

Short Memo to Mrs. Harma

MEMORANDUM

DATE: 31 December 2021

TO: Mrs. Harma

SUBJECT: Findings from Cash Flow Statement

Please review the following points as the findings of the statement of cash flow:

The net cash flow from operating activities is showing a negative outcome which means

that the major cash of the business is getting used up in this activity. The business

liabilities

Inventory -17000

Trade receivable -12000

Cash generated from operating activities(A) -1000

(-)income tax paid Nil

Net cash flow from operating activities

B.) Cash flow from investing activities

-10000

Sale of investments 15000

Net cash flow from investing activities 15000

C.) cash flow from Financing activities

Repayment of loan -10000

Net cash flow from financing activities -10000

Net increase or decrease in cash equivalents

Add- opening balance of cash and cash equivalents 2000

Closing balance of cash and cash equivalents -10000

Short Memo to Mrs. Harma

MEMORANDUM

DATE: 31 December 2021

TO: Mrs. Harma

SUBJECT: Findings from Cash Flow Statement

Please review the following points as the findings of the statement of cash flow:

The net cash flow from operating activities is showing a negative outcome which means

that the major cash of the business is getting used up in this activity. The business

should find ways to reduce the outflow of cash in its inventory and cash receivables. For

doing so, the business should focus on declining the collection period from the

customers.

The net cash flow from financing activity shows a balance of negative 10000 which

means that the cash was used up in this activity. It can be seen that the only particular

there is of repayment of loan. The business should find other ways to overcome this and

create a better liquidity position in the business.

The net cash from investing activity is showing a positive balance which is good for the

business. The business have sold investments worth of 15000.

doing so, the business should focus on declining the collection period from the

customers.

The net cash flow from financing activity shows a balance of negative 10000 which

means that the cash was used up in this activity. It can be seen that the only particular

there is of repayment of loan. The business should find other ways to overcome this and

create a better liquidity position in the business.

The net cash from investing activity is showing a positive balance which is good for the

business. The business have sold investments worth of 15000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.