Wesfarmers' Asset Valuation: Application of Accounting Theory

VerifiedAdded on 2023/06/05

|10

|2704

|254

Report

AI Summary

This report provides an analysis of the asset valuation methods employed by Wesfarmers Limited, an ASX-listed retail leader, in accordance with international accounting standards. It explores different approaches to asset valuation, including the cost model and revaluation model as per IAS 16, and examines how Wesfarmers applies these methods to its tangible and intangible assets, such as property, plant, and equipment, as well as goodwill. The report also discusses the use of depreciation methods, specifically the straight-line method, and assesses how these valuation practices assist users of financial statements in making informed economic decisions, highlighting the importance of accurate asset valuation in reflecting a company's true financial position and profitability.

Accounting Theory

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.................................................................................................................................................3

Different Methods Used in Assets Valuation...............................................................................................3

Use of International accounting standards by Wesfarmers to value their assets........................................4

Use of Different Methods of Asset Valuation in Assisting the Users of Financial Statements.....................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

2

Introduction.................................................................................................................................................3

Different Methods Used in Assets Valuation...............................................................................................3

Use of International accounting standards by Wesfarmers to value their assets........................................4

Use of Different Methods of Asset Valuation in Assisting the Users of Financial Statements.....................6

Conclusion...................................................................................................................................................7

References...................................................................................................................................................8

2

Introduction

The process of asset valuation plays an important role in finance for determination of the

fair value of assets and thus determining the real worth of an entity. The different methods are

used for assets valuation in order to record its accurate value during the financial reporting

process. The valuation of assets by the use of an adequate method or approach is highly essential

for the business entities for analyzing its actual worth. The accurate valuation of assets is highly

essential as they are regarded as an important aspect of business as the balance sheet of a

company is developed on its basis. Balance sheet depicts the actual financial position of a

business and therefore the assets should be correctly valued during the financial reporting

process. In this context, the present report is developed for presenting an analysis and discussion

regarding the different method of asset valuation used by an ASX listed entity as per the

international accounting standards. It has been carried out by discussing the views of different

writers in relation to valuation method of assets in the context of the company selected. The

company selected for the purpose is Wesfarmers Limited, an Australian public listed company

known to be a leader in retail industry of Australia.

Different Methods Used in Assets Valuation

Assets valuation is regarded as an extremely important process for a business entity for

determining its actual worth by assessing its real profit and loss position. Proper valuation of

assets is extremely important to give fair information about the profitability position of a

business. It assists the managers in taking important cessions regarding the future strategies for

promoting the growth of a business. IASB (International Accounting Standards Board) has

developed and prescribed the different business entities adopting the international accounting

standards to value the assets on the basis of IAS 16 for fixed assets. The standard is specifically

developed for describing the methods that should be used by business for accounting of property,

plant and equipment. The standards has provided clarification regarding the different issues that

accountant can face in relation to valuing their fixed assets such as recognition, determination of

carrying amounts, depreciation charges and impairment losses (Cotter and Zimmer, 2003). The

fixed assets under IAS 16 should meet the following conditions to be adequately met:

An asset should provide future economic benefits to an entity

An asset cost should be reliably measured

An asset should be used for producing goods or services by an entity

This is the first step in the valuation of an asset which is followed by measuring the asset

value for their capitalization. As per the international accounting standards, an asset should be

initially measured on the cost that includes its purchase price, expenses related to its installation

and borrowing costs. The subsequent measurement of the fixed assets can be done after its initial

3

The process of asset valuation plays an important role in finance for determination of the

fair value of assets and thus determining the real worth of an entity. The different methods are

used for assets valuation in order to record its accurate value during the financial reporting

process. The valuation of assets by the use of an adequate method or approach is highly essential

for the business entities for analyzing its actual worth. The accurate valuation of assets is highly

essential as they are regarded as an important aspect of business as the balance sheet of a

company is developed on its basis. Balance sheet depicts the actual financial position of a

business and therefore the assets should be correctly valued during the financial reporting

process. In this context, the present report is developed for presenting an analysis and discussion

regarding the different method of asset valuation used by an ASX listed entity as per the

international accounting standards. It has been carried out by discussing the views of different

writers in relation to valuation method of assets in the context of the company selected. The

company selected for the purpose is Wesfarmers Limited, an Australian public listed company

known to be a leader in retail industry of Australia.

Different Methods Used in Assets Valuation

Assets valuation is regarded as an extremely important process for a business entity for

determining its actual worth by assessing its real profit and loss position. Proper valuation of

assets is extremely important to give fair information about the profitability position of a

business. It assists the managers in taking important cessions regarding the future strategies for

promoting the growth of a business. IASB (International Accounting Standards Board) has

developed and prescribed the different business entities adopting the international accounting

standards to value the assets on the basis of IAS 16 for fixed assets. The standard is specifically

developed for describing the methods that should be used by business for accounting of property,

plant and equipment. The standards has provided clarification regarding the different issues that

accountant can face in relation to valuing their fixed assets such as recognition, determination of

carrying amounts, depreciation charges and impairment losses (Cotter and Zimmer, 2003). The

fixed assets under IAS 16 should meet the following conditions to be adequately met:

An asset should provide future economic benefits to an entity

An asset cost should be reliably measured

An asset should be used for producing goods or services by an entity

This is the first step in the valuation of an asset which is followed by measuring the asset

value for their capitalization. As per the international accounting standards, an asset should be

initially measured on the cost that includes its purchase price, expenses related to its installation

and borrowing costs. The subsequent measurement of the fixed assets can be done after its initial

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recognition and measurement by the use of following two methods under IAS as stated as

follows:

Cost Model

The fixed assets of a company after its initial recognition can be measured with the use of

cost model as per international accounting standard. This valuation method has stated an asset

value to be measured at its cost less any accumulated depreciation and impairment losses. As

such, it can be said that the cost model measures the value of fixed assets at the historical prices.

It records the value of an asset on its net book value by charging the accumulated depreciation

mount.

Revaluation Model

On the other hand, this method of asset valuation which is also known as fair value

method which records an asset amount after revaluing it by accounting the depreciation amount.

Revalue amount can be regarded as the fair value of an asset on the date of its measurement that

is determined by considering ay accumulated depreciation or impairment losses. The method

revalues the assets at continuous time-interval such as on an annual basis. Thus, it can be stated

that an asset under this method is primarily recognized at cost but its amount changes due to any

upward or downward movement (IASC Foundation, 2018).

Depreciation Method

Depreciation can be regarded as the reduction in the value of an asset over its economic

useful life. The depreciation charges incurred are allocated to an asset on a systematic basis over

its remaining useful life. The method is used by a business entity for reflecting the pattern in

which the future economic benefits are expected to be realized by an entity through the use of its

asset resources. The changes that is expected to be occur in the future value of an asset on

account of deprecation shall be accounted as per IAS 8 and adjust it accordingly as per the

current and future period changes (Beranová, 2013).

Use of International accounting standards by Wesfarmers to value their

assets

On the basis of the information gained from the annual report of the Wesfarmers there are

two main board categories of assets maintain by the company. These two categories of assets are

tangible assets (Plant, Property, and equipment) and intangible assets (Goodwill and other

intangible assets).

Property, plant and equipment: The value of property, plant and equipment are initially

recognized at cost plus any expenses incurred to bring the assets to place of initial installation.

After the initial recognition, value of property, plant and equipment is subsequent recognised at

4

follows:

Cost Model

The fixed assets of a company after its initial recognition can be measured with the use of

cost model as per international accounting standard. This valuation method has stated an asset

value to be measured at its cost less any accumulated depreciation and impairment losses. As

such, it can be said that the cost model measures the value of fixed assets at the historical prices.

It records the value of an asset on its net book value by charging the accumulated depreciation

mount.

Revaluation Model

On the other hand, this method of asset valuation which is also known as fair value

method which records an asset amount after revaluing it by accounting the depreciation amount.

Revalue amount can be regarded as the fair value of an asset on the date of its measurement that

is determined by considering ay accumulated depreciation or impairment losses. The method

revalues the assets at continuous time-interval such as on an annual basis. Thus, it can be stated

that an asset under this method is primarily recognized at cost but its amount changes due to any

upward or downward movement (IASC Foundation, 2018).

Depreciation Method

Depreciation can be regarded as the reduction in the value of an asset over its economic

useful life. The depreciation charges incurred are allocated to an asset on a systematic basis over

its remaining useful life. The method is used by a business entity for reflecting the pattern in

which the future economic benefits are expected to be realized by an entity through the use of its

asset resources. The changes that is expected to be occur in the future value of an asset on

account of deprecation shall be accounted as per IAS 8 and adjust it accordingly as per the

current and future period changes (Beranová, 2013).

Use of International accounting standards by Wesfarmers to value their

assets

On the basis of the information gained from the annual report of the Wesfarmers there are

two main board categories of assets maintain by the company. These two categories of assets are

tangible assets (Plant, Property, and equipment) and intangible assets (Goodwill and other

intangible assets).

Property, plant and equipment: The value of property, plant and equipment are initially

recognized at cost plus any expenses incurred to bring the assets to place of initial installation.

After the initial recognition, value of property, plant and equipment is subsequent recognised at

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

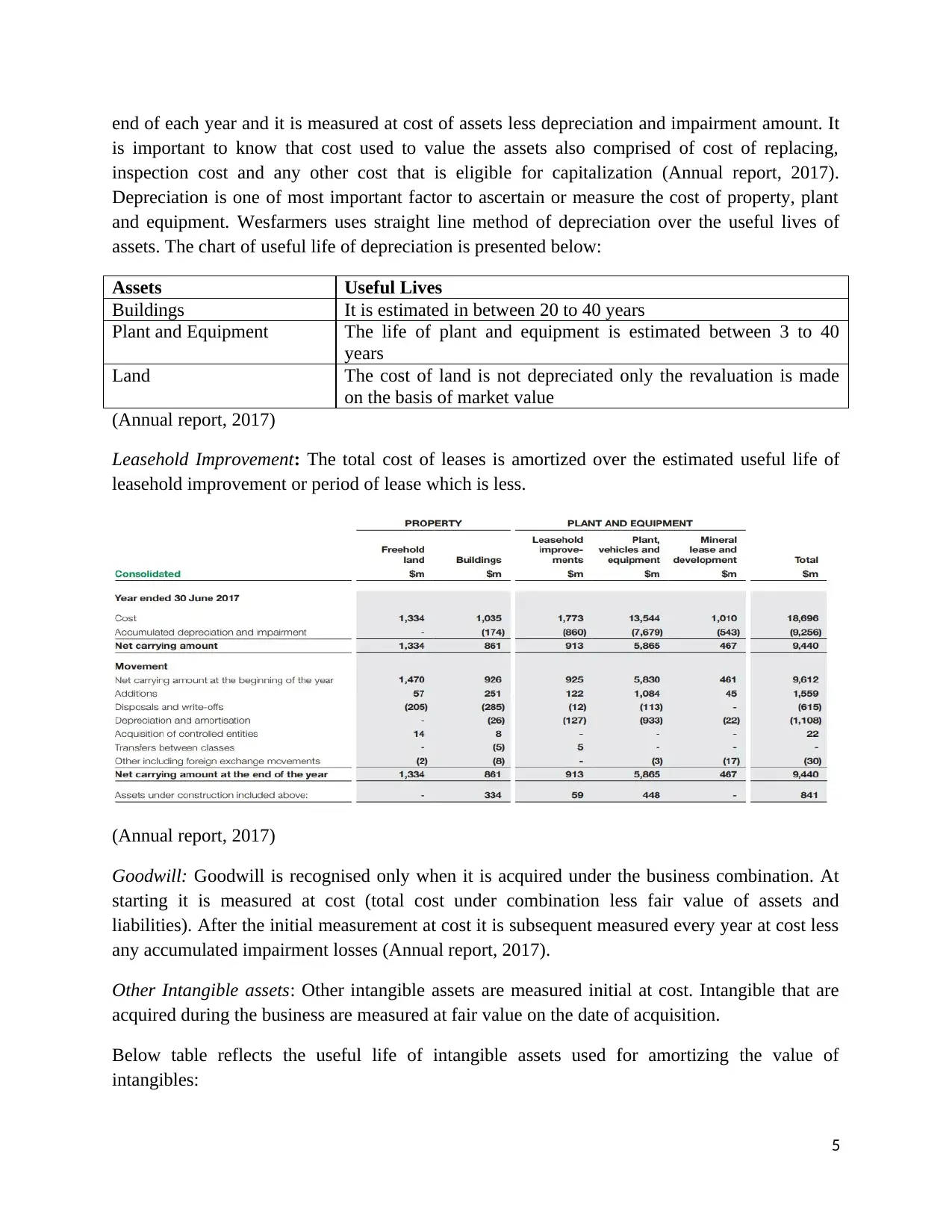

end of each year and it is measured at cost of assets less depreciation and impairment amount. It

is important to know that cost used to value the assets also comprised of cost of replacing,

inspection cost and any other cost that is eligible for capitalization (Annual report, 2017).

Depreciation is one of most important factor to ascertain or measure the cost of property, plant

and equipment. Wesfarmers uses straight line method of depreciation over the useful lives of

assets. The chart of useful life of depreciation is presented below:

Assets Useful Lives

Buildings It is estimated in between 20 to 40 years

Plant and Equipment The life of plant and equipment is estimated between 3 to 40

years

Land The cost of land is not depreciated only the revaluation is made

on the basis of market value

(Annual report, 2017)

Leasehold Improvement: The total cost of leases is amortized over the estimated useful life of

leasehold improvement or period of lease which is less.

(Annual report, 2017)

Goodwill: Goodwill is recognised only when it is acquired under the business combination. At

starting it is measured at cost (total cost under combination less fair value of assets and

liabilities). After the initial measurement at cost it is subsequent measured every year at cost less

any accumulated impairment losses (Annual report, 2017).

Other Intangible assets: Other intangible assets are measured initial at cost. Intangible that are

acquired during the business are measured at fair value on the date of acquisition.

Below table reflects the useful life of intangible assets used for amortizing the value of

intangibles:

5

is important to know that cost used to value the assets also comprised of cost of replacing,

inspection cost and any other cost that is eligible for capitalization (Annual report, 2017).

Depreciation is one of most important factor to ascertain or measure the cost of property, plant

and equipment. Wesfarmers uses straight line method of depreciation over the useful lives of

assets. The chart of useful life of depreciation is presented below:

Assets Useful Lives

Buildings It is estimated in between 20 to 40 years

Plant and Equipment The life of plant and equipment is estimated between 3 to 40

years

Land The cost of land is not depreciated only the revaluation is made

on the basis of market value

(Annual report, 2017)

Leasehold Improvement: The total cost of leases is amortized over the estimated useful life of

leasehold improvement or period of lease which is less.

(Annual report, 2017)

Goodwill: Goodwill is recognised only when it is acquired under the business combination. At

starting it is measured at cost (total cost under combination less fair value of assets and

liabilities). After the initial measurement at cost it is subsequent measured every year at cost less

any accumulated impairment losses (Annual report, 2017).

Other Intangible assets: Other intangible assets are measured initial at cost. Intangible that are

acquired during the business are measured at fair value on the date of acquisition.

Below table reflects the useful life of intangible assets used for amortizing the value of

intangibles:

5

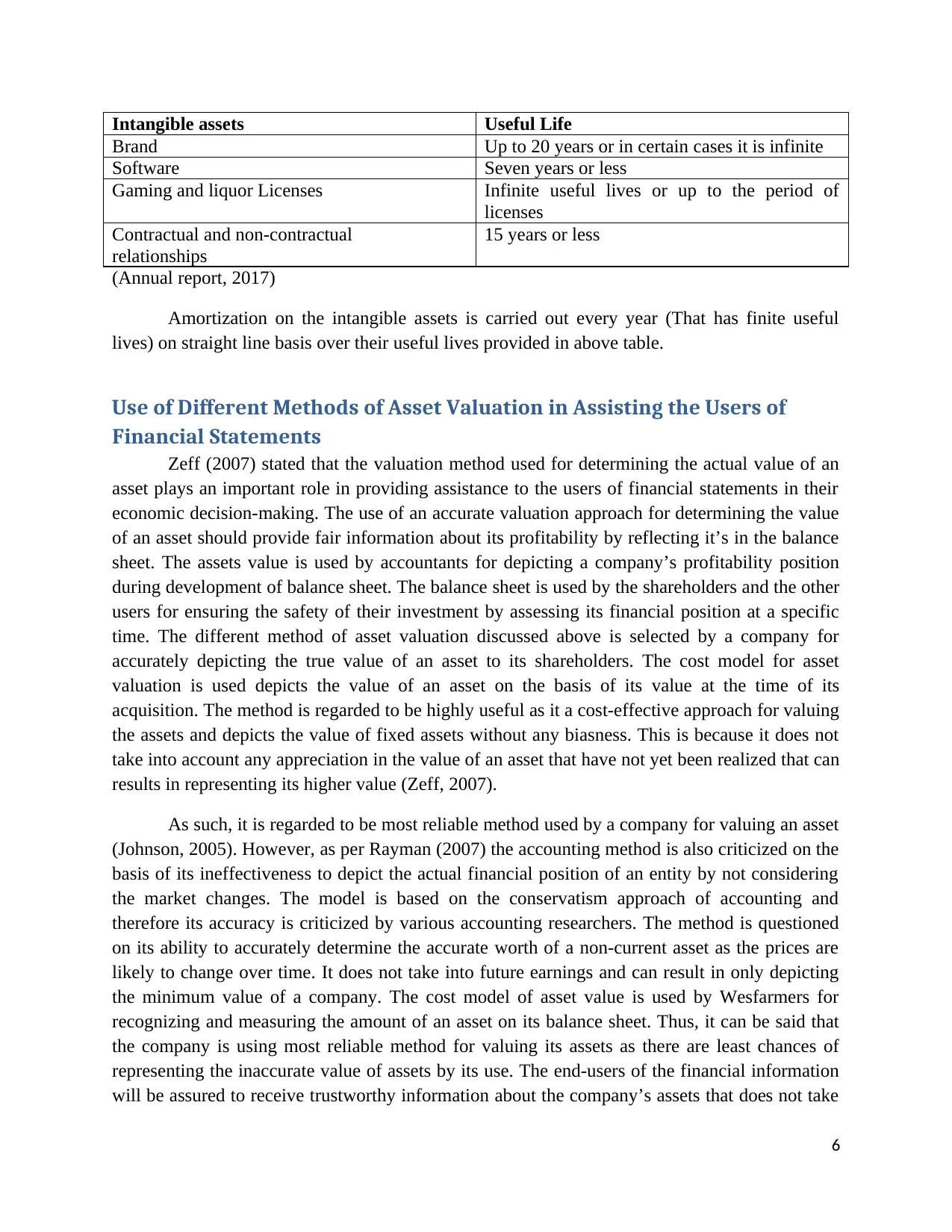

Intangible assets Useful Life

Brand Up to 20 years or in certain cases it is infinite

Software Seven years or less

Gaming and liquor Licenses Infinite useful lives or up to the period of

licenses

Contractual and non-contractual

relationships

15 years or less

(Annual report, 2017)

Amortization on the intangible assets is carried out every year (That has finite useful

lives) on straight line basis over their useful lives provided in above table.

Use of Different Methods of Asset Valuation in Assisting the Users of

Financial Statements

Zeff (2007) stated that the valuation method used for determining the actual value of an

asset plays an important role in providing assistance to the users of financial statements in their

economic decision-making. The use of an accurate valuation approach for determining the value

of an asset should provide fair information about its profitability by reflecting it’s in the balance

sheet. The assets value is used by accountants for depicting a company’s profitability position

during development of balance sheet. The balance sheet is used by the shareholders and the other

users for ensuring the safety of their investment by assessing its financial position at a specific

time. The different method of asset valuation discussed above is selected by a company for

accurately depicting the true value of an asset to its shareholders. The cost model for asset

valuation is used depicts the value of an asset on the basis of its value at the time of its

acquisition. The method is regarded to be highly useful as it a cost-effective approach for valuing

the assets and depicts the value of fixed assets without any biasness. This is because it does not

take into account any appreciation in the value of an asset that have not yet been realized that can

results in representing its higher value (Zeff, 2007).

As such, it is regarded to be most reliable method used by a company for valuing an asset

(Johnson, 2005). However, as per Rayman (2007) the accounting method is also criticized on the

basis of its ineffectiveness to depict the actual financial position of an entity by not considering

the market changes. The model is based on the conservatism approach of accounting and

therefore its accuracy is criticized by various accounting researchers. The method is questioned

on its ability to accurately determine the accurate worth of a non-current asset as the prices are

likely to change over time. It does not take into future earnings and can result in only depicting

the minimum value of a company. The cost model of asset value is used by Wesfarmers for

recognizing and measuring the amount of an asset on its balance sheet. Thus, it can be said that

the company is using most reliable method for valuing its assets as there are least chances of

representing the inaccurate value of assets by its use. The end-users of the financial information

will be assured to receive trustworthy information about the company’s assets that does not take

6

Brand Up to 20 years or in certain cases it is infinite

Software Seven years or less

Gaming and liquor Licenses Infinite useful lives or up to the period of

licenses

Contractual and non-contractual

relationships

15 years or less

(Annual report, 2017)

Amortization on the intangible assets is carried out every year (That has finite useful

lives) on straight line basis over their useful lives provided in above table.

Use of Different Methods of Asset Valuation in Assisting the Users of

Financial Statements

Zeff (2007) stated that the valuation method used for determining the actual value of an

asset plays an important role in providing assistance to the users of financial statements in their

economic decision-making. The use of an accurate valuation approach for determining the value

of an asset should provide fair information about its profitability by reflecting it’s in the balance

sheet. The assets value is used by accountants for depicting a company’s profitability position

during development of balance sheet. The balance sheet is used by the shareholders and the other

users for ensuring the safety of their investment by assessing its financial position at a specific

time. The different method of asset valuation discussed above is selected by a company for

accurately depicting the true value of an asset to its shareholders. The cost model for asset

valuation is used depicts the value of an asset on the basis of its value at the time of its

acquisition. The method is regarded to be highly useful as it a cost-effective approach for valuing

the assets and depicts the value of fixed assets without any biasness. This is because it does not

take into account any appreciation in the value of an asset that have not yet been realized that can

results in representing its higher value (Zeff, 2007).

As such, it is regarded to be most reliable method used by a company for valuing an asset

(Johnson, 2005). However, as per Rayman (2007) the accounting method is also criticized on the

basis of its ineffectiveness to depict the actual financial position of an entity by not considering

the market changes. The model is based on the conservatism approach of accounting and

therefore its accuracy is criticized by various accounting researchers. The method is questioned

on its ability to accurately determine the accurate worth of a non-current asset as the prices are

likely to change over time. It does not take into future earnings and can result in only depicting

the minimum value of a company. The cost model of asset value is used by Wesfarmers for

recognizing and measuring the amount of an asset on its balance sheet. Thus, it can be said that

the company is using most reliable method for valuing its assets as there are least chances of

representing the inaccurate value of assets by its use. The end-users of the financial information

will be assured to receive trustworthy information about the company’s assets that does not take

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

into account any appreciation in the value based on future change in their values. However, the

company should also take into account the significant drawbacks that exist with the use of such

method of accounting (Rayman, 2007).

As such, the company is recommended to adopt the use of revaluation model of cost

accounting in addition with the cost model to overcome its limitations. Taylor (2012) stated that

the IASB is also directing the business entities adopting international accounting standards to

adopt the use of revaluation model over the cost model. This is mainly placed emphasis to

improve stewardship and accountability in the financial reporting process as per the stewardship

theory of accounting. It has been argued by different accounting researchers such as Casta (2003)

on the basis of stewardship theory of accounting that revaluation model is more reliable approach

to measure the value of an asset as it helps in improving the accountability in the financial

reporting. This is because it reflects the fair value of an asset by taking into account the

appreciation in its value that can occur in the future period of time. However, the method is also

criticized on the basis of increasing probability of depicting manipulated financial information to

the end-users. This is because it takes into account the unrealized gains or losses associated with

an asset that may fail to reflect the true value of an asset (Casta, 2003).

Wesfarmers has adopted the use of straight line method of depreciation for measuring the

value of an asset. On the basis of Ball (2006) it is stated to be the most basic method used by

business for calculating depreciation. However, the main criticism against the method is that it

does not consider the repair expenditure and is not useful for valuing assets that have

unpredictable useful life. The method is regarded to be ineffective for valuing the costly assets

such as plant and equipment. In this context, the company is recommended to adopt the use of

declining balance method that writes off depreciation costs on quickly basis and also reduce the

exposure to tax. Thus, it is recommended to the company on the basis of discussing the various

benefits and critics of different asset valuation model that it should adopt the use of debt

accounting model to provide the end-users with right kind of accounting information. This is

essential as the investment decisions are largely based on the economic value of an entity that is

predicted largely on the basis of total worth of its asset base (Ball, 2006).

Conclusion

On the basis of overall analysis of Wesfarmers annual report in relation to methods

adopted to value the assets of the company it has been found that company uses cost method to

value the tangible assets as well as intangibles assets except the assets that are acquired during

the business combination. Straight line method is used to depreciation or amortized the cost

value of assets up to their useful life. Wesfarmers uses international accounting standards IAS 16

and IAS 38 to measure the value of assets in their books of accounts.

7

company should also take into account the significant drawbacks that exist with the use of such

method of accounting (Rayman, 2007).

As such, the company is recommended to adopt the use of revaluation model of cost

accounting in addition with the cost model to overcome its limitations. Taylor (2012) stated that

the IASB is also directing the business entities adopting international accounting standards to

adopt the use of revaluation model over the cost model. This is mainly placed emphasis to

improve stewardship and accountability in the financial reporting process as per the stewardship

theory of accounting. It has been argued by different accounting researchers such as Casta (2003)

on the basis of stewardship theory of accounting that revaluation model is more reliable approach

to measure the value of an asset as it helps in improving the accountability in the financial

reporting. This is because it reflects the fair value of an asset by taking into account the

appreciation in its value that can occur in the future period of time. However, the method is also

criticized on the basis of increasing probability of depicting manipulated financial information to

the end-users. This is because it takes into account the unrealized gains or losses associated with

an asset that may fail to reflect the true value of an asset (Casta, 2003).

Wesfarmers has adopted the use of straight line method of depreciation for measuring the

value of an asset. On the basis of Ball (2006) it is stated to be the most basic method used by

business for calculating depreciation. However, the main criticism against the method is that it

does not consider the repair expenditure and is not useful for valuing assets that have

unpredictable useful life. The method is regarded to be ineffective for valuing the costly assets

such as plant and equipment. In this context, the company is recommended to adopt the use of

declining balance method that writes off depreciation costs on quickly basis and also reduce the

exposure to tax. Thus, it is recommended to the company on the basis of discussing the various

benefits and critics of different asset valuation model that it should adopt the use of debt

accounting model to provide the end-users with right kind of accounting information. This is

essential as the investment decisions are largely based on the economic value of an entity that is

predicted largely on the basis of total worth of its asset base (Ball, 2006).

Conclusion

On the basis of overall analysis of Wesfarmers annual report in relation to methods

adopted to value the assets of the company it has been found that company uses cost method to

value the tangible assets as well as intangibles assets except the assets that are acquired during

the business combination. Straight line method is used to depreciation or amortized the cost

value of assets up to their useful life. Wesfarmers uses international accounting standards IAS 16

and IAS 38 to measure the value of assets in their books of accounts.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Annual report. 2017. Wesfarmers. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed on: 7 October, 2018].

Ball, R. 2006. International Financial Reporting Standards (IFRS): Pros and cons for investors.

Accounting and Business Research 36, pp. 5–27.

Beranová, M. 2013. The Problem Of Accounting Methods In Company Valuation. ACTA LXI

(4), pp. 867-872.

Casta, J. 2003. Does fair value accounting provide a better representation of a company?

[Online]. Available at: https://halshs.archives-ouvertes.fr/halshs-00170461/document [Accessed

on: 7 October 2018].

Cotter, J., & Zimmer, I. 2003. Disclosure versus recognition: The case of asset revaluations.

Asia-Pacific Journal of Accounting and Economics 10 (1), pp. 81-99.

IASC Foundation. 2018. IAS 16 Property, Plant and Equipment. [Online]. Available at:

http://www.tagi.com/UploadFiles/IFRS_AND_IASB_Standards/IAS16.pdf [Accessed on: 7

October 2018].

Johnson, L. T. 2005. Relevance and reliability. The FASB Report.

Rayman, R. 2007. Fair Value Accounting and the Present Value Fallacy: The Need for an

Alternative Conceptual Framework. British Accounting Review 39(3), pp.211-225.

Taylor, C. 2012. Accountant And User Perceptions Of Fair Value Accounting: Evidence From

Fij. Global Journal Of Business Research 6(3), pp. 93-102.

Zeff, S. A. 2007. The SEC rules historical cost accounting: 1934 to the 1970s. Accounting and

Business Research 1, pp. 1–14.

8

Annual report. 2017. Wesfarmers. [Online]. Available at:

https://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed on: 7 October, 2018].

Ball, R. 2006. International Financial Reporting Standards (IFRS): Pros and cons for investors.

Accounting and Business Research 36, pp. 5–27.

Beranová, M. 2013. The Problem Of Accounting Methods In Company Valuation. ACTA LXI

(4), pp. 867-872.

Casta, J. 2003. Does fair value accounting provide a better representation of a company?

[Online]. Available at: https://halshs.archives-ouvertes.fr/halshs-00170461/document [Accessed

on: 7 October 2018].

Cotter, J., & Zimmer, I. 2003. Disclosure versus recognition: The case of asset revaluations.

Asia-Pacific Journal of Accounting and Economics 10 (1), pp. 81-99.

IASC Foundation. 2018. IAS 16 Property, Plant and Equipment. [Online]. Available at:

http://www.tagi.com/UploadFiles/IFRS_AND_IASB_Standards/IAS16.pdf [Accessed on: 7

October 2018].

Johnson, L. T. 2005. Relevance and reliability. The FASB Report.

Rayman, R. 2007. Fair Value Accounting and the Present Value Fallacy: The Need for an

Alternative Conceptual Framework. British Accounting Review 39(3), pp.211-225.

Taylor, C. 2012. Accountant And User Perceptions Of Fair Value Accounting: Evidence From

Fij. Global Journal Of Business Research 6(3), pp. 93-102.

Zeff, S. A. 2007. The SEC rules historical cost accounting: 1934 to the 1970s. Accounting and

Business Research 1, pp. 1–14.

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.