Advanced Financial Accounting Report: Impairment Testing of Assets

VerifiedAdded on 2020/05/28

|14

|3078

|71

Report

AI Summary

This report provides a comprehensive analysis of asset impairment in advanced financial accounting, using M2 Telecommunications Group Limited's 2015 annual report as a case study. It examines the company's impairment testing processes for various asset classes, including intangible assets, goodwill, trade receivables, and property, plant, and equipment. The report delves into the two-step impairment testing technique, assumptions, and subjectivity involved, highlighting the impact of IFRS 36 and the potential for opportunistic management discretion. Furthermore, it explores the concepts of fair value and value-in-use in determining impairment loss and discusses the implications of new accounting standards, particularly regarding lease accounting, US GAAP, and IFRS, and their impact on financial reporting and comparability. The analysis also covers the challenges and controversies associated with changes in accounting standards, emphasizing the need for businesses to adapt and consider the broad commercial implications of such changes.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................2

Answer (i):...................................................................................................................................2

Answer (ii):..................................................................................................................................3

Answer (iii):.................................................................................................................................3

Answer (iv):.................................................................................................................................5

Answer (v):..................................................................................................................................6

Answer (vi):.................................................................................................................................6

Answer (vii):................................................................................................................................7

Answer (viii):...............................................................................................................................7

Part B:..............................................................................................................................................8

Answer (i):...................................................................................................................................8

Answer (ii):..................................................................................................................................8

Answer (iii):.................................................................................................................................9

Answer (iv):.................................................................................................................................9

Answer (v):................................................................................................................................10

References:....................................................................................................................................11

Table of Contents

Part A:..............................................................................................................................................2

Answer (i):...................................................................................................................................2

Answer (ii):..................................................................................................................................3

Answer (iii):.................................................................................................................................3

Answer (iv):.................................................................................................................................5

Answer (v):..................................................................................................................................6

Answer (vi):.................................................................................................................................6

Answer (vii):................................................................................................................................7

Answer (viii):...............................................................................................................................7

Part B:..............................................................................................................................................8

Answer (i):...................................................................................................................................8

Answer (ii):..................................................................................................................................8

Answer (iii):.................................................................................................................................9

Answer (iv):.................................................................................................................................9

Answer (v):................................................................................................................................10

References:....................................................................................................................................11

2ADVANCED FINANCIAL ACCOUNTING

Part A:

This report has an objective to focus on the assumption and impairment criteria employed

in the behalf of M2 Telecommunications Group Limited in order to conduct asset based

impairment tests. This report has an intention of assorting the impairment testing processes along

with associated subjectivity within the process. For explain these processes, the company’s

yearly report for the year ended 30th June, 2015 was taken into account for it did not provide the

yearly report after the mentioned period (Banker, Basu and Byzalov 2016). The company is

renowned as an Australian retailer and wholesaler of offering telecommunication services,

insurance, power and gas products. The firm has two business segments that includes the

wholesale along with the consumer segment. M2 Telecommunications Group Limited has more

than 3000 employees all round New Zealand, Australia and Philippines and is now aligned with

Vocus Communications after 5th February 2016 (Bianchi 2017).

Moreover, an asset is said to be impaired that has a decreased market value in comparison

to its carrying value. The assets those are deemed to be impaired are tangible assets such as

plant, property and equipment as well as goodwill that is an intangible asset (Bond, Govendir

and Wells 2016). After carrying out adjustments with the impaired asset based carrying amount,

loss is mentioned within the firm’s income statement. While writing off an impairment, the asset

can have decreased carrying cost as certain adjustments might be carried out as a part of loss and

this can result in asset value decrease (Bryan 2017).

Answer (i):

Considering the annual report of M2 Telecommunications Group Limited in 2015, the

testing of impairment for different asset classes has been carried out. Intangible assets as well as

Part A:

This report has an objective to focus on the assumption and impairment criteria employed

in the behalf of M2 Telecommunications Group Limited in order to conduct asset based

impairment tests. This report has an intention of assorting the impairment testing processes along

with associated subjectivity within the process. For explain these processes, the company’s

yearly report for the year ended 30th June, 2015 was taken into account for it did not provide the

yearly report after the mentioned period (Banker, Basu and Byzalov 2016). The company is

renowned as an Australian retailer and wholesaler of offering telecommunication services,

insurance, power and gas products. The firm has two business segments that includes the

wholesale along with the consumer segment. M2 Telecommunications Group Limited has more

than 3000 employees all round New Zealand, Australia and Philippines and is now aligned with

Vocus Communications after 5th February 2016 (Bianchi 2017).

Moreover, an asset is said to be impaired that has a decreased market value in comparison

to its carrying value. The assets those are deemed to be impaired are tangible assets such as

plant, property and equipment as well as goodwill that is an intangible asset (Bond, Govendir

and Wells 2016). After carrying out adjustments with the impaired asset based carrying amount,

loss is mentioned within the firm’s income statement. While writing off an impairment, the asset

can have decreased carrying cost as certain adjustments might be carried out as a part of loss and

this can result in asset value decrease (Bryan 2017).

Answer (i):

Considering the annual report of M2 Telecommunications Group Limited in 2015, the

testing of impairment for different asset classes has been carried out. Intangible assets as well as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

goodwill that is not being amortized rather than the fact that there are tested within the

circumstances or events this indicates that the assets that can be impaired along with the fact that

financial statements that is recorded within the financial statements within cost subtracted from

an impaired accumulated loss (Contractor, Yang and Gaur 2016). Certain assets include

property, plant and equipment along with trade receivables that is tested for impairment in a

situation where there is an indication regarding an assets carrying amount that is not that

recoverable.

Answer (ii):

M2 Telecommunications Group Limited initiated a two-step technique for testing of

impairment. The first step is focused on fair value contrasting associated with repotting unit

along with carrying value including the goodwill. In a situation where carrying value of

operating unit remains high in contrast to the fair value, the second step is associated with testing

of impairment test must be conducted in order to make sure impairment loss amount presence

(Detzen, Wersborg and Zülch 2015). The second step is linked with implied fair value related

with the reporting unit in account to the that unit’s carrying amount. In a situation where, implied

fair value is decreased in comparison to the carrying amount, charge of impairment charge

remained within an amount related with that excess along with that realized loss might not go

beyond the assets carrying amount.

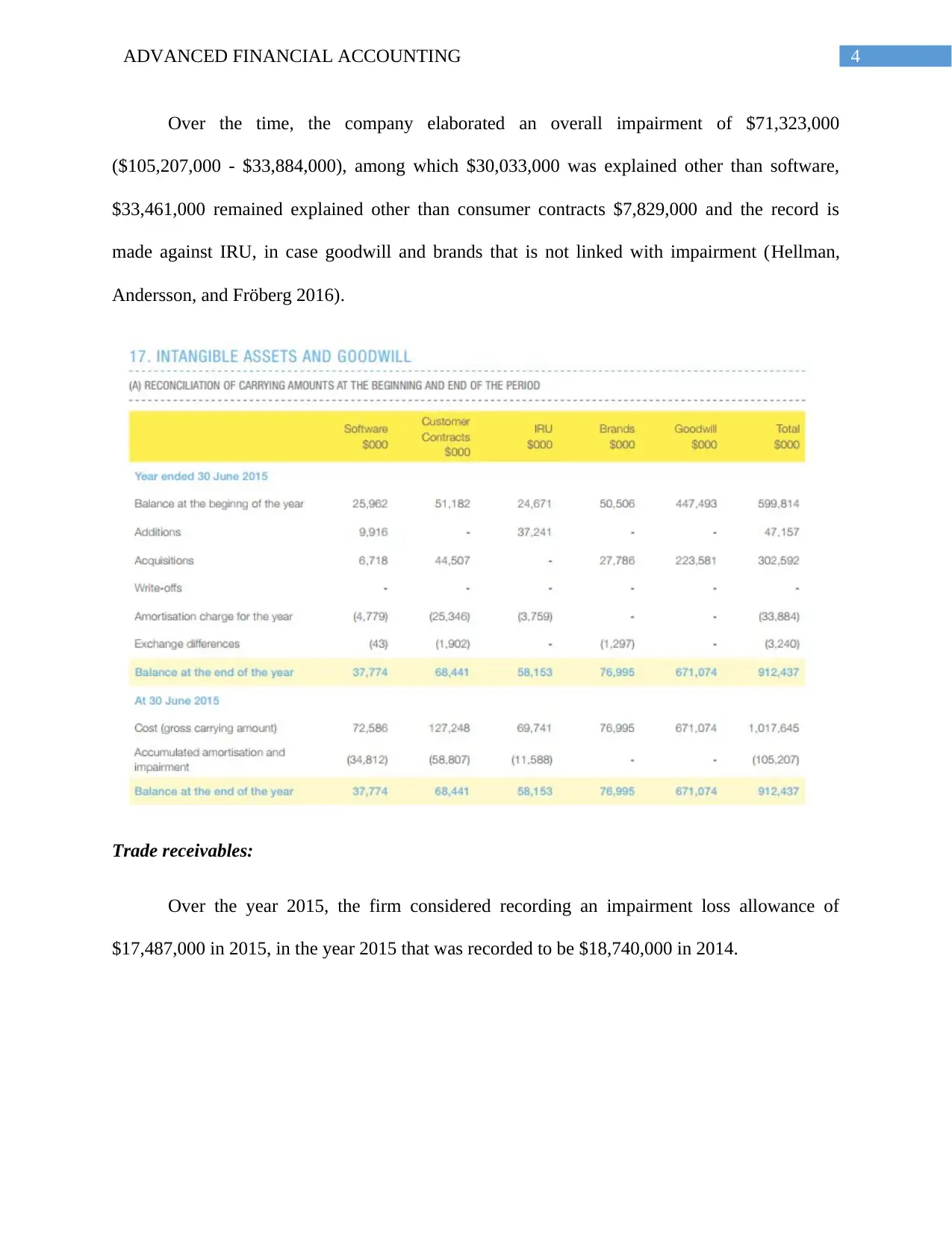

Answer (iii):

The company made certain the following impairment costs over the time ended on 30th

June 2015:

Intangible assets along with goodwill:

goodwill that is not being amortized rather than the fact that there are tested within the

circumstances or events this indicates that the assets that can be impaired along with the fact that

financial statements that is recorded within the financial statements within cost subtracted from

an impaired accumulated loss (Contractor, Yang and Gaur 2016). Certain assets include

property, plant and equipment along with trade receivables that is tested for impairment in a

situation where there is an indication regarding an assets carrying amount that is not that

recoverable.

Answer (ii):

M2 Telecommunications Group Limited initiated a two-step technique for testing of

impairment. The first step is focused on fair value contrasting associated with repotting unit

along with carrying value including the goodwill. In a situation where carrying value of

operating unit remains high in contrast to the fair value, the second step is associated with testing

of impairment test must be conducted in order to make sure impairment loss amount presence

(Detzen, Wersborg and Zülch 2015). The second step is linked with implied fair value related

with the reporting unit in account to the that unit’s carrying amount. In a situation where, implied

fair value is decreased in comparison to the carrying amount, charge of impairment charge

remained within an amount related with that excess along with that realized loss might not go

beyond the assets carrying amount.

Answer (iii):

The company made certain the following impairment costs over the time ended on 30th

June 2015:

Intangible assets along with goodwill:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

Over the time, the company elaborated an overall impairment of $71,323,000

($105,207,000 - $33,884,000), among which $30,033,000 was explained other than software,

$33,461,000 remained explained other than consumer contracts $7,829,000 and the record is

made against IRU, in case goodwill and brands that is not linked with impairment (Hellman,

Andersson, and Fröberg 2016).

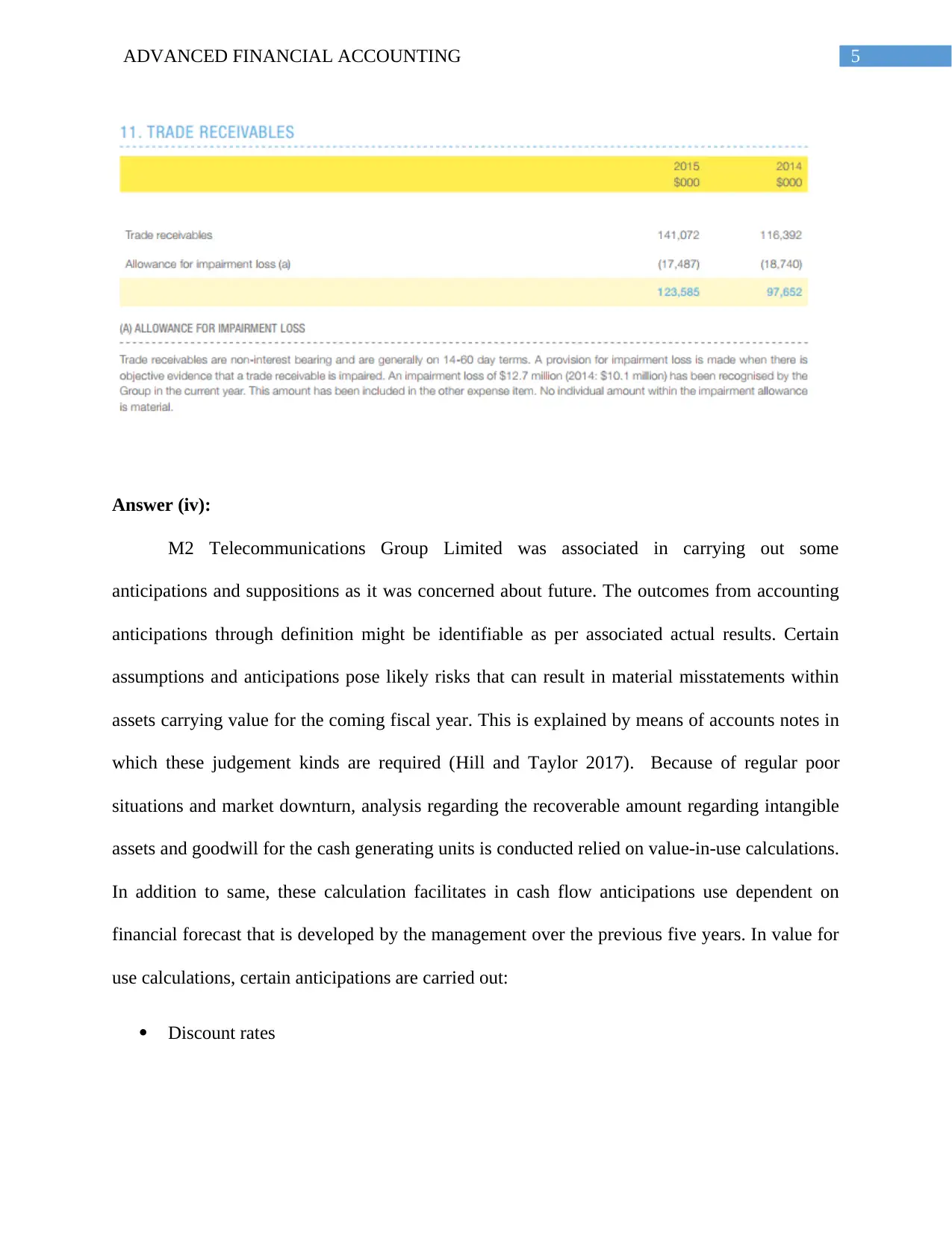

Trade receivables:

Over the year 2015, the firm considered recording an impairment loss allowance of

$17,487,000 in 2015, in the year 2015 that was recorded to be $18,740,000 in 2014.

Over the time, the company elaborated an overall impairment of $71,323,000

($105,207,000 - $33,884,000), among which $30,033,000 was explained other than software,

$33,461,000 remained explained other than consumer contracts $7,829,000 and the record is

made against IRU, in case goodwill and brands that is not linked with impairment (Hellman,

Andersson, and Fröberg 2016).

Trade receivables:

Over the year 2015, the firm considered recording an impairment loss allowance of

$17,487,000 in 2015, in the year 2015 that was recorded to be $18,740,000 in 2014.

5ADVANCED FINANCIAL ACCOUNTING

Answer (iv):

M2 Telecommunications Group Limited was associated in carrying out some

anticipations and suppositions as it was concerned about future. The outcomes from accounting

anticipations through definition might be identifiable as per associated actual results. Certain

assumptions and anticipations pose likely risks that can result in material misstatements within

assets carrying value for the coming fiscal year. This is explained by means of accounts notes in

which these judgement kinds are required (Hill and Taylor 2017). Because of regular poor

situations and market downturn, analysis regarding the recoverable amount regarding intangible

assets and goodwill for the cash generating units is conducted relied on value-in-use calculations.

In addition to same, these calculation facilitates in cash flow anticipations use dependent on

financial forecast that is developed by the management over the previous five years. In value for

use calculations, certain anticipations are carried out:

Discount rates

Answer (iv):

M2 Telecommunications Group Limited was associated in carrying out some

anticipations and suppositions as it was concerned about future. The outcomes from accounting

anticipations through definition might be identifiable as per associated actual results. Certain

assumptions and anticipations pose likely risks that can result in material misstatements within

assets carrying value for the coming fiscal year. This is explained by means of accounts notes in

which these judgement kinds are required (Hill and Taylor 2017). Because of regular poor

situations and market downturn, analysis regarding the recoverable amount regarding intangible

assets and goodwill for the cash generating units is conducted relied on value-in-use calculations.

In addition to same, these calculation facilitates in cash flow anticipations use dependent on

financial forecast that is developed by the management over the previous five years. In value for

use calculations, certain anticipations are carried out:

Discount rates

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

Growth rates through implementation of extrapolate cash flows other than the estimated

period

EBITDA/ Sales margin

Answer (v):

Based on “IAS 36 Impairment of Assets”, this has been gathered that it is specific IFRS

standard as this requires certain subjective interpretation along with that this might be

implemented with respect to the managerial requirements. In addition, it did not facilitate

creative accounting restriction. It has been recognized that financial statements of M2

Telecommunications Group Limited that has considerable subjectivity that is associated in case

the management time carried out the impairment test process (Kuo and Lee 2017). This is due to

the fact that a company’s management can be exploited at the discretion through carrying out

goodwill impairment test opportunistically. This might be validated by allocation of goodwill to

all cash generating units along with computation of recoverable amount while there is a lack of

active prices for goodwill that with discretion subject (Watts and Zuo 2016).

Answer (vi):

After a detailed analysis, this has been gathered that certain difficult or confessing aspect

related to impairment is associated with the impairment indication. Despite of the fact that

indications are based on external as well as internal factors in alignment with the assets

impairment, the regularity of conducting such tests for goodwill along with some tangible assets

totally base on the managements discretion (Linnenluecke et al. 2015). Due to these factors there

is high chance that the management might carry out an opportunistic test in case there occurs any

change in the value.

Growth rates through implementation of extrapolate cash flows other than the estimated

period

EBITDA/ Sales margin

Answer (v):

Based on “IAS 36 Impairment of Assets”, this has been gathered that it is specific IFRS

standard as this requires certain subjective interpretation along with that this might be

implemented with respect to the managerial requirements. In addition, it did not facilitate

creative accounting restriction. It has been recognized that financial statements of M2

Telecommunications Group Limited that has considerable subjectivity that is associated in case

the management time carried out the impairment test process (Kuo and Lee 2017). This is due to

the fact that a company’s management can be exploited at the discretion through carrying out

goodwill impairment test opportunistically. This might be validated by allocation of goodwill to

all cash generating units along with computation of recoverable amount while there is a lack of

active prices for goodwill that with discretion subject (Watts and Zuo 2016).

Answer (vi):

After a detailed analysis, this has been gathered that certain difficult or confessing aspect

related to impairment is associated with the impairment indication. Despite of the fact that

indications are based on external as well as internal factors in alignment with the assets

impairment, the regularity of conducting such tests for goodwill along with some tangible assets

totally base on the managements discretion (Linnenluecke et al. 2015). Due to these factors there

is high chance that the management might carry out an opportunistic test in case there occurs any

change in the value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

Answer (vii):

It has been evident that impairment loss acts as a variation among an assets recoverable

amount of certain asset along with an assets carrying amount. The recoverable asset is high

among the value of fair asset disposal cost along with value-in-use. Fair value is explained by

means of the asset within the active market or sales agreement within which asset trading is

conducted or presence of important information in amount disclosure at which the company

might consider asset sales (Lubbe, Modack and Watson 2014). On the other hand, the value in

use might be deemed as present value of the upcoming cash inflows that is ascertained to be

gathered from a CGU or asset based on IAS 36.

Answer (viii):

IFRS 13 accounting standard, fair value is explained by means of the below points:

Within active market there is an asset value within the asset trading that is carried out

Sales agreement

Existence of better information in amount disclosure in which the companies that might

result in asset sales

Due to the same, fair value is deemed as selling price that is taken into account on the behalf

of both the seller and the purchaser through recognizing that all these parties are involved within

the free transactions. Several investments attained fair value that is explained on the behalf of the

market within which security trading is conducted. In addition, fair value indicates a company’s

liabilities and assets value in the occasion of financial statements of the subsidiary company that

is consolidated with a major company (M2.com.au., 2018). For example, in case of a company’s

stock that is trading within an exchange, the players within market offers a bid by asking price of

that share. In such case, the investors consider selling of stocks to the market leader in a bidding

Answer (vii):

It has been evident that impairment loss acts as a variation among an assets recoverable

amount of certain asset along with an assets carrying amount. The recoverable asset is high

among the value of fair asset disposal cost along with value-in-use. Fair value is explained by

means of the asset within the active market or sales agreement within which asset trading is

conducted or presence of important information in amount disclosure at which the company

might consider asset sales (Lubbe, Modack and Watson 2014). On the other hand, the value in

use might be deemed as present value of the upcoming cash inflows that is ascertained to be

gathered from a CGU or asset based on IAS 36.

Answer (viii):

IFRS 13 accounting standard, fair value is explained by means of the below points:

Within active market there is an asset value within the asset trading that is carried out

Sales agreement

Existence of better information in amount disclosure in which the companies that might

result in asset sales

Due to the same, fair value is deemed as selling price that is taken into account on the behalf

of both the seller and the purchaser through recognizing that all these parties are involved within

the free transactions. Several investments attained fair value that is explained on the behalf of the

market within which security trading is conducted. In addition, fair value indicates a company’s

liabilities and assets value in the occasion of financial statements of the subsidiary company that

is consolidated with a major company (M2.com.au., 2018). For example, in case of a company’s

stock that is trading within an exchange, the players within market offers a bid by asking price of

that share. In such case, the investors consider selling of stocks to the market leader in a bidding

8ADVANCED FINANCIAL ACCOUNTING

price while acquiring shares from any market player within ask price. Considering same this

might be referred that exchange can be a highly reliable method of making sure consideration of

shares fair value.

Part B:

Answer (i):

More than 50% of the companies employing US GAAP or IFRS re impacted as there are some

accounting changes. As per the status, the companies within US GAAP or IFRS have leased

commitments and assets around $3.3 million, among which 85% are mentioned within financial

position as these are considered as a form of operating leases (Sellhorn and Stier 2017). For

compensating the same, all the investors generally encompass the estimation that is inaccurate,

incomparable along with inconsistence. Due to this, it is gathered that certain previous

accounting standard did not succeed for indicating economic actuality.

Answer (ii):

In account to the previous accounting standards, most of the firms has indicated that more than

85% of leases consideration to the amount within operating leases along with that it never

depicted that is explained within the financial situation statement. Even if the operating leases

that was not mentioned in the annual report and there is gradual generation of real liabilities. For

this reason, while the financial crisis certain important retail companies turned out to be loss as

they could not deal with the new economic reality in a prompt manner (Sinclair and Keller

2014). Along with that, the companies have considerable fraction of commitments regarding

long term operating leases and their annual reports was being gradually lean. Therefore, the lease

liabilities of companies within off balance sheet arrangements has been more than 66 times in

comparison to debt values within the statement of balance sheet.

price while acquiring shares from any market player within ask price. Considering same this

might be referred that exchange can be a highly reliable method of making sure consideration of

shares fair value.

Part B:

Answer (i):

More than 50% of the companies employing US GAAP or IFRS re impacted as there are some

accounting changes. As per the status, the companies within US GAAP or IFRS have leased

commitments and assets around $3.3 million, among which 85% are mentioned within financial

position as these are considered as a form of operating leases (Sellhorn and Stier 2017). For

compensating the same, all the investors generally encompass the estimation that is inaccurate,

incomparable along with inconsistence. Due to this, it is gathered that certain previous

accounting standard did not succeed for indicating economic actuality.

Answer (ii):

In account to the previous accounting standards, most of the firms has indicated that more than

85% of leases consideration to the amount within operating leases along with that it never

depicted that is explained within the financial situation statement. Even if the operating leases

that was not mentioned in the annual report and there is gradual generation of real liabilities. For

this reason, while the financial crisis certain important retail companies turned out to be loss as

they could not deal with the new economic reality in a prompt manner (Sinclair and Keller

2014). Along with that, the companies have considerable fraction of commitments regarding

long term operating leases and their annual reports was being gradually lean. Therefore, the lease

liabilities of companies within off balance sheet arrangements has been more than 66 times in

comparison to debt values within the statement of balance sheet.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL ACCOUNTING

Answer (iii):

Prior system of accounting that considers lease might result in comparability loss (Cheng,

Peterson and Sherrill 2017). The aviation sector records most of its leases as a part of operating

lease and such record is not maintained within financial position statement. Therefore, an airline

company associated with leasing all the airline fleet is not the same as its competitors acquiring

all the fleets and the financial obligations in two types of these aviation companies are not the

same. This signifies that there is a great lack of level playing field within the aviation companies.

With emergence of a n innovative standard, all the leases might be recorded in asset form and

such leases might record them as a part of liability. Accordingly, it is anticipated that addressing

such issue is possible.

Answer (iv):

Any alterations within the accounting standard is likely to pose an impact on more than

half of listed companies and they are deemed to be renowned with every companies. The cause

behind this in that certain alterations can result in a lot of controversies long with this might lead

in warning impacts in alignment with negative economic impacts along with expenses associated

with variations within the system (Chang and Yen 2015). Moreover, certain alterations can have

increased impacts of commercial purposes. For instance, variations in banking covenants long

with contractual contracts linked with a firm annual report that includes profit targets to arrange

payment of bonus to employees or gearing ratio can be required in attaining revisions before

emergence of an innovative standard. Conversely, all the business departments require attaining

a viewpoint regarding changes Impact that considers accounting information technology, human

resource, finance along with investor relations department with asset procurement (Visvanathan

Answer (iii):

Prior system of accounting that considers lease might result in comparability loss (Cheng,

Peterson and Sherrill 2017). The aviation sector records most of its leases as a part of operating

lease and such record is not maintained within financial position statement. Therefore, an airline

company associated with leasing all the airline fleet is not the same as its competitors acquiring

all the fleets and the financial obligations in two types of these aviation companies are not the

same. This signifies that there is a great lack of level playing field within the aviation companies.

With emergence of a n innovative standard, all the leases might be recorded in asset form and

such leases might record them as a part of liability. Accordingly, it is anticipated that addressing

such issue is possible.

Answer (iv):

Any alterations within the accounting standard is likely to pose an impact on more than

half of listed companies and they are deemed to be renowned with every companies. The cause

behind this in that certain alterations can result in a lot of controversies long with this might lead

in warning impacts in alignment with negative economic impacts along with expenses associated

with variations within the system (Chang and Yen 2015). Moreover, certain alterations can have

increased impacts of commercial purposes. For instance, variations in banking covenants long

with contractual contracts linked with a firm annual report that includes profit targets to arrange

payment of bonus to employees or gearing ratio can be required in attaining revisions before

emergence of an innovative standard. Conversely, all the business departments require attaining

a viewpoint regarding changes Impact that considers accounting information technology, human

resource, finance along with investor relations department with asset procurement (Visvanathan

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL ACCOUNTING

2017). All these factors can lead to popularity. These are the factors that causes negative impact

on popularity of new accounting standards.

Answer (v):

With support to the new accounting standard, it is also gathered that most of the firms are

considered to be operating leases as a part of off-balance sheet aspects (Carvalho, Rodrigues and

Ferreira 2016). For this reason, the investors along with financial statement users could not attain

an increased insight regarding the company’s financial condition. This does not facilitate them to

contrast leasing of the company’s assets the purchasing assets of the firms. Conversely, this

innovative standard is anticipated to develop IFRS 16 along with that it is estimated that this

might greatly offset the expenses that can lead to highly informed decisions associated with

investment. His might be indicated that within lease devoid of purchase decision in better

manner as a fraction of the management (Su and Wells 2015).

2017). All these factors can lead to popularity. These are the factors that causes negative impact

on popularity of new accounting standards.

Answer (v):

With support to the new accounting standard, it is also gathered that most of the firms are

considered to be operating leases as a part of off-balance sheet aspects (Carvalho, Rodrigues and

Ferreira 2016). For this reason, the investors along with financial statement users could not attain

an increased insight regarding the company’s financial condition. This does not facilitate them to

contrast leasing of the company’s assets the purchasing assets of the firms. Conversely, this

innovative standard is anticipated to develop IFRS 16 along with that it is estimated that this

might greatly offset the expenses that can lead to highly informed decisions associated with

investment. His might be indicated that within lease devoid of purchase decision in better

manner as a fraction of the management (Su and Wells 2015).

11ADVANCED FINANCIAL ACCOUNTING

References:

Banker, R.D., Basu, S. and Byzalov, D., 2016. Implications of Impairment Decisions and Assets'

Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2), pp.41-67.

Bianchi, P., 2017. The economic importance of intangible assets. Routledge.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Bryan, L.E., 2017. Goodwill and Other Intangible Assets: An Exploratory Study into the

Effectiveness of the Accounting Standards Codification (thesis).

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The Recognition of Goodwill and Other

Intangible Assets in Business Combinations–The Portuguese Case. Australian Accounting

Review, 26(1), pp.4-20.

Chang, M.L. and Yen, T.Y., 2015. Does Reversal of Asset Impairment Loss Matter? Evidence

from China. International Research Journal of Applied Finance, 6(4), pp.197-222.

Cheng, Y., Peterson, D. and Sherrill, K., 2017. Admitting mistakes pays: the long term impact of

goodwill impairment write-offs on stock prices. Journal of Economics and Finance, 41(2),

pp.311-329.

Contractor, F., Yang, Y. and Gaur, A.S., 2016. Firm-specific intangible assets and subsidiary

profitability: The moderating role of distance, ownership strategy and subsidiary

experience. Journal of World Business, 51(6), pp.950-964.

Detzen, D., Wersborg, T.S.G. and Zülch, H., 2015. Bleak Weather for Sun-Shine AG: A Case

Study of Impairment of Assets. Issues in Accounting Education, 30(2), pp.18-39.

References:

Banker, R.D., Basu, S. and Byzalov, D., 2016. Implications of Impairment Decisions and Assets'

Cash-Flow Horizons for Conservatism Research. The Accounting Review, 92(2), pp.41-67.

Bianchi, P., 2017. The economic importance of intangible assets. Routledge.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Bryan, L.E., 2017. Goodwill and Other Intangible Assets: An Exploratory Study into the

Effectiveness of the Accounting Standards Codification (thesis).

Carvalho, C., Rodrigues, A.M. and Ferreira, C., 2016. The Recognition of Goodwill and Other

Intangible Assets in Business Combinations–The Portuguese Case. Australian Accounting

Review, 26(1), pp.4-20.

Chang, M.L. and Yen, T.Y., 2015. Does Reversal of Asset Impairment Loss Matter? Evidence

from China. International Research Journal of Applied Finance, 6(4), pp.197-222.

Cheng, Y., Peterson, D. and Sherrill, K., 2017. Admitting mistakes pays: the long term impact of

goodwill impairment write-offs on stock prices. Journal of Economics and Finance, 41(2),

pp.311-329.

Contractor, F., Yang, Y. and Gaur, A.S., 2016. Firm-specific intangible assets and subsidiary

profitability: The moderating role of distance, ownership strategy and subsidiary

experience. Journal of World Business, 51(6), pp.950-964.

Detzen, D., Wersborg, T.S.G. and Zülch, H., 2015. Bleak Weather for Sun-Shine AG: A Case

Study of Impairment of Assets. Issues in Accounting Education, 30(2), pp.18-39.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.