Management Accounting and Techniques Report - Aston Chemicals Analysis

VerifiedAdded on 2020/12/09

|21

|5483

|284

Report

AI Summary

This report provides a detailed analysis of management accounting and its application within Aston Chemicals. It begins by defining management accounting systems and their various uses, including cost accounting, inventory management, and job costing. The report then explores different types of management accounting reports, such as budget reports, performance reports, and accounts receivable aging reports, highlighting their benefits. It evaluates the integration of management accounting systems and reporting within the organization. The assignment delves into absorption and marginal costing techniques, presenting income statements using both methods. Furthermore, it applies break-even analysis and examines the use of management accounting techniques in financial reporting. The report also discusses planning tools for budgetary control, compares Aston Chemicals' responses to financial problems, and analyzes how management accounting techniques can lead to sustainable success. The conclusion summarizes the key findings and emphasizes the importance of management accounting in decision-making.

MANAGEMENT

ACCOUNTING AND

TECHNIQUES

ACCOUNTING AND

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................2

TASK 1 ...........................................................................................................................................3

A. Define the management accounting system and various management accounting system

uses by the organization .............................................................................................................3

B. Explain the various types of management accounting reports used in the organization. ......4

C. Explain the benefits of different types of management accounting system...........................6

D. Evaluating the integration of management accounting system and management accounting

report in the organization ...........................................................................................................7

TASK 2............................................................................................................................................7

A.1 Explaining the absorption costing and marginal costing ....................................................7

A.2. Producing income statements by utilising costing methods................................................8

B. Computing the following problem with the help of break-even analysis. ..........................10

C. Applying the range of management accounting techniques in the proper formal report.....11

D. Produce financial reports that accurately apply and interpret the data for the business

activities ...................................................................................................................................12

TASK 3 .........................................................................................................................................13

A. Explaining the advantages and disadvantages of different types of planning tools for

budgetary control .....................................................................................................................13

C. Comparing how the Aston chemicals is better in responding the financial problems ........17

D. Analysing management accounting techniques which could respond to financial problems

and lead the organization to sustainable success. .....................................................................17

E. Evaluate how planning tools could be used to solve financial problems and lead the

organization to sustainable success. .........................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION

Management accounting is that field of accounting which provides the managers with the

decision making. It plays an important role in an organization. It helps in decision-making

INTRODUCTION...........................................................................................................................2

TASK 1 ...........................................................................................................................................3

A. Define the management accounting system and various management accounting system

uses by the organization .............................................................................................................3

B. Explain the various types of management accounting reports used in the organization. ......4

C. Explain the benefits of different types of management accounting system...........................6

D. Evaluating the integration of management accounting system and management accounting

report in the organization ...........................................................................................................7

TASK 2............................................................................................................................................7

A.1 Explaining the absorption costing and marginal costing ....................................................7

A.2. Producing income statements by utilising costing methods................................................8

B. Computing the following problem with the help of break-even analysis. ..........................10

C. Applying the range of management accounting techniques in the proper formal report.....11

D. Produce financial reports that accurately apply and interpret the data for the business

activities ...................................................................................................................................12

TASK 3 .........................................................................................................................................13

A. Explaining the advantages and disadvantages of different types of planning tools for

budgetary control .....................................................................................................................13

C. Comparing how the Aston chemicals is better in responding the financial problems ........17

D. Analysing management accounting techniques which could respond to financial problems

and lead the organization to sustainable success. .....................................................................17

E. Evaluate how planning tools could be used to solve financial problems and lead the

organization to sustainable success. .........................................................................................18

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................20

INTRODUCTION

Management accounting is that field of accounting which provides the managers with the

decision making. It plays an important role in an organization. It helps in decision-making

process of every system by taking helps from financial record. It has several techniques of like

cost accounting , fund flow analysis , standard costing etc.

Aston chemicals was profound in 1990. It supplies the raw materials to European

personal care industries. The report is about the importance of management accounting and its

techniques required by Aston chemical. The report will provide, deep insight of meaning of

management accounting, the requirement of different types of system with their benefits. The

assignment will also discuss various management accounting reports used by Aston chemicals.

The present assignment will discuss absorption and marginal costing techniques and also

presents income statement on the absorption and marginal costing. This study will present

financial reporting documents by applying the range of management accounting techniques.

Present assignment will be the deep study of various planning tools and their uses which are

required by the Aston chemicals for the further decision-making.

TASK 1

A. Define the management accounting system and various management accounting system uses

by the organization

Management accounting is a type of system which managers of Aston chemicals uses for

the decision making. It is the provision of monetary and non- monetary decision-making

information by managers. It is that field of accounting, which is beneficial to all kind of

organization for better process of decision-making. It is systematic process of making different

types of managerial reports which provides accuracy and timely information required for

manager to take decisions (Ax and Greve, 2017). These reports are derived from financial

accounting reflect the decision-making process.

The information gathers from management accounting is widely different from financial

accounting. Different types of MA system use the various data to identify several information

required by the managers of Aston chemicals. Some of the management accounting system

which are used by the organization are listed under.

Cost accounting system

This system is also known as product costing or costing system. This accounting system

used by Aston chemicals for estimating cost of commodities and services, valuation of inventory,

and cost control. For profitable operations, estimating accurate cost is very much critical. It helps

cost accounting , fund flow analysis , standard costing etc.

Aston chemicals was profound in 1990. It supplies the raw materials to European

personal care industries. The report is about the importance of management accounting and its

techniques required by Aston chemical. The report will provide, deep insight of meaning of

management accounting, the requirement of different types of system with their benefits. The

assignment will also discuss various management accounting reports used by Aston chemicals.

The present assignment will discuss absorption and marginal costing techniques and also

presents income statement on the absorption and marginal costing. This study will present

financial reporting documents by applying the range of management accounting techniques.

Present assignment will be the deep study of various planning tools and their uses which are

required by the Aston chemicals for the further decision-making.

TASK 1

A. Define the management accounting system and various management accounting system uses

by the organization

Management accounting is a type of system which managers of Aston chemicals uses for

the decision making. It is the provision of monetary and non- monetary decision-making

information by managers. It is that field of accounting, which is beneficial to all kind of

organization for better process of decision-making. It is systematic process of making different

types of managerial reports which provides accuracy and timely information required for

manager to take decisions (Ax and Greve, 2017). These reports are derived from financial

accounting reflect the decision-making process.

The information gathers from management accounting is widely different from financial

accounting. Different types of MA system use the various data to identify several information

required by the managers of Aston chemicals. Some of the management accounting system

which are used by the organization are listed under.

Cost accounting system

This system is also known as product costing or costing system. This accounting system

used by Aston chemicals for estimating cost of commodities and services, valuation of inventory,

and cost control. For profitable operations, estimating accurate cost is very much critical. It helps

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to identify the manufacturing cost of each product and services. It helps in determining ending

value of material inventory, finished goods inventory for financial statements. This system

consisted of three basic accounting techniques like actual costing which the records the actual

cost of labors , cost of overheads etc. standard costing , this costing technique provides the actual

costs of goods that were produced and the cost that is occurred. And last is normal costing,

which is used to set annual expenses rates allocated for the production to overhead.

Inventory management system

The inventory management system helps in managing inventory of organization. The

Aston chemicals uses inventory management system to manage its inventory in a proper way. It

takes care of everything starting from purchasing of raw material than to sales of finished goods

(Cooper, Ezzamel and Qu, 2017). The inventory management helps in observing small moving

part of operations, permitting it to make better decisions and investments. Various parts of

supply chain management are being focused by different inventory managers. Examples of

inventory management includes the LIFO i.e. last in first out method , FIFO that is First in First

out method, and JIT

Job costing system

This is used by Aston chemicals in order to assign manufacturing cost to an individual

product or batches of goods. This system is mainly used when commodities are manufactured

sufficiently vary from each other. This system includes process of accumulating information

about various related with a specific production or service job.

Price optimizing system

The system helps to analyze best feasible cost that should be quoted for production is

called price optimizing system. It renders chances to concentrate on different goals and

objectives of Aston chemicals.

B. Explain the various types of management accounting reports used in the organization.

There are five major types of reports which are used by organization are mentioned under

Budget report

Performance report

Accounts receivable aging reports Cost managerial accounting reports

Budget reports

value of material inventory, finished goods inventory for financial statements. This system

consisted of three basic accounting techniques like actual costing which the records the actual

cost of labors , cost of overheads etc. standard costing , this costing technique provides the actual

costs of goods that were produced and the cost that is occurred. And last is normal costing,

which is used to set annual expenses rates allocated for the production to overhead.

Inventory management system

The inventory management system helps in managing inventory of organization. The

Aston chemicals uses inventory management system to manage its inventory in a proper way. It

takes care of everything starting from purchasing of raw material than to sales of finished goods

(Cooper, Ezzamel and Qu, 2017). The inventory management helps in observing small moving

part of operations, permitting it to make better decisions and investments. Various parts of

supply chain management are being focused by different inventory managers. Examples of

inventory management includes the LIFO i.e. last in first out method , FIFO that is First in First

out method, and JIT

Job costing system

This is used by Aston chemicals in order to assign manufacturing cost to an individual

product or batches of goods. This system is mainly used when commodities are manufactured

sufficiently vary from each other. This system includes process of accumulating information

about various related with a specific production or service job.

Price optimizing system

The system helps to analyze best feasible cost that should be quoted for production is

called price optimizing system. It renders chances to concentrate on different goals and

objectives of Aston chemicals.

B. Explain the various types of management accounting reports used in the organization.

There are five major types of reports which are used by organization are mentioned under

Budget report

Performance report

Accounts receivable aging reports Cost managerial accounting reports

Budget reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The budgeting reports are somewhere found critical in measuring the company's

performance because they are made on the basis of size of the organization. Like if there is a

small organization there should be only one budget report is to be made and if there are large

organizations consisted of lots of departments than the budget reports are provided according to

department. organizations. Every entity prepares budget before entering into a new contract or

project in form of report in order to identify the list of expenses. This report of Aston chemicals

was made with help of past experiences, records and budget reports (Management Accounting:

Meaning, Functions and Characteristics. 2017).

It is very important to have budget report in an organization because it helps in control

cost of entire Aston chemicals.

Account receivable aging reports

Accounts receivable aging reports are prepared in firm one the organization is extending

credit. Notify remaining balances of clients helps in identifying the defaulters and issues rising in

collection process (Eldenburg and et.al., 2016). If in report there are many defaulters than Aston

chemicals needs to strict their credit policies.

It is very important to implement the debtors aging reports so that defaulters can be

identify easily.

Cost managerial accounting reports

The cost of product and services that are manufactured is computed by management

accounting. This cost manage reports includes the computation of overhead, labor, material costs

and any added costs in it. The summary of all this information is offers by a cost report. It helps

manager to identify difference between the cost of goods and services to selling price of it.

It is very crucial to implement the cost managerial reports because it provides the exact

understanding of whole expenditures which is required for better optimization of the resources of

all information.

Performance Reports

These reports are made at end of year in order to determine performance of company as

a whole and employee's performance. In large organization performance reports are generated in

each of department.

performance because they are made on the basis of size of the organization. Like if there is a

small organization there should be only one budget report is to be made and if there are large

organizations consisted of lots of departments than the budget reports are provided according to

department. organizations. Every entity prepares budget before entering into a new contract or

project in form of report in order to identify the list of expenses. This report of Aston chemicals

was made with help of past experiences, records and budget reports (Management Accounting:

Meaning, Functions and Characteristics. 2017).

It is very important to have budget report in an organization because it helps in control

cost of entire Aston chemicals.

Account receivable aging reports

Accounts receivable aging reports are prepared in firm one the organization is extending

credit. Notify remaining balances of clients helps in identifying the defaulters and issues rising in

collection process (Eldenburg and et.al., 2016). If in report there are many defaulters than Aston

chemicals needs to strict their credit policies.

It is very important to implement the debtors aging reports so that defaulters can be

identify easily.

Cost managerial accounting reports

The cost of product and services that are manufactured is computed by management

accounting. This cost manage reports includes the computation of overhead, labor, material costs

and any added costs in it. The summary of all this information is offers by a cost report. It helps

manager to identify difference between the cost of goods and services to selling price of it.

It is very crucial to implement the cost managerial reports because it provides the exact

understanding of whole expenditures which is required for better optimization of the resources of

all information.

Performance Reports

These reports are made at end of year in order to determine performance of company as

a whole and employee's performance. In large organization performance reports are generated in

each of department.

Aston chemicals uses performance report in order to identify the capacity and ability of

its employees. For every organization it is very important to develop the performance report in

order to analyse the performance of the organization as well as the employees.

C. Explain the benefits of different types of management accounting system

Management accounting

systems

Benefits

Inventory management

system

The first and foremost benefit of inventory management

system is that it improves accuracy of orders of inventory.

It means that it determines that how much stock should

organization kept in hand so that shortage and exceeding of

inventory do not take place.

It increases the transparency of an information in an

organization.

It improves the flow of goods

Cost accounting system Wastes, inefficiencies and losses are eliminated by cost

accounting system by fixing standard for everything.

In reduces cost by following new and improved method of

the cost (Fullerton, Kennedy and Widener, 2014.).

It helps in determining the make or buy decision.

Job costing system It enables the organization to assess performance of

employees

It facilitates cost control by comparing actual with

estimates.

It helps managers to identify that which job is more

profitable.

Price optimizing system It assists in analysis of adequate cost over good and

services.

It determines the suitable cost of several products of goods

and services.

its employees. For every organization it is very important to develop the performance report in

order to analyse the performance of the organization as well as the employees.

C. Explain the benefits of different types of management accounting system

Management accounting

systems

Benefits

Inventory management

system

The first and foremost benefit of inventory management

system is that it improves accuracy of orders of inventory.

It means that it determines that how much stock should

organization kept in hand so that shortage and exceeding of

inventory do not take place.

It increases the transparency of an information in an

organization.

It improves the flow of goods

Cost accounting system Wastes, inefficiencies and losses are eliminated by cost

accounting system by fixing standard for everything.

In reduces cost by following new and improved method of

the cost (Fullerton, Kennedy and Widener, 2014.).

It helps in determining the make or buy decision.

Job costing system It enables the organization to assess performance of

employees

It facilitates cost control by comparing actual with

estimates.

It helps managers to identify that which job is more

profitable.

Price optimizing system It assists in analysis of adequate cost over good and

services.

It determines the suitable cost of several products of goods

and services.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D. Evaluating the integration of management accounting system and management accounting

report in the organization

The management accounting system and management accounting reporting is very well

integrated in Aston chemicals. Together work of both leads structure in top. The management

accounting system gives organization qualitative and quantitative data about functional and

operational performances. This data presented by management accounting systems in form of

report helps to identify performance of firm. The management reporting system more

specifically are made to proctor the operations of Aston chemicals associated with objectives

which are to be set out in formal plan developed by organization. This combination of

management accounting systems and management reporting systems helps company to identify

their objectives and work on that as soon as possible (Kihn and Ihantola, 2015). The integration

of these two systems is very important in an organization to implement in order to take decision

for productivity of firm. They control duplication of work, saves time and enhance ability of

firm. For Aston chemicals, it is very important to have both systems for sound decisions (Malmi,

2016).

TASK 2

A.1 Explaining the absorption costing and marginal costing

Absorption costing

Absorption costing is the method collection of all the production cost and allocating them

to the actual individual product. In other words, it means that entire cost related with production

like direct labour, overhead costs and direct material etc are included. Absorption costing

methods not only entails cost but also all the manufacturing expenses whether fined and variable.

This technique is also known as full absorption costing. This basically differs from other costing

methods because it takes fixed manufacturing expenses into consideration. For Aston absorption

costing has proven very much beneficial. It determines the value of fixed costs participating in

production (Nitzl, 2018). It shows less alteration in net profits in case of constant production but

fluctuating sales.

Marginal costing

report in the organization

The management accounting system and management accounting reporting is very well

integrated in Aston chemicals. Together work of both leads structure in top. The management

accounting system gives organization qualitative and quantitative data about functional and

operational performances. This data presented by management accounting systems in form of

report helps to identify performance of firm. The management reporting system more

specifically are made to proctor the operations of Aston chemicals associated with objectives

which are to be set out in formal plan developed by organization. This combination of

management accounting systems and management reporting systems helps company to identify

their objectives and work on that as soon as possible (Kihn and Ihantola, 2015). The integration

of these two systems is very important in an organization to implement in order to take decision

for productivity of firm. They control duplication of work, saves time and enhance ability of

firm. For Aston chemicals, it is very important to have both systems for sound decisions (Malmi,

2016).

TASK 2

A.1 Explaining the absorption costing and marginal costing

Absorption costing

Absorption costing is the method collection of all the production cost and allocating them

to the actual individual product. In other words, it means that entire cost related with production

like direct labour, overhead costs and direct material etc are included. Absorption costing

methods not only entails cost but also all the manufacturing expenses whether fined and variable.

This technique is also known as full absorption costing. This basically differs from other costing

methods because it takes fixed manufacturing expenses into consideration. For Aston absorption

costing has proven very much beneficial. It determines the value of fixed costs participating in

production (Nitzl, 2018). It shows less alteration in net profits in case of constant production but

fluctuating sales.

Marginal costing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

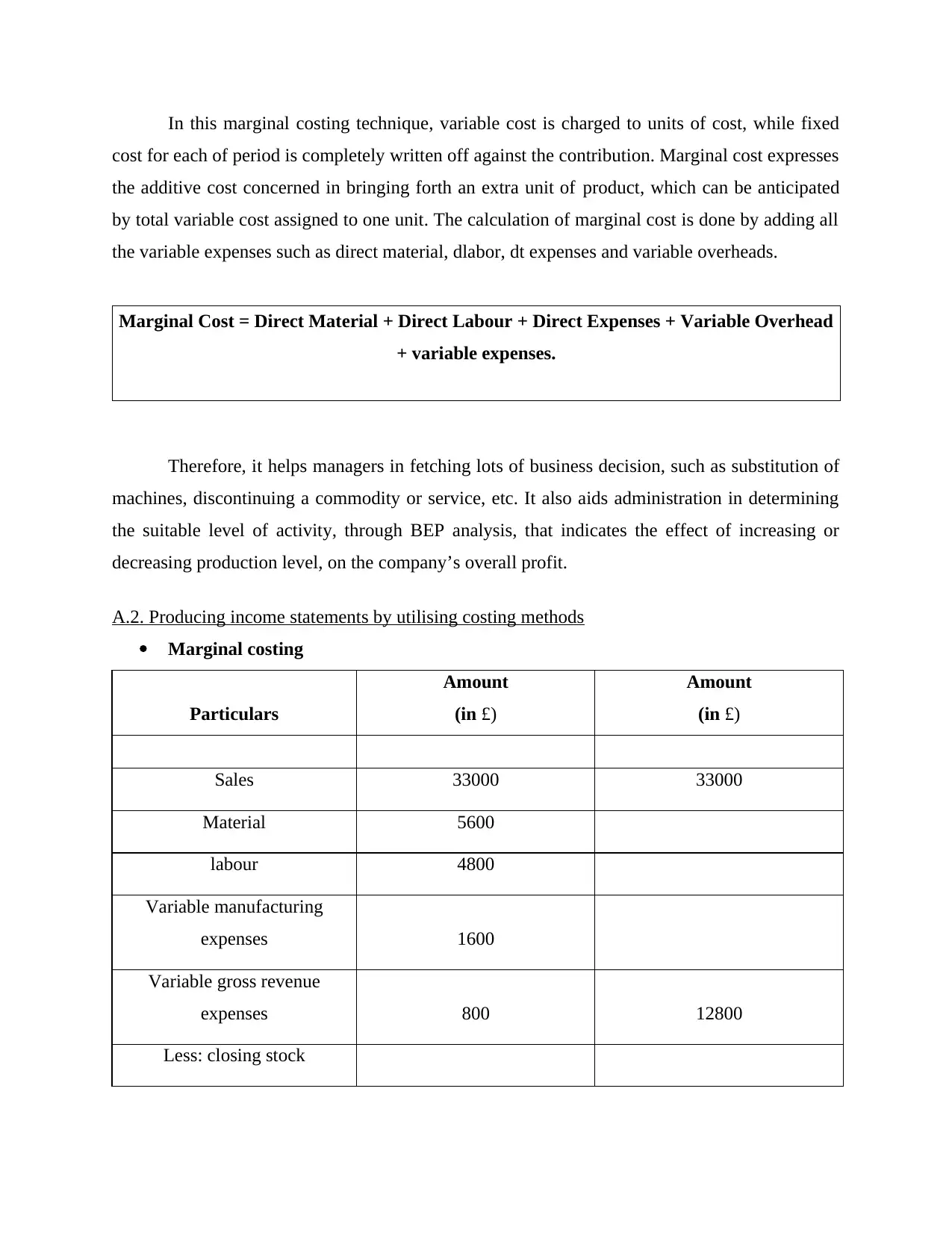

In this marginal costing technique, variable cost is charged to units of cost, while fixed

cost for each of period is completely written off against the contribution. Marginal cost expresses

the additive cost concerned in bringing forth an extra unit of product, which can be anticipated

by total variable cost assigned to one unit. The calculation of marginal cost is done by adding all

the variable expenses such as direct material, dlabor, dt expenses and variable overheads.

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overhead

+ variable expenses.

Therefore, it helps managers in fetching lots of business decision, such as substitution of

machines, discontinuing a commodity or service, etc. It also aids administration in determining

the suitable level of activity, through BEP analysis, that indicates the effect of increasing or

decreasing production level, on the company’s overall profit.

A.2. Producing income statements by utilising costing methods

Marginal costing

Particulars

Amount

(in £)

Amount

(in £)

Sales 33000 33000

Material 5600

labour 4800

Variable manufacturing

expenses 1600

Variable gross revenue

expenses 800 12800

Less: closing stock

cost for each of period is completely written off against the contribution. Marginal cost expresses

the additive cost concerned in bringing forth an extra unit of product, which can be anticipated

by total variable cost assigned to one unit. The calculation of marginal cost is done by adding all

the variable expenses such as direct material, dlabor, dt expenses and variable overheads.

Marginal Cost = Direct Material + Direct Labour + Direct Expenses + Variable Overhead

+ variable expenses.

Therefore, it helps managers in fetching lots of business decision, such as substitution of

machines, discontinuing a commodity or service, etc. It also aids administration in determining

the suitable level of activity, through BEP analysis, that indicates the effect of increasing or

decreasing production level, on the company’s overall profit.

A.2. Producing income statements by utilising costing methods

Marginal costing

Particulars

Amount

(in £)

Amount

(in £)

Sales 33000 33000

Material 5600

labour 4800

Variable manufacturing

expenses 1600

Variable gross revenue

expenses 800 12800

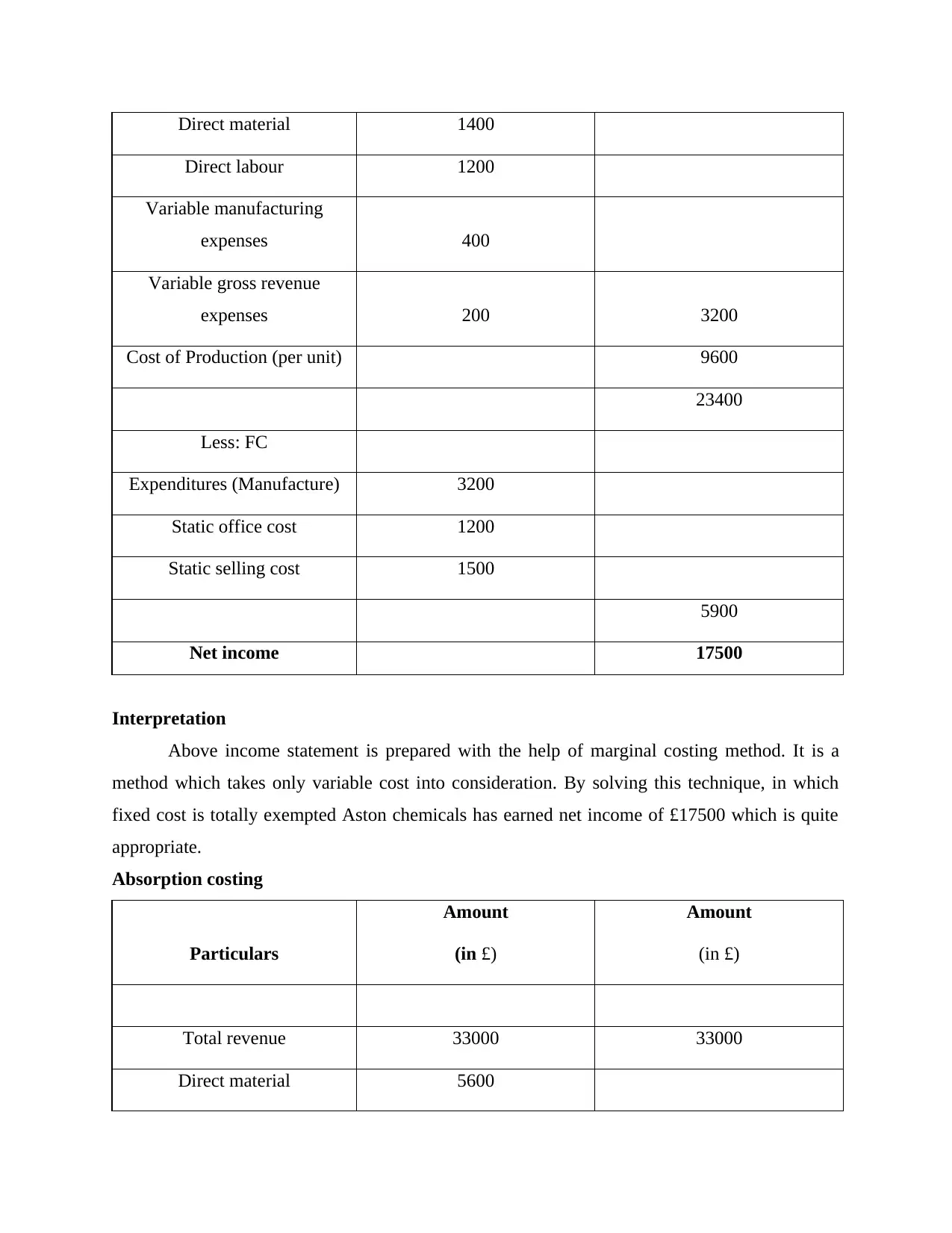

Less: closing stock

Direct material 1400

Direct labour 1200

Variable manufacturing

expenses 400

Variable gross revenue

expenses 200 3200

Cost of Production (per unit) 9600

23400

Less: FC

Expenditures (Manufacture) 3200

Static office cost 1200

Static selling cost 1500

5900

Net income 17500

Interpretation

Above income statement is prepared with the help of marginal costing method. It is a

method which takes only variable cost into consideration. By solving this technique, in which

fixed cost is totally exempted Aston chemicals has earned net income of £17500 which is quite

appropriate.

Absorption costing

Particulars

Amount

(in £)

Amount

(in £)

Total revenue 33000 33000

Direct material 5600

Direct labour 1200

Variable manufacturing

expenses 400

Variable gross revenue

expenses 200 3200

Cost of Production (per unit) 9600

23400

Less: FC

Expenditures (Manufacture) 3200

Static office cost 1200

Static selling cost 1500

5900

Net income 17500

Interpretation

Above income statement is prepared with the help of marginal costing method. It is a

method which takes only variable cost into consideration. By solving this technique, in which

fixed cost is totally exempted Aston chemicals has earned net income of £17500 which is quite

appropriate.

Absorption costing

Particulars

Amount

(in £)

Amount

(in £)

Total revenue 33000 33000

Direct material 5600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

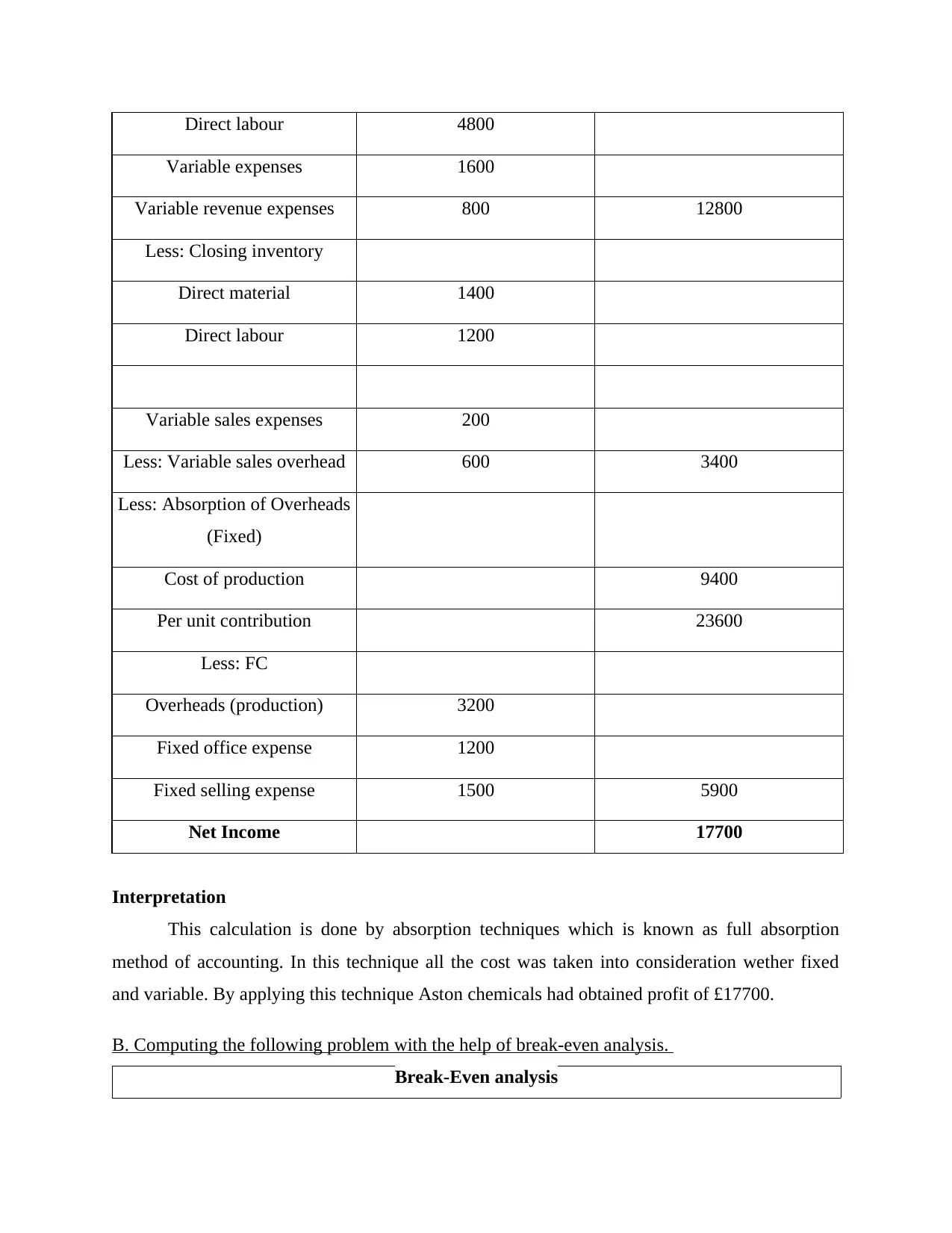

Direct labour 4800

Variable expenses 1600

Variable revenue expenses 800 12800

Less: Closing inventory

Direct material 1400

Direct labour 1200

Variable sales expenses 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

Cost of production 9400

Per unit contribution 23600

Less: FC

Overheads (production) 3200

Fixed office expense 1200

Fixed selling expense 1500 5900

Net Income 17700

Interpretation

This calculation is done by absorption techniques which is known as full absorption

method of accounting. In this technique all the cost was taken into consideration wether fixed

and variable. By applying this technique Aston chemicals had obtained profit of £17700.

B. Computing the following problem with the help of break-even analysis.

Break-Even analysis

Variable expenses 1600

Variable revenue expenses 800 12800

Less: Closing inventory

Direct material 1400

Direct labour 1200

Variable sales expenses 200

Less: Variable sales overhead 600 3400

Less: Absorption of Overheads

(Fixed)

Cost of production 9400

Per unit contribution 23600

Less: FC

Overheads (production) 3200

Fixed office expense 1200

Fixed selling expense 1500 5900

Net Income 17700

Interpretation

This calculation is done by absorption techniques which is known as full absorption

method of accounting. In this technique all the cost was taken into consideration wether fixed

and variable. By applying this technique Aston chemicals had obtained profit of £17700.

B. Computing the following problem with the help of break-even analysis.

Break-Even analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

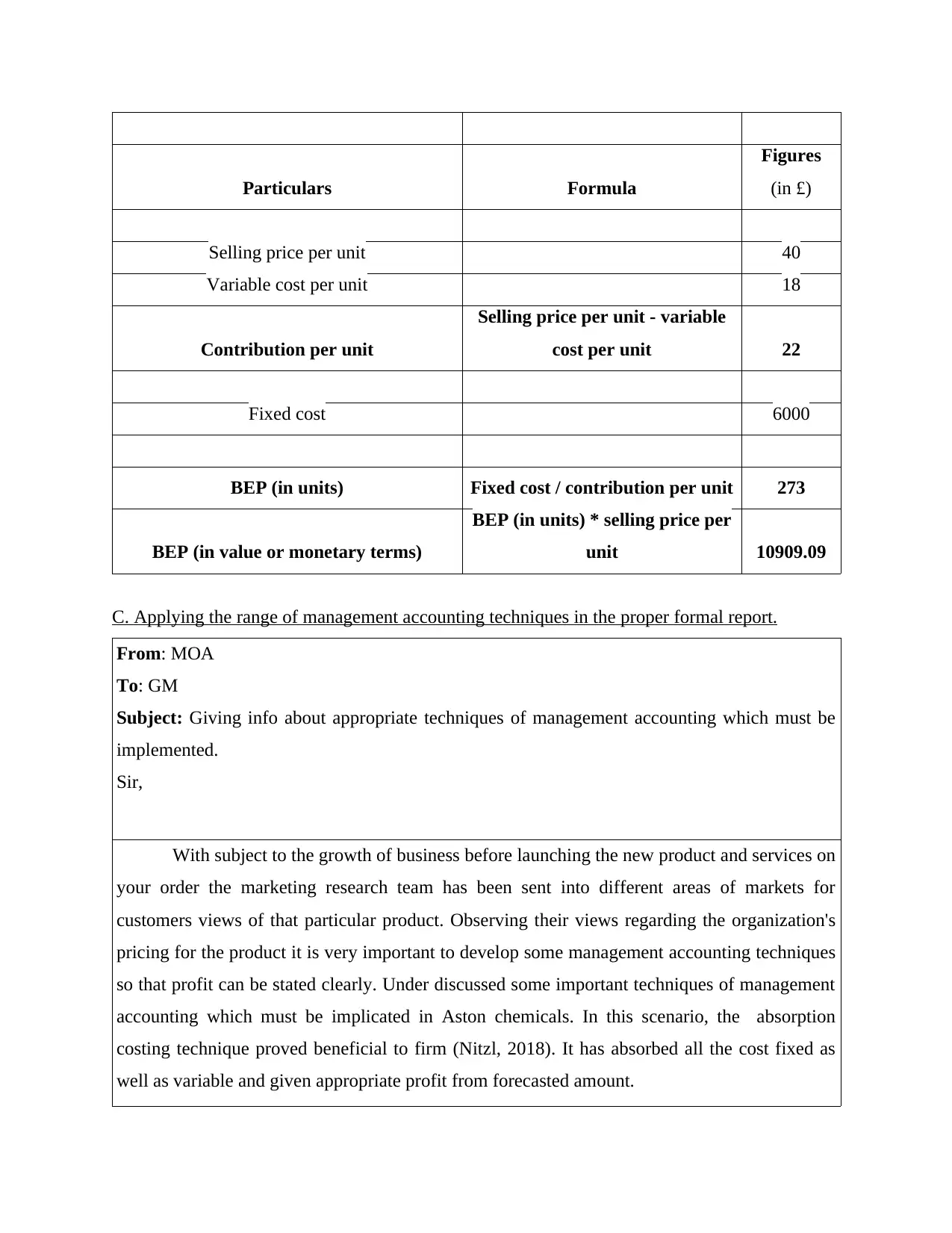

Particulars Formula

Figures

(in £)

Selling price per unit 40

Variable cost per unit 18

Contribution per unit

Selling price per unit - variable

cost per unit 22

Fixed cost 6000

BEP (in units) Fixed cost / contribution per unit 273

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 10909.09

C. Applying the range of management accounting techniques in the proper formal report.

From: MOA

To: GM

Subject: Giving info about appropriate techniques of management accounting which must be

implemented.

Sir,

With subject to the growth of business before launching the new product and services on

your order the marketing research team has been sent into different areas of markets for

customers views of that particular product. Observing their views regarding the organization's

pricing for the product it is very important to develop some management accounting techniques

so that profit can be stated clearly. Under discussed some important techniques of management

accounting which must be implicated in Aston chemicals. In this scenario, the absorption

costing technique proved beneficial to firm (Nitzl, 2018). It has absorbed all the cost fixed as

well as variable and given appropriate profit from forecasted amount.

Figures

(in £)

Selling price per unit 40

Variable cost per unit 18

Contribution per unit

Selling price per unit - variable

cost per unit 22

Fixed cost 6000

BEP (in units) Fixed cost / contribution per unit 273

BEP (in value or monetary terms)

BEP (in units) * selling price per

unit 10909.09

C. Applying the range of management accounting techniques in the proper formal report.

From: MOA

To: GM

Subject: Giving info about appropriate techniques of management accounting which must be

implemented.

Sir,

With subject to the growth of business before launching the new product and services on

your order the marketing research team has been sent into different areas of markets for

customers views of that particular product. Observing their views regarding the organization's

pricing for the product it is very important to develop some management accounting techniques

so that profit can be stated clearly. Under discussed some important techniques of management

accounting which must be implicated in Aston chemicals. In this scenario, the absorption

costing technique proved beneficial to firm (Nitzl, 2018). It has absorbed all the cost fixed as

well as variable and given appropriate profit from forecasted amount.

Cash flow statements, historical checking

Analyzing the financial accounts

Financial accounting

Communicating the information etc.

Review of the accounts

On comparing both the techniques it is found that profit is more in absorption than to

marginal costing techniques. So, it should be appropriate to use absorption costing method in

place of marginal. This method of accounting consisted of some management techniques like

Cash flows

Startup costing

Balance sheet

Budget and forecast table.

Thank you

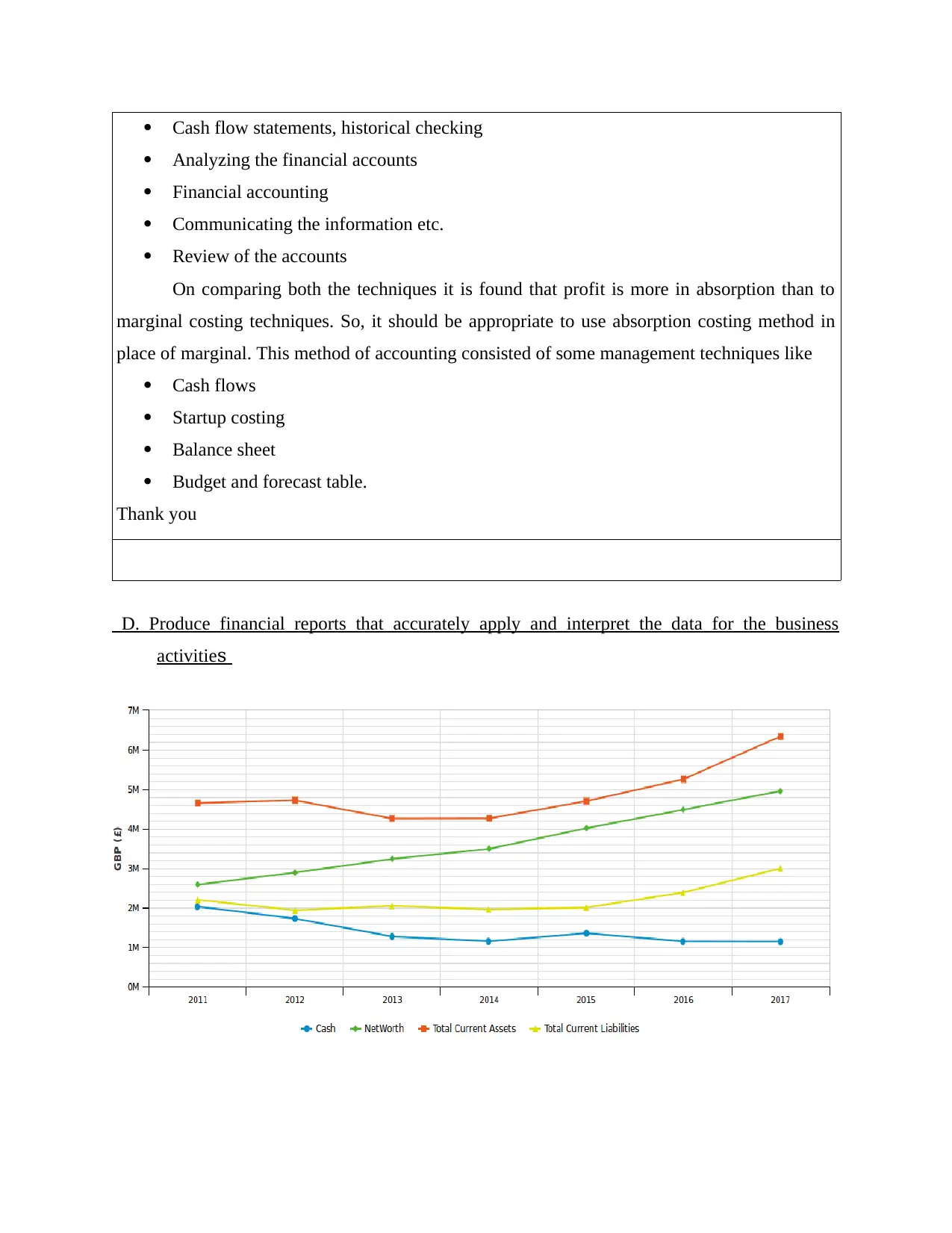

D. Produce financial reports that accurately apply and interpret the data for the business

activities

Analyzing the financial accounts

Financial accounting

Communicating the information etc.

Review of the accounts

On comparing both the techniques it is found that profit is more in absorption than to

marginal costing techniques. So, it should be appropriate to use absorption costing method in

place of marginal. This method of accounting consisted of some management techniques like

Cash flows

Startup costing

Balance sheet

Budget and forecast table.

Thank you

D. Produce financial reports that accurately apply and interpret the data for the business

activities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.