Management Accounting Report: Aston Martin Case Study Analysis

VerifiedAdded on 2020/12/09

|19

|4575

|168

Report

AI Summary

This report delves into the world of management accounting, focusing on its application within the context of Aston Martin. It begins by defining management accounting and its role in organizational decision-making, contrasting it with financial accounting. The report then explores various management accounting systems, including inventory management, price optimization, job costing, and cost accounting systems. It details the components and applications of each system, emphasizing their importance for internal business processes. Furthermore, the report examines different types of management accounting reports, such as budget reports, accounts receivable aging reports, performance reports, and cost managerial accounting reports, highlighting their significance in assessing financial performance and supporting strategic decisions. The report also discusses the benefits of management accounting systems and how planning tools aid in solving financial problems, contributing to an organization's sustainable success. Finally, the report uses Aston Martin as a case study throughout the analysis.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

PART A.......................................................................................................................................1

Different Types of management accounting system ..................................................................2

Management Accounting Reports ..............................................................................................4

Benefits of management accounting system and their application ............................................5

Management accounting system and management accounting reporting is integrated within

organisational processes..............................................................................................................6

PART B.......................................................................................................................................7

Annex (A)....................................................................................................................................7

Annex (B)....................................................................................................................................7

ACTIVITY 2....................................................................................................................................8

Part A:..............................................................................................................................................8

Advantages and disadvantages of different types of planning tools...........................................8

Budgetary Control:......................................................................................................................9

Part B:............................................................................................................................................13

A comparison of how organisations are adapting management accounting systems to respond

to financial problems.................................................................................................................13

An analysis of how in responding to financial problems, management accounting can lead

organisation to sustainable success...........................................................................................14

An evaluation of how planning tools for accounting help to solve problems and support

organisations with sustainable success......................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

PART A.......................................................................................................................................1

Different Types of management accounting system ..................................................................2

Management Accounting Reports ..............................................................................................4

Benefits of management accounting system and their application ............................................5

Management accounting system and management accounting reporting is integrated within

organisational processes..............................................................................................................6

PART B.......................................................................................................................................7

Annex (A)....................................................................................................................................7

Annex (B)....................................................................................................................................7

ACTIVITY 2....................................................................................................................................8

Part A:..............................................................................................................................................8

Advantages and disadvantages of different types of planning tools...........................................8

Budgetary Control:......................................................................................................................9

Part B:............................................................................................................................................13

A comparison of how organisations are adapting management accounting systems to respond

to financial problems.................................................................................................................13

An analysis of how in responding to financial problems, management accounting can lead

organisation to sustainable success...........................................................................................14

An evaluation of how planning tools for accounting help to solve problems and support

organisations with sustainable success......................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management Accounting is a process of develop management reports and accounts that

provide accurate and timely financial and statical information required by managers to make day

to day and short term decisions (Yazdifar and et.al., 2012). It is internal process of an

organisation to identifying, measuring, analysing, interpreting and communicating information

with manager regarding to organisational goals and objectives. On the basis of these information

top management take effective and efficient decision regarding to future growth and success. It is

also known as managerial accounting and cost accounting. Management accountants are looking

around the world which events happen related to business activities. They are considering which

technology and systems needed for business. The aim of the project to present role and function

of management accounts department by line manager. There is selected company Aston Martin,

which is British independent manufacturer of luxury sports cars and grand tourers. It was

established in 1931 by Lionel martin and Robert Bamford. In the present report consist of

different management accounting system which is applied on different systems, management

accounting reports for present performance of company. There is producing a portfolio to

calculate costs through different techniques of cost analysis. In addition for financial stability and

performance apply planning tools and solving financial problems. Apart from identify merits and

demerits of planning tools and compare with other company for apply management accounting

system.

ACTIVITY 1

PART A

Management Accounting

Management accounting includes the financial and accounting tasks for operate a

business as per requirement. It is a internal process which is conducted by accountants such as

monitor costs, sales, spending and budgets, conduct audits, identify past trends and predict future

needs and assist company leaders with financial decisions. It is different from financial

accounting because in managerial accounting financial reports are preparing for managers and

top management and in financial accounting accounts and reports are prepared to present

external and internal stakeholders (Takeda and Boyns, 2014).

Management Accounting System

1

Management Accounting is a process of develop management reports and accounts that

provide accurate and timely financial and statical information required by managers to make day

to day and short term decisions (Yazdifar and et.al., 2012). It is internal process of an

organisation to identifying, measuring, analysing, interpreting and communicating information

with manager regarding to organisational goals and objectives. On the basis of these information

top management take effective and efficient decision regarding to future growth and success. It is

also known as managerial accounting and cost accounting. Management accountants are looking

around the world which events happen related to business activities. They are considering which

technology and systems needed for business. The aim of the project to present role and function

of management accounts department by line manager. There is selected company Aston Martin,

which is British independent manufacturer of luxury sports cars and grand tourers. It was

established in 1931 by Lionel martin and Robert Bamford. In the present report consist of

different management accounting system which is applied on different systems, management

accounting reports for present performance of company. There is producing a portfolio to

calculate costs through different techniques of cost analysis. In addition for financial stability and

performance apply planning tools and solving financial problems. Apart from identify merits and

demerits of planning tools and compare with other company for apply management accounting

system.

ACTIVITY 1

PART A

Management Accounting

Management accounting includes the financial and accounting tasks for operate a

business as per requirement. It is a internal process which is conducted by accountants such as

monitor costs, sales, spending and budgets, conduct audits, identify past trends and predict future

needs and assist company leaders with financial decisions. It is different from financial

accounting because in managerial accounting financial reports are preparing for managers and

top management and in financial accounting accounts and reports are prepared to present

external and internal stakeholders (Takeda and Boyns, 2014).

Management Accounting System

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting system consists as the internal system that is used by business to

evaluate and measure its processes for the management of a company. It is focused on following

the costs associated with the production of goods and services in a business. The system can

provide appropriate information to management for provide help in decision making process

(McLean, McGovern and Davie, 2015) .

Different Types of management accounting system

There is mentioned different types of management accounting system which is used by

organisation, as follows -

Inventory management system -

Inventory management system tracks goods through the whole supply chain or the part of

it a business operates in. That covers everything from production to retail, every moment of each

stocks and parts, from warehouse to shipping. In addition, a business can observe all small

moving parts which is related to operations and it will allow to make better decisions and

investments. In the system work different inventory manager, they are focused on different parts

of the supply chain which is starting from ordering and ending in sales. There is wide variation in

scope, inventory management system also vary widely in cost. For this system used technology

because with the help of software monitoring and maintenance of stocked products in Aston

Martin. In inventory management includes assets of company, raw materials, supplies and

finished products. Hardware tools are used for read bar code labels, handled barcode scanners.

Price Optimization system -

Price optimization is the use of mathematical analysis which is used by company for

determine response of customers regarding to different prices for their products and services. The

system also used to measure the prices that the company determines will best meet its objectives

like maximizing operating profit (Bromiley and et.al, 2015) . It is the use of formal methods to

show structure of price that optimize a goal like profit and customer acquisition targets. Price

optimization is important component of overall price management which is important for

profitability. Now a days it has become increasingly important because sales of products after

that track price, it is created competitive market. In the context of Aston martin apply the system

for know difference prices of their cars according to customer interest.

Job Costing system -

2

evaluate and measure its processes for the management of a company. It is focused on following

the costs associated with the production of goods and services in a business. The system can

provide appropriate information to management for provide help in decision making process

(McLean, McGovern and Davie, 2015) .

Different Types of management accounting system

There is mentioned different types of management accounting system which is used by

organisation, as follows -

Inventory management system -

Inventory management system tracks goods through the whole supply chain or the part of

it a business operates in. That covers everything from production to retail, every moment of each

stocks and parts, from warehouse to shipping. In addition, a business can observe all small

moving parts which is related to operations and it will allow to make better decisions and

investments. In the system work different inventory manager, they are focused on different parts

of the supply chain which is starting from ordering and ending in sales. There is wide variation in

scope, inventory management system also vary widely in cost. For this system used technology

because with the help of software monitoring and maintenance of stocked products in Aston

Martin. In inventory management includes assets of company, raw materials, supplies and

finished products. Hardware tools are used for read bar code labels, handled barcode scanners.

Price Optimization system -

Price optimization is the use of mathematical analysis which is used by company for

determine response of customers regarding to different prices for their products and services. The

system also used to measure the prices that the company determines will best meet its objectives

like maximizing operating profit (Bromiley and et.al, 2015) . It is the use of formal methods to

show structure of price that optimize a goal like profit and customer acquisition targets. Price

optimization is important component of overall price management which is important for

profitability. Now a days it has become increasingly important because sales of products after

that track price, it is created competitive market. In the context of Aston martin apply the system

for know difference prices of their cars according to customer interest.

Job Costing system -

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A job costing system is the process of predication information about the costs which is

related to specific production or service job. All products costs are provided to a customer under

a contract because it is important to submit and it is shown where cost reimbursed. The

information used by customer to measure accuracy of company system, which should be able to

quote prices that allow for a reasonable profit. The information used for appoint invariable costs

to manufactured goods. A job costing system analysed three types information which is

important for company -

Direct Materials – The job costing system can track cost of materials which are used for

scrapped during the course of the job. When business is constructing line so they can

develop custom made machine and the cost sheet used in the construction for predict and

charged to the job (Malinić and Todorović, 2012).

Direct Labour – The job costing system must be track the cost of the labour used on a

job. It is directly related to job with a time card, time sheet and also with networked time

clock application on computer. The particular information automatically recorded

through internet in smart phone.

Overhead – The job costing system allotted overhead costs like depreciation, building

rent and production equipment. At the end of every accounting period the total amount in

each cost pool is assigned to the various open jobs which is based on allocation

methodology.

This term mostly used in manufacturing industry for allocate costs of individual

construction projects at a company. With the proper system to do job cost accounting the end

result is the ability to accurately report on profitability per project.

Cost accounting system -

Cost accounting is a method which aims to getting costs of a company of production after

assessing the input costs of each step of production as well as fixed costs such as depreciation of

capital equipment. It is a framework which is used companies to predict the cost of their products

for the analysis of profitability and also cost control, valuation of stock (Thomas, 2016). The

company Aston Martin can use two cost accounting system which is following as -

Job Order Costing – It is a cost accounting system that helps in evaluate manufacturing

costs of each job. It is important for company because the system related with production of

unique products and special orders.

3

related to specific production or service job. All products costs are provided to a customer under

a contract because it is important to submit and it is shown where cost reimbursed. The

information used by customer to measure accuracy of company system, which should be able to

quote prices that allow for a reasonable profit. The information used for appoint invariable costs

to manufactured goods. A job costing system analysed three types information which is

important for company -

Direct Materials – The job costing system can track cost of materials which are used for

scrapped during the course of the job. When business is constructing line so they can

develop custom made machine and the cost sheet used in the construction for predict and

charged to the job (Malinić and Todorović, 2012).

Direct Labour – The job costing system must be track the cost of the labour used on a

job. It is directly related to job with a time card, time sheet and also with networked time

clock application on computer. The particular information automatically recorded

through internet in smart phone.

Overhead – The job costing system allotted overhead costs like depreciation, building

rent and production equipment. At the end of every accounting period the total amount in

each cost pool is assigned to the various open jobs which is based on allocation

methodology.

This term mostly used in manufacturing industry for allocate costs of individual

construction projects at a company. With the proper system to do job cost accounting the end

result is the ability to accurately report on profitability per project.

Cost accounting system -

Cost accounting is a method which aims to getting costs of a company of production after

assessing the input costs of each step of production as well as fixed costs such as depreciation of

capital equipment. It is a framework which is used companies to predict the cost of their products

for the analysis of profitability and also cost control, valuation of stock (Thomas, 2016). The

company Aston Martin can use two cost accounting system which is following as -

Job Order Costing – It is a cost accounting system that helps in evaluate manufacturing

costs of each job. It is important for company because the system related with production of

unique products and special orders.

3

Process Costing – This system evaluate manufacturing cost of each process and it is

involved different types of departments and cost flow.

Management Accounting Reports

Accounting reports is a statement prepared to analyse the various aspects of business

accounting. system. It helps to display the financial stability of business at the end of a certain

period. It consists of information related to company's performance. All business transactions,

invoices, income statement, balance sheets etc are recorded in order to evaluate organisation

growth. Whether the company is large or small it is compulsion to develop accounting statement.

These helps provides base to financial statement (Grabner and Moers, 2013). Accuracy of these

reports is a key element if data entered in them is not accurate true picture of actual position of

business can not be estimated. Let's study different types of accounting reports in detail:-

Budget Reports- Budgets are set by the managers in order to keep control on

expenditure and estimation of profits. These are planned and prepared in advance to determine

how much money is required to perform certain activity. The size of budget differ according to

the size business. It helps in important decision making regarding cost cutting, how much of

negotiating is required with suppliers and vendors, and what more is needed for the achievement

of organisational goals. Managers can be guided about certain policies that needs to be

incorporated. Aston martin first correct errors if occurred any and then they estimate their

predictions by creating two columns each showing actual and budgeted figures. gives It's the

responsibility of employees to keep everything under set budget. The budget reports are

compared with previous to analyse company's performance.

Accounts receivables aging reports- These are the reports that are prepared when the

business depend too much on credit transactions. When the customer does does not make

payment in cash an invoice is generated as written verification which creates a duty for the

purchaser to pay due amount within the specified time period. It consist a list of customer

invoices, memos. Information about customers and their due payment can be identifies through

this. Date and amounts which customer has to pay is specified in columns (Boiral, 2016). There

are software available that few companies use to generate this data. Aston martin issue invoice

to all it's creditors consisting every single detail about items he purchased, on date he bought

goods, his name, address and other terms and conditions. It helps the customers in evaluation of

bad debts.

4

involved different types of departments and cost flow.

Management Accounting Reports

Accounting reports is a statement prepared to analyse the various aspects of business

accounting. system. It helps to display the financial stability of business at the end of a certain

period. It consists of information related to company's performance. All business transactions,

invoices, income statement, balance sheets etc are recorded in order to evaluate organisation

growth. Whether the company is large or small it is compulsion to develop accounting statement.

These helps provides base to financial statement (Grabner and Moers, 2013). Accuracy of these

reports is a key element if data entered in them is not accurate true picture of actual position of

business can not be estimated. Let's study different types of accounting reports in detail:-

Budget Reports- Budgets are set by the managers in order to keep control on

expenditure and estimation of profits. These are planned and prepared in advance to determine

how much money is required to perform certain activity. The size of budget differ according to

the size business. It helps in important decision making regarding cost cutting, how much of

negotiating is required with suppliers and vendors, and what more is needed for the achievement

of organisational goals. Managers can be guided about certain policies that needs to be

incorporated. Aston martin first correct errors if occurred any and then they estimate their

predictions by creating two columns each showing actual and budgeted figures. gives It's the

responsibility of employees to keep everything under set budget. The budget reports are

compared with previous to analyse company's performance.

Accounts receivables aging reports- These are the reports that are prepared when the

business depend too much on credit transactions. When the customer does does not make

payment in cash an invoice is generated as written verification which creates a duty for the

purchaser to pay due amount within the specified time period. It consist a list of customer

invoices, memos. Information about customers and their due payment can be identifies through

this. Date and amounts which customer has to pay is specified in columns (Boiral, 2016). There

are software available that few companies use to generate this data. Aston martin issue invoice

to all it's creditors consisting every single detail about items he purchased, on date he bought

goods, his name, address and other terms and conditions. It helps the customers in evaluation of

bad debts.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance reports- Such reports are created to analyse the overall performance level

of organisation including the employees working in it. Measuring how the work is being carrying

out is essential. Important decisions are taken about promotions of employees and strategies

needed for increasing the productivity of organisation. These reports helps in the identification of

defects and causes of lack of performance. Assessment of various alternatives to understand

advantages and disadvantages associated with them can be determined. Success ratio of project is

visible by preparing performance reports. Aston martin uses this report to take decisions

regarding continuation of projects and also to estimate reward that needs to be given an

employee based on his performance. Deep functioning of this company is assessed through this

report (Aksoylu and Aykan, 2013).

Cost managerial accounting report- Costs shows the expenditure made on running the

business. These are compared with revenue generated from incurring it. This report comprises

the detailed information about price and the amounts on which they are sold. Profits are

estimated with the help of this. It includes labour cost on hourly basis, overhead cost, direct cost,

indirect cost and inventory cost. Aston martin calculate the profits generated and the amount

incurred in the manufacturing of cars. These helps to give company true picture of production

processes and how company can reduce cost of cars to gain competitive advantage over it's

competitors.

Benefits of management accounting system and their application

Representing the financial position of business is main purpose of management

accounting system. Various benefits linked to this are as follows:-

Job costing system- Figures represents the cost occurred on producing and

manufacturing of products. It is essential to understand the such costs of organisation. Managers

are in stable position to take decisions about matters which are not aware of with the help of this

system. Aston martin uses this system to estimate the cost incurred on manufacturing the cars.

Aston martin gain knowledge about the elements which led to the profitability and growth of

company and also provides information about those which are not contributing positively

towards organisation. Such elements needs to be withdrawn from business (Kober,

Subraamanniam and Watson, 2012).

Price optimisation system- This system evaluates the behaviour of customers to

changing prices. It is used by the companies to determine the pricing structure. Mathematical

5

of organisation including the employees working in it. Measuring how the work is being carrying

out is essential. Important decisions are taken about promotions of employees and strategies

needed for increasing the productivity of organisation. These reports helps in the identification of

defects and causes of lack of performance. Assessment of various alternatives to understand

advantages and disadvantages associated with them can be determined. Success ratio of project is

visible by preparing performance reports. Aston martin uses this report to take decisions

regarding continuation of projects and also to estimate reward that needs to be given an

employee based on his performance. Deep functioning of this company is assessed through this

report (Aksoylu and Aykan, 2013).

Cost managerial accounting report- Costs shows the expenditure made on running the

business. These are compared with revenue generated from incurring it. This report comprises

the detailed information about price and the amounts on which they are sold. Profits are

estimated with the help of this. It includes labour cost on hourly basis, overhead cost, direct cost,

indirect cost and inventory cost. Aston martin calculate the profits generated and the amount

incurred in the manufacturing of cars. These helps to give company true picture of production

processes and how company can reduce cost of cars to gain competitive advantage over it's

competitors.

Benefits of management accounting system and their application

Representing the financial position of business is main purpose of management

accounting system. Various benefits linked to this are as follows:-

Job costing system- Figures represents the cost occurred on producing and

manufacturing of products. It is essential to understand the such costs of organisation. Managers

are in stable position to take decisions about matters which are not aware of with the help of this

system. Aston martin uses this system to estimate the cost incurred on manufacturing the cars.

Aston martin gain knowledge about the elements which led to the profitability and growth of

company and also provides information about those which are not contributing positively

towards organisation. Such elements needs to be withdrawn from business (Kober,

Subraamanniam and Watson, 2012).

Price optimisation system- This system evaluates the behaviour of customers to

changing prices. It is used by the companies to determine the pricing structure. Mathematical

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analysis to forecast response of potential buyers is main function of this system. Prices should

neither be too high nor too low. Aston martin uses this model to set prices of it's cars. It follows

premium pricing strategy as it's customers are of upper class (Yigitbasioglu and Velcu, 2012).

Inventory management system- This system is used to keep a record of stock

availability. Managing ,tracking and predicting the requirement of goods can be be maintained

by the managers with the help of this system. Aston martin company keeps a track of the location

of it's expensive cars their production and spare parts by effectively maintaining this system.

Cost accounting- Investments made by firm on different project and return on them can

be evaluated with the help of accounting management. This system helps to calculate the

profitability and growth of the organisation by successfully maintaining inventory valuation and

cost occurred on each stage of production. Aston martin uses this system for the benefits it

provides to the company (Van Dooren, Bouckaert and Halligan, 2015).

Management accounting system and management accounting reporting is integrated within

organisational processes

Budget Report – These types of report are helping in Aston martin process because with

the help of this report estimate future expenses and incomes so according to that prepare budget.

Upcoming risks are deducted from budget and create fund for financial problems.

Cost managerial accounting report – It will integrated with company because it shows

actual cost structure of company which is related to production. There is included different types

of cost to present actual value of each cars such as over head cost, direct cost and indirect cost.

Performance report – The performance report integrated with Aston martin to present

performance of individual and organisation. The report prepare on the basis of performance and

how many targets achieve by organisation. For appraise of employees the company has provided

reward system to employees like bonus, gift voucher etc.

Accounting receivable agin report – It will help to organisational process and presents

financial condition of company because in this report presents net cash in flow and out flow of

Aston Martin. On the basis of this report the company can take effective decision in the manner

of future growth (Grossi and Steccolini, 2014).

6

neither be too high nor too low. Aston martin uses this model to set prices of it's cars. It follows

premium pricing strategy as it's customers are of upper class (Yigitbasioglu and Velcu, 2012).

Inventory management system- This system is used to keep a record of stock

availability. Managing ,tracking and predicting the requirement of goods can be be maintained

by the managers with the help of this system. Aston martin company keeps a track of the location

of it's expensive cars their production and spare parts by effectively maintaining this system.

Cost accounting- Investments made by firm on different project and return on them can

be evaluated with the help of accounting management. This system helps to calculate the

profitability and growth of the organisation by successfully maintaining inventory valuation and

cost occurred on each stage of production. Aston martin uses this system for the benefits it

provides to the company (Van Dooren, Bouckaert and Halligan, 2015).

Management accounting system and management accounting reporting is integrated within

organisational processes

Budget Report – These types of report are helping in Aston martin process because with

the help of this report estimate future expenses and incomes so according to that prepare budget.

Upcoming risks are deducted from budget and create fund for financial problems.

Cost managerial accounting report – It will integrated with company because it shows

actual cost structure of company which is related to production. There is included different types

of cost to present actual value of each cars such as over head cost, direct cost and indirect cost.

Performance report – The performance report integrated with Aston martin to present

performance of individual and organisation. The report prepare on the basis of performance and

how many targets achieve by organisation. For appraise of employees the company has provided

reward system to employees like bonus, gift voucher etc.

Accounting receivable agin report – It will help to organisational process and presents

financial condition of company because in this report presents net cash in flow and out flow of

Aston Martin. On the basis of this report the company can take effective decision in the manner

of future growth (Grossi and Steccolini, 2014).

6

PART B

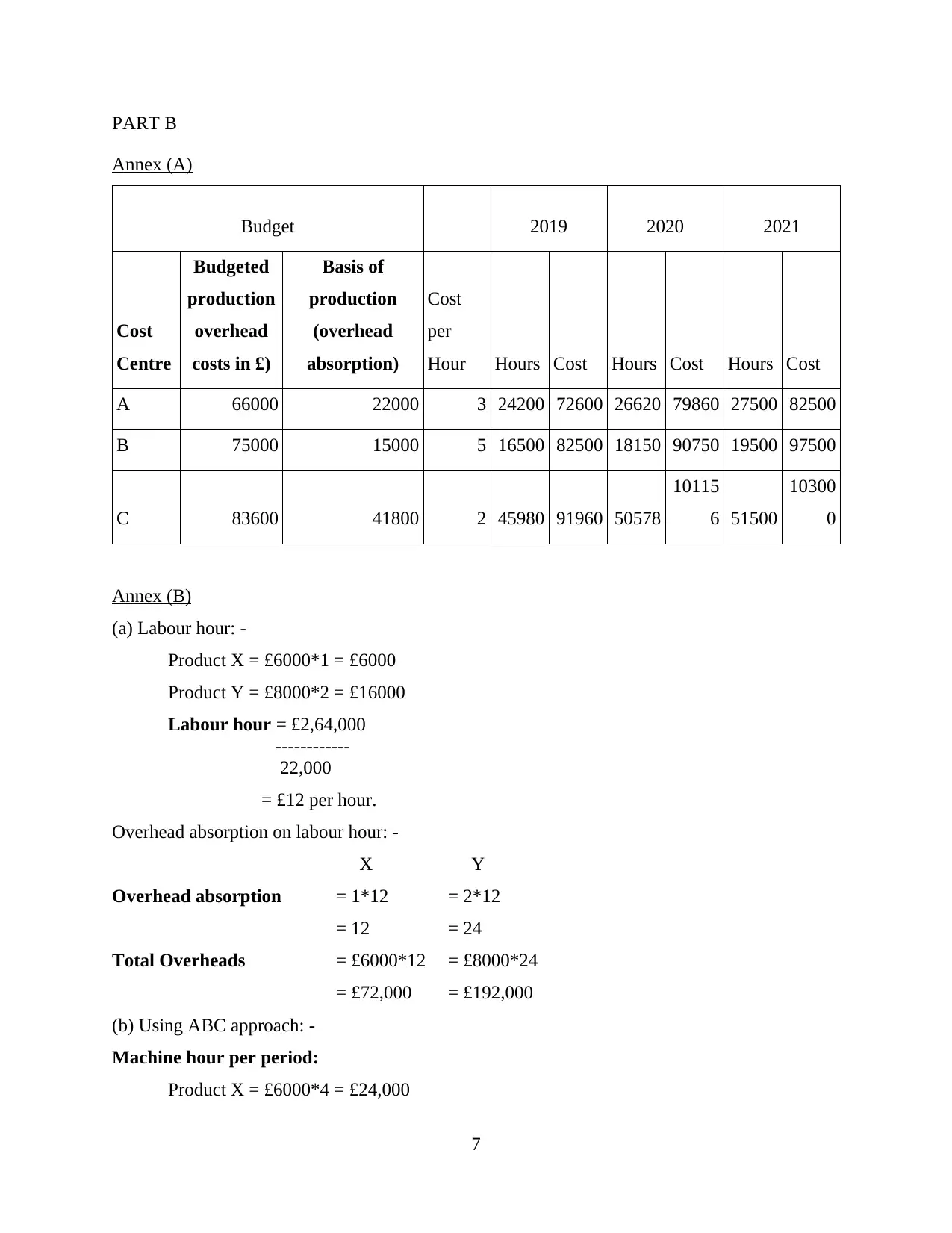

Annex (A)

Budget 2019 2020 2021

Cost

Centre

Budgeted

production

overhead

costs in £)

Basis of

production

(overhead

absorption)

Cost

per

Hour Hours Cost Hours Cost Hours Cost

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

7

Annex (A)

Budget 2019 2020 2021

Cost

Centre

Budgeted

production

overhead

costs in £)

Basis of

production

(overhead

absorption)

Cost

per

Hour Hours Cost Hours Cost Hours Cost

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

ACTIVITY 2

Part A:

Advantages and disadvantages of different types of planning tools

Budget:

It is a formal document which is usually based upon the expenses or incomes related to

future plan strategies or objectives. In other words, budget is basically used for planning and

performance measurement of specific purpose in accounting manner. It also involves in spending

for fixed assets, training of the employees, targeting and making bonus plan and control the

operations within the budget scenario (Ramljak and Rogošić, 2012). In addition to this, the main

use of budget is as a performance of baseline for the actual results of accounts. It can be prepared

by the electronic spreadsheet, business software which use to make more great structure and

8

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

ACTIVITY 2

Part A:

Advantages and disadvantages of different types of planning tools

Budget:

It is a formal document which is usually based upon the expenses or incomes related to

future plan strategies or objectives. In other words, budget is basically used for planning and

performance measurement of specific purpose in accounting manner. It also involves in spending

for fixed assets, training of the employees, targeting and making bonus plan and control the

operations within the budget scenario (Ramljak and Rogošić, 2012). In addition to this, the main

use of budget is as a performance of baseline for the actual results of accounts. It can be prepared

by the electronic spreadsheet, business software which use to make more great structure and

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

remove computational errors. In context of Aston Martin makes budget by electronic spreadsheet

because it is the very easiest way for company to achieve good result in a effective manner.

Budgetary Control:

Budgetary control is the process of analysing the different results with budgeted figures

for the future period and actual performance for evaluation variances in the industry. It also helps

in planning and co-ordination and also provide controlling method in the organization. In short it

is known as the end-result of the company. It also focuses on controlling cost which involves in

the preparation of budget , responsibilities for making budget list by achieving maximum profit

for the firm in as per business concern. In addition to Aston Martin, it uses many systems but in

order to control budget it uses budgetary reports which helps the company in making good

commodities and services in a effective manner. It also helps in controlling or planning all

selling product from the company. Therefore, it is very essential aspect for an organization in

order to save time and cost of the company (Goodman and et.al, 2013).

Zero Base Budget:

It identifies the method of budgeting where all expenses or incomes are analysed by a

new product. It also involves in many systems such as budget system or act like a strategic plan

for the future growth of the company. It also helps in company to create or make strategies

decisions for long term future goals as well as current year planning for an organisation. It also

describes the all scenario of budget or budgetary control.

Advantages:

Accuracy: it involves in creating or developing some changes in the previous year

budget. It makes every department in a good design and every items in this the cash flow or

computer has their separate operation cost in a effective manner.

Efficiency: It helps in providing of resources in order to make good look with actual

numbers in a systematic form.

Disadvantage:

Time consuming: It is a very time consuming process, where government funded entities

comes every year as against the budget plan.

Lack of Expertise: It describes every line item where every cost5 is very difficult that

requires a lot of training and managers.

9

because it is the very easiest way for company to achieve good result in a effective manner.

Budgetary Control:

Budgetary control is the process of analysing the different results with budgeted figures

for the future period and actual performance for evaluation variances in the industry. It also helps

in planning and co-ordination and also provide controlling method in the organization. In short it

is known as the end-result of the company. It also focuses on controlling cost which involves in

the preparation of budget , responsibilities for making budget list by achieving maximum profit

for the firm in as per business concern. In addition to Aston Martin, it uses many systems but in

order to control budget it uses budgetary reports which helps the company in making good

commodities and services in a effective manner. It also helps in controlling or planning all

selling product from the company. Therefore, it is very essential aspect for an organization in

order to save time and cost of the company (Goodman and et.al, 2013).

Zero Base Budget:

It identifies the method of budgeting where all expenses or incomes are analysed by a

new product. It also involves in many systems such as budget system or act like a strategic plan

for the future growth of the company. It also helps in company to create or make strategies

decisions for long term future goals as well as current year planning for an organisation. It also

describes the all scenario of budget or budgetary control.

Advantages:

Accuracy: it involves in creating or developing some changes in the previous year

budget. It makes every department in a good design and every items in this the cash flow or

computer has their separate operation cost in a effective manner.

Efficiency: It helps in providing of resources in order to make good look with actual

numbers in a systematic form.

Disadvantage:

Time consuming: It is a very time consuming process, where government funded entities

comes every year as against the budget plan.

Lack of Expertise: It describes every line item where every cost5 is very difficult that

requires a lot of training and managers.

9

High manpower requirement: it needs large number of employee in the organisation

and also need human resources which can make its easy (Sisaye, and Birnberg, 2012) .

In the context of Aston Martin, it is important to have lot of human resource3s for future

growth of their company in a effective way. It also follows method of zero based budgeting

which helps in maximise their strategic plan in a efficient manner.

Incremental Budget

An incremental budget is vital part of management accounting which is based on adding

incremental amounts to existing budget to arrive to new budget . Management of Aston martin

make assumptions that every department will continue its operations from the current level of

expenditure. It is also assumed that expenditures incurred in previous year will be the base for

current year. Incremental budget is simple but generally not recommended by professionals. This

budgeting is relates to slight or little changes in the existing budget (Padovani, Orelli and Young,

2014).

Advantages : Incremental budget help to immediately check impact of change, easy to

implement, suitable for fixed funding requirements, don't requires detailed analysis, shows the

true financial position of Aston martin and based on recent financial budget.

Disadvantages: Incremental budget limits Aston martin to do spending, lack of

innovation, disconnection from reality as budget is based on previous year budget and business

runs into conservative mode.

Rolling budget

The word Rolling means continuous. Rolling budget is incremental extension of the past

budget period completed. In this revised financial plans of Aston martin for the next

accounting period is used to replace the old budget from the budgeting system. Rolling budget is

also known as perpetual budget and rolling horizon budget. It is futuristic in nature and help

Aston martin to do long term financial planning. Rolling budget allows to reallocate funds from

the non performing segments to performing segments. Rolling budget are regularly updated

during the year to know about changes in Aston martin (Schaltegger and Zvezdov, 2015).

Advantages: Rolling budget prevents Aston martin from creation of debts, creation of

emergency and saving funds, covers the inefficiencies of budgeting, responsive to changes,

prevent Aston martin from generating negative cash flow, shows accurate image of business, and

views the budget as a guide.

10

and also need human resources which can make its easy (Sisaye, and Birnberg, 2012) .

In the context of Aston Martin, it is important to have lot of human resource3s for future

growth of their company in a effective way. It also follows method of zero based budgeting

which helps in maximise their strategic plan in a efficient manner.

Incremental Budget

An incremental budget is vital part of management accounting which is based on adding

incremental amounts to existing budget to arrive to new budget . Management of Aston martin

make assumptions that every department will continue its operations from the current level of

expenditure. It is also assumed that expenditures incurred in previous year will be the base for

current year. Incremental budget is simple but generally not recommended by professionals. This

budgeting is relates to slight or little changes in the existing budget (Padovani, Orelli and Young,

2014).

Advantages : Incremental budget help to immediately check impact of change, easy to

implement, suitable for fixed funding requirements, don't requires detailed analysis, shows the

true financial position of Aston martin and based on recent financial budget.

Disadvantages: Incremental budget limits Aston martin to do spending, lack of

innovation, disconnection from reality as budget is based on previous year budget and business

runs into conservative mode.

Rolling budget

The word Rolling means continuous. Rolling budget is incremental extension of the past

budget period completed. In this revised financial plans of Aston martin for the next

accounting period is used to replace the old budget from the budgeting system. Rolling budget is

also known as perpetual budget and rolling horizon budget. It is futuristic in nature and help

Aston martin to do long term financial planning. Rolling budget allows to reallocate funds from

the non performing segments to performing segments. Rolling budget are regularly updated

during the year to know about changes in Aston martin (Schaltegger and Zvezdov, 2015).

Advantages: Rolling budget prevents Aston martin from creation of debts, creation of

emergency and saving funds, covers the inefficiencies of budgeting, responsive to changes,

prevent Aston martin from generating negative cash flow, shows accurate image of business, and

views the budget as a guide.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.