Asset Liability Management: Motivation and Techniques Analysis Report

VerifiedAdded on 2022/12/22

|6

|825

|55

Report

AI Summary

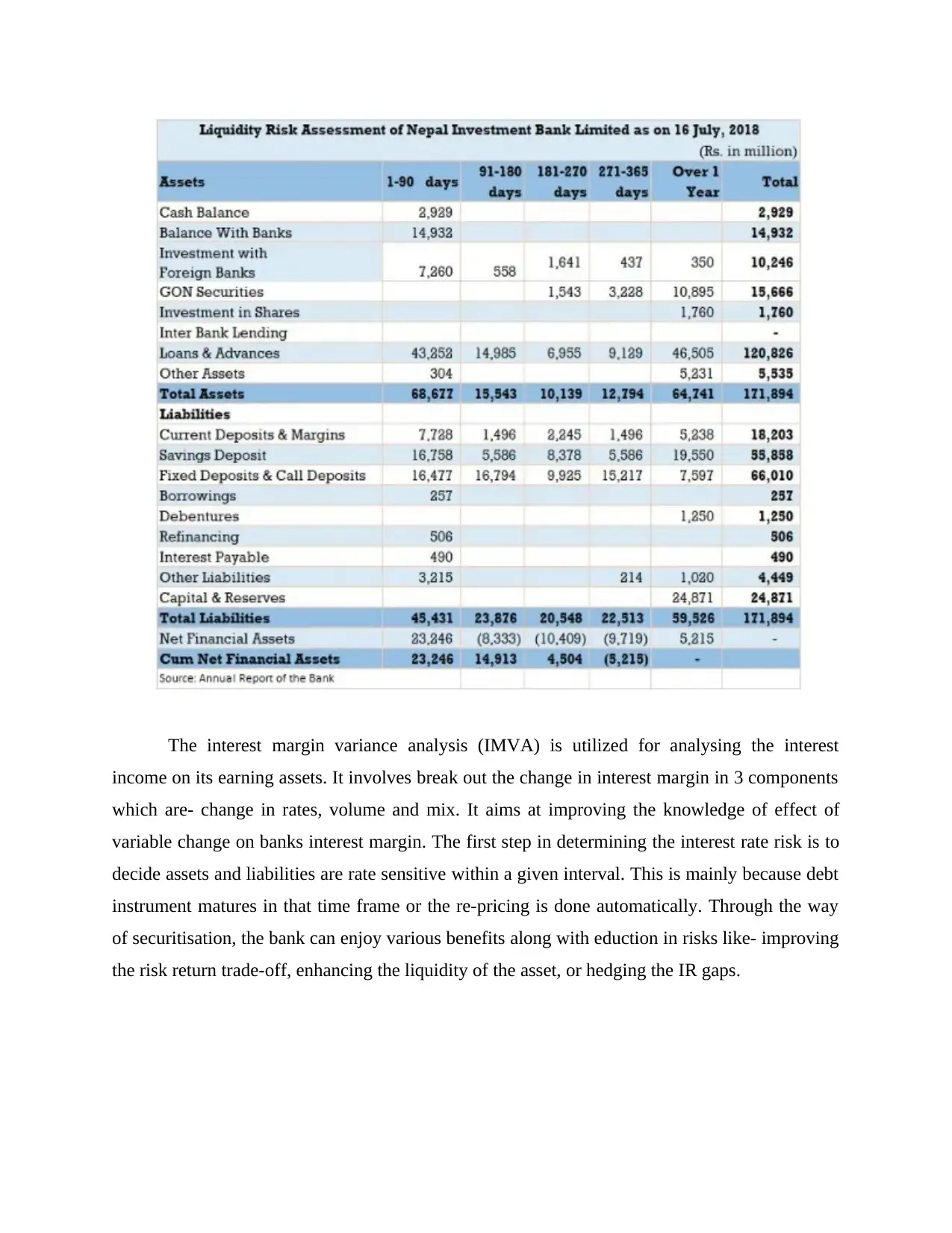

This report provides an overview of Asset Liability Management (ALM), focusing on its motivation and various techniques. It explores the management of interest rate risk and liquidity risk within financial institutions, emphasizing the significance of gap analysis and the net interest margin in assessing bank profitability. The report delves into the practical application of ALM strategies, including gap analysis and interest margin variance analysis (IMVA), illustrating how banks can mitigate risks and optimize their financial performance. It also examines the sources of liquidity and the impact of maturity mismatches on banks. The report concludes by highlighting the benefits of securitization in reducing risks and improving financial outcomes. The content is contributed by a student and available on Desklib for educational purposes.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.