Management Accounting Report: Analysis of Aston Martin's System

VerifiedAdded on 2020/12/18

|17

|3875

|411

Report

AI Summary

This report delves into the realm of management accounting, employing Aston Martin, an engineering and automobile manufacturing company, as a case study. It initiates with an introduction to management accounting, also recognized as cost accounting, elucidating its pivotal role in assisting managers to pinpoint production costs, devise strategies for cost reduction, and maximize profitability. The report then dissects various facets of management accounting, encompassing the essential requirements and different types of management accounting systems, such as cost accounting and inventory management systems. It also highlights the methods used for management accounting reporting, including budget reports, and performance reports. Furthermore, the report explores the benefits of these systems and their practical applications, along with the integration of management accounting systems and reporting. Annex A provides data and analysis using techniques such as payback period and Net Present Value (NPV) calculations. The report also discusses different planning tools used for preparing and forecasting budgets, and it concludes with an evaluation of how these tools aid in problem-solving and support organizations in achieving sustainable success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Part A...............................................................................................................................................1

LO1: Understanding of Management Accounting System....................................................1

P1 Essential requirements and Different types of Management Accounting system.............1

P2 Different methods used for Management accounting reporting........................................3

M1 Benefits of management accounting system and their applications................................4

D1 Integration of management accounting systems and management accounting reporting 4

Part B...............................................................................................................................................5

LO2: Application of range of Management Accounting Techniques....................................5

P3............................................................................................................................................5

M2...........................................................................................................................................5

D2...........................................................................................................................................5

ACTIVITY 2....................................................................................................................................5

Part A...............................................................................................................................................5

LO3: Uses of planing tools used in Management Accounting...............................................5

P4. Advantages and disadvantages of different types of planning tools................................5

M3. Use of different planning tools and their application for preparing and forecasting budget

................................................................................................................................................7

P5. Comparison of how organisations are adapting management accounting systems to

respond to financial problems................................................................................................7

M4. Analysis of how in responding to financial problems, management accounting can lead

organisation to sustainable success........................................................................................9

D3. An evaluation of how planning tools for accounting help to solve problems and support

organisations with sustainable success...................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Part A...............................................................................................................................................1

LO1: Understanding of Management Accounting System....................................................1

P1 Essential requirements and Different types of Management Accounting system.............1

P2 Different methods used for Management accounting reporting........................................3

M1 Benefits of management accounting system and their applications................................4

D1 Integration of management accounting systems and management accounting reporting 4

Part B...............................................................................................................................................5

LO2: Application of range of Management Accounting Techniques....................................5

P3............................................................................................................................................5

M2...........................................................................................................................................5

D2...........................................................................................................................................5

ACTIVITY 2....................................................................................................................................5

Part A...............................................................................................................................................5

LO3: Uses of planing tools used in Management Accounting...............................................5

P4. Advantages and disadvantages of different types of planning tools................................5

M3. Use of different planning tools and their application for preparing and forecasting budget

................................................................................................................................................7

P5. Comparison of how organisations are adapting management accounting systems to

respond to financial problems................................................................................................7

M4. Analysis of how in responding to financial problems, management accounting can lead

organisation to sustainable success........................................................................................9

D3. An evaluation of how planning tools for accounting help to solve problems and support

organisations with sustainable success...................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting which is also known as cost accounting (Alyousef and Mickan

2016). This is the process which help managers to identify cost of production and find ways to

reduce cost of production and maximize its profit. It focuses on every field of accounting and

gives this information to the management about the operations of business. In this report the

engineering company taken for the purpose to study of various task is Aston Martin. Aston

Martin is purely in field of engineering and auto mobile manufacturing. With the help of this

report managers analyse uses of management accounting process and different types of

management accounting system. This reports also gives different methods used for the purpose

of management accounting reporting. This report also talks about different types of tools used for

planning the budgetary control and also advantages and disadvantages of budgetary control tools.

ACTIVITY 1

Part A

LO1: Understanding of Management Accounting System

P1 Essential requirements and Different types of Management Accounting system.

Management Accounting: management accounting is a process of preparation of

accounts and report which help mangers to get accurate position of the company (Bellassen and

Stephan 2015). It also helps companies to make day to day short term decisions, for this the

information required by managers are timely financial information and statistical information.

Management accounting help mangers to generate monthly and weekly reports which assists

managers in decision making process and also these reports are used by the organisation's

internal stakeholders. Following are some types of management accounting system.

Cost Accounting System: A cost accounting system is a system which helps the

organisation to estimate cost of products incurred by company to produces its products (Brierley

and Gwilliam 2017). It also helps mangers to analyse their cost and check its profitability,

control its cost and for valuation of its inventory. Mostly cost accounting system helps managers

to reduce its cost by analysing the expenses and to cut those expense which are not necessary.

Aston Martin also uses this cost accounting system to see the cost of the products. There are

1

Management accounting which is also known as cost accounting (Alyousef and Mickan

2016). This is the process which help managers to identify cost of production and find ways to

reduce cost of production and maximize its profit. It focuses on every field of accounting and

gives this information to the management about the operations of business. In this report the

engineering company taken for the purpose to study of various task is Aston Martin. Aston

Martin is purely in field of engineering and auto mobile manufacturing. With the help of this

report managers analyse uses of management accounting process and different types of

management accounting system. This reports also gives different methods used for the purpose

of management accounting reporting. This report also talks about different types of tools used for

planning the budgetary control and also advantages and disadvantages of budgetary control tools.

ACTIVITY 1

Part A

LO1: Understanding of Management Accounting System

P1 Essential requirements and Different types of Management Accounting system.

Management Accounting: management accounting is a process of preparation of

accounts and report which help mangers to get accurate position of the company (Bellassen and

Stephan 2015). It also helps companies to make day to day short term decisions, for this the

information required by managers are timely financial information and statistical information.

Management accounting help mangers to generate monthly and weekly reports which assists

managers in decision making process and also these reports are used by the organisation's

internal stakeholders. Following are some types of management accounting system.

Cost Accounting System: A cost accounting system is a system which helps the

organisation to estimate cost of products incurred by company to produces its products (Brierley

and Gwilliam 2017). It also helps mangers to analyse their cost and check its profitability,

control its cost and for valuation of its inventory. Mostly cost accounting system helps managers

to reduce its cost by analysing the expenses and to cut those expense which are not necessary.

Aston Martin also uses this cost accounting system to see the cost of the products. There are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

mainly two types of cost accounting system used in the engineering company the Job Order

Costing and the Process Costing

Job Order Costing System: In job order costing system it spreads the cost over the

particular job order (Busco and Quattrone 2015). Which helps the managers to see the individual

cost incurred in order to meet that order. This system is used in the Aston Martin as it has to find

out the individual cost of each model of the car produced.

Process Costing: Process order costing system gives the advantage to the company to find

out the cost involved in the particular process (Common 2017). As in the Aston Martin it is very

important for the company to see the individual cost involved in different process such as

installation of accessories, installation of tyres, finishing etc. In the auto mobile industry there

are various different process involved in the production of a car for this the car has to go through

various process and it is very essential for the company to record the cost related to different

process.

Inventory Management Systems: Inventory refers to the stock of the company, stock

includes the raw material, finished good and the stock which is stuck in work in progress

(Davila, Foster and Jia, 2015). It is very important for the company to manage their stock. To

manage the stock in an organisation an inventory management system is used, which gives the

benefit to the company to properly manage the stock in the company so that the storing cost of

the stock does not increase. It also gives the clear picture of the finished goods which is still in

the showrooms and take some necessary steps to clear those blocked stock. Aston Martin uses

this system to see that how many cars are still not sold and what new techniques can be used by

the company to clear those stock. There are many important functions of the inventory

management system which helps the company to create Purchase order if the raw materials is

running out, this system also provides the function to relocate, receive and dispose of inventory

which is stuck in the manufacturing plant. There are some benefits of using the inventory

management system as it helps the company to improve its inventory accuracy and also to

improve the proper work flow in the company.

Price Optimising System: Price optimising system is a system which is mathematically

programmed to calculate that how at the different level of prices the demand for the product

varies (Drake, Roulstone and Thornock, 2016).It is used to analyse the variations in demand and

2

Costing and the Process Costing

Job Order Costing System: In job order costing system it spreads the cost over the

particular job order (Busco and Quattrone 2015). Which helps the managers to see the individual

cost incurred in order to meet that order. This system is used in the Aston Martin as it has to find

out the individual cost of each model of the car produced.

Process Costing: Process order costing system gives the advantage to the company to find

out the cost involved in the particular process (Common 2017). As in the Aston Martin it is very

important for the company to see the individual cost involved in different process such as

installation of accessories, installation of tyres, finishing etc. In the auto mobile industry there

are various different process involved in the production of a car for this the car has to go through

various process and it is very essential for the company to record the cost related to different

process.

Inventory Management Systems: Inventory refers to the stock of the company, stock

includes the raw material, finished good and the stock which is stuck in work in progress

(Davila, Foster and Jia, 2015). It is very important for the company to manage their stock. To

manage the stock in an organisation an inventory management system is used, which gives the

benefit to the company to properly manage the stock in the company so that the storing cost of

the stock does not increase. It also gives the clear picture of the finished goods which is still in

the showrooms and take some necessary steps to clear those blocked stock. Aston Martin uses

this system to see that how many cars are still not sold and what new techniques can be used by

the company to clear those stock. There are many important functions of the inventory

management system which helps the company to create Purchase order if the raw materials is

running out, this system also provides the function to relocate, receive and dispose of inventory

which is stuck in the manufacturing plant. There are some benefits of using the inventory

management system as it helps the company to improve its inventory accuracy and also to

improve the proper work flow in the company.

Price Optimising System: Price optimising system is a system which is mathematically

programmed to calculate that how at the different level of prices the demand for the product

varies (Drake, Roulstone and Thornock, 2016).It is used to analyse the variations in demand and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

combining the data with the information provided on inventory and cost levels in order to

recommend the prices which will help the company to improve its profits.

P2 Different methods used for Management accounting reporting.

Management Accounting Report: Accounting report are considered as a crucial part of

any accounting system as it helps the management to see the actual picture and position of the

company (Fayol, 2016). Accounting reports are created after every quarter to give a proper and

holistic view of the company's growth and to see that the resources are utilized in the company

efficiently and effectively. These helps the company to have a clear insights of the company and

the strategies which are being used in the company. Aston Martin also uses these reports to

check the validity of the strategies which is being developed by the top level management that

are working properly or not or the company needs to formulate new strategies. There are many

accounting reports which help the management to take necessary decisions are mentioned as

below:

Budget Reports: Budget reports are the very important reports which helps in measuring

the company,s overall performance and also helps in comparing the stability and growth from

since the last year (Hsu and Lin 2016). As the budget reports is the estimated report for the

company which show the cost and all the expenses on the estimate basis, now it becomes the

duty of the managerial staff to meet all the expenses in the given budget and can even try to

reduce the expenses. In the budget reports the company list all the various sources of income for

the company and the expenditure which the company might incur. In Aston Martin the top level

management sees all the report and carefully analyse it to make right decisions for the benefits of

the company.

Account Receivable Aging Reports: Account receivable aging report is the reports

which shows the position of the debtors (Jefrey ed., 2018). This report is considered as

mandatory reports for those organisation which relies heavily on the credit sales. With the help

of this report the company can have the track of the defaulters and if the rate of defaulters

increase the company can re think their credit policy. The company should follow the strict credit

policy so that the company can maintain the in flow of the cash as it is considered as one of the

most important part of the working capital. In Aston Martin this report plays an important role as

the company sends his finished cars to the different exclusive showrooms on credit basis and it is

very important for the company to manage its debtors.

3

recommend the prices which will help the company to improve its profits.

P2 Different methods used for Management accounting reporting.

Management Accounting Report: Accounting report are considered as a crucial part of

any accounting system as it helps the management to see the actual picture and position of the

company (Fayol, 2016). Accounting reports are created after every quarter to give a proper and

holistic view of the company's growth and to see that the resources are utilized in the company

efficiently and effectively. These helps the company to have a clear insights of the company and

the strategies which are being used in the company. Aston Martin also uses these reports to

check the validity of the strategies which is being developed by the top level management that

are working properly or not or the company needs to formulate new strategies. There are many

accounting reports which help the management to take necessary decisions are mentioned as

below:

Budget Reports: Budget reports are the very important reports which helps in measuring

the company,s overall performance and also helps in comparing the stability and growth from

since the last year (Hsu and Lin 2016). As the budget reports is the estimated report for the

company which show the cost and all the expenses on the estimate basis, now it becomes the

duty of the managerial staff to meet all the expenses in the given budget and can even try to

reduce the expenses. In the budget reports the company list all the various sources of income for

the company and the expenditure which the company might incur. In Aston Martin the top level

management sees all the report and carefully analyse it to make right decisions for the benefits of

the company.

Account Receivable Aging Reports: Account receivable aging report is the reports

which shows the position of the debtors (Jefrey ed., 2018). This report is considered as

mandatory reports for those organisation which relies heavily on the credit sales. With the help

of this report the company can have the track of the defaulters and if the rate of defaulters

increase the company can re think their credit policy. The company should follow the strict credit

policy so that the company can maintain the in flow of the cash as it is considered as one of the

most important part of the working capital. In Aston Martin this report plays an important role as

the company sends his finished cars to the different exclusive showrooms on credit basis and it is

very important for the company to manage its debtors.

3

Cost Managerial Accounting Reports: This report helps the company to see their cost

of production and it computes its cost of articles which are produced (Kolk and Perego, 2015).

While preparing this report various cost such as cost of raw material, labour cost, overhead cost

and all other costs which are added to products are considered. This report help managers to take

the estimated cost of their product and selling price of product to check profit margin earned by

sale of that product. This managerial report also contains the waste in inventory, cost which is

being paid to labours on hourly basis and all the other variable overhead and fixed overhead cost.

It provide exact understanding of various costs directly or indirectly associated with the

production, which is assumed to be essential part for betterment and optimum utilization of

resources in all departments.

Performance Report: These reports are created by companies to review its performance

during the year (Labro, 2015). While preparing this report performance of employee and all other

staffs as a whole. Mangers uses this report to take make necessary decisions for the benefits of

organisation. With the help of these reports individual who performed well during the year are

awarded.

M1 Benefits of management accounting system and their applications

Management accounting system help mangers to make the necessary measures for the

company future growth (Leung, 2016). It provides framework for mangers to control its cost of

products and maximize its profit. It also helps to measure actual performance of the company in

contrast with the budgets. It also gives management a way which can help in maximizing the

return on the capital employed.

D1 Integration of management accounting systems and management accounting reporting

In Aston Martin mangers uses management accounting system to generate the reports

which is required by company to plan for the next year. Management accounting reports and

management accounting system is closely related and interlinked to each other (Luft, 2016).

Management accounting system gives the access to generate these reports and the reports

generated are later on used by the mangers to take necessary step to improve the position of the

company.

4

of production and it computes its cost of articles which are produced (Kolk and Perego, 2015).

While preparing this report various cost such as cost of raw material, labour cost, overhead cost

and all other costs which are added to products are considered. This report help managers to take

the estimated cost of their product and selling price of product to check profit margin earned by

sale of that product. This managerial report also contains the waste in inventory, cost which is

being paid to labours on hourly basis and all the other variable overhead and fixed overhead cost.

It provide exact understanding of various costs directly or indirectly associated with the

production, which is assumed to be essential part for betterment and optimum utilization of

resources in all departments.

Performance Report: These reports are created by companies to review its performance

during the year (Labro, 2015). While preparing this report performance of employee and all other

staffs as a whole. Mangers uses this report to take make necessary decisions for the benefits of

organisation. With the help of these reports individual who performed well during the year are

awarded.

M1 Benefits of management accounting system and their applications

Management accounting system help mangers to make the necessary measures for the

company future growth (Leung, 2016). It provides framework for mangers to control its cost of

products and maximize its profit. It also helps to measure actual performance of the company in

contrast with the budgets. It also gives management a way which can help in maximizing the

return on the capital employed.

D1 Integration of management accounting systems and management accounting reporting

In Aston Martin mangers uses management accounting system to generate the reports

which is required by company to plan for the next year. Management accounting reports and

management accounting system is closely related and interlinked to each other (Luft, 2016).

Management accounting system gives the access to generate these reports and the reports

generated are later on used by the mangers to take necessary step to improve the position of the

company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part B

LO2: Application of range of Management Accounting Techniques

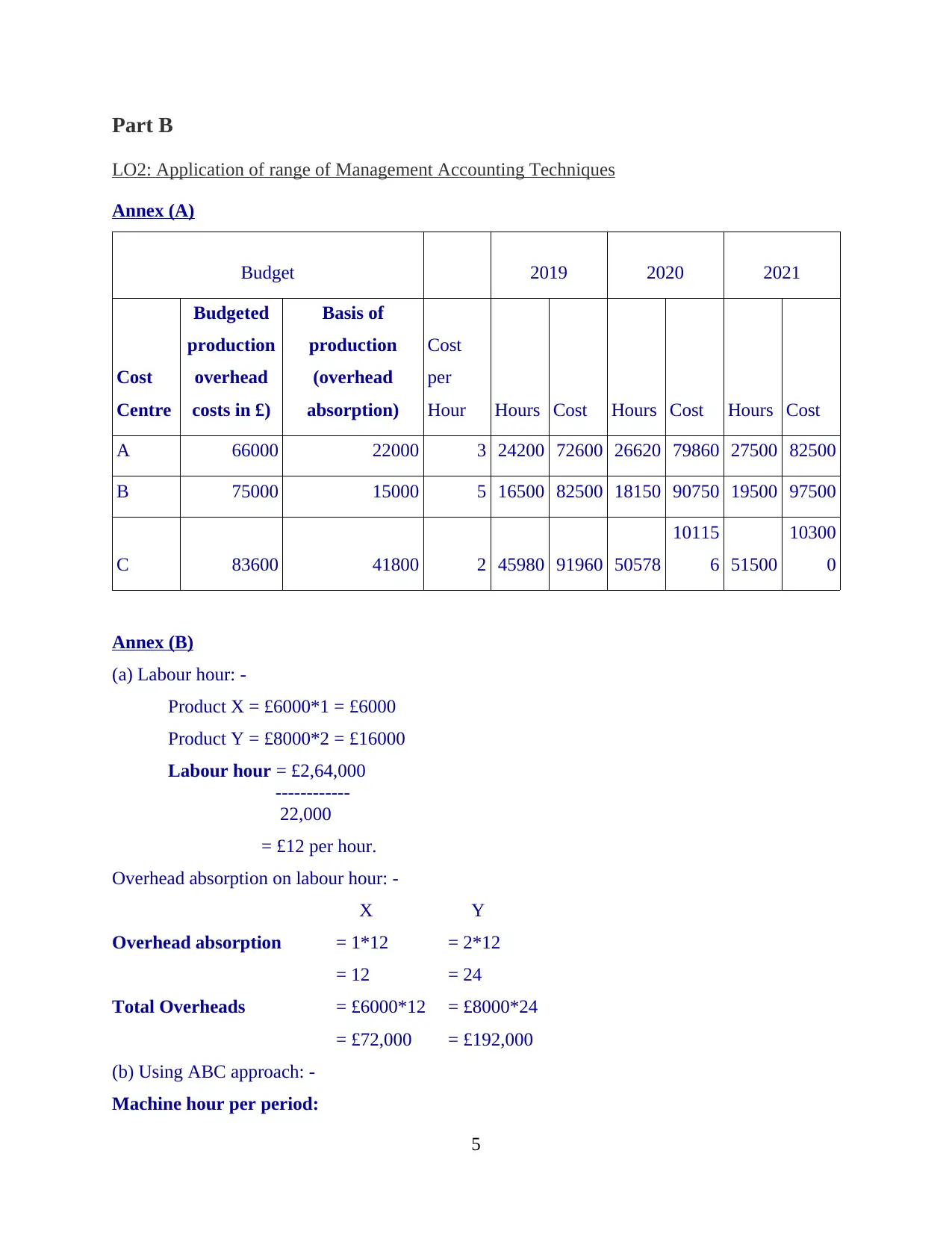

Annex (A)

Budget 2019 2020 2021

Cost

Centre

Budgeted

production

overhead

costs in £)

Basis of

production

(overhead

absorption)

Cost

per

Hour Hours Cost Hours Cost Hours Cost

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

5

LO2: Application of range of Management Accounting Techniques

Annex (A)

Budget 2019 2020 2021

Cost

Centre

Budgeted

production

overhead

costs in £)

Basis of

production

(overhead

absorption)

Cost

per

Hour Hours Cost Hours Cost Hours Cost

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

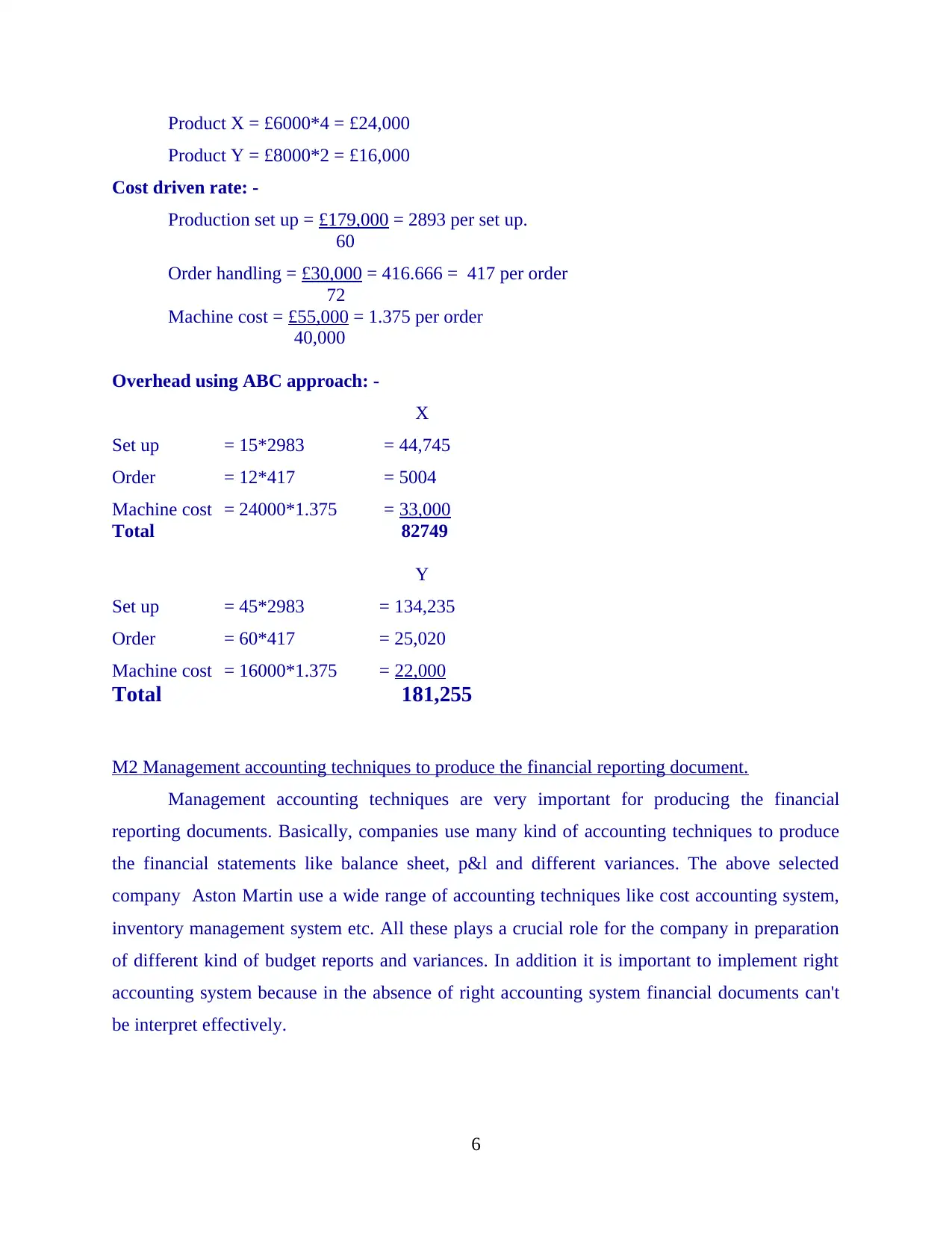

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

M2 Management accounting techniques to produce the financial reporting document.

Management accounting techniques are very important for producing the financial

reporting documents. Basically, companies use many kind of accounting techniques to produce

the financial statements like balance sheet, p&l and different variances. The above selected

company Aston Martin use a wide range of accounting techniques like cost accounting system,

inventory management system etc. All these plays a crucial role for the company in preparation

of different kind of budget reports and variances. In addition it is important to implement right

accounting system because in the absence of right accounting system financial documents can't

be interpret effectively.

6

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

M2 Management accounting techniques to produce the financial reporting document.

Management accounting techniques are very important for producing the financial

reporting documents. Basically, companies use many kind of accounting techniques to produce

the financial statements like balance sheet, p&l and different variances. The above selected

company Aston Martin use a wide range of accounting techniques like cost accounting system,

inventory management system etc. All these plays a crucial role for the company in preparation

of different kind of budget reports and variances. In addition it is important to implement right

accounting system because in the absence of right accounting system financial documents can't

be interpret effectively.

6

D2 Financial reports that interpret the a range of business activities.

Financial reports are those reports which reflects the business activities in a conclusion

way. Herein, the selected company Aston Martin use activity based costing approach to

calculate various costs. In 2019 they incurs the cost of £ 72600 which will increase continuously

in the further years and becomes £ 82500 in 2021. As well as in annex B cost driven rate is

categorised into three parts that are production setup, order handling and machine cost. That is £

82749 in project X and £ 181255 in project Y.

ACTIVITY 2

Part A

LO3: Uses of planing tools used in Management Accounting

P4. Advantages and disadvantages of different types of planning tools

Budget is considered as a formal document that is generally prepared on the basis of

revenue as well expenditures (McVay, Kennedy and Fullerton, 2016). It is usually formulate by

organisation in order to allot finances for many functions and process after examining the

receipts, expenditure and profit of previous year.

Now a days in large or reputed company, it can be formulated through e- spreadsheet, business

software as this helps to create effective framework and remove computational mistakes. In

respect of Aston Martin prepare budgets through electronic spreadsheet as it is simple way of

firm to accomplish effectual outcomes in goods manner.

Budgetary control is considered as methods of examining the outcomes with budgeted

figures for upcoming years as well as actual performance to evaluate the variance within

organisation (Monden, 2018). It usually concentrate on controlling cost that are included in

budget formulation, accountabilities for preparing the list of budget by attaining maximum

profitability for company.

Aston Martin which is a engineering company should need to manage and control the

budgeted figure as well as also many process and activities in order to accomplish sustainability

in growth and maximise profitability. Organisation should prepare a effective plan for

7

Financial reports are those reports which reflects the business activities in a conclusion

way. Herein, the selected company Aston Martin use activity based costing approach to

calculate various costs. In 2019 they incurs the cost of £ 72600 which will increase continuously

in the further years and becomes £ 82500 in 2021. As well as in annex B cost driven rate is

categorised into three parts that are production setup, order handling and machine cost. That is £

82749 in project X and £ 181255 in project Y.

ACTIVITY 2

Part A

LO3: Uses of planing tools used in Management Accounting

P4. Advantages and disadvantages of different types of planning tools

Budget is considered as a formal document that is generally prepared on the basis of

revenue as well expenditures (McVay, Kennedy and Fullerton, 2016). It is usually formulate by

organisation in order to allot finances for many functions and process after examining the

receipts, expenditure and profit of previous year.

Now a days in large or reputed company, it can be formulated through e- spreadsheet, business

software as this helps to create effective framework and remove computational mistakes. In

respect of Aston Martin prepare budgets through electronic spreadsheet as it is simple way of

firm to accomplish effectual outcomes in goods manner.

Budgetary control is considered as methods of examining the outcomes with budgeted

figures for upcoming years as well as actual performance to evaluate the variance within

organisation (Monden, 2018). It usually concentrate on controlling cost that are included in

budget formulation, accountabilities for preparing the list of budget by attaining maximum

profitability for company.

Aston Martin which is a engineering company should need to manage and control the

budgeted figure as well as also many process and activities in order to accomplish sustainability

in growth and maximise profitability. Organisation should prepare a effective plan for

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

controlling the budget. Therefore, Aston Martin can use various planning tools which are

mentioned below:

Contingency tools:

This tool is helpful to identify and allocate the risky factors that can effects the operation,

functions, growth, performance etc (Newberry, 2015). of the organisation in future. Aston

Martin can apply this planning tools of budgetary control so that they can examine as well as

measure the financial position in terms of net and gross profitability condition and performance

of many organisational activities. Respective company required to analyse cause and formulate

effective strategies so that they can solve that rapidly.

Advantage:

With the help of this tool company can find out the potential resources in case any types

of difficulties occurs at the time of performing activities regarding resources.

Disadvantage:

Through this tool manager of the firm can not control their internal as well as external

functions as these are uncertain in nature.

Scenario Planning tool:

Scenario planning tool developed a structural and organised way to formulate framework

for strategical planning of the organisation (Nilsson and Stockenstrand, 2015). This is helpful to

create a base for assuming possible impacts of environments within firm. Aston Martin can use

this tool to recognise expected occurrent which can affect the organisational segment of business

in upcoming years.

Advantage:

This tool also refers as the flexible tool so that it can be modified as per the stimulated

situations of the company.

Disadvantage:

This tool is not suitable at the time of practical implications as it is more time consuming.

Forecasting planning tools:

Forecasting tools us used by the firm to develop a framework for future occurrences and

happenings by considering previous as well as present adjustment in trends (Parker and

Fleischman, 2017). For profitable results from this tool an appropriate and relevant data are used

8

mentioned below:

Contingency tools:

This tool is helpful to identify and allocate the risky factors that can effects the operation,

functions, growth, performance etc (Newberry, 2015). of the organisation in future. Aston

Martin can apply this planning tools of budgetary control so that they can examine as well as

measure the financial position in terms of net and gross profitability condition and performance

of many organisational activities. Respective company required to analyse cause and formulate

effective strategies so that they can solve that rapidly.

Advantage:

With the help of this tool company can find out the potential resources in case any types

of difficulties occurs at the time of performing activities regarding resources.

Disadvantage:

Through this tool manager of the firm can not control their internal as well as external

functions as these are uncertain in nature.

Scenario Planning tool:

Scenario planning tool developed a structural and organised way to formulate framework

for strategical planning of the organisation (Nilsson and Stockenstrand, 2015). This is helpful to

create a base for assuming possible impacts of environments within firm. Aston Martin can use

this tool to recognise expected occurrent which can affect the organisational segment of business

in upcoming years.

Advantage:

This tool also refers as the flexible tool so that it can be modified as per the stimulated

situations of the company.

Disadvantage:

This tool is not suitable at the time of practical implications as it is more time consuming.

Forecasting planning tools:

Forecasting tools us used by the firm to develop a framework for future occurrences and

happenings by considering previous as well as present adjustment in trends (Parker and

Fleischman, 2017). For profitable results from this tool an appropriate and relevant data are used

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

by the organisation from its internal as well as external resources. Management of Aston Martin

can utilise this tool for understanding of future trends which affects the company in future.

Advantage:

This tool aids firm managers to forecast for future by developing effective directions so

that they can accomplish their targets. As consumers wants are changing which allow Aston

Martin to invent creative designs cars and so on.

Disadvantage:

As forecasting is the performed on the basis of estimation so firm cannot acquire the

accurate as well as relevant results in all situations while using this tool.

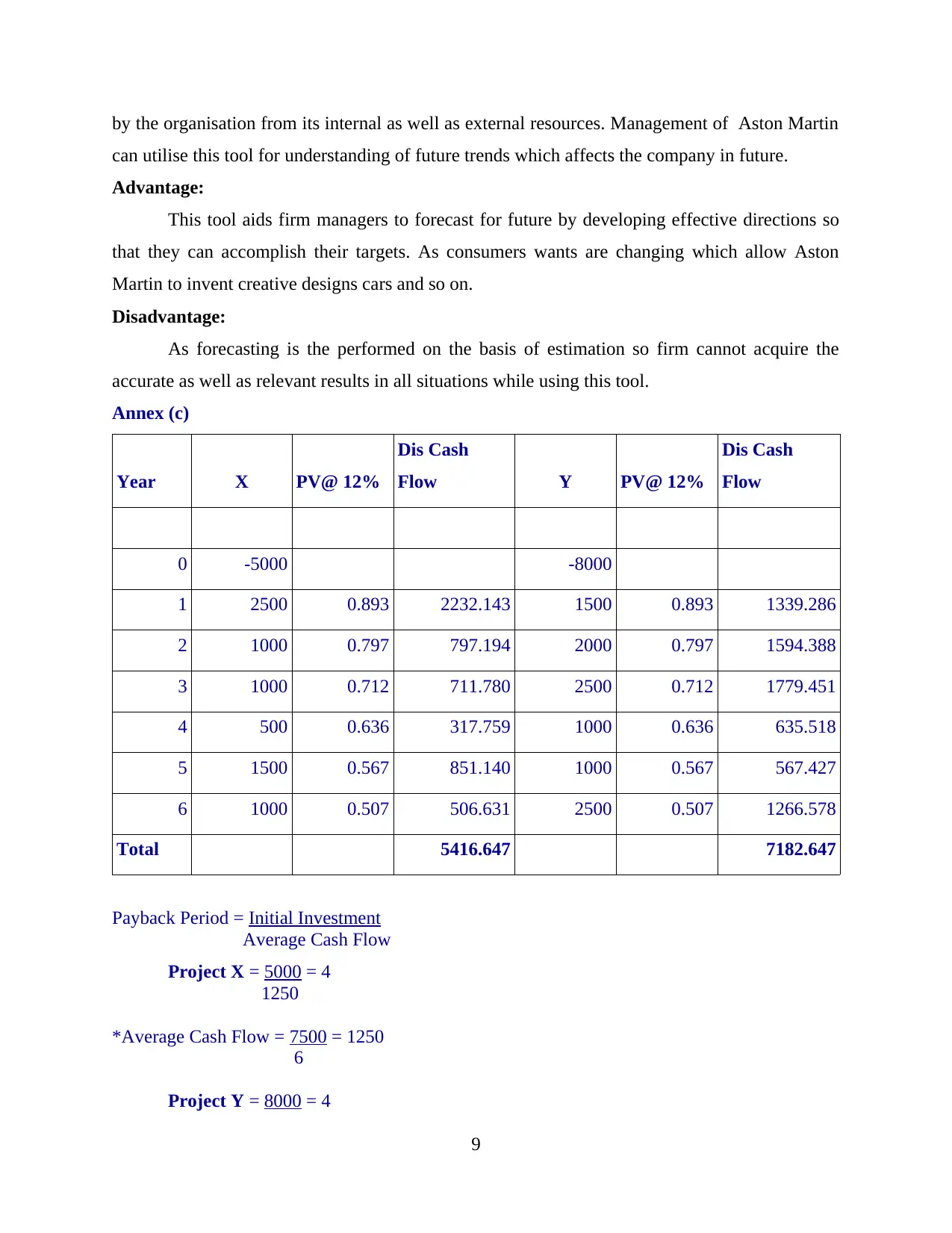

Annex (c)

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.780 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.140 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 5416.647 7182.647

Payback Period = Initial Investment

Average Cash Flow

Project X = 5000 = 4

1250

*Average Cash Flow = 7500 = 1250

6

Project Y = 8000 = 4

9

can utilise this tool for understanding of future trends which affects the company in future.

Advantage:

This tool aids firm managers to forecast for future by developing effective directions so

that they can accomplish their targets. As consumers wants are changing which allow Aston

Martin to invent creative designs cars and so on.

Disadvantage:

As forecasting is the performed on the basis of estimation so firm cannot acquire the

accurate as well as relevant results in all situations while using this tool.

Annex (c)

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.780 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.140 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 5416.647 7182.647

Payback Period = Initial Investment

Average Cash Flow

Project X = 5000 = 4

1250

*Average Cash Flow = 7500 = 1250

6

Project Y = 8000 = 4

9

1750

*Average Cash Flow = 10500 = 1750

6

NPV: -

Project X = Dis Cash Flow – Initial Investment

= 5416.647 – 5000

= £416.647

Project Y = Dis Cash Flow – Initial Investment

= 7182.647 – 8000

= - £817.353

M3. Use of different planning tools and their application for preparing and forecasting budget

After examining the different planning tool it is clear that this aids Aston Martin

management for maintaining process that is related to budget preparation and planning (Ruch

and Taylor, 2015). All tools gives a preparation of blue print framework to manage whole

functions that assists to determine the organisational growth as well as performance. Aston

Martin can apply this tool to identify the threats and opportunities. For effectualness of planning

process all these tools play essential role.

P5. Comparison of how organisations are adapting management accounting systems to respond

to financial problems

Financial problems is considered as a situation where money matters a lot (Soderstrom,

Soderstrom and Stewart 2017). It have been seen that various kinds of financial issues are

occurring in the firm that impact the whole organisational growth. So there are certain financial

problems which effects the sustainability as well as growth of Aston Martin. Financial problem

are mentioned below:

Funds mismanagement: Funds management is crucial for all companies different

strategies are formulated and approaches are used by to maintain financial system (Spraakman,

2015). In Aston Martin managers can not able to manage funds appropriately due to which this

financial problems occurs.

10

*Average Cash Flow = 10500 = 1750

6

NPV: -

Project X = Dis Cash Flow – Initial Investment

= 5416.647 – 5000

= £416.647

Project Y = Dis Cash Flow – Initial Investment

= 7182.647 – 8000

= - £817.353

M3. Use of different planning tools and their application for preparing and forecasting budget

After examining the different planning tool it is clear that this aids Aston Martin

management for maintaining process that is related to budget preparation and planning (Ruch

and Taylor, 2015). All tools gives a preparation of blue print framework to manage whole

functions that assists to determine the organisational growth as well as performance. Aston

Martin can apply this tool to identify the threats and opportunities. For effectualness of planning

process all these tools play essential role.

P5. Comparison of how organisations are adapting management accounting systems to respond

to financial problems

Financial problems is considered as a situation where money matters a lot (Soderstrom,

Soderstrom and Stewart 2017). It have been seen that various kinds of financial issues are

occurring in the firm that impact the whole organisational growth. So there are certain financial

problems which effects the sustainability as well as growth of Aston Martin. Financial problem

are mentioned below:

Funds mismanagement: Funds management is crucial for all companies different

strategies are formulated and approaches are used by to maintain financial system (Spraakman,

2015). In Aston Martin managers can not able to manage funds appropriately due to which this

financial problems occurs.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.