Accounting for Fair Valuation, Intangibles and Employee Benefits

VerifiedAdded on 2020/04/07

|9

|2159

|41

Homework Assignment

AI Summary

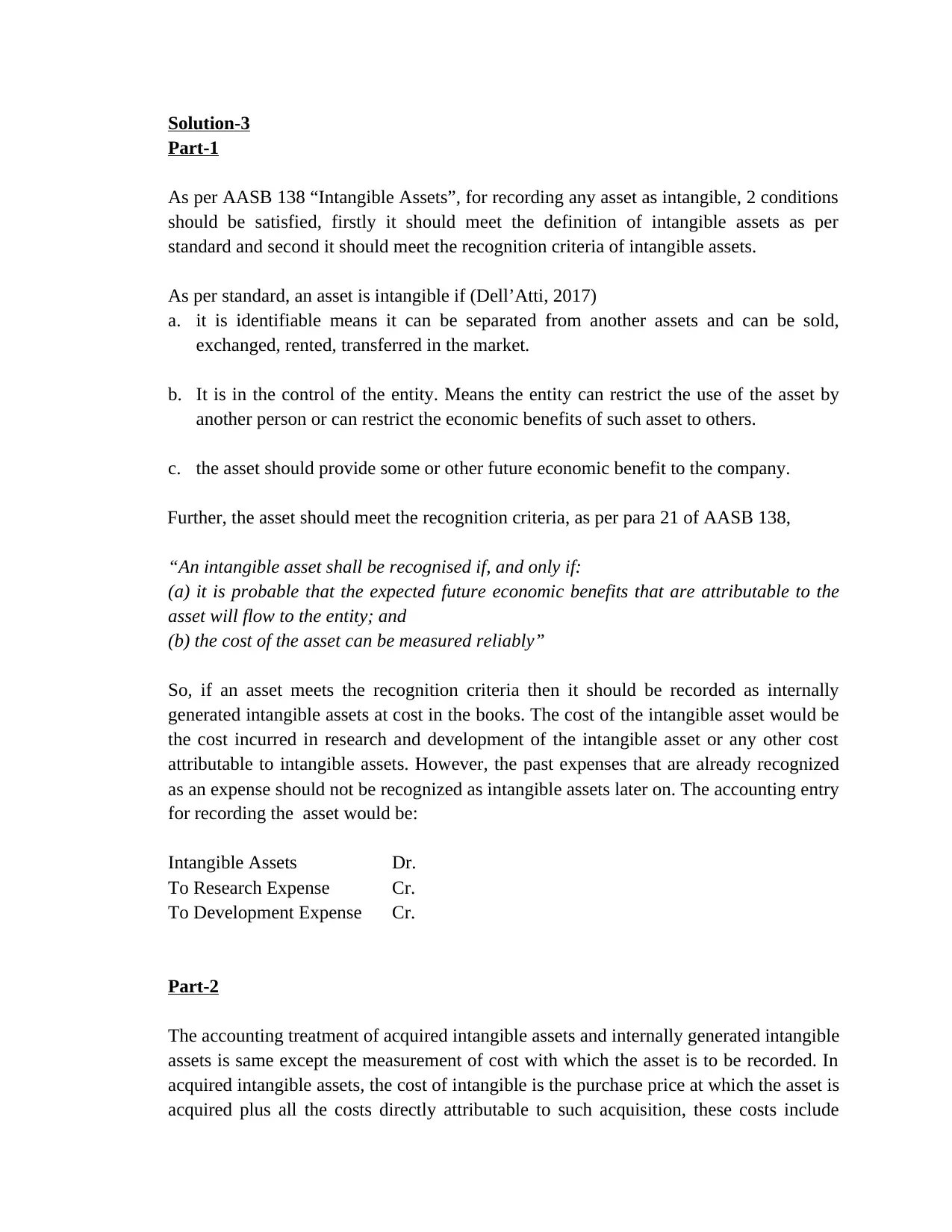

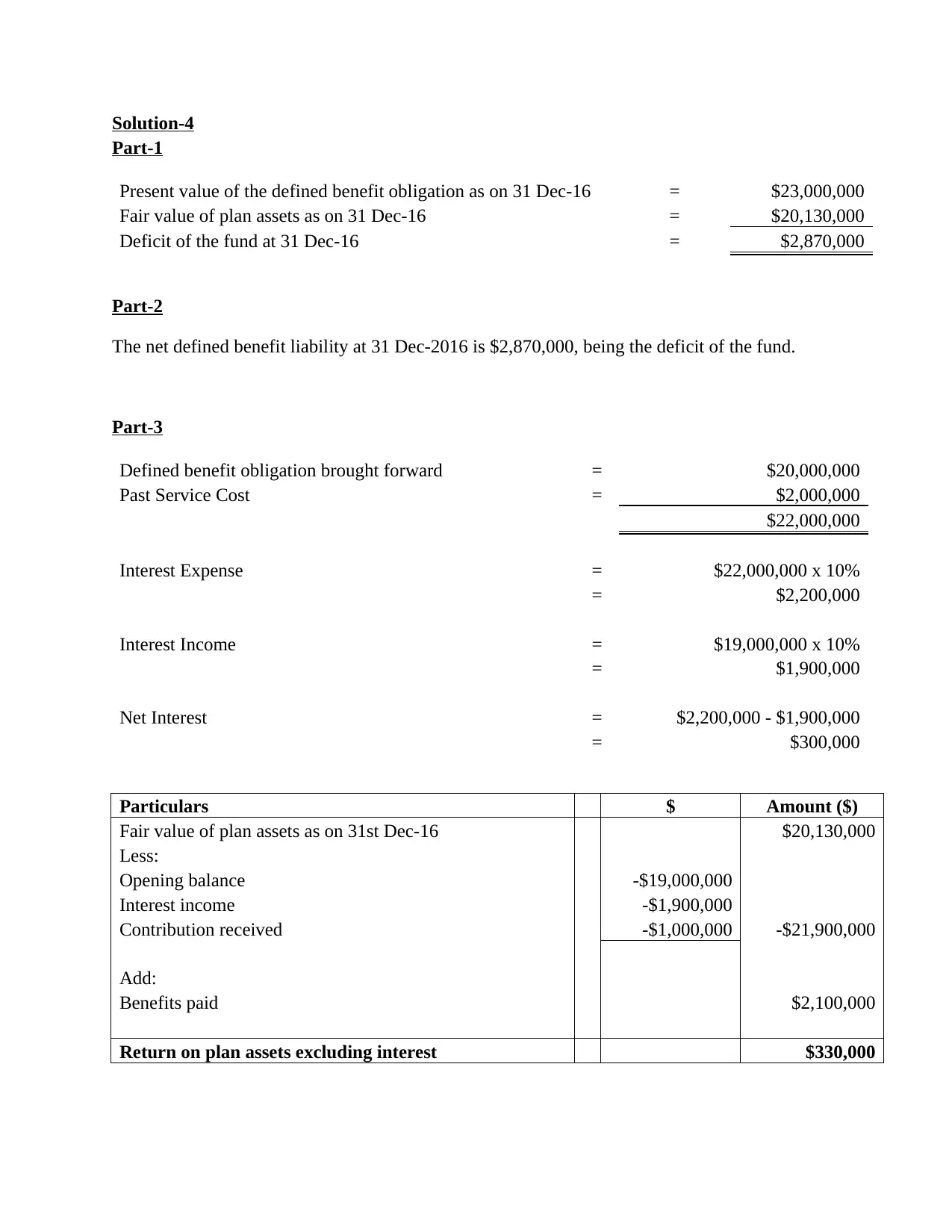

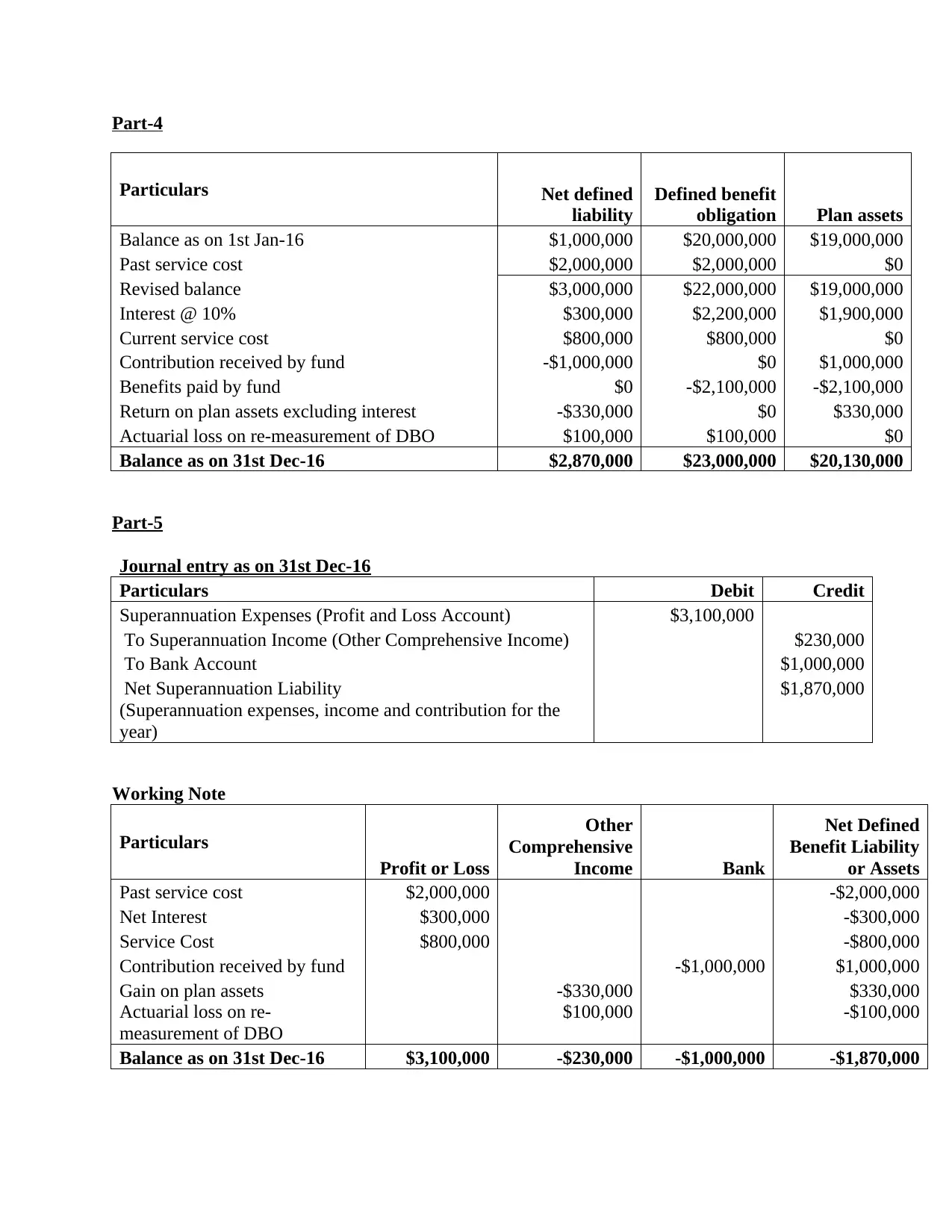

This assignment solution addresses key aspects of accounting, including the fair valuation of assets according to AASB 116, covering both cost and revaluation models. It provides journal entries for asset valuation, depreciation, and revaluation surplus or loss. The solution further delves into intangible assets as per AASB 138, differentiating between acquired and internally generated assets and discussing accounting treatments. The assignment also examines employee benefits, specifically defined benefit obligations, calculating present values, net liabilities, and related journal entries for superannuation expenses, contributions, and actuarial gains/losses. It provides detailed workings and calculations, including the impact of past service costs, interest, and plan asset returns, offering a comprehensive understanding of these financial accounting topics.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.