Financial Analysis of AstraZeneca

VerifiedAdded on 2020/01/16

|21

|4018

|450

Report

AI Summary

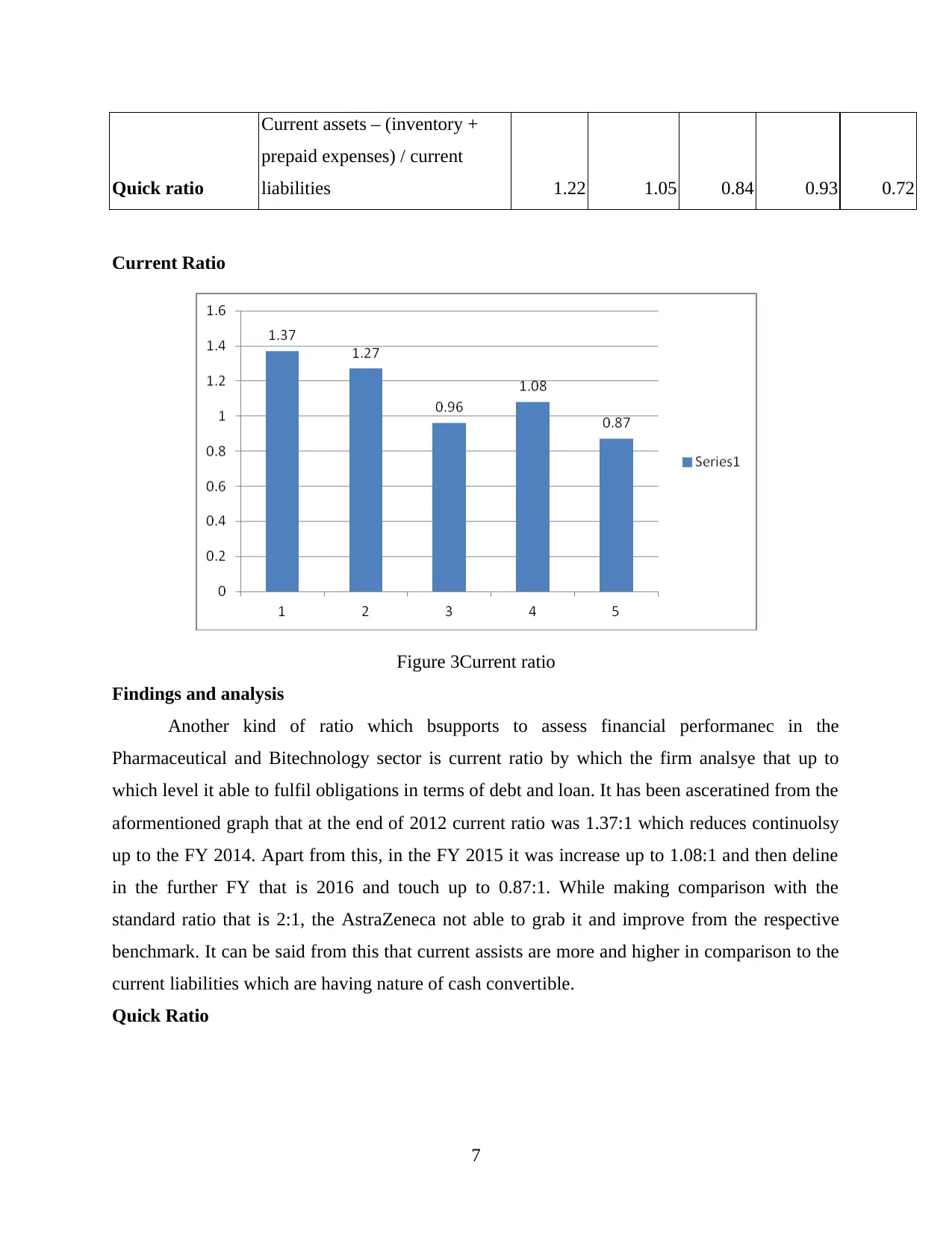

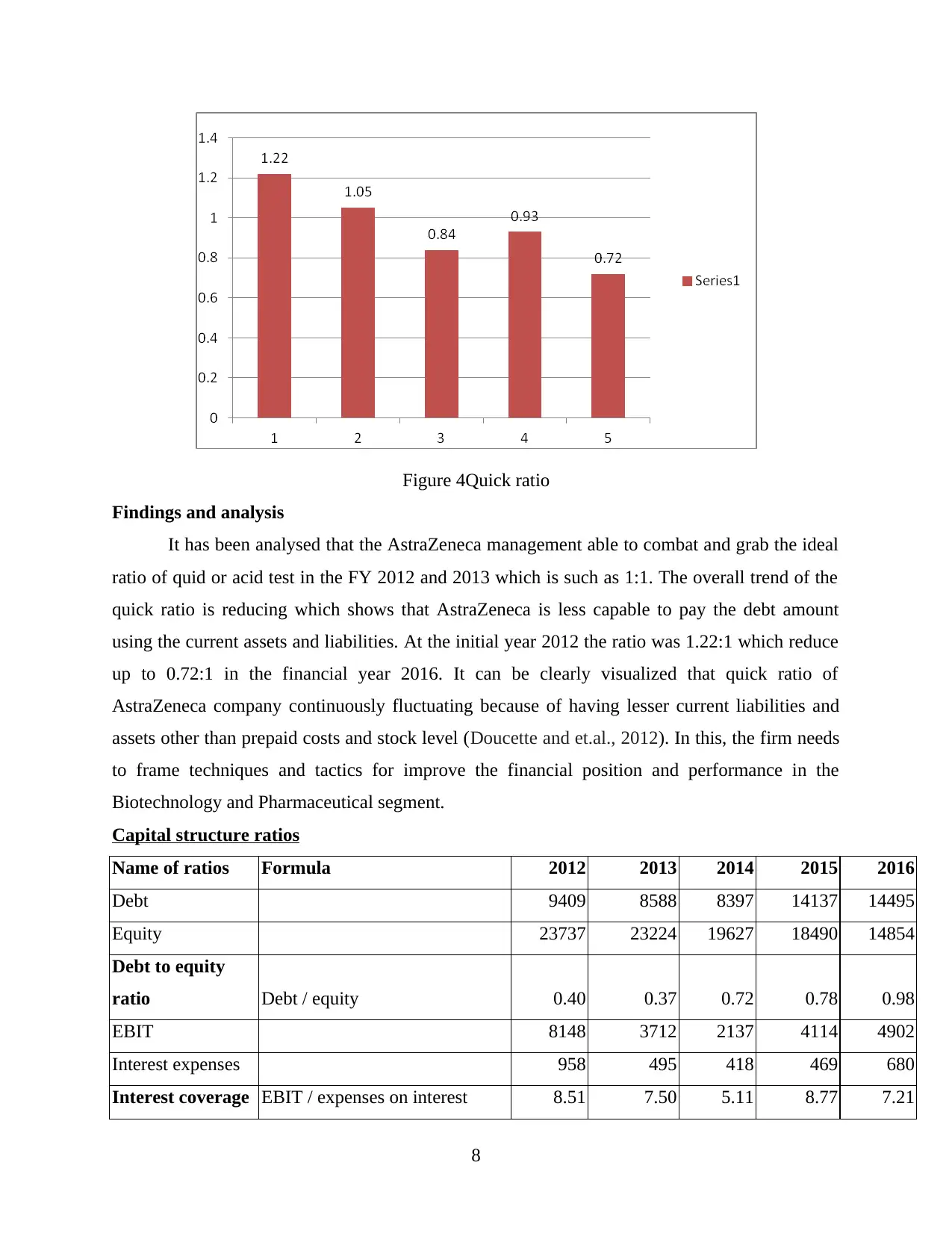

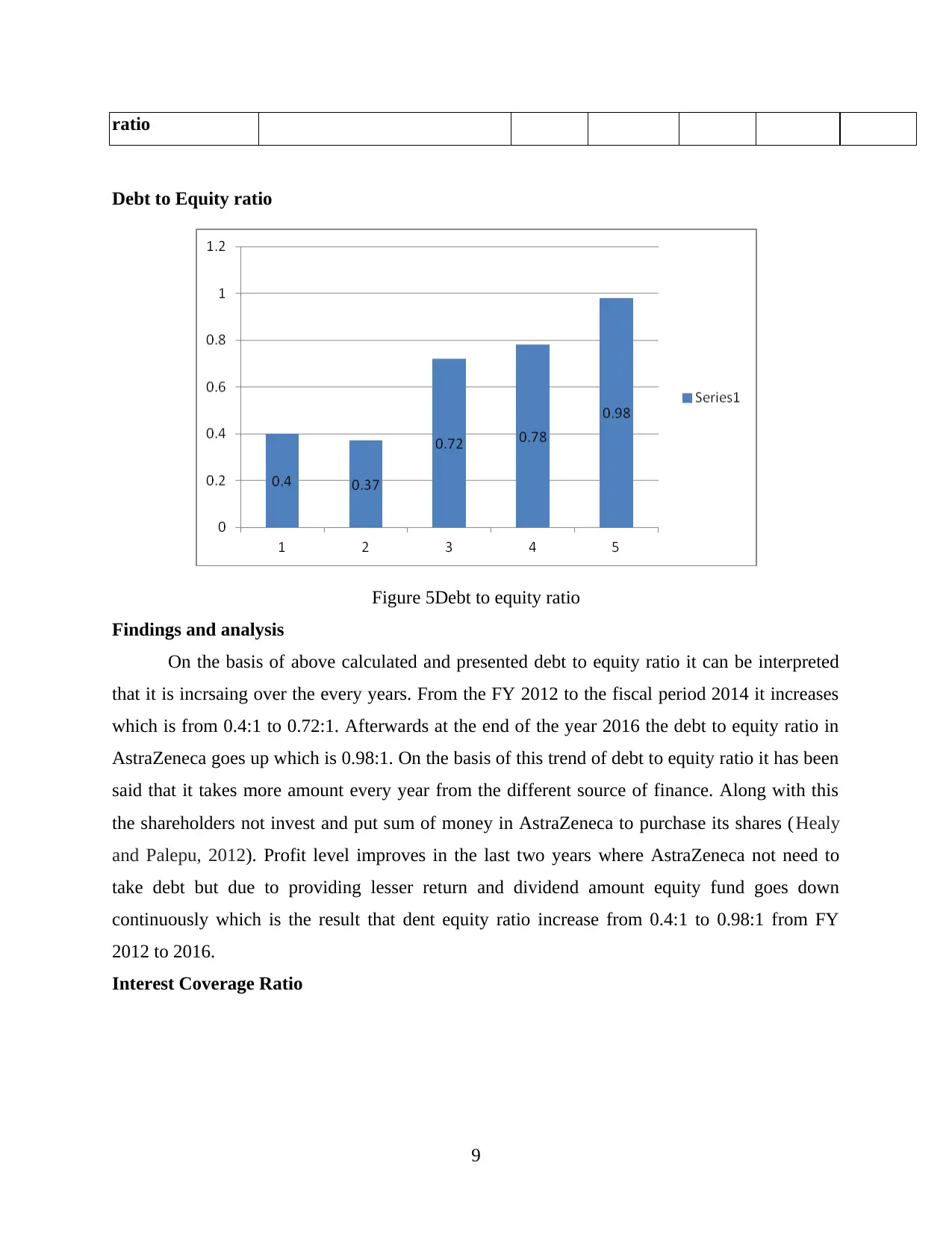

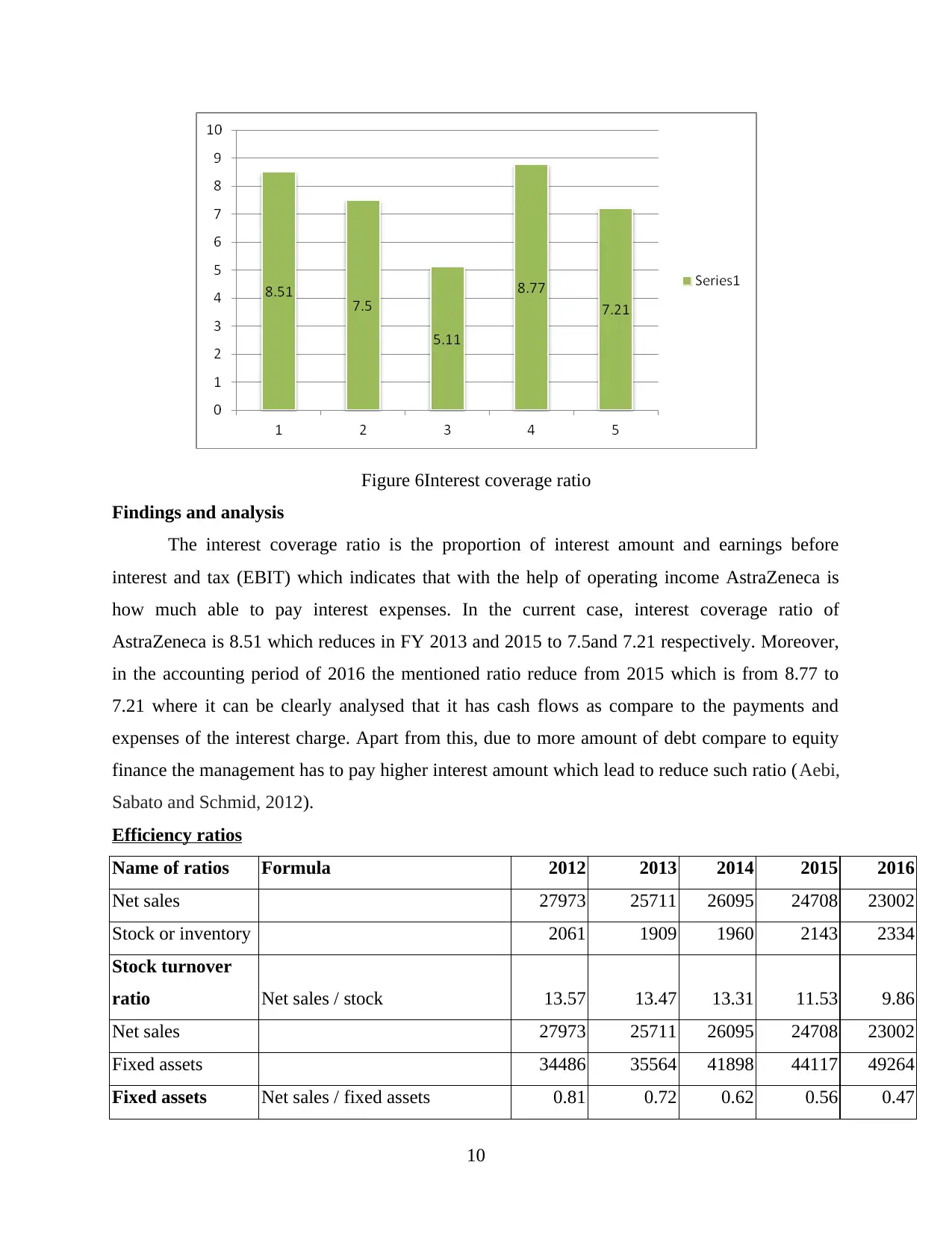

This report provides a comprehensive financial analysis of AstraZeneca PLC, a public limited company operating in the pharmaceutical and biotechnology industry. The analysis spans five accounting periods and utilizes various financial ratios to assess profitability, liquidity, efficiency, capital structure, and stock market performance. Specific ratios examined include gross profit ratio, operating profit ratio, net profit ratio, current ratio, quick ratio, debt-to-equity ratio, interest coverage ratio, stock turnover ratio, fixed assets turnover ratio, total assets turnover ratio, earnings per share, and return on equity. The report also discusses limitations of the analysis, such as reliance on quantitative data and the potential for variations in accounting practices. Finally, it offers suggestions for AstraZeneca to improve its financial performance, including enhancing marketing efforts, implementing cost-control strategies, increasing shareholder returns, and engaging in corporate social responsibility initiatives. The overall conclusion highlights AstraZeneca's relatively poor financial performance from 2012-2014, with improvement seen from 2014-2016, but still needing further strategic improvements.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.