MBS614 Taxation Principles: Analyzing CGT on Asset Transfer & Sale

VerifiedAdded on 2023/06/03

|6

|1149

|180

Report

AI Summary

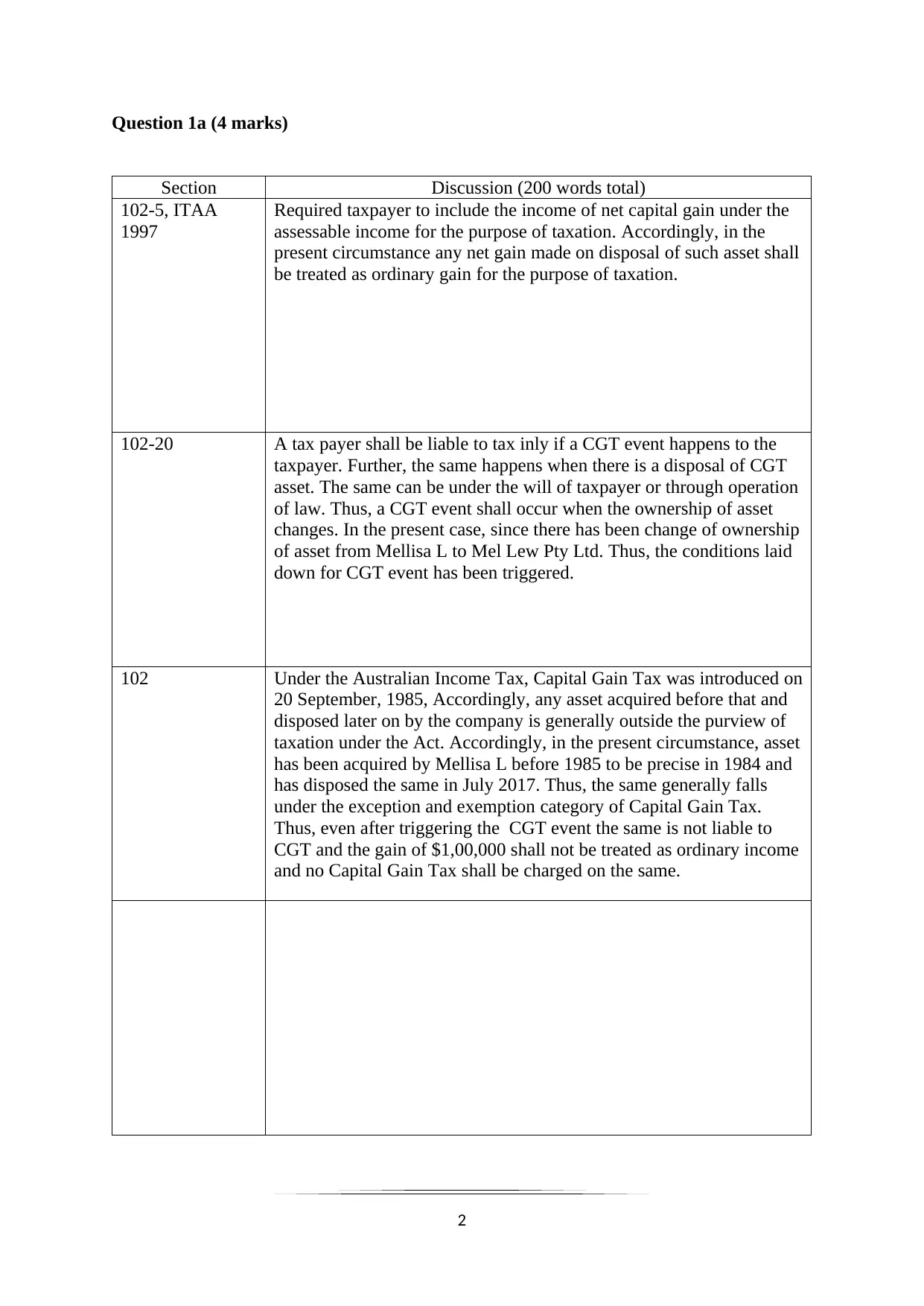

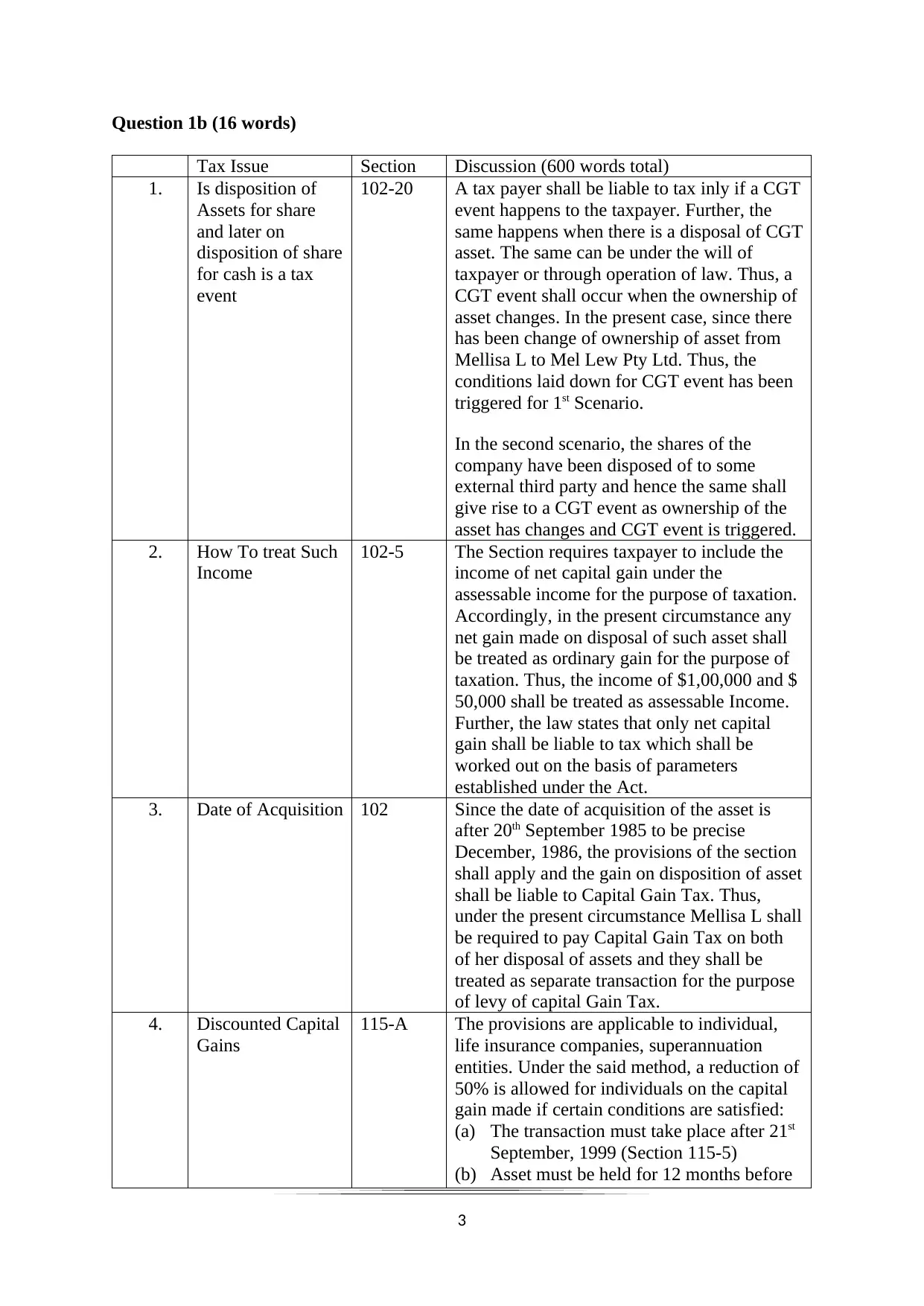

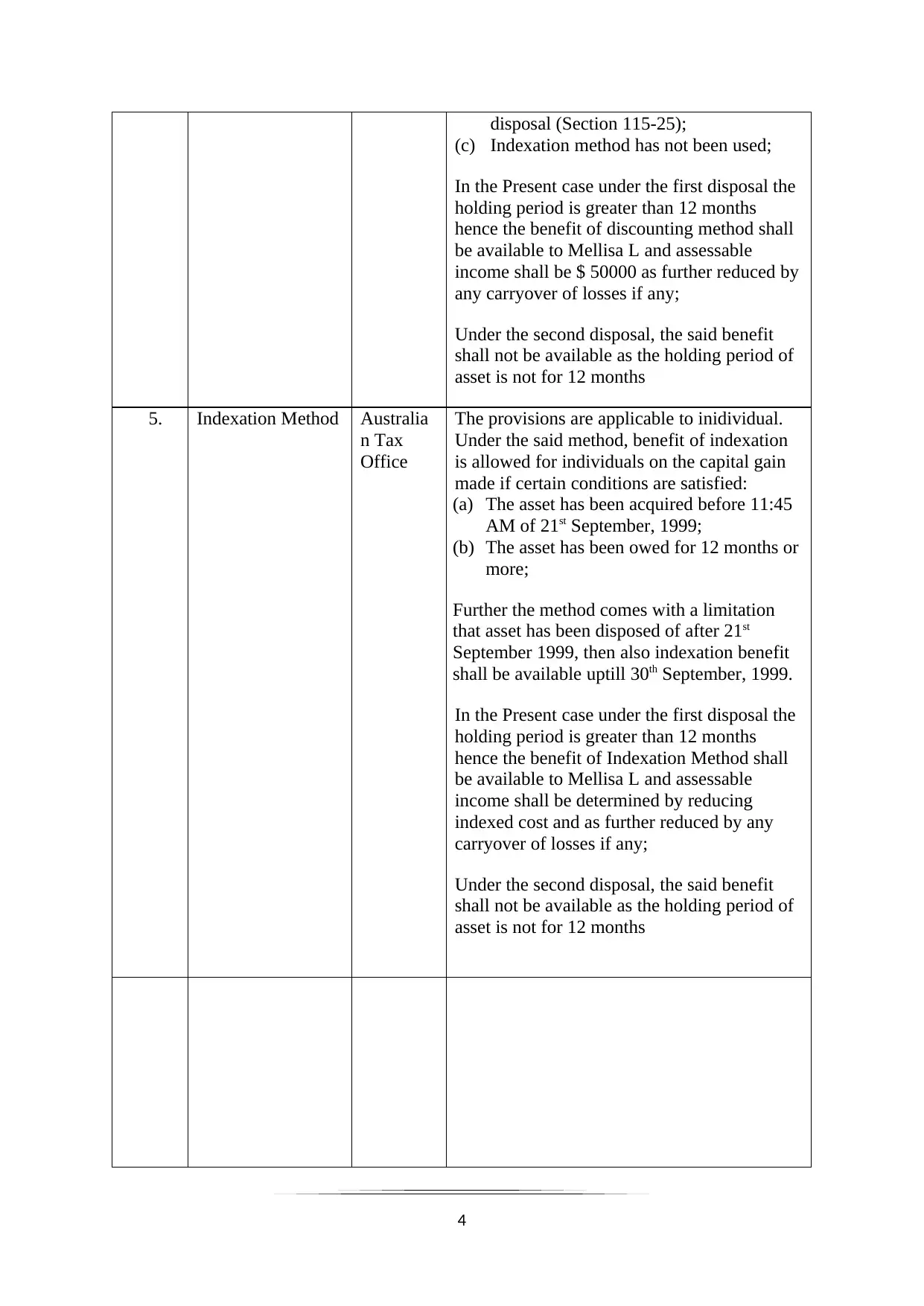

This report addresses the tax implications of asset transfers and share sales by Mellisa L to Mel Lew Pty Ltd, focusing on Capital Gains Tax (CGT) under Australian tax law. It examines two scenarios: the initial transfer of assets acquired before 1985 and a subsequent sale of shares acquired after 1986. The analysis considers whether CGT events are triggered, the applicability of discounted capital gains and indexation methods, and relevant sections of the Income Tax Assessment Act 1997. The report concludes that the initial asset transfer, due to pre-1985 acquisition, is generally exempt from CGT, while the later share sale is subject to CGT, with potential eligibility for the discount method based on holding period. The report references key legal precedents and legislation.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.