SBM3201 Management Accounting: Assessment 3 Finance Report

VerifiedAdded on 2022/09/26

|16

|3245

|18

Report

AI Summary

This report presents a detailed analysis of Tinka Tokyo Truck Manufacturing Co.'s financial performance, including cost of goods manufactured, cost of goods sold, and income statements. The report calculates and interprets key financial metrics, such as gross profit and net income, providing insights into the company's efficiency and profitability. It examines direct and indirect costs, analyzing manufacturing overheads, direct labor, and raw materials. The analysis further explores the company's inventory management, identifying areas for improvement like Work-In-Progress. The report also differentiates between manufacturing and production costs and provides recommendations for enhancing operational efficiency and profitability, including reducing batch sizes and improving administrative charges. The analysis also considers the impact of income taxes on the company's net income and concludes that the company has been profitable overall and needs to be continued in the way it has been doing.

Running head: ASSESSMENT 3

Assessment 3

Name of the Student

Name of the University

Author Note

Assessment 3

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ASSESSMENT 3

Table of Contents

Answer to Question 1......................................................................................................................2

a. Cost of Goods Manufactured Statement...............................................................................2

b. Cost of Goods Sold Statement..............................................................................................3

c. Income Statement.................................................................................................................4

Analysis........................................................................................................................................5

Answer to Question 2......................................................................................................................8

References..................................................................................................................................12

Table of Contents

Answer to Question 1......................................................................................................................2

a. Cost of Goods Manufactured Statement...............................................................................2

b. Cost of Goods Sold Statement..............................................................................................3

c. Income Statement.................................................................................................................4

Analysis........................................................................................................................................5

Answer to Question 2......................................................................................................................8

References..................................................................................................................................12

2ASSESSMENT 3

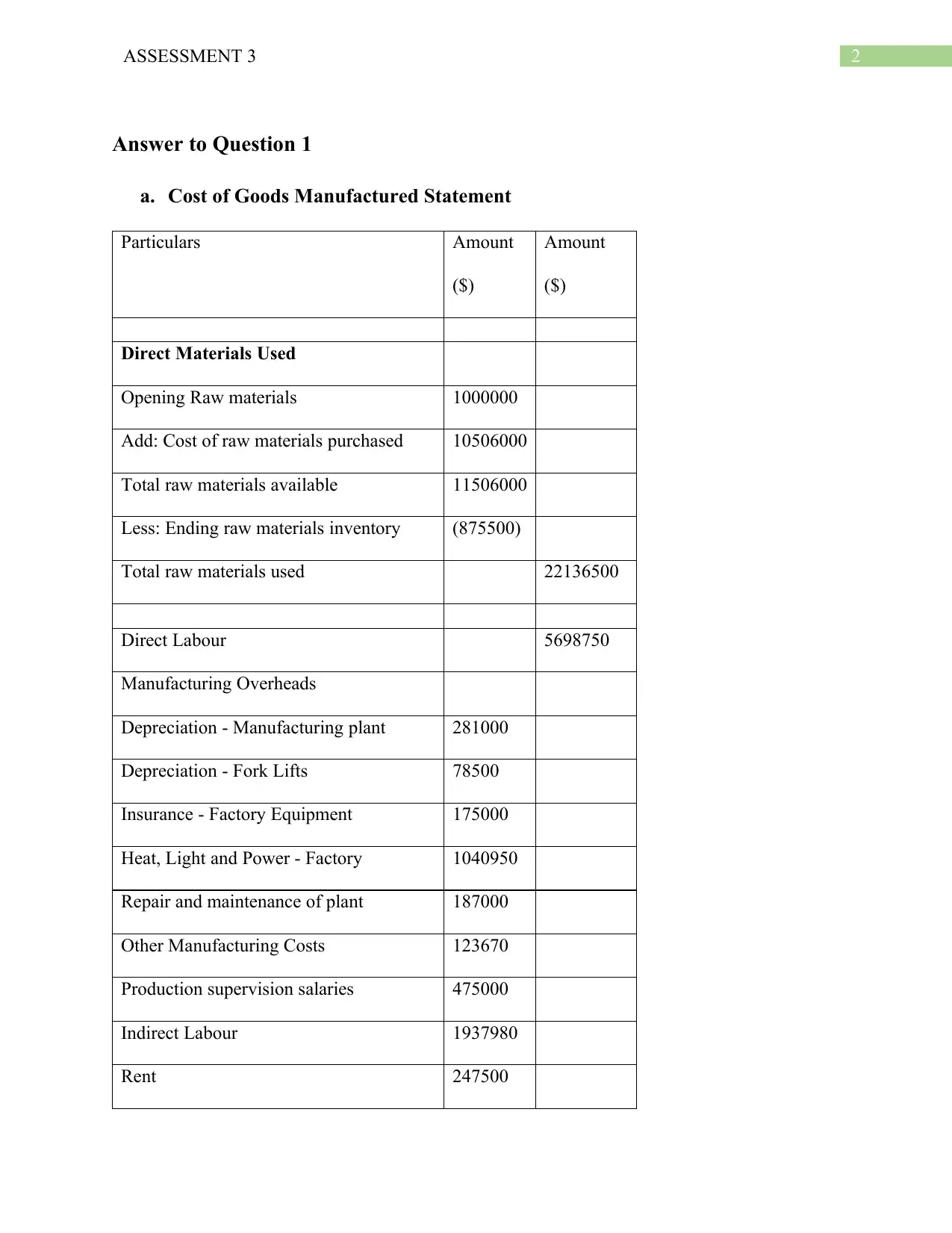

Answer to Question 1

a. Cost of Goods Manufactured Statement

Particulars Amount

($)

Amount

($)

Direct Materials Used

Opening Raw materials 1000000

Add: Cost of raw materials purchased 10506000

Total raw materials available 11506000

Less: Ending raw materials inventory (875500)

Total raw materials used 22136500

Direct Labour 5698750

Manufacturing Overheads

Depreciation - Manufacturing plant 281000

Depreciation - Fork Lifts 78500

Insurance - Factory Equipment 175000

Heat, Light and Power - Factory 1040950

Repair and maintenance of plant 187000

Other Manufacturing Costs 123670

Production supervision salaries 475000

Indirect Labour 1937980

Rent 247500

Answer to Question 1

a. Cost of Goods Manufactured Statement

Particulars Amount

($)

Amount

($)

Direct Materials Used

Opening Raw materials 1000000

Add: Cost of raw materials purchased 10506000

Total raw materials available 11506000

Less: Ending raw materials inventory (875500)

Total raw materials used 22136500

Direct Labour 5698750

Manufacturing Overheads

Depreciation - Manufacturing plant 281000

Depreciation - Fork Lifts 78500

Insurance - Factory Equipment 175000

Heat, Light and Power - Factory 1040950

Repair and maintenance of plant 187000

Other Manufacturing Costs 123670

Production supervision salaries 475000

Indirect Labour 1937980

Rent 247500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ASSESSMENT 3

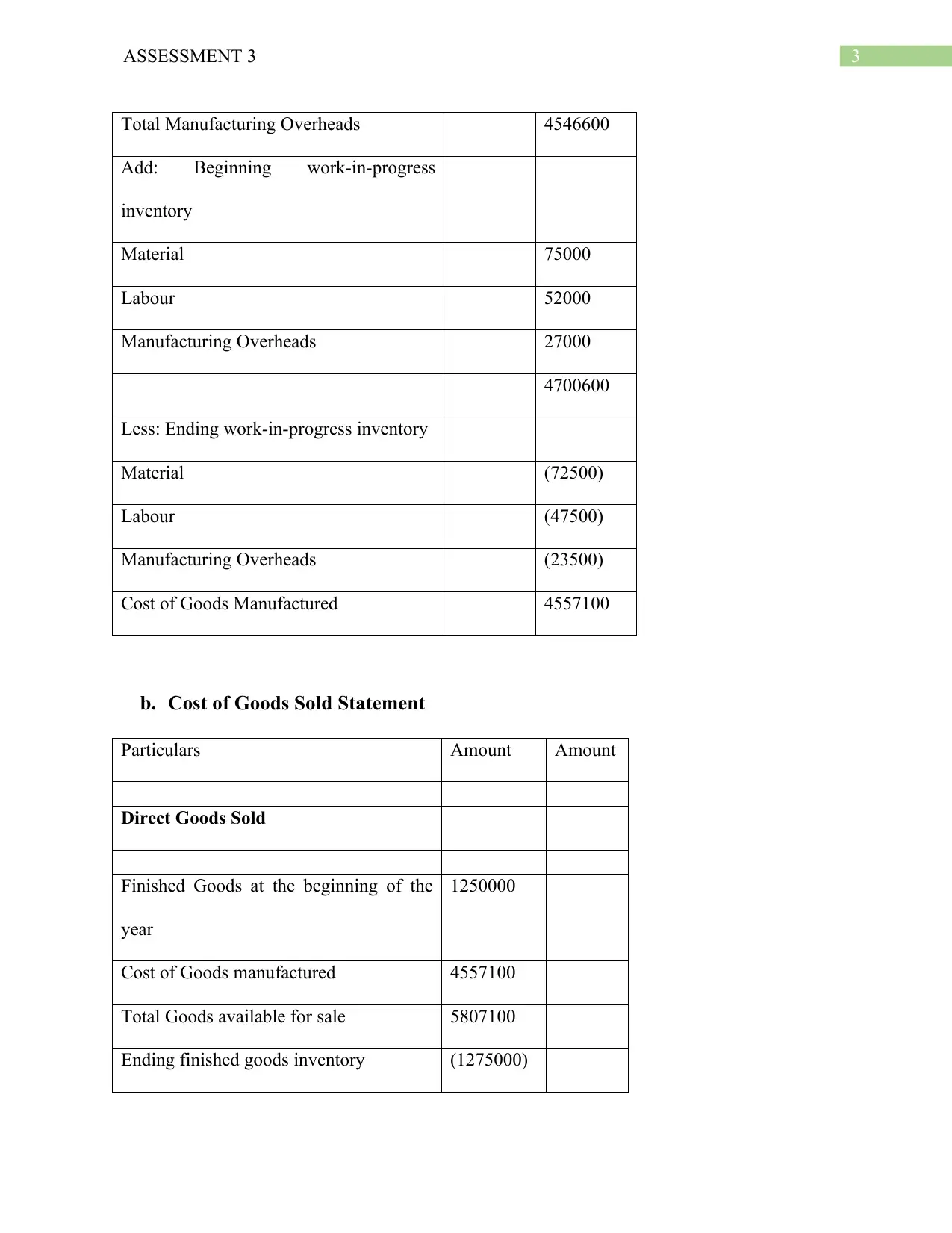

Total Manufacturing Overheads 4546600

Add: Beginning work-in-progress

inventory

Material 75000

Labour 52000

Manufacturing Overheads 27000

4700600

Less: Ending work-in-progress inventory

Material (72500)

Labour (47500)

Manufacturing Overheads (23500)

Cost of Goods Manufactured 4557100

b. Cost of Goods Sold Statement

Particulars Amount Amount

Direct Goods Sold

Finished Goods at the beginning of the

year

1250000

Cost of Goods manufactured 4557100

Total Goods available for sale 5807100

Ending finished goods inventory (1275000)

Total Manufacturing Overheads 4546600

Add: Beginning work-in-progress

inventory

Material 75000

Labour 52000

Manufacturing Overheads 27000

4700600

Less: Ending work-in-progress inventory

Material (72500)

Labour (47500)

Manufacturing Overheads (23500)

Cost of Goods Manufactured 4557100

b. Cost of Goods Sold Statement

Particulars Amount Amount

Direct Goods Sold

Finished Goods at the beginning of the

year

1250000

Cost of Goods manufactured 4557100

Total Goods available for sale 5807100

Ending finished goods inventory (1275000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ASSESSMENT 3

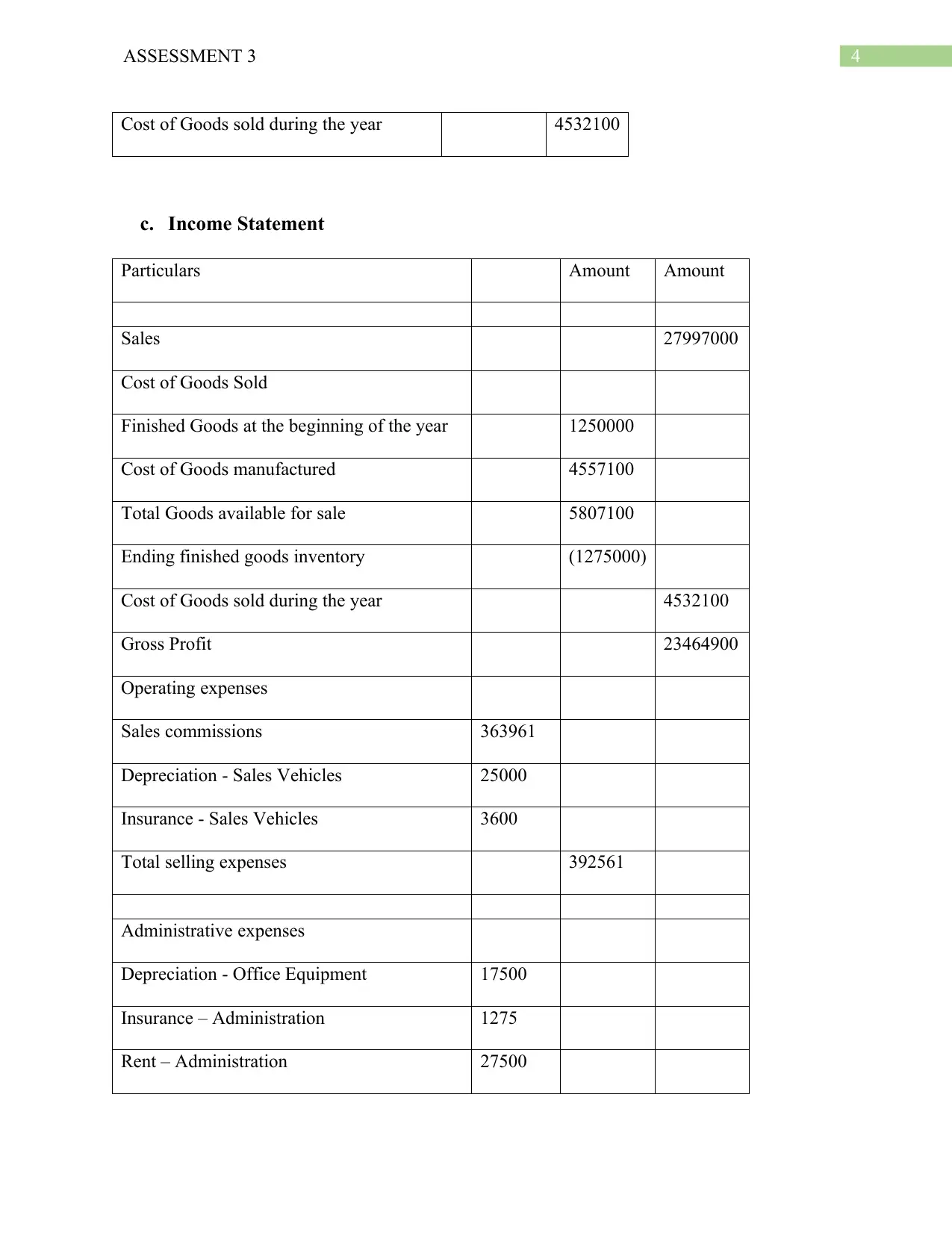

Cost of Goods sold during the year 4532100

c. Income Statement

Particulars Amount Amount

Sales 27997000

Cost of Goods Sold

Finished Goods at the beginning of the year 1250000

Cost of Goods manufactured 4557100

Total Goods available for sale 5807100

Ending finished goods inventory (1275000)

Cost of Goods sold during the year 4532100

Gross Profit 23464900

Operating expenses

Sales commissions 363961

Depreciation - Sales Vehicles 25000

Insurance - Sales Vehicles 3600

Total selling expenses 392561

Administrative expenses

Depreciation - Office Equipment 17500

Insurance – Administration 1275

Rent – Administration 27500

Cost of Goods sold during the year 4532100

c. Income Statement

Particulars Amount Amount

Sales 27997000

Cost of Goods Sold

Finished Goods at the beginning of the year 1250000

Cost of Goods manufactured 4557100

Total Goods available for sale 5807100

Ending finished goods inventory (1275000)

Cost of Goods sold during the year 4532100

Gross Profit 23464900

Operating expenses

Sales commissions 363961

Depreciation - Sales Vehicles 25000

Insurance - Sales Vehicles 3600

Total selling expenses 392561

Administrative expenses

Depreciation - Office Equipment 17500

Insurance – Administration 1275

Rent – Administration 27500

5ASSESSMENT 3

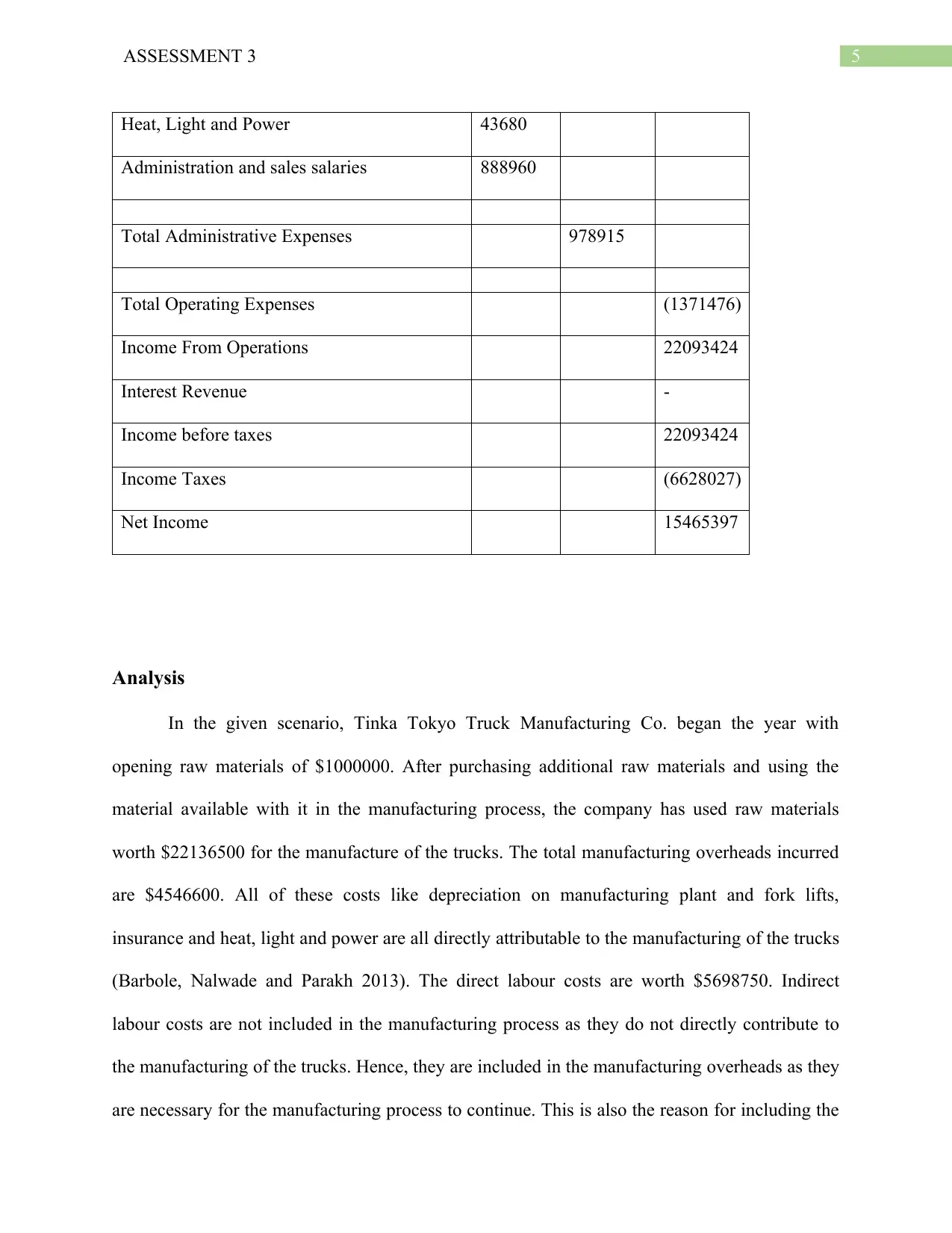

Heat, Light and Power 43680

Administration and sales salaries 888960

Total Administrative Expenses 978915

Total Operating Expenses (1371476)

Income From Operations 22093424

Interest Revenue -

Income before taxes 22093424

Income Taxes (6628027)

Net Income 15465397

Analysis

In the given scenario, Tinka Tokyo Truck Manufacturing Co. began the year with

opening raw materials of $1000000. After purchasing additional raw materials and using the

material available with it in the manufacturing process, the company has used raw materials

worth $22136500 for the manufacture of the trucks. The total manufacturing overheads incurred

are $4546600. All of these costs like depreciation on manufacturing plant and fork lifts,

insurance and heat, light and power are all directly attributable to the manufacturing of the trucks

(Barbole, Nalwade and Parakh 2013). The direct labour costs are worth $5698750. Indirect

labour costs are not included in the manufacturing process as they do not directly contribute to

the manufacturing of the trucks. Hence, they are included in the manufacturing overheads as they

are necessary for the manufacturing process to continue. This is also the reason for including the

Heat, Light and Power 43680

Administration and sales salaries 888960

Total Administrative Expenses 978915

Total Operating Expenses (1371476)

Income From Operations 22093424

Interest Revenue -

Income before taxes 22093424

Income Taxes (6628027)

Net Income 15465397

Analysis

In the given scenario, Tinka Tokyo Truck Manufacturing Co. began the year with

opening raw materials of $1000000. After purchasing additional raw materials and using the

material available with it in the manufacturing process, the company has used raw materials

worth $22136500 for the manufacture of the trucks. The total manufacturing overheads incurred

are $4546600. All of these costs like depreciation on manufacturing plant and fork lifts,

insurance and heat, light and power are all directly attributable to the manufacturing of the trucks

(Barbole, Nalwade and Parakh 2013). The direct labour costs are worth $5698750. Indirect

labour costs are not included in the manufacturing process as they do not directly contribute to

the manufacturing of the trucks. Hence, they are included in the manufacturing overheads as they

are necessary for the manufacturing process to continue. This is also the reason for including the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ASSESSMENT 3

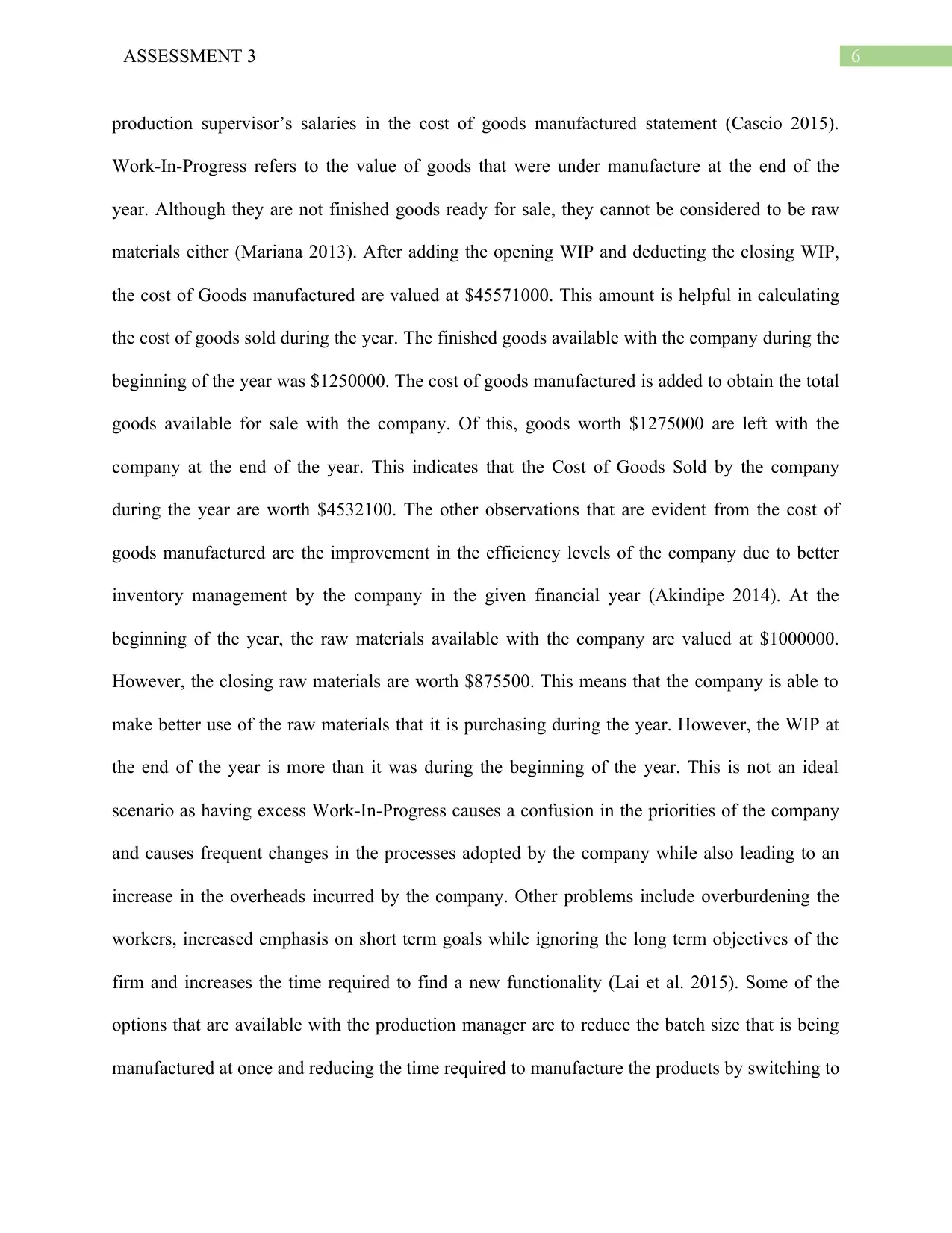

production supervisor’s salaries in the cost of goods manufactured statement (Cascio 2015).

Work-In-Progress refers to the value of goods that were under manufacture at the end of the

year. Although they are not finished goods ready for sale, they cannot be considered to be raw

materials either (Mariana 2013). After adding the opening WIP and deducting the closing WIP,

the cost of Goods manufactured are valued at $45571000. This amount is helpful in calculating

the cost of goods sold during the year. The finished goods available with the company during the

beginning of the year was $1250000. The cost of goods manufactured is added to obtain the total

goods available for sale with the company. Of this, goods worth $1275000 are left with the

company at the end of the year. This indicates that the Cost of Goods Sold by the company

during the year are worth $4532100. The other observations that are evident from the cost of

goods manufactured are the improvement in the efficiency levels of the company due to better

inventory management by the company in the given financial year (Akindipe 2014). At the

beginning of the year, the raw materials available with the company are valued at $1000000.

However, the closing raw materials are worth $875500. This means that the company is able to

make better use of the raw materials that it is purchasing during the year. However, the WIP at

the end of the year is more than it was during the beginning of the year. This is not an ideal

scenario as having excess Work-In-Progress causes a confusion in the priorities of the company

and causes frequent changes in the processes adopted by the company while also leading to an

increase in the overheads incurred by the company. Other problems include overburdening the

workers, increased emphasis on short term goals while ignoring the long term objectives of the

firm and increases the time required to find a new functionality (Lai et al. 2015). Some of the

options that are available with the production manager are to reduce the batch size that is being

manufactured at once and reducing the time required to manufacture the products by switching to

production supervisor’s salaries in the cost of goods manufactured statement (Cascio 2015).

Work-In-Progress refers to the value of goods that were under manufacture at the end of the

year. Although they are not finished goods ready for sale, they cannot be considered to be raw

materials either (Mariana 2013). After adding the opening WIP and deducting the closing WIP,

the cost of Goods manufactured are valued at $45571000. This amount is helpful in calculating

the cost of goods sold during the year. The finished goods available with the company during the

beginning of the year was $1250000. The cost of goods manufactured is added to obtain the total

goods available for sale with the company. Of this, goods worth $1275000 are left with the

company at the end of the year. This indicates that the Cost of Goods Sold by the company

during the year are worth $4532100. The other observations that are evident from the cost of

goods manufactured are the improvement in the efficiency levels of the company due to better

inventory management by the company in the given financial year (Akindipe 2014). At the

beginning of the year, the raw materials available with the company are valued at $1000000.

However, the closing raw materials are worth $875500. This means that the company is able to

make better use of the raw materials that it is purchasing during the year. However, the WIP at

the end of the year is more than it was during the beginning of the year. This is not an ideal

scenario as having excess Work-In-Progress causes a confusion in the priorities of the company

and causes frequent changes in the processes adopted by the company while also leading to an

increase in the overheads incurred by the company. Other problems include overburdening the

workers, increased emphasis on short term goals while ignoring the long term objectives of the

firm and increases the time required to find a new functionality (Lai et al. 2015). Some of the

options that are available with the production manager are to reduce the batch size that is being

manufactured at once and reducing the time required to manufacture the products by switching to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ASSESSMENT 3

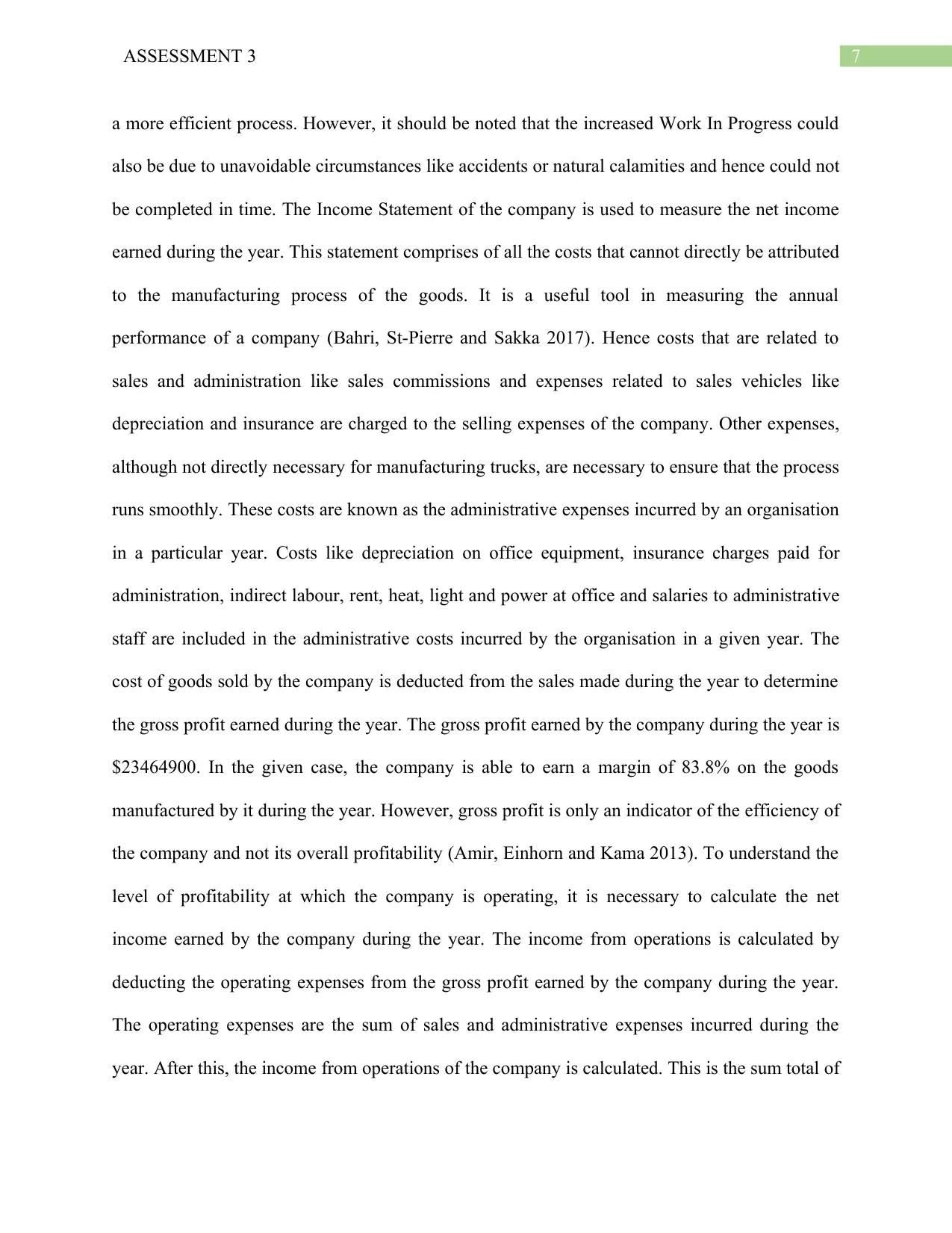

a more efficient process. However, it should be noted that the increased Work In Progress could

also be due to unavoidable circumstances like accidents or natural calamities and hence could not

be completed in time. The Income Statement of the company is used to measure the net income

earned during the year. This statement comprises of all the costs that cannot directly be attributed

to the manufacturing process of the goods. It is a useful tool in measuring the annual

performance of a company (Bahri, St-Pierre and Sakka 2017). Hence costs that are related to

sales and administration like sales commissions and expenses related to sales vehicles like

depreciation and insurance are charged to the selling expenses of the company. Other expenses,

although not directly necessary for manufacturing trucks, are necessary to ensure that the process

runs smoothly. These costs are known as the administrative expenses incurred by an organisation

in a particular year. Costs like depreciation on office equipment, insurance charges paid for

administration, indirect labour, rent, heat, light and power at office and salaries to administrative

staff are included in the administrative costs incurred by the organisation in a given year. The

cost of goods sold by the company is deducted from the sales made during the year to determine

the gross profit earned during the year. The gross profit earned by the company during the year is

$23464900. In the given case, the company is able to earn a margin of 83.8% on the goods

manufactured by it during the year. However, gross profit is only an indicator of the efficiency of

the company and not its overall profitability (Amir, Einhorn and Kama 2013). To understand the

level of profitability at which the company is operating, it is necessary to calculate the net

income earned by the company during the year. The income from operations is calculated by

deducting the operating expenses from the gross profit earned by the company during the year.

The operating expenses are the sum of sales and administrative expenses incurred during the

year. After this, the income from operations of the company is calculated. This is the sum total of

a more efficient process. However, it should be noted that the increased Work In Progress could

also be due to unavoidable circumstances like accidents or natural calamities and hence could not

be completed in time. The Income Statement of the company is used to measure the net income

earned during the year. This statement comprises of all the costs that cannot directly be attributed

to the manufacturing process of the goods. It is a useful tool in measuring the annual

performance of a company (Bahri, St-Pierre and Sakka 2017). Hence costs that are related to

sales and administration like sales commissions and expenses related to sales vehicles like

depreciation and insurance are charged to the selling expenses of the company. Other expenses,

although not directly necessary for manufacturing trucks, are necessary to ensure that the process

runs smoothly. These costs are known as the administrative expenses incurred by an organisation

in a particular year. Costs like depreciation on office equipment, insurance charges paid for

administration, indirect labour, rent, heat, light and power at office and salaries to administrative

staff are included in the administrative costs incurred by the organisation in a given year. The

cost of goods sold by the company is deducted from the sales made during the year to determine

the gross profit earned during the year. The gross profit earned by the company during the year is

$23464900. In the given case, the company is able to earn a margin of 83.8% on the goods

manufactured by it during the year. However, gross profit is only an indicator of the efficiency of

the company and not its overall profitability (Amir, Einhorn and Kama 2013). To understand the

level of profitability at which the company is operating, it is necessary to calculate the net

income earned by the company during the year. The income from operations is calculated by

deducting the operating expenses from the gross profit earned by the company during the year.

The operating expenses are the sum of sales and administrative expenses incurred during the

year. After this, the income from operations of the company is calculated. This is the sum total of

8ASSESSMENT 3

the entire income earned by the company during the financial year. Any revenue earned from the

interest is added to the income from operations to calculate the income earned before taxes. As

the company is paying taxes @30%, these taxes are deducted to know the value of the net

income earned by the company during the year. Tinka Tokyo Manufacturing Co. has paid taxes

worth $6628027 during the financial year. The net income earned by the company during the

year is $15465397. The net income earned by the company is 55 percent of the sales made by it

in the financial year. This means that the company is having an excess balance of $15465397

after deducting all the expenses incurred by it during the year from the revenues generated by it

from its operations. This amount can be used by the company as an investment for its future

operations and is useful in the expansion of the business as a whole (Acaravci 2015). It can be

suggested on an overall basis that the business of the manufacturing firm has been profitable as a

whole and hence needs to be continued in the way it has been doing. However, it should try to

improve its efficiency in areas where there is scope for improvement like WIP and reducing its

administration charges.

Answer to Question 2

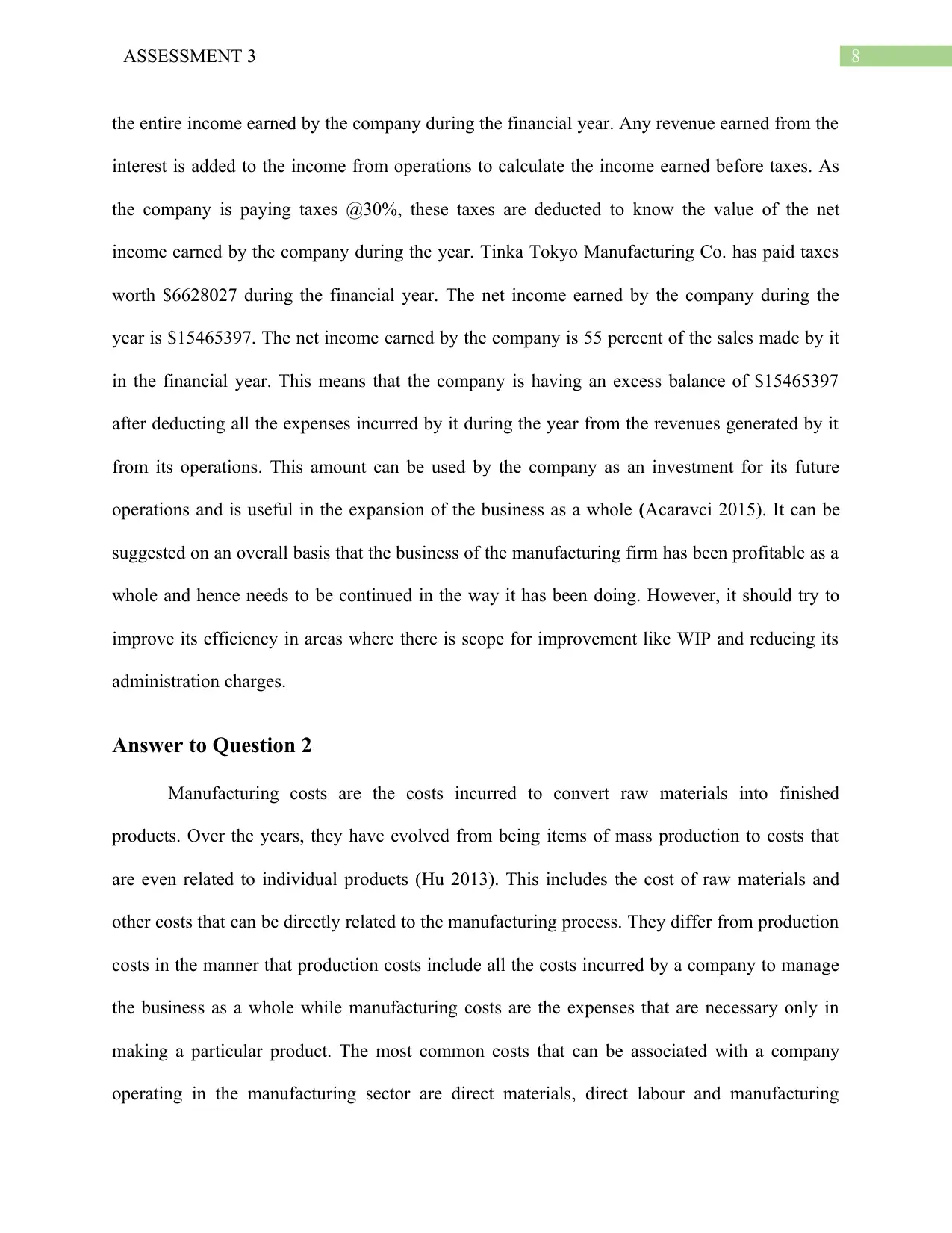

Manufacturing costs are the costs incurred to convert raw materials into finished

products. Over the years, they have evolved from being items of mass production to costs that

are even related to individual products (Hu 2013). This includes the cost of raw materials and

other costs that can be directly related to the manufacturing process. They differ from production

costs in the manner that production costs include all the costs incurred by a company to manage

the business as a whole while manufacturing costs are the expenses that are necessary only in

making a particular product. The most common costs that can be associated with a company

operating in the manufacturing sector are direct materials, direct labour and manufacturing

the entire income earned by the company during the financial year. Any revenue earned from the

interest is added to the income from operations to calculate the income earned before taxes. As

the company is paying taxes @30%, these taxes are deducted to know the value of the net

income earned by the company during the year. Tinka Tokyo Manufacturing Co. has paid taxes

worth $6628027 during the financial year. The net income earned by the company during the

year is $15465397. The net income earned by the company is 55 percent of the sales made by it

in the financial year. This means that the company is having an excess balance of $15465397

after deducting all the expenses incurred by it during the year from the revenues generated by it

from its operations. This amount can be used by the company as an investment for its future

operations and is useful in the expansion of the business as a whole (Acaravci 2015). It can be

suggested on an overall basis that the business of the manufacturing firm has been profitable as a

whole and hence needs to be continued in the way it has been doing. However, it should try to

improve its efficiency in areas where there is scope for improvement like WIP and reducing its

administration charges.

Answer to Question 2

Manufacturing costs are the costs incurred to convert raw materials into finished

products. Over the years, they have evolved from being items of mass production to costs that

are even related to individual products (Hu 2013). This includes the cost of raw materials and

other costs that can be directly related to the manufacturing process. They differ from production

costs in the manner that production costs include all the costs incurred by a company to manage

the business as a whole while manufacturing costs are the expenses that are necessary only in

making a particular product. The most common costs that can be associated with a company

operating in the manufacturing sector are direct materials, direct labour and manufacturing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ASSESSMENT 3

overheads (Chryssolouris 2013). In calculating the cost of goods manufactured in a year, it is

important to differentiate between the direct and indirect costs. This is to be able to easily

differentiate between the costs that need to be reduced to produce a particular product at a lesser

cost. Direct material costs are the costs of raw materials that can be directly identified in the final

product. For example, cost of iron required to manufacture a crane. Indirect materials involve

those items that cannot be directly identified in a product but are necessary to bring the material

to a usable state. Various functions are applied to the direct materials like welding, cutting and

bending that are not directly traceable in a product but are necessary (Henri, Boiral and Roy

2016). These costs come under the indirect material required for production. Direct labour is the

amount of wages or other monetary benefits earned by individuals who directly contribute to the

manufacturing process. This includes individuals who are physically involved in the production

like manual labour or contract labour who are responsible for ensuring that the manufacturing is

taking place in a proper manner. Indirect labour consists of people responsible for carrying the

goods from the place of purchase to the factory, material handling labourers and supervisors that

are responsible for bringing a product to its finished state (Cushen and Thompson 2016).

Manufacturing overheads includes the costs that cannot be attributed to both material and labour

costs but are necessary for the production process to take place. These costs include depreciation

and repairs and maintenance of plant and equipment, insurance paid for factory premises,

salaries to supervisors and production heads who take care of the production process as a whole.

Other costs include heat, lighting and power in factory and rent paid for the factory or machinery

being used in the manufacture of the final products. Indirect labour costs, like costs associated

with workers that are involved in the supervision of the production process and handling of

materials are also included in the manufacturing overheads (Oluwagbemiga, Olugbenga and

overheads (Chryssolouris 2013). In calculating the cost of goods manufactured in a year, it is

important to differentiate between the direct and indirect costs. This is to be able to easily

differentiate between the costs that need to be reduced to produce a particular product at a lesser

cost. Direct material costs are the costs of raw materials that can be directly identified in the final

product. For example, cost of iron required to manufacture a crane. Indirect materials involve

those items that cannot be directly identified in a product but are necessary to bring the material

to a usable state. Various functions are applied to the direct materials like welding, cutting and

bending that are not directly traceable in a product but are necessary (Henri, Boiral and Roy

2016). These costs come under the indirect material required for production. Direct labour is the

amount of wages or other monetary benefits earned by individuals who directly contribute to the

manufacturing process. This includes individuals who are physically involved in the production

like manual labour or contract labour who are responsible for ensuring that the manufacturing is

taking place in a proper manner. Indirect labour consists of people responsible for carrying the

goods from the place of purchase to the factory, material handling labourers and supervisors that

are responsible for bringing a product to its finished state (Cushen and Thompson 2016).

Manufacturing overheads includes the costs that cannot be attributed to both material and labour

costs but are necessary for the production process to take place. These costs include depreciation

and repairs and maintenance of plant and equipment, insurance paid for factory premises,

salaries to supervisors and production heads who take care of the production process as a whole.

Other costs include heat, lighting and power in factory and rent paid for the factory or machinery

being used in the manufacture of the final products. Indirect labour costs, like costs associated

with workers that are involved in the supervision of the production process and handling of

materials are also included in the manufacturing overheads (Oluwagbemiga, Olugbenga and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ASSESSMENT 3

Zaccheaus 2014). Indirect materials that cannot directly be traced in the materials manufactured

during the year like diesel, grease and coal in machinery are charged under the manufacturing

overheads.

Capacity refers to the amount of goods that can be manufactured by a company in a given

financial year by taking all the constraints like availability of space, labour, materials and access

to capital into consideration. Theoretical capacity of a manufacturer refers to the amount of

production that can be achieved in a given year if all the machinery and labour that are being

used in the production process performed at their optimal capacity on a continuous basis

throughout the duration of the production process (DRURY 2013). Theoretical capacity is also

known as the ideal capacity. Practical capacity refers to the amount of goods that a company or

manufacturer can produce in a given year by taking the availability of materials, labour hours

and machine hours into consideration. This is always less than or equal to the ideal capacity. In

case of manufacturing concerns, the practical or ideal capacity are calculated using different

units of measurement like machine hours, number of units of a product etc. Differences in

practical and theoretical capacity occur due to a number of reasons (Schröter et al. 2014). They

include repairs and maintenance related to the machinery, shutdown of the plant on account of

holidays, wrong estimation of the theoretical capacity by the accountants, and other factors

responsible for causing downtime. In cases where practical capacity differs from theoretical

capacity due to wrong estimations, there is a need to review the policies followed by the

accountant. The review conducted by them include a review of the annual machine hours for

which a machinery can be used for production and the expected level of production that can be

achieved by the company in the future. In order to determine an effective system of

manufacturing in a company, there are various techniques. Some of them include Quality Circle,

Zaccheaus 2014). Indirect materials that cannot directly be traced in the materials manufactured

during the year like diesel, grease and coal in machinery are charged under the manufacturing

overheads.

Capacity refers to the amount of goods that can be manufactured by a company in a given

financial year by taking all the constraints like availability of space, labour, materials and access

to capital into consideration. Theoretical capacity of a manufacturer refers to the amount of

production that can be achieved in a given year if all the machinery and labour that are being

used in the production process performed at their optimal capacity on a continuous basis

throughout the duration of the production process (DRURY 2013). Theoretical capacity is also

known as the ideal capacity. Practical capacity refers to the amount of goods that a company or

manufacturer can produce in a given year by taking the availability of materials, labour hours

and machine hours into consideration. This is always less than or equal to the ideal capacity. In

case of manufacturing concerns, the practical or ideal capacity are calculated using different

units of measurement like machine hours, number of units of a product etc. Differences in

practical and theoretical capacity occur due to a number of reasons (Schröter et al. 2014). They

include repairs and maintenance related to the machinery, shutdown of the plant on account of

holidays, wrong estimation of the theoretical capacity by the accountants, and other factors

responsible for causing downtime. In cases where practical capacity differs from theoretical

capacity due to wrong estimations, there is a need to review the policies followed by the

accountant. The review conducted by them include a review of the annual machine hours for

which a machinery can be used for production and the expected level of production that can be

achieved by the company in the future. In order to determine an effective system of

manufacturing in a company, there are various techniques. Some of them include Quality Circle,

11ASSESSMENT 3

Kanban system and 5S housekeeping. One of the modern techniques that is used to reduce

wastage and improve the practical capacity of an organisation is lean manufacturing (Rahman,

Sharif and Esa 2013). These are a set of tools that help in the reduction of wastage and improve

the quality and price of the product. Some of the recent researches show that the phenomenon of

sticky costs is due to the deliberate management decision making while also considering

adjustment costs. However, it has been found that these costs show a much more asymmetric

behaviour and cannot be attributed directly to the capacity of the organisation (Banker et al.

2014). Hence, there is a requirement of new methods that take the uncertain nature of business

costs into account and should be useful in the estimation of future capacity in an accurate

manner. In conclusion, it can be said that in the modern day business organisations, allocating

the manufacturing costs has become increasingly complex there is a need for an updated method

that measures these costs appropriately. Apart from that, it should also be able to allocate them in

a proper way to determine the capacity of an organisation in a more reliable manner.

Kanban system and 5S housekeeping. One of the modern techniques that is used to reduce

wastage and improve the practical capacity of an organisation is lean manufacturing (Rahman,

Sharif and Esa 2013). These are a set of tools that help in the reduction of wastage and improve

the quality and price of the product. Some of the recent researches show that the phenomenon of

sticky costs is due to the deliberate management decision making while also considering

adjustment costs. However, it has been found that these costs show a much more asymmetric

behaviour and cannot be attributed directly to the capacity of the organisation (Banker et al.

2014). Hence, there is a requirement of new methods that take the uncertain nature of business

costs into account and should be useful in the estimation of future capacity in an accurate

manner. In conclusion, it can be said that in the modern day business organisations, allocating

the manufacturing costs has become increasingly complex there is a need for an updated method

that measures these costs appropriately. Apart from that, it should also be able to allocate them in

a proper way to determine the capacity of an organisation in a more reliable manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.