Financial Aspects for Marketing, Events & Tourism: Investment Analysis

VerifiedAdded on 2022/07/21

|8

|2022

|21

Report

AI Summary

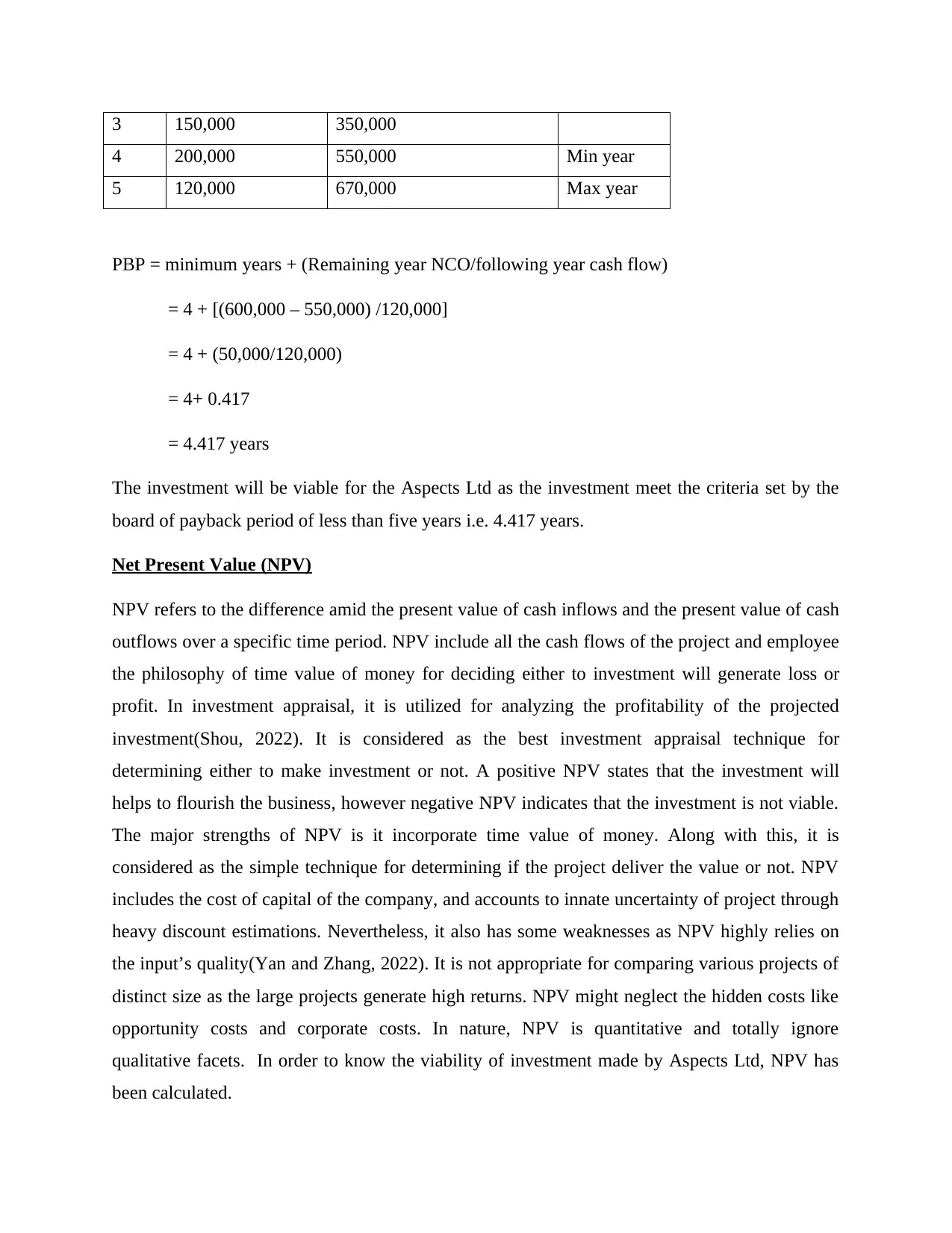

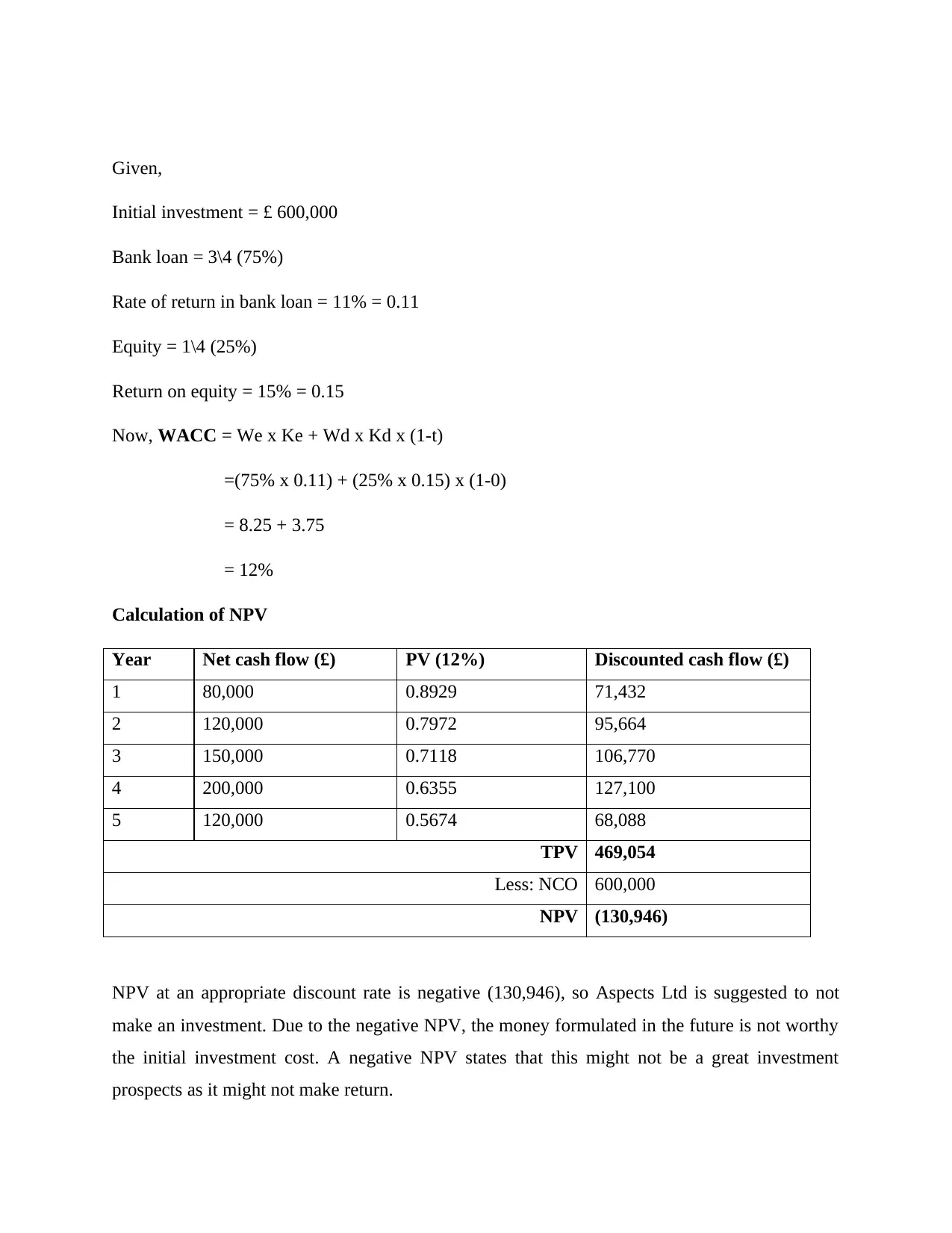

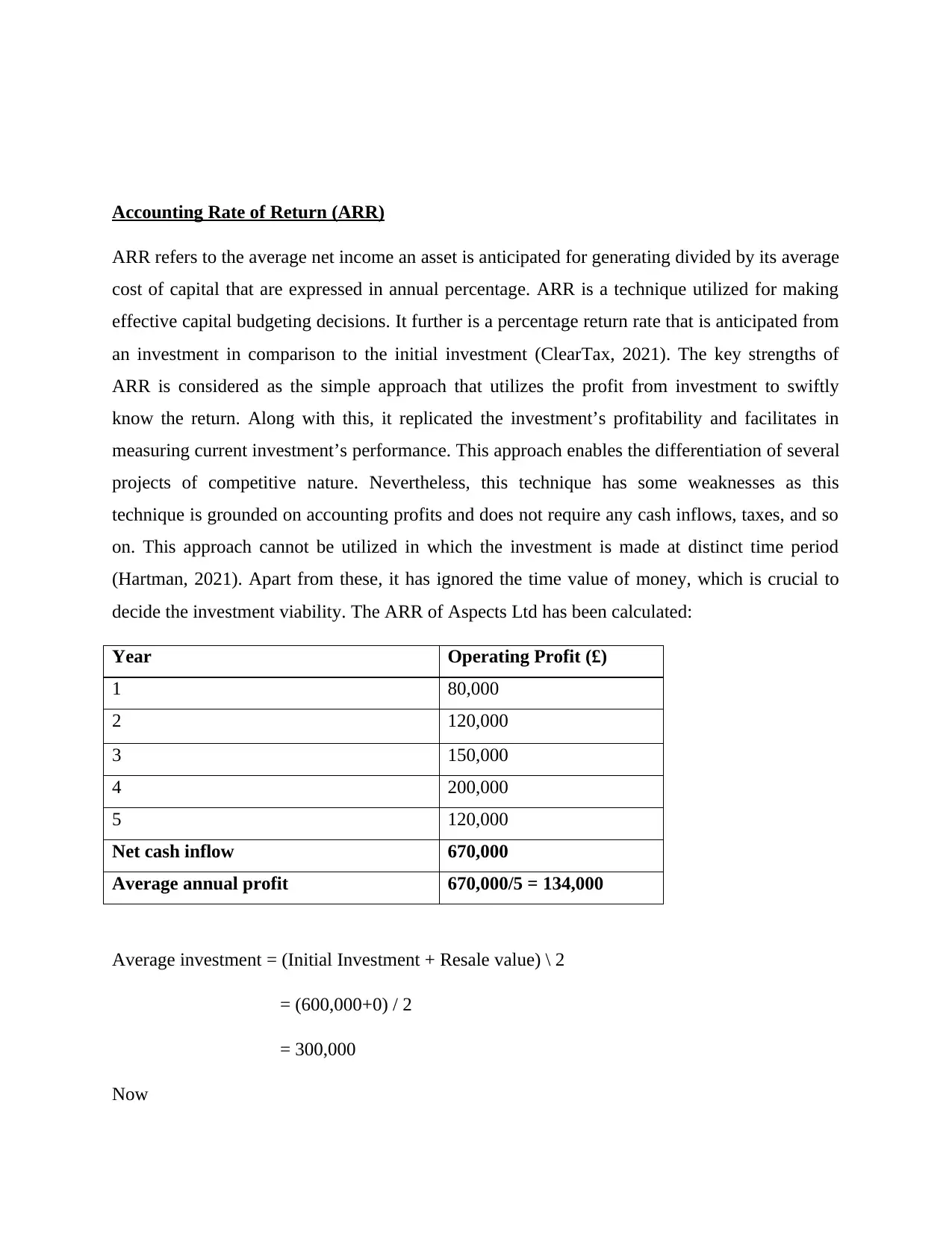

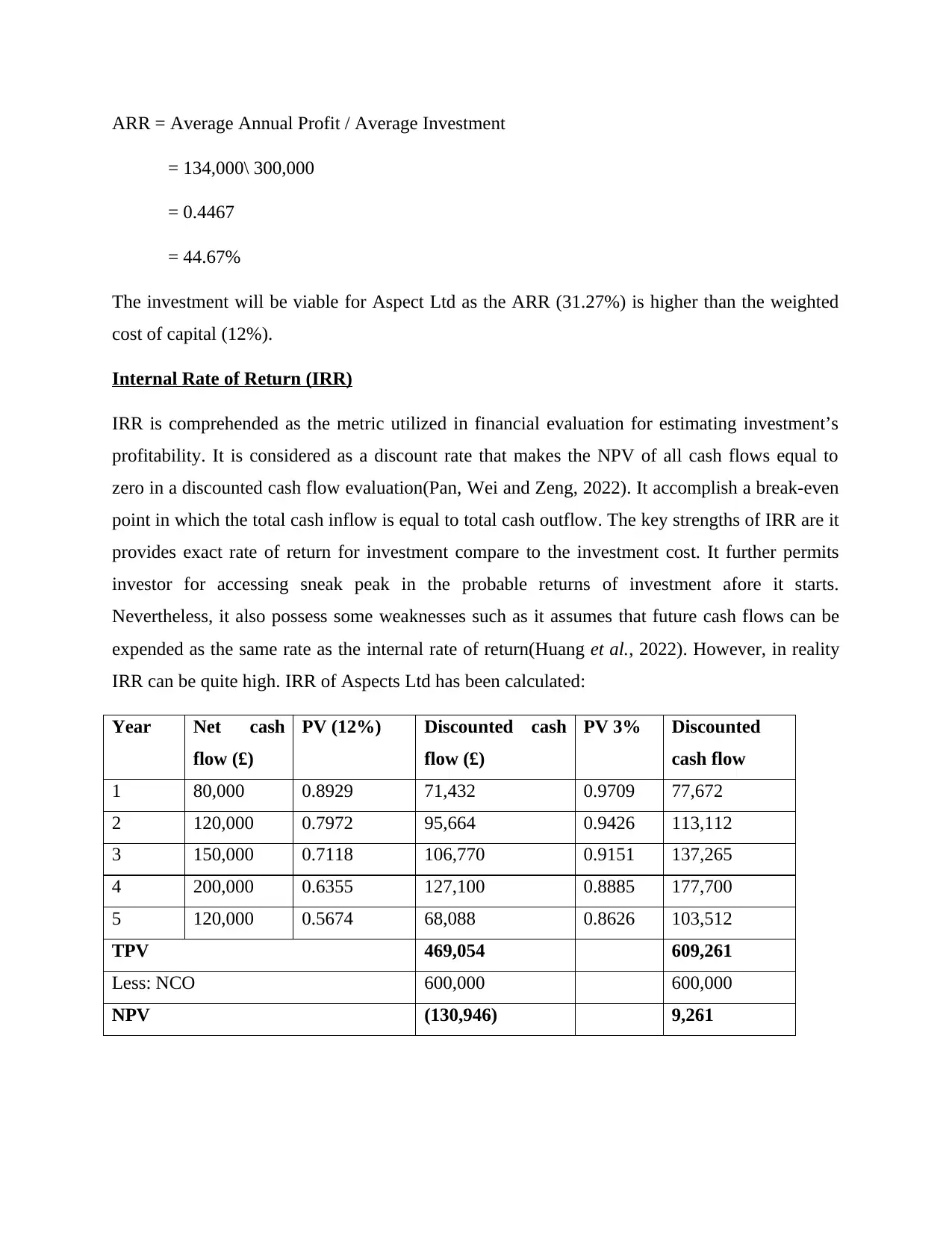

This report provides a detailed investment appraisal analysis for Aspect Ltd, evaluating the financial viability of a potential investment using several key methods. The analysis includes the calculation and interpretation of the payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). The report assesses each method's strengths and weaknesses, providing a comprehensive understanding of the investment's potential. The payback period is calculated to determine the time required to recover the initial investment, while ARR assesses the average profitability. NPV and IRR are used to evaluate the project's profitability considering the time value of money. The report concludes with a recommendation based on the findings, suggesting whether Aspect Ltd should proceed with the investment. The analysis highlights the importance of considering both short-term and long-term financial implications, providing valuable insights for informed decision-making.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.