Analysis of IAS 36 and Asset Impairment for Myer Holdings Limited

VerifiedAdded on 2020/02/24

|7

|1615

|57

Report

AI Summary

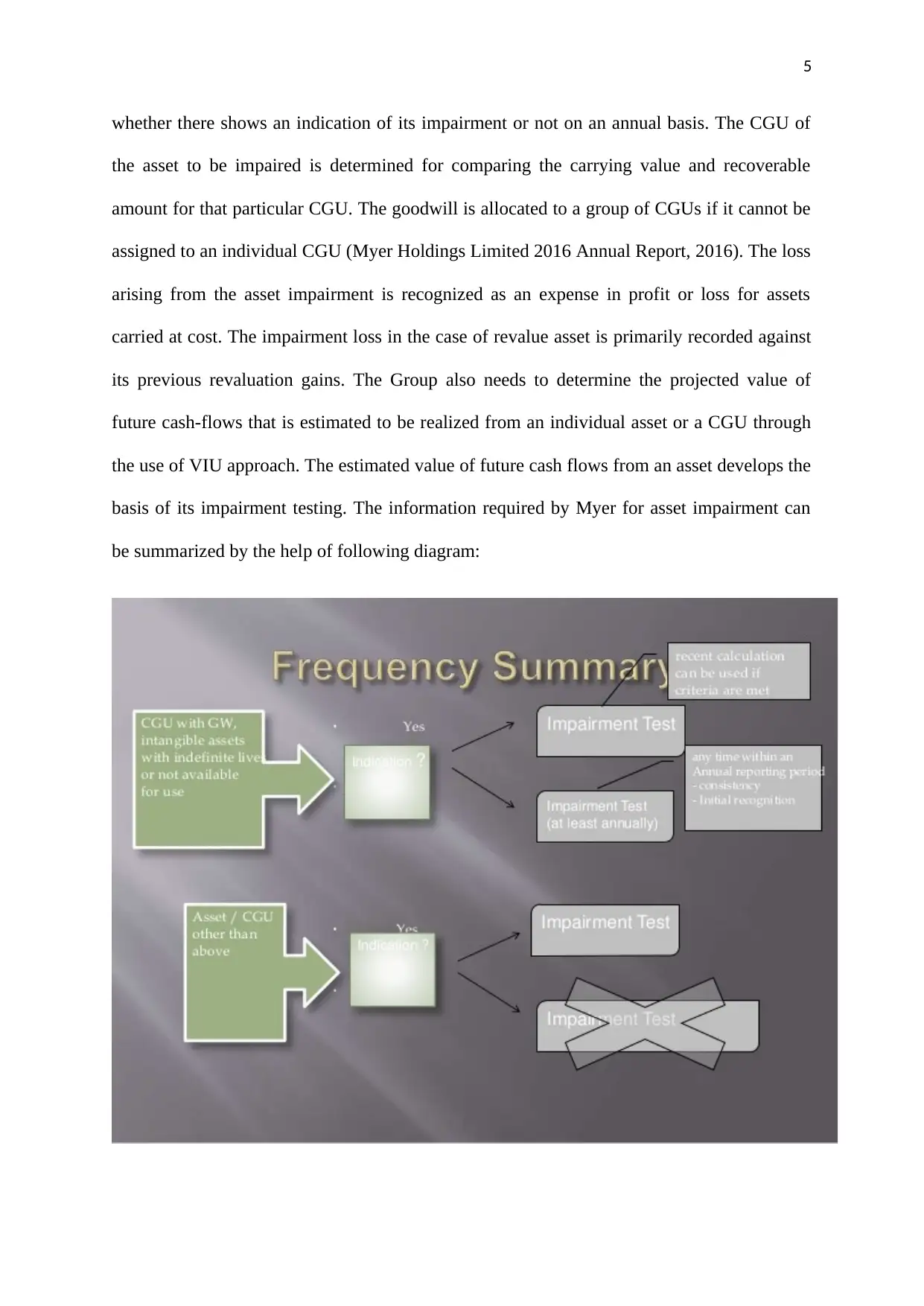

This report analyzes the asset impairment practices of Myer Holdings Limited, focusing on the application of IAS 36. The report details the process of determining asset impairment, including the division of assets into tangible and intangible categories, and the assessment of indicators suggesting impairment. It examines the methods used by Myer Holdings, such as the discounted cash flow model, to determine the recoverable amount of assets, particularly goodwill. The report highlights the importance of comparing the value in use with the recoverable amount to identify impairment losses. It also covers the data and information required for the impairment process, the role of both external and internal sources in gathering relevant information, and the flexibility of the management in analyzing the impairment of assets. The analysis concludes that the company effectively follows the procedures outlined in IAS 36 for asset impairment and advises continued adherence to these practices.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.