Asset Impairment Report

VerifiedAdded on 2019/11/20

|8

|1563

|135

Report

AI Summary

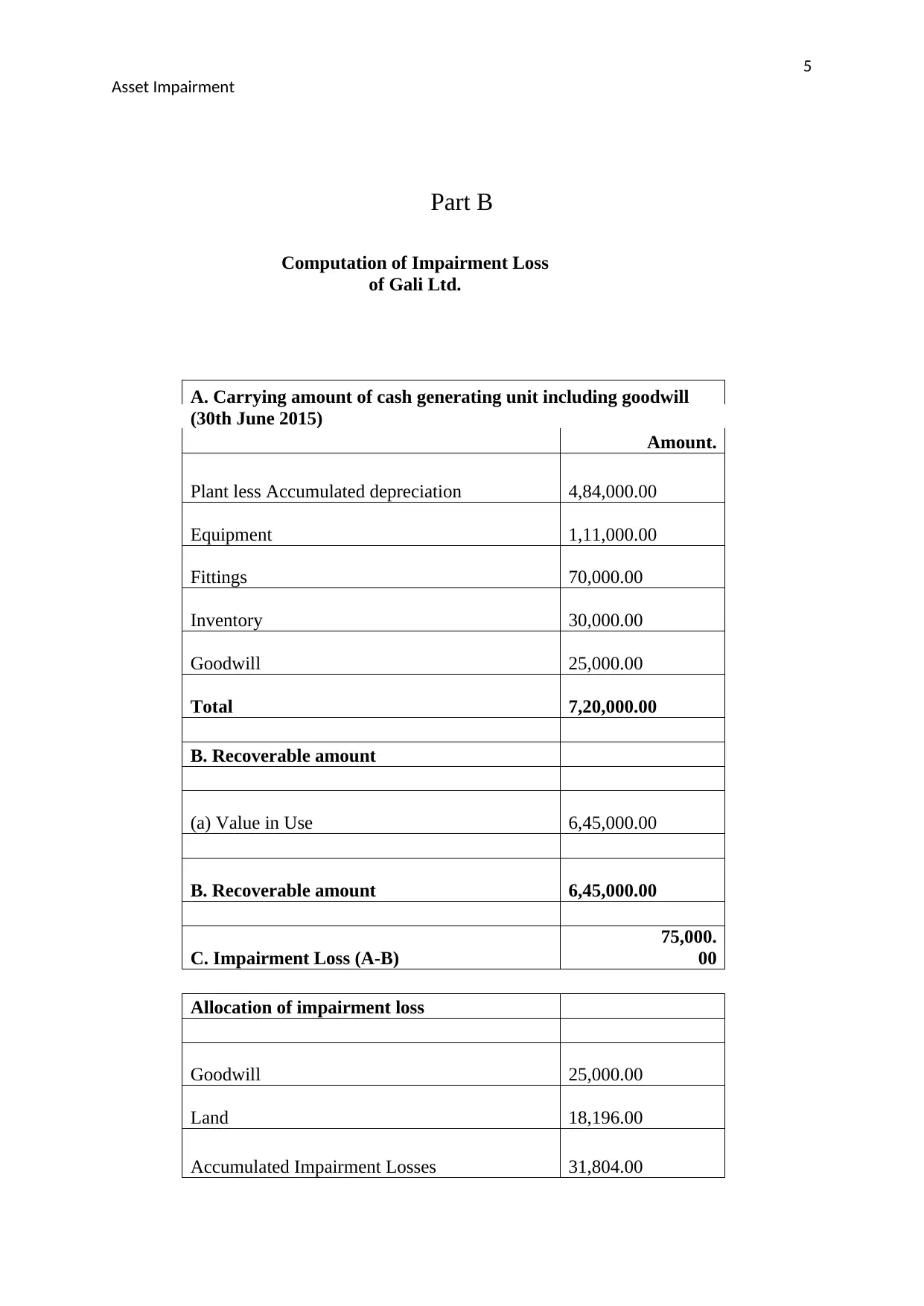

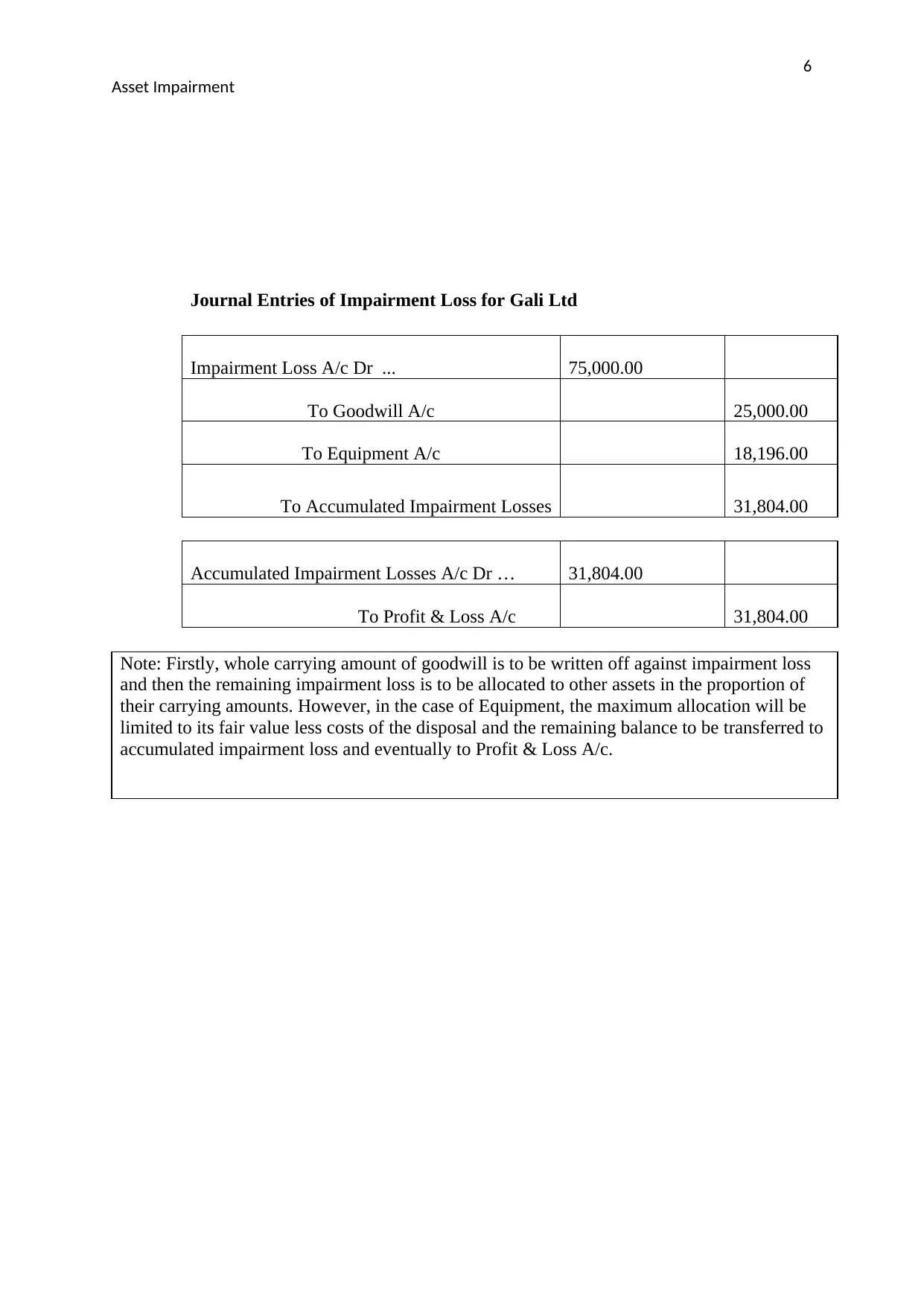

This report thoroughly explains the concept of asset impairment, its recognition, and measurement according to accounting standards like AASB 136. It defines asset impairment as a situation where an asset's carrying value exceeds its recoverable amount. The report details the accounting treatment for impairment losses, including how they are recognized in the profit and loss statement and the impact of revaluation reserves. It also identifies internal and external factors that indicate potential impairment, such as market value decline, technological changes, and asset obsolescence. The recoverable amount is determined as the higher of an asset's value in use and its fair value. A case study of Gali Ltd. demonstrates the computation of impairment loss and its allocation among different assets, including goodwill. The report concludes by emphasizing the importance of regular impairment checks, particularly for intangible assets, to mitigate the impact of asset value decline. Journal entries are provided to illustrate the accounting treatment of the impairment loss.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.