HI6028 T3 2019: Accounting and Taxation - Assessable Income Analysis

VerifiedAdded on 2023/01/13

|11

|2729

|83

Homework Assignment

AI Summary

This accounting assignment analyzes the assessable income of an accounting student, Emmi, working part-time, considering various income sources like tips, employment income, and gifts, and calculating her total assessable income and tax liability. It also addresses the capital gains tax consequences for Liu, a retiring resident selling assets, including a residential house, car, small business (including goodwill and equipment), and other assets. The assignment references relevant legislation, including ITAA 1936 and ITAA 1997, and explores exemptions, deductions, and the application of capital gains tax to various asset sales, providing a comprehensive overview of Australian taxation principles.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A) Tips from customers...............................................................................................................1

b) Income from employment.......................................................................................................2

c) Perfume from customer on Christmas.....................................................................................2

d) Payment of meals by the employer..........................................................................................2

e) Gift of money from parents.....................................................................................................3

Assessable Income of Emmi for the year. ..................................................................................3

QUESTION 2 ..................................................................................................................................4

a) Sale of residential house..........................................................................................................5

b) Sale of Car ..............................................................................................................................6

c) Sale of small business .............................................................................................................6

d) Sale of furniture ......................................................................................................................7

e) Sale of paintings .....................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A) Tips from customers...............................................................................................................1

b) Income from employment.......................................................................................................2

c) Perfume from customer on Christmas.....................................................................................2

d) Payment of meals by the employer..........................................................................................2

e) Gift of money from parents.....................................................................................................3

Assessable Income of Emmi for the year. ..................................................................................3

QUESTION 2 ..................................................................................................................................4

a) Sale of residential house..........................................................................................................5

b) Sale of Car ..............................................................................................................................6

c) Sale of small business .............................................................................................................6

d) Sale of furniture ......................................................................................................................7

e) Sale of paintings .....................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Taxation system of Australia can be said as among the complex systems of tax in the

countries. Australian taxation system consists of more variety of taxes including taxes like tax on

capital gain, fringe benefits, income tax and goods and service tax. The integrity of tax system is

maintained by number of organisation who are playing different roles in the system, ensuring

that all the Australian are treated with equality. Every individual resident of Australian is

required to pay income tax on the income earned during the year. Present report is based on the

income earned by an student by working with studies. It swill also analyse the tax consequences

on the capital gains from sale of assets. Taxation system also provides for the deductions and

exemptions for various incomes on fulfilling certain conditions. Study will provide

understanding about the taxation system of Australia.

QUESTION 1

Australian as per OECD who analyse tax burdens of around 35 countries, Australians pay

more tax as compared with other nations. At the same time benefits are also highest in he

country. Income tax is most significant revenue generating stream of Australian taxation system

and it is required to be paid over all the forms of income. Tax is paid mainly over three sources

of income that are business earnings, personal earnings and capital gains. Income includes salary

from employment, profits from running business & returns over investments (Australian Income

Tax, 2019). It also includes the benefits on sale of capital assets.

In this question Emmi is an accounts students who works part time in Crown Melbourne

Restaurant. During her working tenure she has earned various incomes and gifts. Emmi wants to

know her assessable income for the year after claiming all the deductions and exemptions that

are available.

A) Tips from customers

Para 26(e) of ITAA 1936 provides that all the tips receive by employees working in

hotels and restaurants will form part of their assessable income. ATO has stated in its guidelines

that when an employee receives any tips directly form the customers or is transferred by

employer without deducting tax it will be reported in the income tax return of individual. As per

1

Taxation system of Australia can be said as among the complex systems of tax in the

countries. Australian taxation system consists of more variety of taxes including taxes like tax on

capital gain, fringe benefits, income tax and goods and service tax. The integrity of tax system is

maintained by number of organisation who are playing different roles in the system, ensuring

that all the Australian are treated with equality. Every individual resident of Australian is

required to pay income tax on the income earned during the year. Present report is based on the

income earned by an student by working with studies. It swill also analyse the tax consequences

on the capital gains from sale of assets. Taxation system also provides for the deductions and

exemptions for various incomes on fulfilling certain conditions. Study will provide

understanding about the taxation system of Australia.

QUESTION 1

Australian as per OECD who analyse tax burdens of around 35 countries, Australians pay

more tax as compared with other nations. At the same time benefits are also highest in he

country. Income tax is most significant revenue generating stream of Australian taxation system

and it is required to be paid over all the forms of income. Tax is paid mainly over three sources

of income that are business earnings, personal earnings and capital gains. Income includes salary

from employment, profits from running business & returns over investments (Australian Income

Tax, 2019). It also includes the benefits on sale of capital assets.

In this question Emmi is an accounts students who works part time in Crown Melbourne

Restaurant. During her working tenure she has earned various incomes and gifts. Emmi wants to

know her assessable income for the year after claiming all the deductions and exemptions that

are available.

A) Tips from customers

Para 26(e) of ITAA 1936 provides that all the tips receive by employees working in

hotels and restaurants will form part of their assessable income. ATO has stated in its guidelines

that when an employee receives any tips directly form the customers or is transferred by

employer without deducting tax it will be reported in the income tax return of individual. As per

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the above guidelines given by taxation office it is clear that the tips received by Emmi directly

from customers will form part of her assessable income.

b) Income from employment

Every individual is required to pay tax over the income received from employment.

Though government grants exemption to the individual from payment of taxes if income earned

is below the threshold limit of $18200. Section 15 of ITAA 1997 states that income from

employment of an individual is taxable. Individual may be receiving various income from her

employment that are assessable but the tax law provides deductions for income employment

allowance and fringe benefits. In the present case Emmi is only receiving salary from working at

restaurant therefore the salary income of whole $ 25000 is taxable under the income tax (Sadiq,

2019). She will be available with deduction of zero tax upto the income of $ 18200. If she had

been working at more than one office she was required to pay tax over all the income received

during the year from all the employment.

c) Perfume from customer on Christmas

Tax law ITAA 1997 states that gifts received by employee are not taxable. The gifts

above the threshold limit of $ 10000 are taxable to the individual, however gifts given on special

occasion are exempt and are not required to be disclosed in the tax returns. Also the gift of

perfume is not related to any business activity of or in relation to income earning activity. Emmi

received perfume worth $250 from an customer on an special occasion of Christmas as present

or gift. This is below the threshold limit and also not related to business or employment related

activities. Emmi gifted the same perfume to her mother. No deductions is available for the gift to

her mother. It is not required to be reported in the tax return of Emmi as it is exempt in her

hands. Deductions are available for charity and not for gift to family member.

d) Payment of meals by the employer

Tax law provides that the entertainment charges paid by the employer for employee

amounts to fringe benefits. Tax law provides for separate tax department for taxing of fringe

benefits received from employer. Section 32 of ITAA' 97 provides that fringe benefits means

benefits which are received from the employer after their salary (Hobson, 2019). It is the benefit

that employer provides to its employees in addition to their salary. Australian taxation office

2

from customers will form part of her assessable income.

b) Income from employment

Every individual is required to pay tax over the income received from employment.

Though government grants exemption to the individual from payment of taxes if income earned

is below the threshold limit of $18200. Section 15 of ITAA 1997 states that income from

employment of an individual is taxable. Individual may be receiving various income from her

employment that are assessable but the tax law provides deductions for income employment

allowance and fringe benefits. In the present case Emmi is only receiving salary from working at

restaurant therefore the salary income of whole $ 25000 is taxable under the income tax (Sadiq,

2019). She will be available with deduction of zero tax upto the income of $ 18200. If she had

been working at more than one office she was required to pay tax over all the income received

during the year from all the employment.

c) Perfume from customer on Christmas

Tax law ITAA 1997 states that gifts received by employee are not taxable. The gifts

above the threshold limit of $ 10000 are taxable to the individual, however gifts given on special

occasion are exempt and are not required to be disclosed in the tax returns. Also the gift of

perfume is not related to any business activity of or in relation to income earning activity. Emmi

received perfume worth $250 from an customer on an special occasion of Christmas as present

or gift. This is below the threshold limit and also not related to business or employment related

activities. Emmi gifted the same perfume to her mother. No deductions is available for the gift to

her mother. It is not required to be reported in the tax return of Emmi as it is exempt in her

hands. Deductions are available for charity and not for gift to family member.

d) Payment of meals by the employer

Tax law provides that the entertainment charges paid by the employer for employee

amounts to fringe benefits. Tax law provides for separate tax department for taxing of fringe

benefits received from employer. Section 32 of ITAA' 97 provides that fringe benefits means

benefits which are received from the employer after their salary (Hobson, 2019). It is the benefit

that employer provides to its employees in addition to their salary. Australian taxation office

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

states that individual is not required to state the benefits in tax return if they are below $ 2000.

This means if the fringe benefits exceeds $ 2000 it is required to be reported in tax returns of the

year. Fringe benefits are taxed separately under Fringe Benefits Tax Assessment Act, 1986.

Payment of meals by employer amounted to $ 385, and it is not taxable as per guideline of tax

law.

e) Gift of money from parents

Australian Taxation law provides that giving money as gift top parents is not an taxable

event. Tax is to be deducted over the income received form sale of monetary gifts. Money

received by individual from parents on special occasion is not taxable. Provided that money is

paid out of love and affection and is not having connection with the income generating activities

of the individual. The law provides that gifts above the limit of $10000 are taxable. Since the

money is given on special occasion of Christmas out of love and affection it is not chargeable for

tax. Monetary gift of $1500 by her father is exempt in the hands of Emmi and also not required

to be declared in her tax returns.

Assessable Income of Emmi for the year.

Assessable income is defined as the income on which tax is to be paid by the individual.

Assessable income is calculated by adding all the income earned by an individual during the

year. It includes income from employment, tips from customers, allowances, bank interests and

many more which brings benefit in monetary terms (Assessable Income, 2019). Individuals can

claim the allowable deductions over their assessable income for reducing the taxable income on

which tax is actually calculated. Tax liability can be reduced through the deductions (Maley and

Maley, 2018). Deductions are not used for reducing the tax liability but for reducing the taxable

income.

Assessable income of Emmi for the year is $25335 from salary and tips from customers

since she is not having any deductions, assessable income will be the taxable and tax will be

calculated over the same. Tax liability is $2216 and the medicare levy of 380.25, aggregating

total income tax payable of $2596.37. The tax liability and assessable income has been

calculated as per the guidelines provided by Australian taxation office in accordance with ITAA,

1936 and ITAA 1997.

3

This means if the fringe benefits exceeds $ 2000 it is required to be reported in tax returns of the

year. Fringe benefits are taxed separately under Fringe Benefits Tax Assessment Act, 1986.

Payment of meals by employer amounted to $ 385, and it is not taxable as per guideline of tax

law.

e) Gift of money from parents

Australian Taxation law provides that giving money as gift top parents is not an taxable

event. Tax is to be deducted over the income received form sale of monetary gifts. Money

received by individual from parents on special occasion is not taxable. Provided that money is

paid out of love and affection and is not having connection with the income generating activities

of the individual. The law provides that gifts above the limit of $10000 are taxable. Since the

money is given on special occasion of Christmas out of love and affection it is not chargeable for

tax. Monetary gift of $1500 by her father is exempt in the hands of Emmi and also not required

to be declared in her tax returns.

Assessable Income of Emmi for the year.

Assessable income is defined as the income on which tax is to be paid by the individual.

Assessable income is calculated by adding all the income earned by an individual during the

year. It includes income from employment, tips from customers, allowances, bank interests and

many more which brings benefit in monetary terms (Assessable Income, 2019). Individuals can

claim the allowable deductions over their assessable income for reducing the taxable income on

which tax is actually calculated. Tax liability can be reduced through the deductions (Maley and

Maley, 2018). Deductions are not used for reducing the tax liability but for reducing the taxable

income.

Assessable income of Emmi for the year is $25335 from salary and tips from customers

since she is not having any deductions, assessable income will be the taxable and tax will be

calculated over the same. Tax liability is $2216 and the medicare levy of 380.25, aggregating

total income tax payable of $2596.37. The tax liability and assessable income has been

calculated as per the guidelines provided by Australian taxation office in accordance with ITAA,

1936 and ITAA 1997.

3

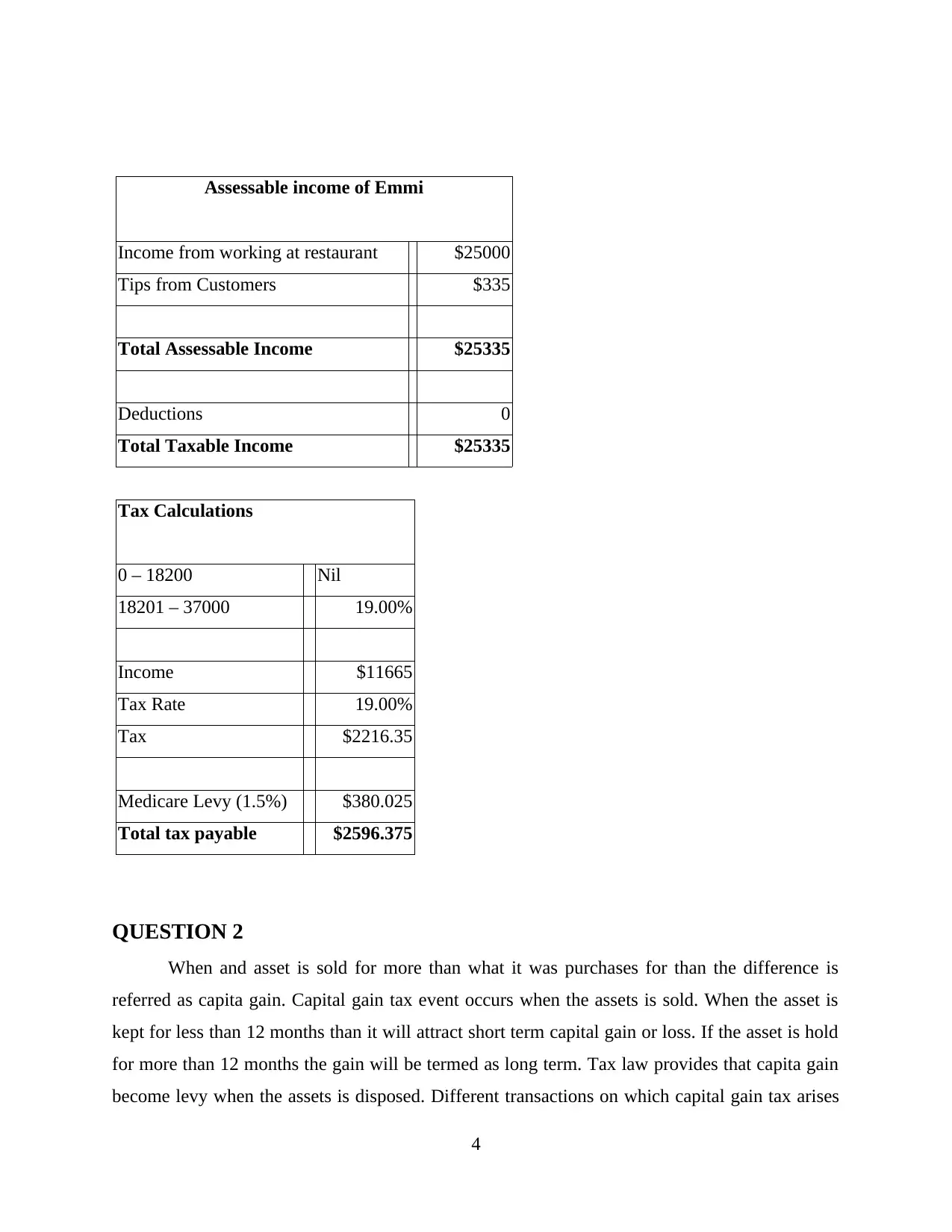

Assessable income of Emmi

Income from working at restaurant $25000

Tips from Customers $335

Total Assessable Income $25335

Deductions 0

Total Taxable Income $25335

Tax Calculations

0 – 18200 Nil

18201 – 37000 19.00%

Income $11665

Tax Rate 19.00%

Tax $2216.35

Medicare Levy (1.5%) $380.025

Total tax payable $2596.375

QUESTION 2

When and asset is sold for more than what it was purchases for than the difference is

referred as capita gain. Capital gain tax event occurs when the assets is sold. When the asset is

kept for less than 12 months than it will attract short term capital gain or loss. If the asset is hold

for more than 12 months the gain will be termed as long term. Tax law provides that capita gain

become levy when the assets is disposed. Different transactions on which capital gain tax arises

4

Income from working at restaurant $25000

Tips from Customers $335

Total Assessable Income $25335

Deductions 0

Total Taxable Income $25335

Tax Calculations

0 – 18200 Nil

18201 – 37000 19.00%

Income $11665

Tax Rate 19.00%

Tax $2216.35

Medicare Levy (1.5%) $380.025

Total tax payable $2596.375

QUESTION 2

When and asset is sold for more than what it was purchases for than the difference is

referred as capita gain. Capital gain tax event occurs when the assets is sold. When the asset is

kept for less than 12 months than it will attract short term capital gain or loss. If the asset is hold

for more than 12 months the gain will be termed as long term. Tax law provides that capita gain

become levy when the assets is disposed. Different transactions on which capital gain tax arises

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

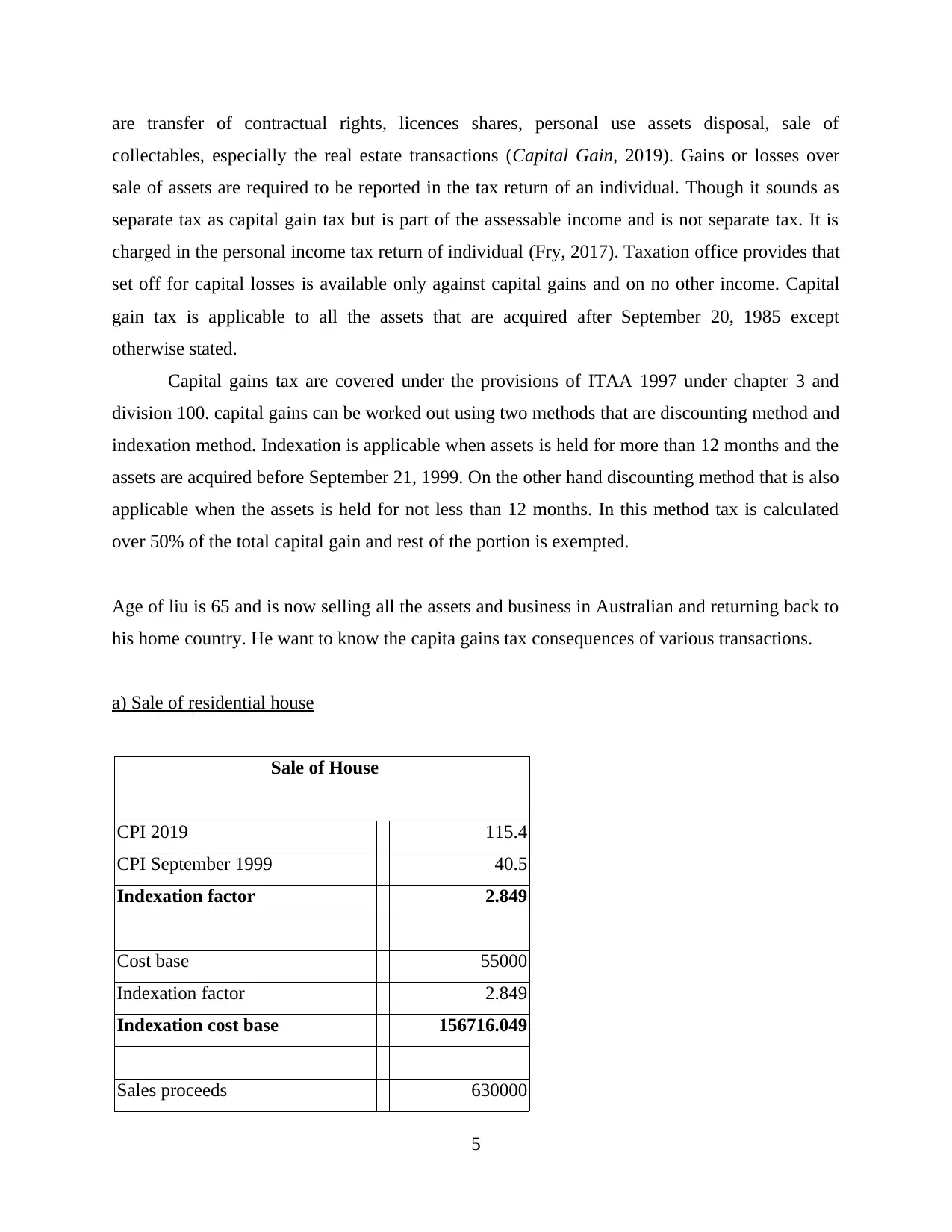

are transfer of contractual rights, licences shares, personal use assets disposal, sale of

collectables, especially the real estate transactions (Capital Gain, 2019). Gains or losses over

sale of assets are required to be reported in the tax return of an individual. Though it sounds as

separate tax as capital gain tax but is part of the assessable income and is not separate tax. It is

charged in the personal income tax return of individual (Fry, 2017). Taxation office provides that

set off for capital losses is available only against capital gains and on no other income. Capital

gain tax is applicable to all the assets that are acquired after September 20, 1985 except

otherwise stated.

Capital gains tax are covered under the provisions of ITAA 1997 under chapter 3 and

division 100. capital gains can be worked out using two methods that are discounting method and

indexation method. Indexation is applicable when assets is held for more than 12 months and the

assets are acquired before September 21, 1999. On the other hand discounting method that is also

applicable when the assets is held for not less than 12 months. In this method tax is calculated

over 50% of the total capital gain and rest of the portion is exempted.

Age of liu is 65 and is now selling all the assets and business in Australian and returning back to

his home country. He want to know the capita gains tax consequences of various transactions.

a) Sale of residential house

Sale of House

CPI 2019 115.4

CPI September 1999 40.5

Indexation factor 2.849

Cost base 55000

Indexation factor 2.849

Indexation cost base 156716.049

Sales proceeds 630000

5

collectables, especially the real estate transactions (Capital Gain, 2019). Gains or losses over

sale of assets are required to be reported in the tax return of an individual. Though it sounds as

separate tax as capital gain tax but is part of the assessable income and is not separate tax. It is

charged in the personal income tax return of individual (Fry, 2017). Taxation office provides that

set off for capital losses is available only against capital gains and on no other income. Capital

gain tax is applicable to all the assets that are acquired after September 20, 1985 except

otherwise stated.

Capital gains tax are covered under the provisions of ITAA 1997 under chapter 3 and

division 100. capital gains can be worked out using two methods that are discounting method and

indexation method. Indexation is applicable when assets is held for more than 12 months and the

assets are acquired before September 21, 1999. On the other hand discounting method that is also

applicable when the assets is held for not less than 12 months. In this method tax is calculated

over 50% of the total capital gain and rest of the portion is exempted.

Age of liu is 65 and is now selling all the assets and business in Australian and returning back to

his home country. He want to know the capita gains tax consequences of various transactions.

a) Sale of residential house

Sale of House

CPI 2019 115.4

CPI September 1999 40.5

Indexation factor 2.849

Cost base 55000

Indexation factor 2.849

Indexation cost base 156716.049

Sales proceeds 630000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

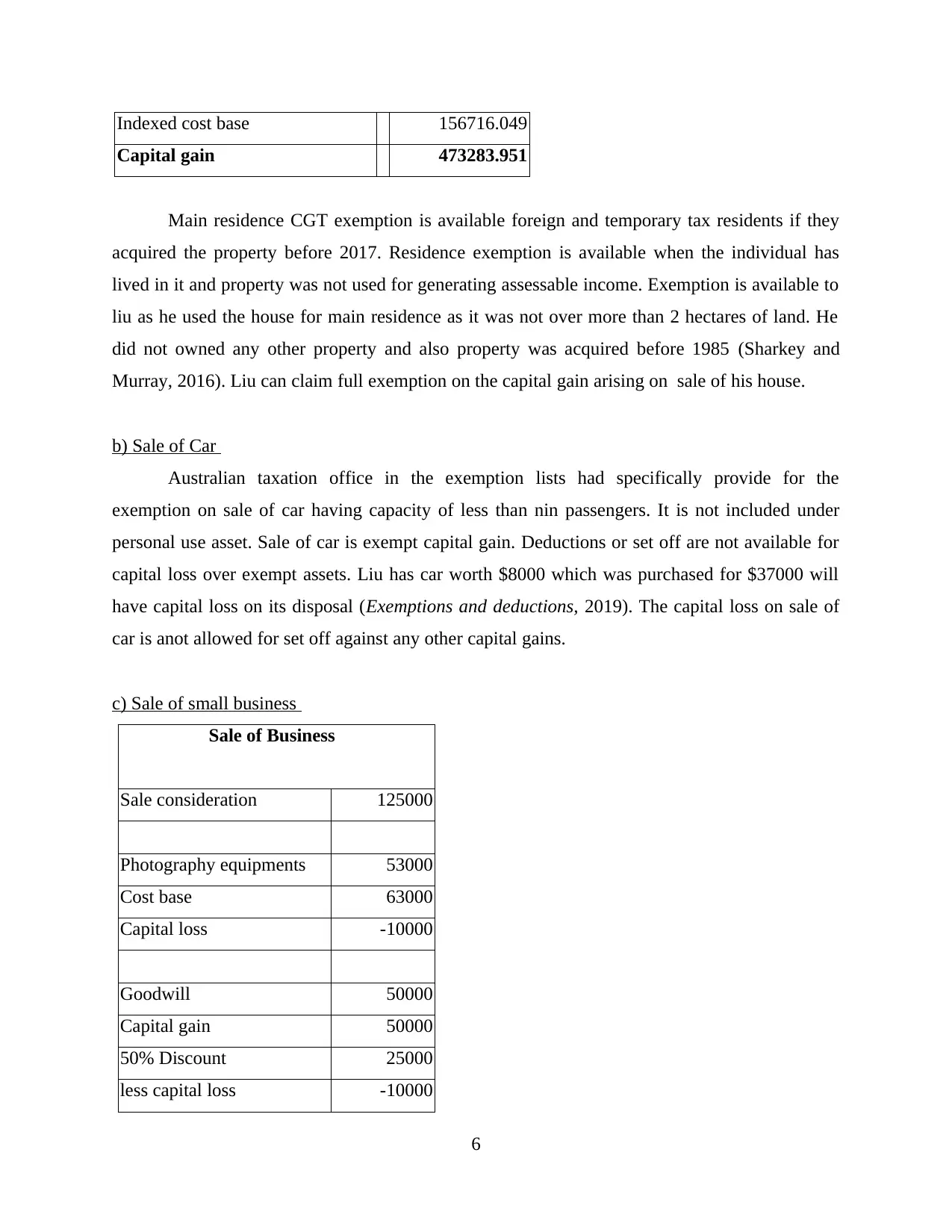

Indexed cost base 156716.049

Capital gain 473283.951

Main residence CGT exemption is available foreign and temporary tax residents if they

acquired the property before 2017. Residence exemption is available when the individual has

lived in it and property was not used for generating assessable income. Exemption is available to

liu as he used the house for main residence as it was not over more than 2 hectares of land. He

did not owned any other property and also property was acquired before 1985 (Sharkey and

Murray, 2016). Liu can claim full exemption on the capital gain arising on sale of his house.

b) Sale of Car

Australian taxation office in the exemption lists had specifically provide for the

exemption on sale of car having capacity of less than nin passengers. It is not included under

personal use asset. Sale of car is exempt capital gain. Deductions or set off are not available for

capital loss over exempt assets. Liu has car worth $8000 which was purchased for $37000 will

have capital loss on its disposal (Exemptions and deductions, 2019). The capital loss on sale of

car is anot allowed for set off against any other capital gains.

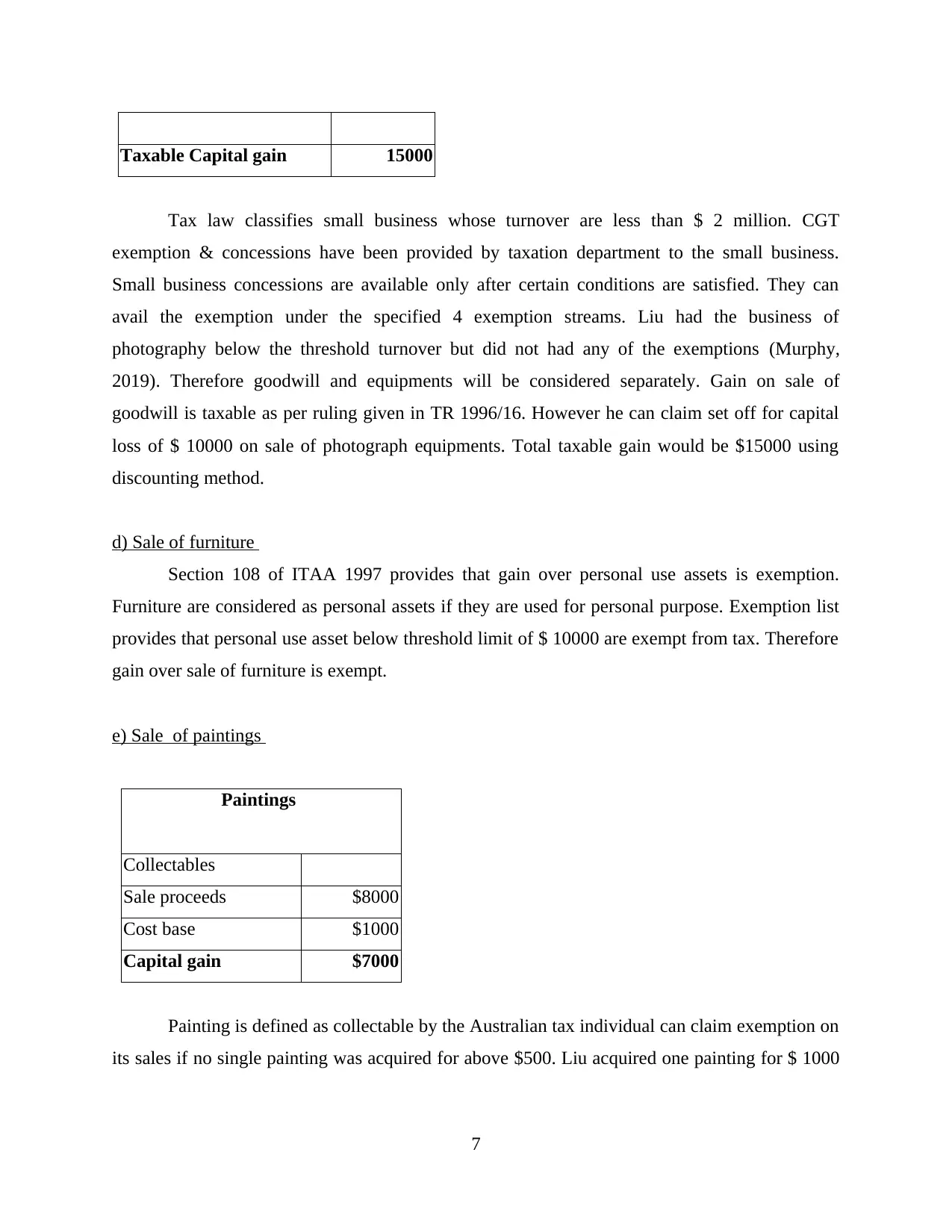

c) Sale of small business

Sale of Business

Sale consideration 125000

Photography equipments 53000

Cost base 63000

Capital loss -10000

Goodwill 50000

Capital gain 50000

50% Discount 25000

less capital loss -10000

6

Capital gain 473283.951

Main residence CGT exemption is available foreign and temporary tax residents if they

acquired the property before 2017. Residence exemption is available when the individual has

lived in it and property was not used for generating assessable income. Exemption is available to

liu as he used the house for main residence as it was not over more than 2 hectares of land. He

did not owned any other property and also property was acquired before 1985 (Sharkey and

Murray, 2016). Liu can claim full exemption on the capital gain arising on sale of his house.

b) Sale of Car

Australian taxation office in the exemption lists had specifically provide for the

exemption on sale of car having capacity of less than nin passengers. It is not included under

personal use asset. Sale of car is exempt capital gain. Deductions or set off are not available for

capital loss over exempt assets. Liu has car worth $8000 which was purchased for $37000 will

have capital loss on its disposal (Exemptions and deductions, 2019). The capital loss on sale of

car is anot allowed for set off against any other capital gains.

c) Sale of small business

Sale of Business

Sale consideration 125000

Photography equipments 53000

Cost base 63000

Capital loss -10000

Goodwill 50000

Capital gain 50000

50% Discount 25000

less capital loss -10000

6

Taxable Capital gain 15000

Tax law classifies small business whose turnover are less than $ 2 million. CGT

exemption & concessions have been provided by taxation department to the small business.

Small business concessions are available only after certain conditions are satisfied. They can

avail the exemption under the specified 4 exemption streams. Liu had the business of

photography below the threshold turnover but did not had any of the exemptions (Murphy,

2019). Therefore goodwill and equipments will be considered separately. Gain on sale of

goodwill is taxable as per ruling given in TR 1996/16. However he can claim set off for capital

loss of $ 10000 on sale of photograph equipments. Total taxable gain would be $15000 using

discounting method.

d) Sale of furniture

Section 108 of ITAA 1997 provides that gain over personal use assets is exemption.

Furniture are considered as personal assets if they are used for personal purpose. Exemption list

provides that personal use asset below threshold limit of $ 10000 are exempt from tax. Therefore

gain over sale of furniture is exempt.

e) Sale of paintings

Paintings

Collectables

Sale proceeds $8000

Cost base $1000

Capital gain $7000

Painting is defined as collectable by the Australian tax individual can claim exemption on

its sales if no single painting was acquired for above $500. Liu acquired one painting for $ 1000

7

Tax law classifies small business whose turnover are less than $ 2 million. CGT

exemption & concessions have been provided by taxation department to the small business.

Small business concessions are available only after certain conditions are satisfied. They can

avail the exemption under the specified 4 exemption streams. Liu had the business of

photography below the threshold turnover but did not had any of the exemptions (Murphy,

2019). Therefore goodwill and equipments will be considered separately. Gain on sale of

goodwill is taxable as per ruling given in TR 1996/16. However he can claim set off for capital

loss of $ 10000 on sale of photograph equipments. Total taxable gain would be $15000 using

discounting method.

d) Sale of furniture

Section 108 of ITAA 1997 provides that gain over personal use assets is exemption.

Furniture are considered as personal assets if they are used for personal purpose. Exemption list

provides that personal use asset below threshold limit of $ 10000 are exempt from tax. Therefore

gain over sale of furniture is exempt.

e) Sale of paintings

Paintings

Collectables

Sale proceeds $8000

Cost base $1000

Capital gain $7000

Painting is defined as collectable by the Australian tax individual can claim exemption on

its sales if no single painting was acquired for above $500. Liu acquired one painting for $ 1000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and is sold at $ 8000 (Murphy, 2019). Capital gain arising on this painting is taxable while all

other paintings which are acquired for less than $500 are not taxable as they are exempt.

8

other paintings which are acquired for less than $500 are not taxable as they are exempt.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office. The APPEA Journal.57(1). pp.49-63.

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian Tax

Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The

Australian National University.

Lymer, A., 2019. Contemporary issues in taxation research. Routledge.

Maley, M.N. and Maley, D.M., 2018. Australian Taxation Office Guidance on the Diverted

Profits Tax.

Murphy, K., 2019. Moving towards a more effective model of regulatory enforcement in the

Australian Taxation Office. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Murphy, K., 2019. Procedural justice and the Australian Taxation Office: A study of scheme

investors. Centre for Tax System Integrity (CTSI), Research School of Social Sciences,

The Australian National University.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Sharkey, N. and Murray, I., 2016. Reinventing administrative leadership in Australian taxation:

beware the fine balance of social psychological and rule of law principles. Austl. Tax

F..31. p.63.

Online

Exemptions and deductions. 2019. [Online]. Available through :

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>.

Capital Gain. 2019. [Online]. Available through : <https://www.ato.gov.au/Individuals/Tax-

return/2019/Supplementary-tax-return/Income-questions-13-24/18-Capital-gains-2019/>.

Assessable Income. 2019. [Online]. Available through :

<https://www.ato.gov.au/non-profit/your-organisation/in-detail/income-tax/mutuality-

and-taxable-income/?page=13>.

Australian Income Tax. 2019. [Online]. Available through : <https://www.hrblock.com.au/tax-

tips/understanding-the-australian-income-tax-system>.

9

Books and Journals

Fry, M., 2017. Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office. The APPEA Journal.57(1). pp.49-63.

Hobson, K., 2019. 'Say no to the ATO': The cultural politics of protest against the Australian Tax

Office. Centre for Tax System Integrity (CTSI), Research School of Social Sciences, The

Australian National University.

Lymer, A., 2019. Contemporary issues in taxation research. Routledge.

Maley, M.N. and Maley, D.M., 2018. Australian Taxation Office Guidance on the Diverted

Profits Tax.

Murphy, K., 2019. Moving towards a more effective model of regulatory enforcement in the

Australian Taxation Office. Centre for Tax System Integrity (CTSI), Research School of

Social Sciences, The Australian National University.

Murphy, K., 2019. Procedural justice and the Australian Taxation Office: A study of scheme

investors. Centre for Tax System Integrity (CTSI), Research School of Social Sciences,

The Australian National University.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Sharkey, N. and Murray, I., 2016. Reinventing administrative leadership in Australian taxation:

beware the fine balance of social psychological and rule of law principles. Austl. Tax

F..31. p.63.

Online

Exemptions and deductions. 2019. [Online]. Available through :

<https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/>.

Capital Gain. 2019. [Online]. Available through : <https://www.ato.gov.au/Individuals/Tax-

return/2019/Supplementary-tax-return/Income-questions-13-24/18-Capital-gains-2019/>.

Assessable Income. 2019. [Online]. Available through :

<https://www.ato.gov.au/non-profit/your-organisation/in-detail/income-tax/mutuality-

and-taxable-income/?page=13>.

Australian Income Tax. 2019. [Online]. Available through : <https://www.hrblock.com.au/tax-

tips/understanding-the-australian-income-tax-system>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.