Analysis of Assurance and Forensic Accounting in Financial Reports

VerifiedAdded on 2022/09/16

|13

|2608

|18

Report

AI Summary

This report provides an analysis of assurance and forensic accounting practices, focusing on key audit matters (KAMs) and their impact on financial reporting. The report examines alterations in financial statements made by AMP, Commonwealth Bank, and Bank of Queensland, comparing 2018 and 2017 annual reports. It discusses the optional inclusion of findings in audit reports as per ASA701 and highlights risks identified by the Royal Commission, emphasizing the importance of auditor communication and addressing material misstatements. The report further explores audit procedures, including inquiry, observation, evidence checking, re-performance, and CAAT, and examines the role of organizational culture audits. It concludes by summarizing the key findings and implications of the Haynes Royal Commission on financial services, reflecting the threats from the results of the royal banking commission and its impact on financial reporting and auditing practices.

Running head: ASSURANCE AND FORENSIC ACCOUNTING

Assurance and forensic accounting

Name of the university:

Name of the student:

Authors note:

Assurance and forensic accounting

Name of the university:

Name of the student:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ASSURANCE AND FORENSIC ACCOUNTING

Table of Contents

PART A:.....................................................................................................................................2

Answer to question 1..................................................................................................................2

Answer to question 2..................................................................................................................4

Answer to question 3:.................................................................................................................4

PART B:.....................................................................................................................................5

Answer to question 1..................................................................................................................5

Answer to question 2:.................................................................................................................5

PART C:.....................................................................................................................................5

Conclusion:................................................................................................................................5

Reference:..................................................................................................................................5

Table of Contents

PART A:.....................................................................................................................................2

Answer to question 1..................................................................................................................2

Answer to question 2..................................................................................................................4

Answer to question 3:.................................................................................................................4

PART B:.....................................................................................................................................5

Answer to question 1..................................................................................................................5

Answer to question 2:.................................................................................................................5

PART C:.....................................................................................................................................5

Conclusion:................................................................................................................................5

Reference:..................................................................................................................................5

2ASSURANCE AND FORENSIC ACCOUNTING

PART A:

Answer to question 1.

Certain alternation are made in the financial report of 2018 as compared to annual

report of 2017:

AMP: As per the provisions of ASA701 with respect to key audit matters company made

certain alternations for financial year of 2018 as compared to financial year of 2017 that has

been included in annual report (Afterman 2016).

Financial instruments earlier arranged as loans and receivables are presently arranged

as amortized cost.

Equity instruments which were earlier arranged and known to me available for sale

are presently arranged as fair value with the help of other comprehensive income

(FVOCI).Since there is consistency maintained for treatment of sale of equity

instruments which are available, movement in terms of value for equity instruments

are known as FVOCI and are known as per fair value reserve included in the

statement of equity change. Gains as well as losses for equity securities are

measurable at FVOCI are not at all rearranged into profit or loss (Appelbaum, Kogan

and Vasarhelyi 2017).

Debt instruments that were held by the AMP Bank were earlier arranged as maturity

to be held and for measurement at amortized cost .AMP has rearranged the financial

instruments as FVOCI to be known as debt instruments in order to meet all cash flow

characteristics as per contractual basis that will help to collect cash flows as well as

help to manage liquidity needs (Bédard, Gonthier-Besacier and Schatt 2014).

PART A:

Answer to question 1.

Certain alternation are made in the financial report of 2018 as compared to annual

report of 2017:

AMP: As per the provisions of ASA701 with respect to key audit matters company made

certain alternations for financial year of 2018 as compared to financial year of 2017 that has

been included in annual report (Afterman 2016).

Financial instruments earlier arranged as loans and receivables are presently arranged

as amortized cost.

Equity instruments which were earlier arranged and known to me available for sale

are presently arranged as fair value with the help of other comprehensive income

(FVOCI).Since there is consistency maintained for treatment of sale of equity

instruments which are available, movement in terms of value for equity instruments

are known as FVOCI and are known as per fair value reserve included in the

statement of equity change. Gains as well as losses for equity securities are

measurable at FVOCI are not at all rearranged into profit or loss (Appelbaum, Kogan

and Vasarhelyi 2017).

Debt instruments that were held by the AMP Bank were earlier arranged as maturity

to be held and for measurement at amortized cost .AMP has rearranged the financial

instruments as FVOCI to be known as debt instruments in order to meet all cash flow

characteristics as per contractual basis that will help to collect cash flows as well as

help to manage liquidity needs (Bédard, Gonthier-Besacier and Schatt 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ASSURANCE AND FORENSIC ACCOUNTING

Commonwealth bank:

The common wealth bank is one of the biggest multinational banks throughout the world.

Generally the bank conducts its operations across the whole of United Kingdom, Asia and

New Zealand. Various different types of financial services along with banking institution and

retail business services are provided by the bank. As per the provisions of ASA701 with

respect to Key audit matters (KAM’s) company has made several alterations for the financial

year 2018. Making comparison to the financial year 2017 that has been shown in company’s

annual report (Bédard, Gonthier-Besacie and Schatt 2015).

More weightage on financial as well as quantitative measure in STVR.

Being 50% of STVR withheld into equity.

A long period of STVR withheld period for two years.

Introducing some new LTVR measures for performance.

To allocate reward rights with respect to LTVR as per face value basis.

Enhancement for risk as well as governance of remuneration as well as frameworks

(Motahary and Emami 2016).

Bank of Queensland:

As per provisions followed under SA701 with respect to Key audit matters (KAM’s) the

company could make some alterations for the financial year 2018. As per comparison in the

financial year 2017 that has disclosure in annual report of the company (Gimbar, Hansen and

Ozlanski 2016).

Changes in terms of remuneration in the financial year 2018 and for the financial year

2019. Changes in terms of remuneration framework do cover specific management

personnel that were made for FY 18 in order to meet the needs for executive

Commonwealth bank:

The common wealth bank is one of the biggest multinational banks throughout the world.

Generally the bank conducts its operations across the whole of United Kingdom, Asia and

New Zealand. Various different types of financial services along with banking institution and

retail business services are provided by the bank. As per the provisions of ASA701 with

respect to Key audit matters (KAM’s) company has made several alterations for the financial

year 2018. Making comparison to the financial year 2017 that has been shown in company’s

annual report (Bédard, Gonthier-Besacie and Schatt 2015).

More weightage on financial as well as quantitative measure in STVR.

Being 50% of STVR withheld into equity.

A long period of STVR withheld period for two years.

Introducing some new LTVR measures for performance.

To allocate reward rights with respect to LTVR as per face value basis.

Enhancement for risk as well as governance of remuneration as well as frameworks

(Motahary and Emami 2016).

Bank of Queensland:

As per provisions followed under SA701 with respect to Key audit matters (KAM’s) the

company could make some alterations for the financial year 2018. As per comparison in the

financial year 2017 that has disclosure in annual report of the company (Gimbar, Hansen and

Ozlanski 2016).

Changes in terms of remuneration in the financial year 2018 and for the financial year

2019. Changes in terms of remuneration framework do cover specific management

personnel that were made for FY 18 in order to meet the needs for executive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ASSURANCE AND FORENSIC ACCOUNTING

remuneration. As per BEAR Legislation and for alignment in terms of expectations of

community (Kholvadia 2016).

On 10th May 2018 specific changes for Group Executive to management personnel

were announced. Restructure had the purpose for providing and consolidation of

operations as per COO in order to improve the support for front line employee.

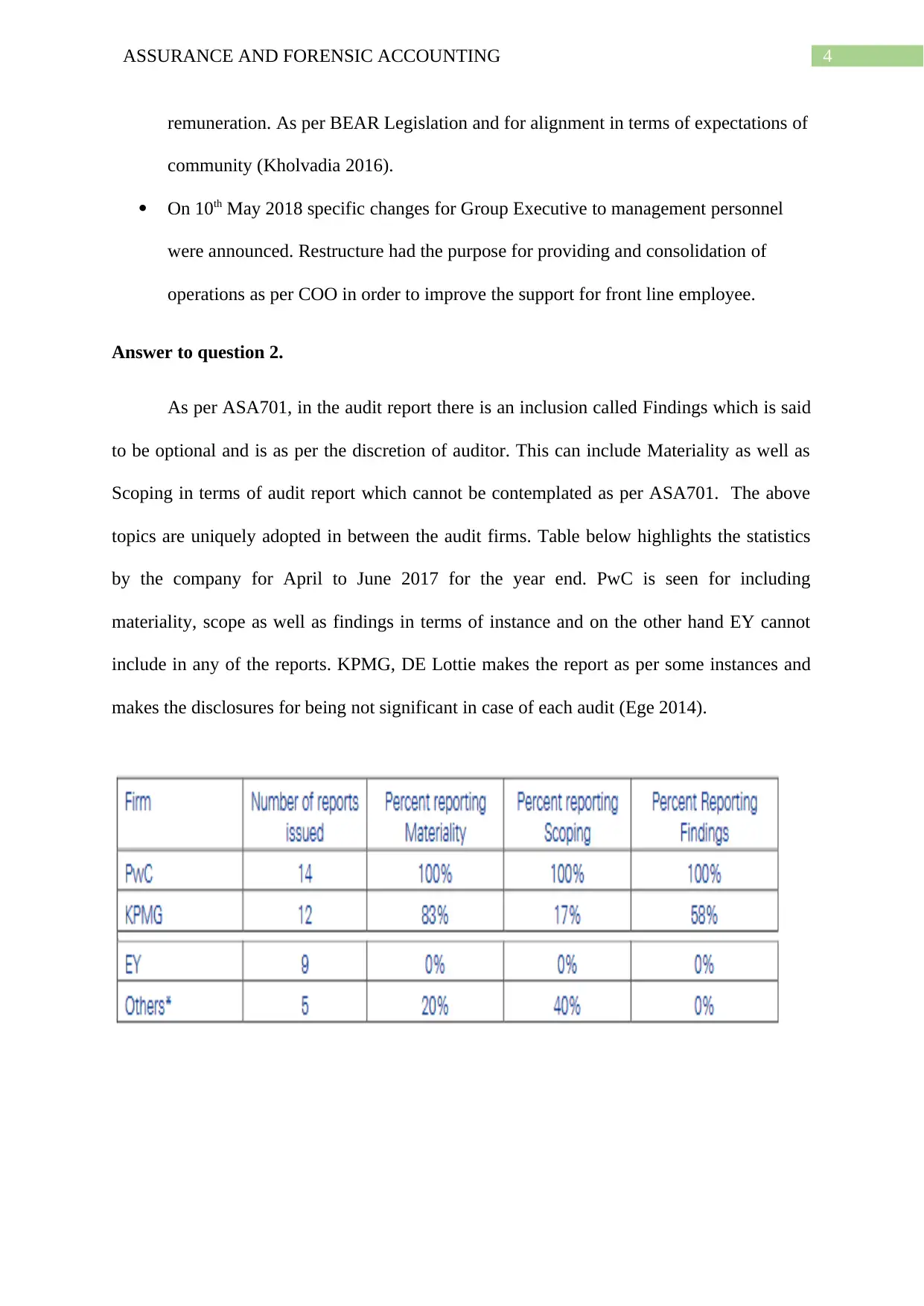

Answer to question 2.

As per ASA701, in the audit report there is an inclusion called Findings which is said

to be optional and is as per the discretion of auditor. This can include Materiality as well as

Scoping in terms of audit report which cannot be contemplated as per ASA701. The above

topics are uniquely adopted in between the audit firms. Table below highlights the statistics

by the company for April to June 2017 for the year end. PwC is seen for including

materiality, scope as well as findings in terms of instance and on the other hand EY cannot

include in any of the reports. KPMG, DE Lottie makes the report as per some instances and

makes the disclosures for being not significant in case of each audit (Ege 2014).

remuneration. As per BEAR Legislation and for alignment in terms of expectations of

community (Kholvadia 2016).

On 10th May 2018 specific changes for Group Executive to management personnel

were announced. Restructure had the purpose for providing and consolidation of

operations as per COO in order to improve the support for front line employee.

Answer to question 2.

As per ASA701, in the audit report there is an inclusion called Findings which is said

to be optional and is as per the discretion of auditor. This can include Materiality as well as

Scoping in terms of audit report which cannot be contemplated as per ASA701. The above

topics are uniquely adopted in between the audit firms. Table below highlights the statistics

by the company for April to June 2017 for the year end. PwC is seen for including

materiality, scope as well as findings in terms of instance and on the other hand EY cannot

include in any of the reports. KPMG, DE Lottie makes the report as per some instances and

makes the disclosures for being not significant in case of each audit (Ege 2014).

5ASSURANCE AND FORENSIC ACCOUNTING

Answer to question 3:

There are certain risk which is highlighted by the commission along with the banks

consumers, also there are certain high risk or hazards which are identified as per ISA 315.

The basic level of honesty has been sacrificed for the generation of short term profit, this was

in the report submitted by the commission. In order to identify and assess risks for material

misstatement as per the understanding of Entity and for its environment individual judgments

of an auditor with respect to areas in financial statements are involved with the critical

decision of management inclusion of accounting estimates and also the effect of audit in case

of events or transactions occurred. Description of essential audit matter in terms of auditor’s

report would include: The reason for matter being considered for being one of the important

in audit and for determination of KMA.

1.) The matter has been addressed by the audit report is,

The auditors are significantly trying to ensure communication which is useful in the group

engagement: (Lanis and Richardson 2015)

Communication should be free between the auditors and the group engagement as

per the audit policy.

The governance of the group on a time basis is carried by the auditor and are

communicated to the people. (Bowlin, Hobson and Piercey 2015).

Answer to question 3:

There are certain risk which is highlighted by the commission along with the banks

consumers, also there are certain high risk or hazards which are identified as per ISA 315.

The basic level of honesty has been sacrificed for the generation of short term profit, this was

in the report submitted by the commission. In order to identify and assess risks for material

misstatement as per the understanding of Entity and for its environment individual judgments

of an auditor with respect to areas in financial statements are involved with the critical

decision of management inclusion of accounting estimates and also the effect of audit in case

of events or transactions occurred. Description of essential audit matter in terms of auditor’s

report would include: The reason for matter being considered for being one of the important

in audit and for determination of KMA.

1.) The matter has been addressed by the audit report is,

The auditors are significantly trying to ensure communication which is useful in the group

engagement: (Lanis and Richardson 2015)

Communication should be free between the auditors and the group engagement as

per the audit policy.

The governance of the group on a time basis is carried by the auditor and are

communicated to the people. (Bowlin, Hobson and Piercey 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ASSURANCE AND FORENSIC ACCOUNTING

PART B:

Answer to question 1.

The audit matter generally tries to show the risk relating to the corporation of finance

followed from the year 2017 and 2018. A report on the high level of misconduct was

provided by the royal banking commission which was in respect to super annulation and

banking. The final report has to be looked upon with the interim report to get a clear idea of

the requirement of observation. (Cordoş and Fülöp 2015). It has well been documented as per

Commission received for 10000 submissions of public and for holding of 68 days for

hearings.

Final Report includes financial services that are already examined and identified with issues,

causes as well as responses which can also include recommendations as well. The Australian

Securities and Investments Commission as well as Australian Prudential Regulation

Association Commission has brought about 24 instances (Afterman 2016). The basic level of

honesty has been sacrificed for the generation of short term profit, this was in the report

submitted by the commission. (Sirois, Bédard and Bera 2018).

In commission there are 4 observation:

There can be link between reward as well as conduct.

In conflict there can be effect between interest as well as duty

There can be a holding account of an organization.

Answer to question 2:

PART B:

Answer to question 1.

The audit matter generally tries to show the risk relating to the corporation of finance

followed from the year 2017 and 2018. A report on the high level of misconduct was

provided by the royal banking commission which was in respect to super annulation and

banking. The final report has to be looked upon with the interim report to get a clear idea of

the requirement of observation. (Cordoş and Fülöp 2015). It has well been documented as per

Commission received for 10000 submissions of public and for holding of 68 days for

hearings.

Final Report includes financial services that are already examined and identified with issues,

causes as well as responses which can also include recommendations as well. The Australian

Securities and Investments Commission as well as Australian Prudential Regulation

Association Commission has brought about 24 instances (Afterman 2016). The basic level of

honesty has been sacrificed for the generation of short term profit, this was in the report

submitted by the commission. (Sirois, Bédard and Bera 2018).

In commission there are 4 observation:

There can be link between reward as well as conduct.

In conflict there can be effect between interest as well as duty

There can be a holding account of an organization.

Answer to question 2:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ASSURANCE AND FORENSIC ACCOUNTING

Organizational culture can be audited for external auditor as there can be agreement

between Board and either Audit Committee in order to proceed for audit or for review of

culture or internal audit departments that take several methods for auditing culture:

Incorporation of element of culture for each and every risk-based audit for tailor

testing programmer

For performing of standalone culture audit

There can be Thematic analysis for internal audit work

Several internal audit functions can implement one and others can implement other

procedures (Chambers and Odar 2015).

Specific audit procedure can be used by auditors in order to determine quality of financial

information which can be provided by the clients.

Inquiry: As an auditor has the purpose of auditing the financial statements of a companies

and verify that it is showing true and fair value with transparency. Thus an auditor can clear

any of its doubt by taking to the relevance authority of the same.

Observation: when certain activities of a company a carried out without any proper

documentation. The auditor can verify the same by visually observing the events relating to

the activity this method is carried and preferable when no proper documentation is available.

(Brasel et al. 2016).

Checking of evidences: The auditor cannot blindly rely on the available documents, without

conforming the genuinely of those documents. Thus, the auditor has to develop means to

inspect and verify the evidences provided to him. If any of the evidences fail to be true the

auditor should carry out extensive inspection of evidence.

Organizational culture can be audited for external auditor as there can be agreement

between Board and either Audit Committee in order to proceed for audit or for review of

culture or internal audit departments that take several methods for auditing culture:

Incorporation of element of culture for each and every risk-based audit for tailor

testing programmer

For performing of standalone culture audit

There can be Thematic analysis for internal audit work

Several internal audit functions can implement one and others can implement other

procedures (Chambers and Odar 2015).

Specific audit procedure can be used by auditors in order to determine quality of financial

information which can be provided by the clients.

Inquiry: As an auditor has the purpose of auditing the financial statements of a companies

and verify that it is showing true and fair value with transparency. Thus an auditor can clear

any of its doubt by taking to the relevance authority of the same.

Observation: when certain activities of a company a carried out without any proper

documentation. The auditor can verify the same by visually observing the events relating to

the activity this method is carried and preferable when no proper documentation is available.

(Brasel et al. 2016).

Checking of evidences: The auditor cannot blindly rely on the available documents, without

conforming the genuinely of those documents. Thus, the auditor has to develop means to

inspect and verify the evidences provided to him. If any of the evidences fail to be true the

auditor should carry out extensive inspection of evidence.

8ASSURANCE AND FORENSIC ACCOUNTING

Re performances: when all the above methods fail to provide satisfaction to the auditor, the

auditor himself needs to re-perform the calculation to check whether they are correct or not.

This is done when all the above methods fail to provide satisfactory result to the auditor.

CAAT: This method is used when the volume of data is large and each and every transaction

needs to be analysts. A special software is needed to perform the same.

KAM are known to be matter for auditor’s professional judgment which are of most

importance in terms of audit for financial statements of current period. The matters known to

be important are further communicated to TCWG by the auditors on either quarterly or six

month basis as per audit committee meetings during the reviews that are limited. Most of the

important matter arise to get out of audit report formats those are uninteresting. KAM can

further make audit reports to be more and more interesting, transparent as well as those will

capture attention for readers of financial statements for matters that are important for

professional judgment of the company. KAM becomes applicable in case of certain situations

for statutory auditor decisions in case of professional judgment in order to communicate

KAM in terms of audit report of other company which does not fulfill the conditions that are

mentioned above. It becomes significant to note down KAM that is not applicable for report

having limited review by the statutory auditor on either quarterly or six month outcomes

(Bowlin, Hobson and Piercey 2015).

PART C:

Conclusion:

It can be concluded that the Followed the provisions under ASA701 relating to key

audit matters (KAM’s) the company made some relieved alteration in the financial year 2018

Comparing the fiscal year 2017, which are disclosed in the company’s annual report and the

description of the Key audit matter differ between audits undertaken by Ernst & Young, KPMG

Re performances: when all the above methods fail to provide satisfaction to the auditor, the

auditor himself needs to re-perform the calculation to check whether they are correct or not.

This is done when all the above methods fail to provide satisfactory result to the auditor.

CAAT: This method is used when the volume of data is large and each and every transaction

needs to be analysts. A special software is needed to perform the same.

KAM are known to be matter for auditor’s professional judgment which are of most

importance in terms of audit for financial statements of current period. The matters known to

be important are further communicated to TCWG by the auditors on either quarterly or six

month basis as per audit committee meetings during the reviews that are limited. Most of the

important matter arise to get out of audit report formats those are uninteresting. KAM can

further make audit reports to be more and more interesting, transparent as well as those will

capture attention for readers of financial statements for matters that are important for

professional judgment of the company. KAM becomes applicable in case of certain situations

for statutory auditor decisions in case of professional judgment in order to communicate

KAM in terms of audit report of other company which does not fulfill the conditions that are

mentioned above. It becomes significant to note down KAM that is not applicable for report

having limited review by the statutory auditor on either quarterly or six month outcomes

(Bowlin, Hobson and Piercey 2015).

PART C:

Conclusion:

It can be concluded that the Followed the provisions under ASA701 relating to key

audit matters (KAM’s) the company made some relieved alteration in the financial year 2018

Comparing the fiscal year 2017, which are disclosed in the company’s annual report and the

description of the Key audit matter differ between audits undertaken by Ernst & Young, KPMG

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ASSURANCE AND FORENSIC ACCOUNTING

and PWC of those companies as well as key audit matters are communicated. Critical risks and

audit procedures to the users of audited statements. Finally, the findings of the Haynes Royal

commission in to the financial services and reflected the threats from the results of the royal

banking commission.

and PWC of those companies as well as key audit matters are communicated. Critical risks and

audit procedures to the users of audited statements. Finally, the findings of the Haynes Royal

commission in to the financial services and reflected the threats from the results of the royal

banking commission.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ASSURANCE AND FORENSIC ACCOUNTING

Reference:

Afterman, A.B., 2016. The PCAOB's Proposed New Auditor's Report. The CPA Journal,

86(7), p.64.

Appelbaum, D., Kogan, A. and Vasarhelyi, M.A., 2017. Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), pp.1-27.

Bédard, J., Gonthier-Besacier, N. and Schatt, A., 2014, January. Costs and benefits of

reporting Key Audit Matters in the audit report: The French experience. In International

Symposium on Audit Research. Available at: http://documents. escdijon.

eu/pdf/cig2014/ACTESDUCOLLOQUE/BEDARD_GONTHIER_BESACIER_SCHATT. pdf.

Bédard, J., Gonthier-Besacier, N. and Schatt, A., 2015. Analysis of the Consequences of the

Disclosure of Key Audit Matters. Working Paper, Universite Laval.

Bowlin, K.O., Hobson, J.L. and Piercey, M.D., 2015. The effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The Accounting

Review, 90(4), pp.1363-1393.

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), pp.1345-1362.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., 2018. Evolution of Auditing: From the Traditional Approach to the Future

Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing

Limited.

Reference:

Afterman, A.B., 2016. The PCAOB's Proposed New Auditor's Report. The CPA Journal,

86(7), p.64.

Appelbaum, D., Kogan, A. and Vasarhelyi, M.A., 2017. Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), pp.1-27.

Bédard, J., Gonthier-Besacier, N. and Schatt, A., 2014, January. Costs and benefits of

reporting Key Audit Matters in the audit report: The French experience. In International

Symposium on Audit Research. Available at: http://documents. escdijon.

eu/pdf/cig2014/ACTESDUCOLLOQUE/BEDARD_GONTHIER_BESACIER_SCHATT. pdf.

Bédard, J., Gonthier-Besacier, N. and Schatt, A., 2015. Analysis of the Consequences of the

Disclosure of Key Audit Matters. Working Paper, Universite Laval.

Bowlin, K.O., Hobson, J.L. and Piercey, M.D., 2015. The effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The Accounting

Review, 90(4), pp.1363-1393.

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), pp.1345-1362.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., 2018. Evolution of Auditing: From the Traditional Approach to the Future

Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing

Limited.

11ASSURANCE AND FORENSIC ACCOUNTING

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

CORDOŞ, G.S. and FÜLÖP, M.T., 2014. A FRAMEWORK FOR UNDERSTANDING

AND RESEARCHING AUDIT CHANGES: KEY AUDIT MATTERS. AMIS 2014, p.935.

Cordoş, G.S. and Fülöp, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Ege, M.S., 2014. Does internal audit function quality deter management misconduct?. The

Accounting Review, 90(2), pp.495-527.

Gimbar, C., Hansen, B. and Ozlanski, M.E., 2016. The effects of critical audit matter

paragraphs and accounting standard precision on auditor liability. The Accounting Review,

91(6), pp.1629-1646.

Kholvadia, F., 2016, November. AUD 09: THE EFFECT OF CHANGES IN AUDITOR

REPORTING STANDARDS ON AUDIT QUALITY. In REGIONAL SAAA

CONFERENCES (p. 77).

Motahary, H. and Emami, T., 2016. Key audit matters-the answer?: An exploratory study

investigating auditors possibilty to accomplish the purpose of the new audit report.

Sirois, L.P., Bédard, J. and Bera, P., 2018. The informational value of key audit matters in the

auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2), pp.141-

162.

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

CORDOŞ, G.S. and FÜLÖP, M.T., 2014. A FRAMEWORK FOR UNDERSTANDING

AND RESEARCHING AUDIT CHANGES: KEY AUDIT MATTERS. AMIS 2014, p.935.

Cordoş, G.S. and Fülöp, M.T., 2015. Understanding audit reporting changes: introduction of

Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Ege, M.S., 2014. Does internal audit function quality deter management misconduct?. The

Accounting Review, 90(2), pp.495-527.

Gimbar, C., Hansen, B. and Ozlanski, M.E., 2016. The effects of critical audit matter

paragraphs and accounting standard precision on auditor liability. The Accounting Review,

91(6), pp.1629-1646.

Kholvadia, F., 2016, November. AUD 09: THE EFFECT OF CHANGES IN AUDITOR

REPORTING STANDARDS ON AUDIT QUALITY. In REGIONAL SAAA

CONFERENCES (p. 77).

Motahary, H. and Emami, T., 2016. Key audit matters-the answer?: An exploratory study

investigating auditors possibilty to accomplish the purpose of the new audit report.

Sirois, L.P., Bédard, J. and Bera, P., 2018. The informational value of key audit matters in the

auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2), pp.141-

162.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.