Double Ink Printers Audit Report: Assurance & Compliance Diploma

VerifiedAdded on 2023/06/13

|11

|2960

|153

Report

AI Summary

This document presents a detailed solution to an assignment related to an Audit, Assurance & Compliance Diploma, focusing on the auditing process within the Australian context, guided by the Corporation Acts 2001 and Auditing Standards set by the AUASB. It discusses the application of ASA 300 and ISA 300 concerning financial audit planning, the role of expert auditors as per ASA 600, and the importance of evaluating the entity's environment using ASA 315, particularly in the case of Double Ink Printers Limited (DIPL). The report emphasizes the necessity of IT expertise in auditing firms with advanced IT systems and addresses the concept of materiality in financial statements, outlining factors affecting materiality levels and benchmarks for determining them. It also highlights the significance of considering the collective impact of small errors and incorrect statements during the auditing process, providing a comprehensive overview of the factors influencing the preliminary figure for materiality of DIPL.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

AUDIT, ASSURANCE & COMPLIANCE

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

AUDIT, ASSURANCE & COMPLIANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIPL

Answer 1

The auditing process and the big firms in Australia are directed by the provisions of the

Corporation Acts, 2001 which is the only Act which is being discussed in the document

below. The section 336 of The Corporation Act, 2001 is taken into adherence by the auditors

while auditing the company. This act has mentioned all the necessary rules and regulations in

the form of Auditing Standards which are needed to be kept in mind while preparing the audit

file. The Auditing and Assurance Standards Board (AUASB) is the formulation body which

makes the Auditing Standards which are to be taken into consideration by the auditors while

preparing the report (Manoharan, 2011).

ASA 300 and ISA 300 have the same subject or topic being narrated about the planning of

the compiled financial audit report which is issued with the accordance to International

standards of auditing AUASB. ASA 30 states that an auditor of the financial report should

formulate his plan and remember his responsibility while auditing the statement. If an auditor

has a well planned and responsible method to perform an audit, then he will be able to

complete his work in the most effective and efficient manner. It is the decision of the auditor

whether to use the advice and services of an expert or not as an advice may help the auditor

to improve the quality of the work.

The advice or help of an expert auditor (ASA 600) is also stated in the AUSAB to teach the

other auditors that whether they need the help and assistance of an expert auditor while

preparing the audit report of a particular firm. It also helps the incompetent auditors to look

and learn by seeing the adequacy of the work which is initiated by the expert auditors while

preparing audit report of the firm (Lapsley, 2012). An expert is an individual who is said to

have sufficient essential skills and understanding after completing his necessary professional

qualifications, and who also gives important advice on the matters related or not related to

accounting and auditing (Matthew, 2015). If the inexperienced auditor finds that he is not

able to fulfil the requirements of the work then he should positively take help and advice

from a senior and much-experienced auditor for completing his work in a professional

manner. The auditor decides the method or way in which the expert or experienced auditor

will be carrying out or helping for the audit process (Livne, 2015).

ASA 315 may be helpful for the auditors to evaluate the entity and the environment of the

firm which need to be audited. It also helps the auditor to find whether he needs an expert

auditor for guidance or not. ASA 315 helps the auditor to analyze the firm’s environment and

Answer 1

The auditing process and the big firms in Australia are directed by the provisions of the

Corporation Acts, 2001 which is the only Act which is being discussed in the document

below. The section 336 of The Corporation Act, 2001 is taken into adherence by the auditors

while auditing the company. This act has mentioned all the necessary rules and regulations in

the form of Auditing Standards which are needed to be kept in mind while preparing the audit

file. The Auditing and Assurance Standards Board (AUASB) is the formulation body which

makes the Auditing Standards which are to be taken into consideration by the auditors while

preparing the report (Manoharan, 2011).

ASA 300 and ISA 300 have the same subject or topic being narrated about the planning of

the compiled financial audit report which is issued with the accordance to International

standards of auditing AUASB. ASA 30 states that an auditor of the financial report should

formulate his plan and remember his responsibility while auditing the statement. If an auditor

has a well planned and responsible method to perform an audit, then he will be able to

complete his work in the most effective and efficient manner. It is the decision of the auditor

whether to use the advice and services of an expert or not as an advice may help the auditor

to improve the quality of the work.

The advice or help of an expert auditor (ASA 600) is also stated in the AUSAB to teach the

other auditors that whether they need the help and assistance of an expert auditor while

preparing the audit report of a particular firm. It also helps the incompetent auditors to look

and learn by seeing the adequacy of the work which is initiated by the expert auditors while

preparing audit report of the firm (Lapsley, 2012). An expert is an individual who is said to

have sufficient essential skills and understanding after completing his necessary professional

qualifications, and who also gives important advice on the matters related or not related to

accounting and auditing (Matthew, 2015). If the inexperienced auditor finds that he is not

able to fulfil the requirements of the work then he should positively take help and advice

from a senior and much-experienced auditor for completing his work in a professional

manner. The auditor decides the method or way in which the expert or experienced auditor

will be carrying out or helping for the audit process (Livne, 2015).

ASA 315 may be helpful for the auditors to evaluate the entity and the environment of the

firm which need to be audited. It also helps the auditor to find whether he needs an expert

auditor for guidance or not. ASA 315 helps the auditor to analyze the firm’s environment and

DIPL

thus helping him to identify the inappropriate statements of the firm while auditing. The case

of Double ink printers limited is having the same necessity of analyzing and evaluating all the

account balances, types of transactions and the conditions of the firm so that the auditor can

be advised if he needs the help of an expert auditor in accordance to the ASA 315 (Merchant,

2012). According to ASA 600, an auditor faces no change in his situation of completing the

audit process which keeps it unchanged and unaltered no matter if an expert auditors help is

taken or not (Kaplan Kaplan, 2011). Even if the auditor of the firm DIPL takes help from an

expert or not, he needs to still needed to find out the data and give an opinion on the financial

performance and position of the firm.

While checking the background of the company Double Ink Private Limited, it was clearly

noted from the financial and non-financial data that the firm was moving rapidly towards

making an efficient progress by automating the tasks and also making use of the information

technology frequently so as to improve the efficiency of the firm and increase its profit. It is

duly noted that it is not possible for every auditor to be familiar with the knowledge and the

terms of Information Technology system used by the firm in its mechanism that is how the

policy is adapted and used, an auditor for understanding the effectiveness and efficiency of

the IT process used by the firm should analyze the past experiences of the firm where the

methods and the tricks of using the IT technology have been duly noted with the documents

containing financial statements which may help the auditor to work in the limits of the way

that the expert have advised him to proceed with the accordance of ASA 600 (Hoffelder,

2012). It was also found that the main source of revenue generation is from the E-book

revenue. The information provided about the terms and agreements of the firm DIPL in the E-

book should be always verified and assessed in order to ensure that there may not arise any

disputes between the companies and different publishers in future. It was also noticed that the

firm DIPL was charging an advance annual 12 months storage fees to its clients which makes

it necessary for the auditor to check the financial statements of the storage fee billing and any

related documents. If a proper judgment of data is needed then it is not possible for a non-IT

professional to assess this type of advanced IT system. Therefore the auditor is required to

use the help of a person who attains expertise in the IT field and thus also ensures that all the

data is assessed and the IT system is analyzed carefully so that the auditor can finalize his

reports in an efficient and effective way (Geoffrey et. al, 2016). It should be clearly known

that the auditor has the full right to choose that he or she may choose if they need an expert

on the judgement of the audit report as even after the analysis of all the documents, the

thus helping him to identify the inappropriate statements of the firm while auditing. The case

of Double ink printers limited is having the same necessity of analyzing and evaluating all the

account balances, types of transactions and the conditions of the firm so that the auditor can

be advised if he needs the help of an expert auditor in accordance to the ASA 315 (Merchant,

2012). According to ASA 600, an auditor faces no change in his situation of completing the

audit process which keeps it unchanged and unaltered no matter if an expert auditors help is

taken or not (Kaplan Kaplan, 2011). Even if the auditor of the firm DIPL takes help from an

expert or not, he needs to still needed to find out the data and give an opinion on the financial

performance and position of the firm.

While checking the background of the company Double Ink Private Limited, it was clearly

noted from the financial and non-financial data that the firm was moving rapidly towards

making an efficient progress by automating the tasks and also making use of the information

technology frequently so as to improve the efficiency of the firm and increase its profit. It is

duly noted that it is not possible for every auditor to be familiar with the knowledge and the

terms of Information Technology system used by the firm in its mechanism that is how the

policy is adapted and used, an auditor for understanding the effectiveness and efficiency of

the IT process used by the firm should analyze the past experiences of the firm where the

methods and the tricks of using the IT technology have been duly noted with the documents

containing financial statements which may help the auditor to work in the limits of the way

that the expert have advised him to proceed with the accordance of ASA 600 (Hoffelder,

2012). It was also found that the main source of revenue generation is from the E-book

revenue. The information provided about the terms and agreements of the firm DIPL in the E-

book should be always verified and assessed in order to ensure that there may not arise any

disputes between the companies and different publishers in future. It was also noticed that the

firm DIPL was charging an advance annual 12 months storage fees to its clients which makes

it necessary for the auditor to check the financial statements of the storage fee billing and any

related documents. If a proper judgment of data is needed then it is not possible for a non-IT

professional to assess this type of advanced IT system. Therefore the auditor is required to

use the help of a person who attains expertise in the IT field and thus also ensures that all the

data is assessed and the IT system is analyzed carefully so that the auditor can finalize his

reports in an efficient and effective way (Geoffrey et. al, 2016). It should be clearly known

that the auditor has the full right to choose that he or she may choose if they need an expert

on the judgement of the audit report as even after the analysis of all the documents, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIPL

auditor is left with the lone responsibility to choose whether it needs an expert opinion or not.

However looking after the gritty situation of the firms IT advancements, it is advised that the

auditor must opt for an expert opinion (Niemi & Sundgren, 2012).

Answer 2

Materiality in terms of financial aspects may be defined as the negligence of any information

which may cause a direct material effect on the financial statements of the business. There are

various standards of auditing related to the topic of materiality. A thorough analysis should

be made in order to understand these standards in the different parts of the question (Gay &

Simnet, 2015).

Part A

In auditing, it is important for an auditor to seek for the materiality of the financial statements

of the firm as it is not feasible to give every single item of expense, income and asset and

liability equal importance. The materiality of the financial statements id distinguished on, the

basis of the balances of the accounts and the divisions of the transactions are to be evaluated

on the basis of the entity and the financial statements of the business. ASA 315’s principle of

Identifying and assessing the risks of materials should be taken into consideration for

understanding the environment and financial aspects of the firm (Fazal, 2013). Is should be

followed so that there may be no state of confusion when there is a need to gain a proper idea

of the account balances or the environment of the firm on the basis of the operations in near

future while processing the report. ASA 320 issued by AUSAB gives the brief information

about the responsibility of an auditor in accordance with the materiality in the audit of a firm

(Roach, 2010).

The five factors affecting the materiality in the levels of the audit report of a DIPL firm’s

financial statements are:

1. Categories of transactions, declaration of items and account balances of the financial

statements of the company. For the estimation of materiality, the firm DIPL needs to divide

its financial statements into different categories of transaction like E-books, irregular

expenses, and storage fee according to their level of importance.

auditor is left with the lone responsibility to choose whether it needs an expert opinion or not.

However looking after the gritty situation of the firms IT advancements, it is advised that the

auditor must opt for an expert opinion (Niemi & Sundgren, 2012).

Answer 2

Materiality in terms of financial aspects may be defined as the negligence of any information

which may cause a direct material effect on the financial statements of the business. There are

various standards of auditing related to the topic of materiality. A thorough analysis should

be made in order to understand these standards in the different parts of the question (Gay &

Simnet, 2015).

Part A

In auditing, it is important for an auditor to seek for the materiality of the financial statements

of the firm as it is not feasible to give every single item of expense, income and asset and

liability equal importance. The materiality of the financial statements id distinguished on, the

basis of the balances of the accounts and the divisions of the transactions are to be evaluated

on the basis of the entity and the financial statements of the business. ASA 315’s principle of

Identifying and assessing the risks of materials should be taken into consideration for

understanding the environment and financial aspects of the firm (Fazal, 2013). Is should be

followed so that there may be no state of confusion when there is a need to gain a proper idea

of the account balances or the environment of the firm on the basis of the operations in near

future while processing the report. ASA 320 issued by AUSAB gives the brief information

about the responsibility of an auditor in accordance with the materiality in the audit of a firm

(Roach, 2010).

The five factors affecting the materiality in the levels of the audit report of a DIPL firm’s

financial statements are:

1. Categories of transactions, declaration of items and account balances of the financial

statements of the company. For the estimation of materiality, the firm DIPL needs to divide

its financial statements into different categories of transaction like E-books, irregular

expenses, and storage fee according to their level of importance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIPL

2. The level of materiality will also be changed or altered if there is any disposal of an asset

or a part of it during the period of auditing. Also if any business combination takes place, it

affects the materiality of the business (Fazal, 2013).

3. The percentage of the specified benchmark of the total expenditure or total revenue like

profit before tax, gross profit, and net profit will be very helpful in determining the levels of

materiality for the auditing process. The auditor decides the percentage on the basis of the

professional judgments made on the circumstances of the firm.

4. Qualitative disclosures like the use of the new and advanced IT infrastructure in the

business is also a huge regulating factor which influences the materiality levels of the

financial statements of the firm (Elder et. al, 2010).

5. The collective impact of small errors should also be noticed as they may not affect the

financial position as the whole but may affect it when combined.

Part B

Some of the general categories of transaction like the inventory in hand, revenue generated

from e-books, storage fee revenue and cash balances are very essential to the business of the

firm DIPL and hence they should be given utter importance as far as it is concerned with the

financial statements of the firm. The materiality of the financial statements also depends on

the nature of the transaction and their relation to these transactions.

The introduction of the new advanced IT system by the firm during 2017 should be given

utter importance as this event caused a huge change in the working of the firm. The

background information about the company clears that the firm is heavily dependent on the

newly introduced IT system. The company has also decided to invest in new IT system in

order to fully computerize its financial activities (Cappelleto, 2010). Hence it has been

mentioned in one of the five factors which are influencing the financial statements of the

firm.

The use of benchmarks of different levels of percentage has been a useful method for finding

the materiality levels of a firm’s financial statement while auditing. Hence several different

benchmarks like the total revenue, total expenses, net profit, gross profit and PAT can be

used by the firm to determine the materiality level of the income and expenses of the firm for

2. The level of materiality will also be changed or altered if there is any disposal of an asset

or a part of it during the period of auditing. Also if any business combination takes place, it

affects the materiality of the business (Fazal, 2013).

3. The percentage of the specified benchmark of the total expenditure or total revenue like

profit before tax, gross profit, and net profit will be very helpful in determining the levels of

materiality for the auditing process. The auditor decides the percentage on the basis of the

professional judgments made on the circumstances of the firm.

4. Qualitative disclosures like the use of the new and advanced IT infrastructure in the

business is also a huge regulating factor which influences the materiality levels of the

financial statements of the firm (Elder et. al, 2010).

5. The collective impact of small errors should also be noticed as they may not affect the

financial position as the whole but may affect it when combined.

Part B

Some of the general categories of transaction like the inventory in hand, revenue generated

from e-books, storage fee revenue and cash balances are very essential to the business of the

firm DIPL and hence they should be given utter importance as far as it is concerned with the

financial statements of the firm. The materiality of the financial statements also depends on

the nature of the transaction and their relation to these transactions.

The introduction of the new advanced IT system by the firm during 2017 should be given

utter importance as this event caused a huge change in the working of the firm. The

background information about the company clears that the firm is heavily dependent on the

newly introduced IT system. The company has also decided to invest in new IT system in

order to fully computerize its financial activities (Cappelleto, 2010). Hence it has been

mentioned in one of the five factors which are influencing the financial statements of the

firm.

The use of benchmarks of different levels of percentage has been a useful method for finding

the materiality levels of a firm’s financial statement while auditing. Hence several different

benchmarks like the total revenue, total expenses, net profit, gross profit and PAT can be

used by the firm to determine the materiality level of the income and expenses of the firm for

DIPL

auditing the financial reports of the firm DIPL. Use of 1% to 5% would be helpful according

to the level of activities and quality of transactions.

The background information about the company clears that the firm is heavily dependent on

the newly introduced IT system. The company has also decided to invest in new IT system in

order to fully computerize its financial activities. This also states the reason that why the

income and expenditures are wholly collected using the It systems of the company (Baldwin,

2010).

It is specially provided in the 27th paragraph of ASA 320 about the collective influence of the

incorrect statements and small mistakes should be considered while evaluating the materiality

of the firm’s financial statement. The incorrect statements and financial values may not affect

the firm’s financial condition materially but when they are accumulated as a whole it

becomes a material change which should be duly noted while the auditing of the firm’s

financial statement.

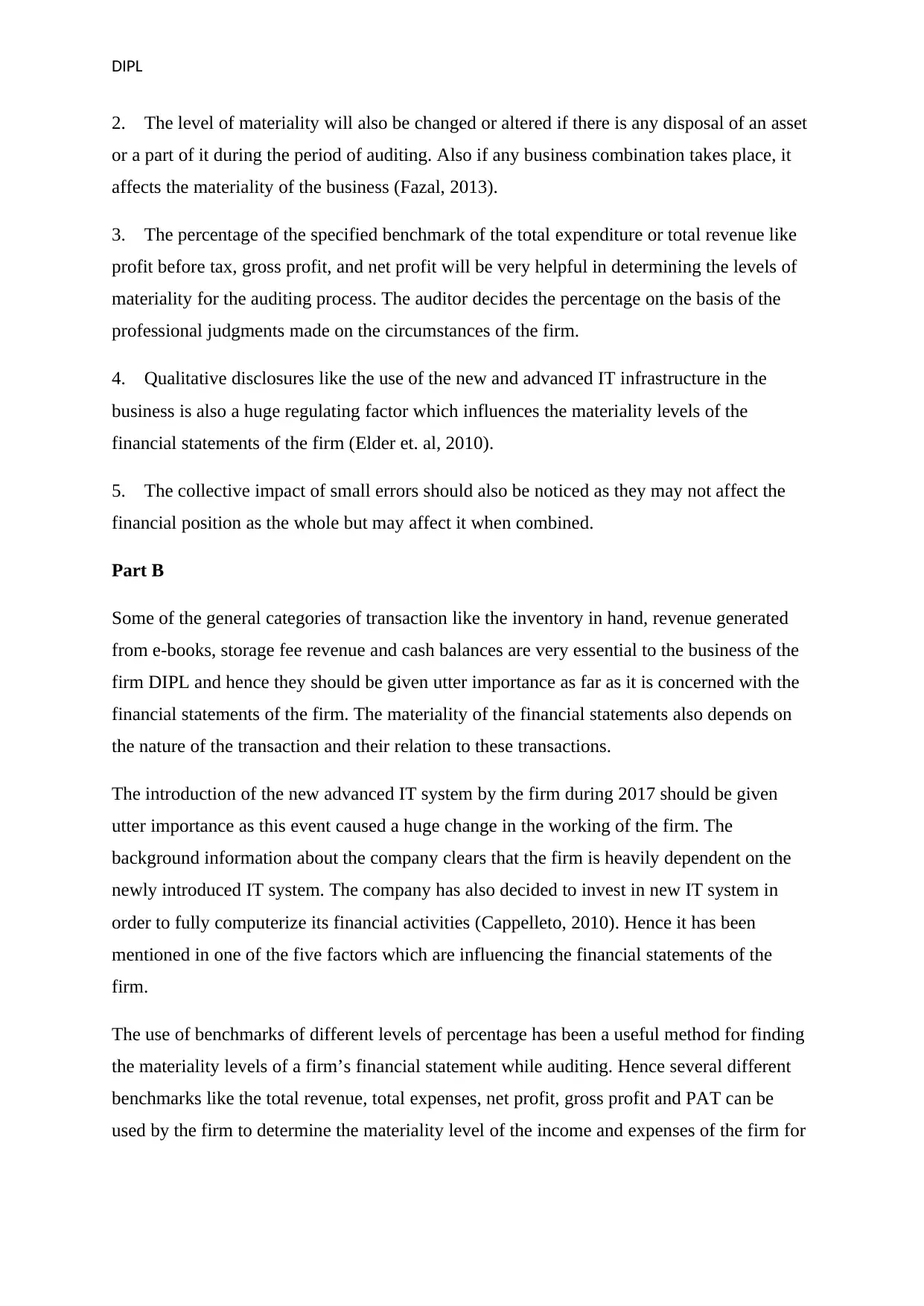

Part – c

To know about the factors that are traced in part (a) above will have a bearing on the

preliminary figure for materiality of DIPL, it is imperative to know the profit and loss of the

company.

Revenue of Double Ink Printers Limited

Amount in AUD Years

Details 2015 2016 2017

Revenue 34,212,000.0

0

37,699,500.

00

43,459,500.0

0

Less: Cost of sales 28,207,500.0

0

31,620,000.

00

36,855,000.0

0

Gross Profit 6,004,500.0

0

6,079,500.

00

6,604,500.0

0

Add: Indirect incomes

auditing the financial reports of the firm DIPL. Use of 1% to 5% would be helpful according

to the level of activities and quality of transactions.

The background information about the company clears that the firm is heavily dependent on

the newly introduced IT system. The company has also decided to invest in new IT system in

order to fully computerize its financial activities. This also states the reason that why the

income and expenditures are wholly collected using the It systems of the company (Baldwin,

2010).

It is specially provided in the 27th paragraph of ASA 320 about the collective influence of the

incorrect statements and small mistakes should be considered while evaluating the materiality

of the firm’s financial statement. The incorrect statements and financial values may not affect

the firm’s financial condition materially but when they are accumulated as a whole it

becomes a material change which should be duly noted while the auditing of the firm’s

financial statement.

Part – c

To know about the factors that are traced in part (a) above will have a bearing on the

preliminary figure for materiality of DIPL, it is imperative to know the profit and loss of the

company.

Revenue of Double Ink Printers Limited

Amount in AUD Years

Details 2015 2016 2017

Revenue 34,212,000.0

0

37,699,500.

00

43,459,500.0

0

Less: Cost of sales 28,207,500.0

0

31,620,000.

00

36,855,000.0

0

Gross Profit 6,004,500.0

0

6,079,500.

00

6,604,500.0

0

Add: Indirect incomes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIPL

Obsolescence of inventory

Allowance reversed

155,588.0

0

Income from commission 108,000.0

0

123,000.

00

130,500.0

0

Storage fee for e-books 667,500.0

0

1,027,500.

00

1,417,500.0

0

(A): Operating income 6,780,000.0

0

7,230,000.

00

8,308,088.0

0

Less: Indirect Expenses

Expenses for advertisement 83,725.0

0

115,923.

00

125,778.0

0

Audit fees 112,500.0

0

127,500.

00

135,000.0

0

Bad debts 150,000.0

0

195,000.

00

210,000.0

0

Depreciation 249,375.0

0

274,312.

00

472,688.0

0

Expenses on discount allowed 195,000.0

0

285,000.

00

335,500.0

0

Legal fees expenditures 74,000.0

0

111,500.

00

137,000.0

0

Exchange loss (foreign) 38,500.0

0

49,750.

00

Rates 98,500.0

0

106,000.

00

113,500.0

0

Expenditures on repair and 224,000.0 276,500. 306,500.0

Obsolescence of inventory

Allowance reversed

155,588.0

0

Income from commission 108,000.0

0

123,000.

00

130,500.0

0

Storage fee for e-books 667,500.0

0

1,027,500.

00

1,417,500.0

0

(A): Operating income 6,780,000.0

0

7,230,000.

00

8,308,088.0

0

Less: Indirect Expenses

Expenses for advertisement 83,725.0

0

115,923.

00

125,778.0

0

Audit fees 112,500.0

0

127,500.

00

135,000.0

0

Bad debts 150,000.0

0

195,000.

00

210,000.0

0

Depreciation 249,375.0

0

274,312.

00

472,688.0

0

Expenses on discount allowed 195,000.0

0

285,000.

00

335,500.0

0

Legal fees expenditures 74,000.0

0

111,500.

00

137,000.0

0

Exchange loss (foreign) 38,500.0

0

49,750.

00

Rates 98,500.0

0

106,000.

00

113,500.0

0

Expenditures on repair and 224,000.0 276,500. 306,500.0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIPL

maintenance 0 00 0

Salary expenses 1,965,000.0

0

2,190,000.

00

2,445,000.0

0

Costs of telecommunication 134,750.0

0

141,478.

00

159,785.0

0

(B): Total Indirect expenses 3,325,350.0

0

3,872,963.

00

4,440,751.0

0

Profit before interest and taxes (A-

B)

3,454,650.0

0

3,357,037.

00

3,867,337.0

0

Less: Interest 84,379.0

0

83,663.

00

808,038.0

0

Profit before tax 3,370,271.0

0

3,273,374.

00

3,059,299.0

0

Less: Income tax 1,011,081.0

0

982,012.

00

87,116.0

0

Profit after tax 2,359,190.0

0

2,291,362.

00

2,972,183.0

0

Going by the items projected in the income statement that is the items pertaining to the

income and expenditure, all can be tagged as relevant, as well as material in nature because

they are used in determining the profit and loss of the company for three regular years.

Moreover, all the inclusion of the sub-items contained in the revenue and expenditure that are

surpassing 5% of the overall company’s revenue will be deemed to be material for the

purpose of financial statements audit. However, the auditor needs to have substantive, as

well as analytical procedure on every item of income and expenditure hence; nothing can stop

the auditor to extend the procedure of audit on every item of financial statements if he

considers it necessary to project an opinion on the financial statements.

maintenance 0 00 0

Salary expenses 1,965,000.0

0

2,190,000.

00

2,445,000.0

0

Costs of telecommunication 134,750.0

0

141,478.

00

159,785.0

0

(B): Total Indirect expenses 3,325,350.0

0

3,872,963.

00

4,440,751.0

0

Profit before interest and taxes (A-

B)

3,454,650.0

0

3,357,037.

00

3,867,337.0

0

Less: Interest 84,379.0

0

83,663.

00

808,038.0

0

Profit before tax 3,370,271.0

0

3,273,374.

00

3,059,299.0

0

Less: Income tax 1,011,081.0

0

982,012.

00

87,116.0

0

Profit after tax 2,359,190.0

0

2,291,362.

00

2,972,183.0

0

Going by the items projected in the income statement that is the items pertaining to the

income and expenditure, all can be tagged as relevant, as well as material in nature because

they are used in determining the profit and loss of the company for three regular years.

Moreover, all the inclusion of the sub-items contained in the revenue and expenditure that are

surpassing 5% of the overall company’s revenue will be deemed to be material for the

purpose of financial statements audit. However, the auditor needs to have substantive, as

well as analytical procedure on every item of income and expenditure hence; nothing can stop

the auditor to extend the procedure of audit on every item of financial statements if he

considers it necessary to project an opinion on the financial statements.

DIPL

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DIPL

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Melbourne

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Fazal, H. (2013, May 13). What is Intimidation threat in auditing?.Retrieved from:

http://pakaccountants.com/what-is-intimidation-threat-in-auditing/

Gay, G., and Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons, 30(1), 143-156. https://doi.org/10.2308/acch-51309

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies. Retrieved

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University.

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. https://doi.org/10.2308/accr-

50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. https://doi.org/10.1108/01140581211283904

References

Baldwin, S. (2010). Doing a content audit or inventory. Pearson Press.

Cappelleto, G. (2010) Challenges Facing Accounting Education in Australia. AFAANZ,

Melbourne

Elder, J. R., Beasley S. M., and Arens A. A. (2010). Auditing and Assurance Services. Person

Education, New Jersey: USA

Fazal, H. (2013, May 13). What is Intimidation threat in auditing?.Retrieved from:

http://pakaccountants.com/what-is-intimidation-threat-in-auditing/

Gay, G., and Simnet, R. (2015). Auditing and Assurance Services. McGraw Hill

Geoffrey D. B., Joleen K., K. K.S., and David A. W. (2016). Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors.

Accounting Horizons, 30(1), 143-156. https://doi.org/10.2308/acch-51309

Hoffelder, K. (2012). New Audit Standard Encourages More Talking. Harvard Press.

Kaplan, R.S. (2011). Accounting scholarship that advances professional knowledge and

practice. The Accounting Review, 86(2), 367–383.

https://doi.org/10.2308/accr.00000031

Lapsley, I. (2012). Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management, 9(3), pp. 291-292.

https://doi.org/10.1111/1468-0408.00081

Livne, G. (2015, May 12). Threats to Auditor Independence and Possible Remedies. Retrieved

from: http://www.financepractitioner.com/auditing-best-practice/threats-to-auditor-

independence-and-possible-remedies?full

Manoharan, T.N. (2011). Financial Statement Fraud and Corporate Governance. The

George Washington University.

Matthew, S. E. (2015). Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review, 90(2), 495-527. https://doi.org/10.2308/accr-

50871

Merchant, K. A. (2012). Making Management Accounting Research More Useful. Pacific

Accounting Review, 24(3), 1-34. https://doi.org/10.1108/01140581211283904

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DIPL

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

https://doi.org/10.1080/09638180.2012.671465

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

Niemi, L., and Sundgren, S. (2012). Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review, 21(4), 767-796.

https://doi.org/10.1080/09638180.2012.671465

Roach, L. (2010). Auditor Liability: Liability Limitation Agreements. Pearson.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.