Financial Analysis and Reporting on AstraZeneca: A Detailed Task

VerifiedAdded on 2023/06/15

|12

|3941

|485

Report

AI Summary

This report provides a financial analysis of AstraZeneca, a British-Swedish pharmaceutical company. It outlines the company's key features and objectives, emphasizing its commitment to delivering quality medicines and ethical standards. The report discusses the significance of financial statements—cash flow statement, income statement, and statement of financial position—in providing insights into the company's profitability, liquidity, and overall financial health. It calculates and interprets profitability and investment ratios for 2019 and 2020, revealing improved performance and growth. The analysis anticipates future business performance based on past and current financial positions and also examines the pros and cons of historical cost accounting. This report highlights AstraZeneca's financial strategies and their impacts on stakeholders and the company's market position.

Financial Analysis and

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

TASK...............................................................................................................................................3

(i) Key features and Key objectives of AstraZeneca-............................................................3

(ii) Significance of statement of cash flow, statement of financial position and income

statement as part of the financial information:.......................................................................4

(iii) Calculation of the profitability and investment ratios of Astra Zeneca:.........................6

(iv) Anticipation of the future performance of business on the basis of its past and current

position...................................................................................................................................8

(v) Pros and cons of historical cost accounting......................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

TASK...............................................................................................................................................3

(i) Key features and Key objectives of AstraZeneca-............................................................3

(ii) Significance of statement of cash flow, statement of financial position and income

statement as part of the financial information:.......................................................................4

(iii) Calculation of the profitability and investment ratios of Astra Zeneca:.........................6

(iv) Anticipation of the future performance of business on the basis of its past and current

position...................................................................................................................................8

(v) Pros and cons of historical cost accounting......................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial reporting and analysis means to calculates its financial health by collecting related

data and information by preparing budgetary accounts, fund flow statements, balance sheet etc.

for knowing where a business stands in the market. It also helps to know about creditability,

soundness of business, carrying out of operations, to know about future plans of the organisation

and how the plans can be carried out. It is helpful for the comparison of present with past

performances, to keep useful data for future as well, have proof regarding any dispute if arises, it

keeps the data relevant as well (Vicari, A., 2021). This report discusses about AstraZeneca

company which deals in pharmaceutical & biotechnology and is counted among one of the

companies which came forward to become a helping hand at the time of pandemic. Further it

states about the objectives and background of the company. Along with the discussion

importance of financial statements in context with the users of accounting information.

Moreover, the financial performance of the organisation has been evaluated by the help of

productivity and investment ratios. Also the estimated future performance of the business has

been analysed in relation to the current and past fiscal information of the firm. At the end pros

and cons of historical cost accounting is discussed.

TASK

(i) Key features and Key objectives of AstraZeneca-

AstraZeneca is a British-Swedish pharmaceutical product company. It is established in the

year 1999 by merging two another companies named Swedish Astra AB and British Zeneca

group (Dong, Liao, and Zhang 2018) It mainly deals in products for diseases such as

cardiovascular, oncology, neuroscience, gastrointestinal and inflammation. It's headquarter are

situated at Cambridge Biomedical campus in Cambridge, England. It believes in delivering best

quality medicines to their buyers so that they can cure billions of people. Creating impact on the

minds of people by not only delivering their product but also work for fulfilling ethical and

moral standards of the society. It provides a friendly working environment by providing them

with mental health care as well as flexible hours of working to reduce fatigue and stress among

its personnel. It focuses on unity in diversity by employing persons from different cultures

because integrating minds and views of various areas helps to create an innovative product. It

Financial reporting and analysis means to calculates its financial health by collecting related

data and information by preparing budgetary accounts, fund flow statements, balance sheet etc.

for knowing where a business stands in the market. It also helps to know about creditability,

soundness of business, carrying out of operations, to know about future plans of the organisation

and how the plans can be carried out. It is helpful for the comparison of present with past

performances, to keep useful data for future as well, have proof regarding any dispute if arises, it

keeps the data relevant as well (Vicari, A., 2021). This report discusses about AstraZeneca

company which deals in pharmaceutical & biotechnology and is counted among one of the

companies which came forward to become a helping hand at the time of pandemic. Further it

states about the objectives and background of the company. Along with the discussion

importance of financial statements in context with the users of accounting information.

Moreover, the financial performance of the organisation has been evaluated by the help of

productivity and investment ratios. Also the estimated future performance of the business has

been analysed in relation to the current and past fiscal information of the firm. At the end pros

and cons of historical cost accounting is discussed.

TASK

(i) Key features and Key objectives of AstraZeneca-

AstraZeneca is a British-Swedish pharmaceutical product company. It is established in the

year 1999 by merging two another companies named Swedish Astra AB and British Zeneca

group (Dong, Liao, and Zhang 2018) It mainly deals in products for diseases such as

cardiovascular, oncology, neuroscience, gastrointestinal and inflammation. It's headquarter are

situated at Cambridge Biomedical campus in Cambridge, England. It believes in delivering best

quality medicines to their buyers so that they can cure billions of people. Creating impact on the

minds of people by not only delivering their product but also work for fulfilling ethical and

moral standards of the society. It provides a friendly working environment by providing them

with mental health care as well as flexible hours of working to reduce fatigue and stress among

its personnel. It focuses on unity in diversity by employing persons from different cultures

because integrating minds and views of various areas helps to create an innovative product. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

main objectives is to work on the area of oncology, due to rise in covid spotting cancer became

difficult and hidden. They are working on therapies which are cell based to cure cancer. It joins

hands with the Haya a leading solution for oncology, working on the education and motivation of

patients to win this devastating disease (Ji and Zhang, 2019) They are investing huge amount in

achieving net zero carbon emission across the globe which is possible by using chemicals that

did not harm the environment. It welcomes all the ideas and have a unique research and

development which works to transform impossible thoughts into reality. They are using high

powered technology through which they are able to attain their societal and dynamic targets. In

the time of pandemic, it contributes in vaccine development as well as safeguarding the society

by delivering superior services to make this planet healthy and safe.

(ii) Significance of statement of cash flow, statement of financial position and income statement

as part of the financial information:

Financial statements are the collection of financial information about its profitability, liquidity

and its turnover in a particular financial year. These statements also get verified by government

auditors and stakeholders of an enterprise to know the accuracy of the same.

Financial statements are the key tools to know about its position to its external users. Importance

of financial information with respect to its users can be analysed as given below-

1.Cash flow statement-This statement is used to analyse the liquidity position of an enterprise

which helps to run the daily operations of an organisation in a smooth way. It tells about the cash

and cash equivalents such as bank overdraft available in an institution (Oussii and Taktak, 2018)

CFS supplements profit statement and statement of financial position. It includes cash flow

from operating, investing and financing activities. Operating activities includes adjustment of

current assets and liabilities and income related to daily activities of a business. Investing

comprises purchase and sale of fixed or non-current assets. Activities included in financing are

redemption and issue of share capital, debentures and other long term loans. It can be calculated

by using two ways: direct method and indirect method. Persons who wants to invest, inspect or

know about the financial status of an enterprise can easily get to know about the same by going

through it. External users of AstraZeneca, get acknowledged about the liquidity and cash inflows

and outflows of the respective company with the help of CFS.

difficult and hidden. They are working on therapies which are cell based to cure cancer. It joins

hands with the Haya a leading solution for oncology, working on the education and motivation of

patients to win this devastating disease (Ji and Zhang, 2019) They are investing huge amount in

achieving net zero carbon emission across the globe which is possible by using chemicals that

did not harm the environment. It welcomes all the ideas and have a unique research and

development which works to transform impossible thoughts into reality. They are using high

powered technology through which they are able to attain their societal and dynamic targets. In

the time of pandemic, it contributes in vaccine development as well as safeguarding the society

by delivering superior services to make this planet healthy and safe.

(ii) Significance of statement of cash flow, statement of financial position and income statement

as part of the financial information:

Financial statements are the collection of financial information about its profitability, liquidity

and its turnover in a particular financial year. These statements also get verified by government

auditors and stakeholders of an enterprise to know the accuracy of the same.

Financial statements are the key tools to know about its position to its external users. Importance

of financial information with respect to its users can be analysed as given below-

1.Cash flow statement-This statement is used to analyse the liquidity position of an enterprise

which helps to run the daily operations of an organisation in a smooth way. It tells about the cash

and cash equivalents such as bank overdraft available in an institution (Oussii and Taktak, 2018)

CFS supplements profit statement and statement of financial position. It includes cash flow

from operating, investing and financing activities. Operating activities includes adjustment of

current assets and liabilities and income related to daily activities of a business. Investing

comprises purchase and sale of fixed or non-current assets. Activities included in financing are

redemption and issue of share capital, debentures and other long term loans. It can be calculated

by using two ways: direct method and indirect method. Persons who wants to invest, inspect or

know about the financial status of an enterprise can easily get to know about the same by going

through it. External users of AstraZeneca, get acknowledged about the liquidity and cash inflows

and outflows of the respective company with the help of CFS.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.Income statement- A profit and loss statement signifies about the profit or loss in an

accounting year. It shows income on the credit side and expenditure on the debit side. Income

includes rent received, commission received, interest on drawing and also takes gross profit from

the trading account. Expenses include office and administration, marketing and financial

expenses. This is prepared to calculate the net profit of an organisation which assist in making

various decisions regarding future outcomes of an organisation. It also uses the application of

various accounting principles and conventions such as revenue recognition and accrual principle.

Usually there two methods of preparing income statement either cash or accrual system

(Venturelli and et.al., 2018) Net income can be obtained by subtracting net expenses from net

income of a specific period. For computing ratios, profitability ratios can be calculated by using

income statement of an enterprise. In short, profit and loss takes a snapshot of all the income,

expenditure and profitability. Users such as stakeholders, government, investing agencies get to

know about the financial health of AstraZeneca by which they recognize the gains and losses of

this pharmaceutical company.

3.Statement of financial Position-It is also called balance sheet which takes into consideration

all the assets and liabilities of a firm. Section of assets includes all the current and fixed assets.

(Wei and et.al., 2019) Current assets includes sundry debtors, bill receivable, prepaid expenses

and inventory etc. whereas fixed assets involve land and building, fixtures and machinery etc.

Liabilities entail both current and non-current. Current are those which repaid in a year but non-

current are those which are not paid in 12 months and remain for a long term. Every company

publishes its balance sheet either quarterly or yearly in its annual report. It owns and owes can be

evaluated from the statement of financial position. It is also used to interpret the ratios which

shows comparative analysis of two accounting years. Activity or turnover rations, liquidity ratios

are calculated from the balance sheet. If an organisation need to merger and acquire any another

company so it will firstly inspect the assets, liabilities, equity of the specific concern. It helps to

know investors, suppliers, creditors about the sources of capital and its cost of procuring it.

(Parker and Burke, 2018). Equation of balance sheet (assets=liabilities + capital) it prepares the

base for double entry system of accounting. External parties of AstraZeneca benefited by going

through the balance sheet because it reveals the true position of it.

accounting year. It shows income on the credit side and expenditure on the debit side. Income

includes rent received, commission received, interest on drawing and also takes gross profit from

the trading account. Expenses include office and administration, marketing and financial

expenses. This is prepared to calculate the net profit of an organisation which assist in making

various decisions regarding future outcomes of an organisation. It also uses the application of

various accounting principles and conventions such as revenue recognition and accrual principle.

Usually there two methods of preparing income statement either cash or accrual system

(Venturelli and et.al., 2018) Net income can be obtained by subtracting net expenses from net

income of a specific period. For computing ratios, profitability ratios can be calculated by using

income statement of an enterprise. In short, profit and loss takes a snapshot of all the income,

expenditure and profitability. Users such as stakeholders, government, investing agencies get to

know about the financial health of AstraZeneca by which they recognize the gains and losses of

this pharmaceutical company.

3.Statement of financial Position-It is also called balance sheet which takes into consideration

all the assets and liabilities of a firm. Section of assets includes all the current and fixed assets.

(Wei and et.al., 2019) Current assets includes sundry debtors, bill receivable, prepaid expenses

and inventory etc. whereas fixed assets involve land and building, fixtures and machinery etc.

Liabilities entail both current and non-current. Current are those which repaid in a year but non-

current are those which are not paid in 12 months and remain for a long term. Every company

publishes its balance sheet either quarterly or yearly in its annual report. It owns and owes can be

evaluated from the statement of financial position. It is also used to interpret the ratios which

shows comparative analysis of two accounting years. Activity or turnover rations, liquidity ratios

are calculated from the balance sheet. If an organisation need to merger and acquire any another

company so it will firstly inspect the assets, liabilities, equity of the specific concern. It helps to

know investors, suppliers, creditors about the sources of capital and its cost of procuring it.

(Parker and Burke, 2018). Equation of balance sheet (assets=liabilities + capital) it prepares the

base for double entry system of accounting. External parties of AstraZeneca benefited by going

through the balance sheet because it reveals the true position of it.

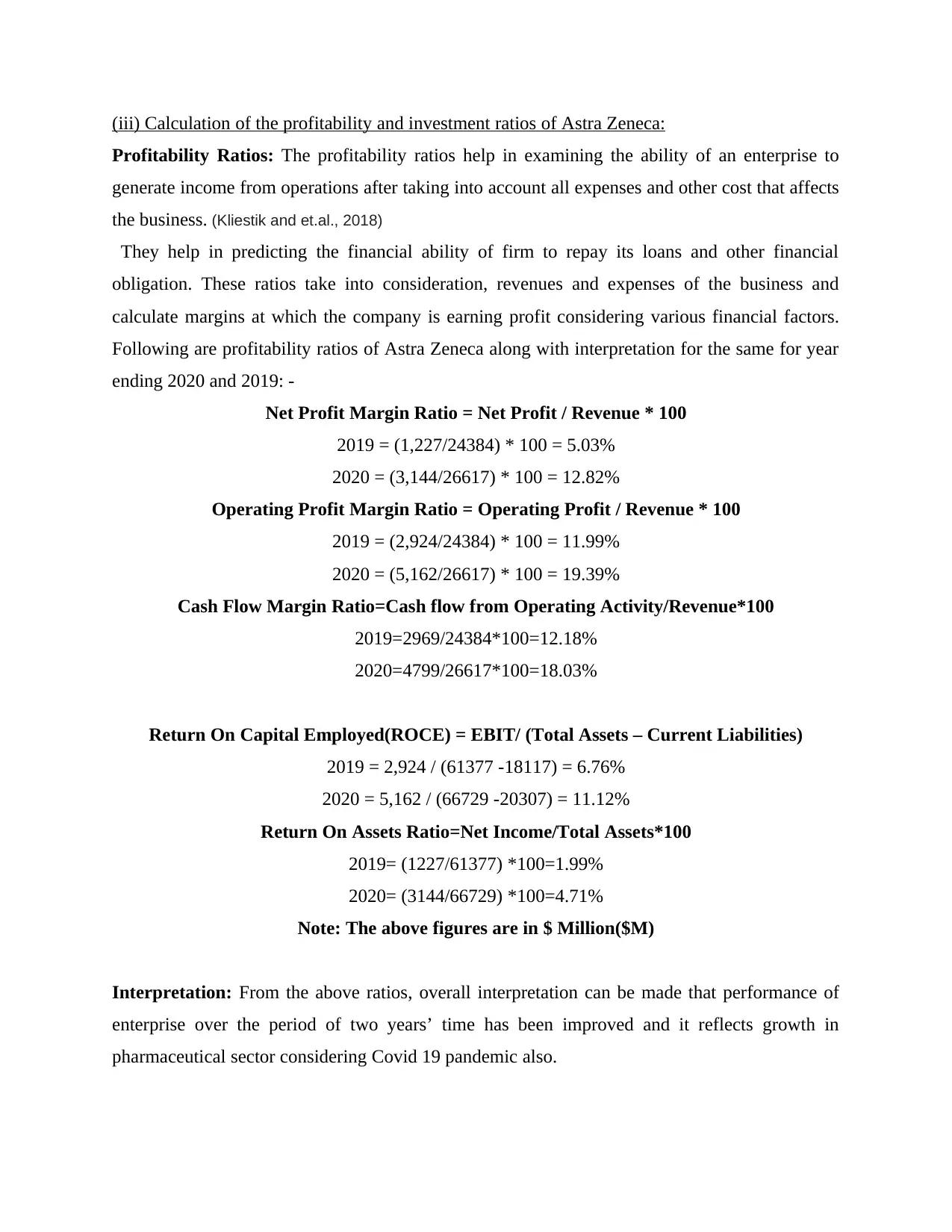

(iii) Calculation of the profitability and investment ratios of Astra Zeneca:

Profitability Ratios: The profitability ratios help in examining the ability of an enterprise to

generate income from operations after taking into account all expenses and other cost that affects

the business. (Kliestik and et.al., 2018)

They help in predicting the financial ability of firm to repay its loans and other financial

obligation. These ratios take into consideration, revenues and expenses of the business and

calculate margins at which the company is earning profit considering various financial factors.

Following are profitability ratios of Astra Zeneca along with interpretation for the same for year

ending 2020 and 2019: -

Net Profit Margin Ratio = Net Profit / Revenue * 100

2019 = (1,227/24384) * 100 = 5.03%

2020 = (3,144/26617) * 100 = 12.82%

Operating Profit Margin Ratio = Operating Profit / Revenue * 100

2019 = (2,924/24384) * 100 = 11.99%

2020 = (5,162/26617) * 100 = 19.39%

Cash Flow Margin Ratio=Cash flow from Operating Activity/Revenue*100

2019=2969/24384*100=12.18%

2020=4799/26617*100=18.03%

Return On Capital Employed(ROCE) = EBIT/ (Total Assets – Current Liabilities)

2019 = 2,924 / (61377 -18117) = 6.76%

2020 = 5,162 / (66729 -20307) = 11.12%

Return On Assets Ratio=Net Income/Total Assets*100

2019= (1227/61377) *100=1.99%

2020= (3144/66729) *100=4.71%

Note: The above figures are in $ Million($M)

Interpretation: From the above ratios, overall interpretation can be made that performance of

enterprise over the period of two years’ time has been improved and it reflects growth in

pharmaceutical sector considering Covid 19 pandemic also.

Profitability Ratios: The profitability ratios help in examining the ability of an enterprise to

generate income from operations after taking into account all expenses and other cost that affects

the business. (Kliestik and et.al., 2018)

They help in predicting the financial ability of firm to repay its loans and other financial

obligation. These ratios take into consideration, revenues and expenses of the business and

calculate margins at which the company is earning profit considering various financial factors.

Following are profitability ratios of Astra Zeneca along with interpretation for the same for year

ending 2020 and 2019: -

Net Profit Margin Ratio = Net Profit / Revenue * 100

2019 = (1,227/24384) * 100 = 5.03%

2020 = (3,144/26617) * 100 = 12.82%

Operating Profit Margin Ratio = Operating Profit / Revenue * 100

2019 = (2,924/24384) * 100 = 11.99%

2020 = (5,162/26617) * 100 = 19.39%

Cash Flow Margin Ratio=Cash flow from Operating Activity/Revenue*100

2019=2969/24384*100=12.18%

2020=4799/26617*100=18.03%

Return On Capital Employed(ROCE) = EBIT/ (Total Assets – Current Liabilities)

2019 = 2,924 / (61377 -18117) = 6.76%

2020 = 5,162 / (66729 -20307) = 11.12%

Return On Assets Ratio=Net Income/Total Assets*100

2019= (1227/61377) *100=1.99%

2020= (3144/66729) *100=4.71%

Note: The above figures are in $ Million($M)

Interpretation: From the above ratios, overall interpretation can be made that performance of

enterprise over the period of two years’ time has been improved and it reflects growth in

pharmaceutical sector considering Covid 19 pandemic also.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Net Profit Margin Ratio: This ratio shows how much profit is generated by organisation

per 1$ of sales. By comparing above figure’s it can be interpreted that Astra Zeneca Net

Profit Margin has been increased from 2019 to 2020 by 7.79%(12.82-5.03) which reflects

that on 1$ of sales they are making profit higher than 7.79% as compare to last years.

Further increase in ratio also indicates that Astra Zeneca is effectively controlling its cost

by selling their products at higher prices as compare to cost.

2. Operating Profit Margin Ratio: This ratio signifies that how much profit an enterprise

would generate after payment of variable cost of production such as raw material cost,

wages etc. The above ratio indicates operating profit of Astra Zeneca has increased by

7.38% in 2020 compare to 2019 due to increase in operating profits by 2238 $M by way

of Reduction in R&D cost and increase in revenues by 2238 $M.

3. Cash Flow Margin Ratio: It indicates that how effectively the firm converts their sales

into cash. There is significant increase in Astra Zeneca’s ratio in 2020 that is 18.03% as

compare to 2019 that is 12.18%. It indicates that Astra Zeneca is able to meet out its short

term liabilities and working capital requirements. Further it indicates that Payment to

suppliers and other creditor has been made on timely basis.

4. Return On Capital Employed: This ratio shows how much amount of profit the

organisation is earning for every $ of capital employed. From the above analysis in can

be interpreted that Astra Zeneca is generating higher profits as compare to capital they

have invested. Further they are earning higher profits for their stakeholders in year 2020

as compare to 2019. It implies that they are meeting shareholder’s expectation which

results in increase in price of share of Astra Zeneca in market.

5. Return On Total Assets Ratio: This ratio implies that how effectively an entity is utilising

its assets for generating profit. On the basis of above ratio, it can be interpreted that Astra

Zeneca is effectively utilising their assets in year 2020 as compare to previous year

because their net income is twice that is 3144$M as compare to year 2019 which implies

that assets are being used to fulfil the objectives of entity only.

Investment Ratios: The investment ratios highlights how much business is earning on their

investment and what return the firm is able to generate for their stakeholders who have invested

in form of capital. (Dinçer and Yüksel, 2018)

per 1$ of sales. By comparing above figure’s it can be interpreted that Astra Zeneca Net

Profit Margin has been increased from 2019 to 2020 by 7.79%(12.82-5.03) which reflects

that on 1$ of sales they are making profit higher than 7.79% as compare to last years.

Further increase in ratio also indicates that Astra Zeneca is effectively controlling its cost

by selling their products at higher prices as compare to cost.

2. Operating Profit Margin Ratio: This ratio signifies that how much profit an enterprise

would generate after payment of variable cost of production such as raw material cost,

wages etc. The above ratio indicates operating profit of Astra Zeneca has increased by

7.38% in 2020 compare to 2019 due to increase in operating profits by 2238 $M by way

of Reduction in R&D cost and increase in revenues by 2238 $M.

3. Cash Flow Margin Ratio: It indicates that how effectively the firm converts their sales

into cash. There is significant increase in Astra Zeneca’s ratio in 2020 that is 18.03% as

compare to 2019 that is 12.18%. It indicates that Astra Zeneca is able to meet out its short

term liabilities and working capital requirements. Further it indicates that Payment to

suppliers and other creditor has been made on timely basis.

4. Return On Capital Employed: This ratio shows how much amount of profit the

organisation is earning for every $ of capital employed. From the above analysis in can

be interpreted that Astra Zeneca is generating higher profits as compare to capital they

have invested. Further they are earning higher profits for their stakeholders in year 2020

as compare to 2019. It implies that they are meeting shareholder’s expectation which

results in increase in price of share of Astra Zeneca in market.

5. Return On Total Assets Ratio: This ratio implies that how effectively an entity is utilising

its assets for generating profit. On the basis of above ratio, it can be interpreted that Astra

Zeneca is effectively utilising their assets in year 2020 as compare to previous year

because their net income is twice that is 3144$M as compare to year 2019 which implies

that assets are being used to fulfil the objectives of entity only.

Investment Ratios: The investment ratios highlights how much business is earning on their

investment and what return the firm is able to generate for their stakeholders who have invested

in form of capital. (Dinçer and Yüksel, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

These ratios are also known as financial ratios. It also shows how an entity is managing their

investment proposals and what return they are generating by way of dividend and interest

payments.

Return On Equity = Net Income / Shareholder's Equity

2019 = 1,227 / 14,596 = 0.084%

2020 = 3,144 / 15,638 = 0.201%

Debt Equity Ratio = Total Debts / Total Equity

2019 = 46781 / 14,596 = 3.20 times

2020 = 51091 / 15,638 = 3.26 times

Interpretation:

1.Return On Equity: -From the above calculations it can be seen that return on equity of Astra

Zeneca have been increased to some extent from 2019 to 2020. It shows how a firm is able to

manage capital to perform their business operations. There is an upward trend in return on equity

of Astra Zeneca that reflects shareholder’s expectation are fulfilled.

2.Debt Equity Ratio: - The debt to equity ratio reflects how an organisation is maintaining

balance between debt and equity structure. The ideal debt structure for any enterprise is 2:1 and

not beyond that. The debt equity ratio of Astra Zeneca is reflecting that they are at risk as

compare to their competitors because owner’s funds are less as compare to borrowed funds in

form of loans in two consecutive years. Astra Zeneca must focus on restructuring their capital

structure and should not raise funds by way of loans from banks and debenture holders.

(iv) Anticipation of the future performance of business on the basis of its past and current

position.

The future of Astra Zeneca can be forecasted by looking at current and past performance of

entity. Astra Zeneca is one of the famous medical manufacturer around the globe. The business

of Astra Zeneca has been efficient and effective and company always look for ways to bring new

innovations by way of huge spending on research and development in their products.

The past trends in their profits over the years indicates they are earning regular profits

during regular intervals ignoring some ups and downs in trends.

investment proposals and what return they are generating by way of dividend and interest

payments.

Return On Equity = Net Income / Shareholder's Equity

2019 = 1,227 / 14,596 = 0.084%

2020 = 3,144 / 15,638 = 0.201%

Debt Equity Ratio = Total Debts / Total Equity

2019 = 46781 / 14,596 = 3.20 times

2020 = 51091 / 15,638 = 3.26 times

Interpretation:

1.Return On Equity: -From the above calculations it can be seen that return on equity of Astra

Zeneca have been increased to some extent from 2019 to 2020. It shows how a firm is able to

manage capital to perform their business operations. There is an upward trend in return on equity

of Astra Zeneca that reflects shareholder’s expectation are fulfilled.

2.Debt Equity Ratio: - The debt to equity ratio reflects how an organisation is maintaining

balance between debt and equity structure. The ideal debt structure for any enterprise is 2:1 and

not beyond that. The debt equity ratio of Astra Zeneca is reflecting that they are at risk as

compare to their competitors because owner’s funds are less as compare to borrowed funds in

form of loans in two consecutive years. Astra Zeneca must focus on restructuring their capital

structure and should not raise funds by way of loans from banks and debenture holders.

(iv) Anticipation of the future performance of business on the basis of its past and current

position.

The future of Astra Zeneca can be forecasted by looking at current and past performance of

entity. Astra Zeneca is one of the famous medical manufacturer around the globe. The business

of Astra Zeneca has been efficient and effective and company always look for ways to bring new

innovations by way of huge spending on research and development in their products.

The past trends in their profits over the years indicates they are earning regular profits

during regular intervals ignoring some ups and downs in trends.

The covid-19 pandemic brought a lot of opportunities for AstraZeneca as they invested a

lot in research and development of vaccine for the new outbreak. (Latan, Jabbour, and de Sousa

Jabbour, 2019)

The strategy adopted by AstraZeneca is that they collaborated with different local

medicine manufacturers of various countries and purchase multiple vaccines using available

resources and also with the help of research.

They made a lot of profit from the sale of these different vaccines which are priced

differently in countries and this made entity stand out in worldwide industry of medicine

manufacturers. As pandemic is ongoing, it can be said that business is yet to do better in industry

for a longer period of time if it keeps investing in research and development to prevent such

virus.

The future of AstraZeneca is brighter as compare to their competitors as it is the only

manufacturer whose vaccines are developed and distributed world-wide and many studies have

called their vaccines much effective and efficient to prevent the spread..

(v) Pros and cons of historical cost accounting

Historical cost accounting – This explains accounting in a different way it states that

every asset so recorded in the balance sheet would be of the original price at the time it was

acquired by the company. It is considered to be one of the easiest to apply and understand as well

also it does not take into account the prevailing market values which makes it less time

consuming resulting in more efficient and effective working. It increases the speed of managers

in preparing financial records and reports as well (Epizitone, A., 2021).

Advantages of Historical cost accounting –

Considered simple to understand and easiest to be applied to business because it does not

count market changes such as inflation and deflation or changes in prices.

The concept is verified to be user friendly even to the person not belonging from finance

background due to the reason of not being complex in terms.

Original cost can easily be found just by going through original documents such as

receipts or invoices at the time of purchases.

3. The concept is followed since many years & is considered reliable by managers too.

4. It contributes in the easy working at the time of preparation of financial reports and

statements as it doesn't count any replacement cost, any price changes, any economic

lot in research and development of vaccine for the new outbreak. (Latan, Jabbour, and de Sousa

Jabbour, 2019)

The strategy adopted by AstraZeneca is that they collaborated with different local

medicine manufacturers of various countries and purchase multiple vaccines using available

resources and also with the help of research.

They made a lot of profit from the sale of these different vaccines which are priced

differently in countries and this made entity stand out in worldwide industry of medicine

manufacturers. As pandemic is ongoing, it can be said that business is yet to do better in industry

for a longer period of time if it keeps investing in research and development to prevent such

virus.

The future of AstraZeneca is brighter as compare to their competitors as it is the only

manufacturer whose vaccines are developed and distributed world-wide and many studies have

called their vaccines much effective and efficient to prevent the spread..

(v) Pros and cons of historical cost accounting

Historical cost accounting – This explains accounting in a different way it states that

every asset so recorded in the balance sheet would be of the original price at the time it was

acquired by the company. It is considered to be one of the easiest to apply and understand as well

also it does not take into account the prevailing market values which makes it less time

consuming resulting in more efficient and effective working. It increases the speed of managers

in preparing financial records and reports as well (Epizitone, A., 2021).

Advantages of Historical cost accounting –

Considered simple to understand and easiest to be applied to business because it does not

count market changes such as inflation and deflation or changes in prices.

The concept is verified to be user friendly even to the person not belonging from finance

background due to the reason of not being complex in terms.

Original cost can easily be found just by going through original documents such as

receipts or invoices at the time of purchases.

3. The concept is followed since many years & is considered reliable by managers too.

4. It contributes in the easy working at the time of preparation of financial reports and

statements as it doesn't count any replacement cost, any price changes, any economic

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

disparities, any fluctuations nor the present market value and net realisable values as

well.

Disadvantages of Historical cost accounting

1. The cost of assets in such accounting is fixed and doesn't show any change even after rise

or fall in market conditions and it becomes a key concern because no real picture of any

business can be framed with the help of such accounting.

2. As the name says itself historical cost accounting means cost considered from the history.

In simple words considering what has happened and not what is going to happen, what is

happening or any current situation or condition (Qiu, F. and et.al., 2020).

3. It only takes in record the asset value at date on which it was acquired and does not

change over years too.

4. Depreciation is also considered to be fixed line i.e. it does not change and is charged on

original price only for the whole life cycle of an asset.

5. It is not profitable to apply such accounting during changing conditions i.e. inflation or

deflation.

6. It is not reliable for consumers as they are not aware of the true position of the business in

market and by this method we can never conclude what is real and what is unrealistic.

7. It is not profitable at times as ignores many aspects to be taken into account to provide a

fair image and know the exact working of business in market and to sustain in changing

market and environmental conditions as well (Takeshima, and et.al., 2020).

CONCLUSION

With the help of report prepared it can be summarised that financial reporting and analysis is

a useful method in every field be it management accounting or any finance related activity. It

helps to know about the financial position of a company in market and ascertain that what is

shown in the records is true, fair and reliable. Every organisation has its own ways of working

and taking decisions which are fruitful for the company in the long run. As everyone is aware

about AstraZeneca and the products it had been dealing so far. The best part of report prepared

so far is that is easy to understand for internal as well as external users and serves as a guide to

know what would be the future plans of company and what is its present position in the market

and its liquidity too. For having a better knowledge of the working of the company some ratios

well.

Disadvantages of Historical cost accounting

1. The cost of assets in such accounting is fixed and doesn't show any change even after rise

or fall in market conditions and it becomes a key concern because no real picture of any

business can be framed with the help of such accounting.

2. As the name says itself historical cost accounting means cost considered from the history.

In simple words considering what has happened and not what is going to happen, what is

happening or any current situation or condition (Qiu, F. and et.al., 2020).

3. It only takes in record the asset value at date on which it was acquired and does not

change over years too.

4. Depreciation is also considered to be fixed line i.e. it does not change and is charged on

original price only for the whole life cycle of an asset.

5. It is not profitable to apply such accounting during changing conditions i.e. inflation or

deflation.

6. It is not reliable for consumers as they are not aware of the true position of the business in

market and by this method we can never conclude what is real and what is unrealistic.

7. It is not profitable at times as ignores many aspects to be taken into account to provide a

fair image and know the exact working of business in market and to sustain in changing

market and environmental conditions as well (Takeshima, and et.al., 2020).

CONCLUSION

With the help of report prepared it can be summarised that financial reporting and analysis is

a useful method in every field be it management accounting or any finance related activity. It

helps to know about the financial position of a company in market and ascertain that what is

shown in the records is true, fair and reliable. Every organisation has its own ways of working

and taking decisions which are fruitful for the company in the long run. As everyone is aware

about AstraZeneca and the products it had been dealing so far. The best part of report prepared

so far is that is easy to understand for internal as well as external users and serves as a guide to

know what would be the future plans of company and what is its present position in the market

and its liquidity too. For having a better knowledge of the working of the company some ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are being calculated which are then compared with its best competitors like Amgen. The last part

of report explains how historical costing can be applied in the business and to what extent it will

turn out to be useful for the company and what risks are involved so far.

of report explains how historical costing can be applied in the business and to what extent it will

turn out to be useful for the company and what risks are involved so far.

REFERENCES

Books and Journals

Dinçer, H. and Yüksel, S., 2018. Financial sector-based analysis of the G20 economies using the

integrated decision-making approach with DEMATEL and TOPSIS. In Emerging

trends in banking and finance (pp. 210-223). Springer, Cham.

Dong, W., Liao, S. and Zhang, Z., 2018. Leveraging financial social media data for corporate

fraud detection. Journal of Management Information Systems. 35(2). pp.461-487.

Epizitone, A., 2021. INTERNATIONAL CRITIQUE ON THE IAS16 PRESCRIPTION

APPLICATION AND TREATMENT. Academy of Accounting and Financial Studies

Journal. 25(1). pp.1-16.

Ji, Q. and Zhang, D., 2019. How much does financial development contribute to renewable

energy growth and upgrading of energy structure in China?. Energy Policy. 128.

pp.114-124.

Kliestik, and et.al., 2018. Bankruptcy prevention: new effort to reflect on legal and social

changes. Science and Engineering Ethics. 24(2). pp.791-803.

Latan, H., Jabbour, C.J.C. and de Sousa Jabbour, A.B.L., 2019. ‘Whistleblowing triangle’:

Framework and empirical evidence. Journal of Business Ethics. 160(1). pp.189-204

Oussii, A.A. and Taktak, N.B., 2018. Audit report timeliness: does internal audit function

coordination with external auditors matter? Empirical evidence from Tunisia. EuroMed

Journal of Business.

Parker, H. and Burke, K., 2018. Engagement Essentials: Preparation, Compilation, and Review

of Financial Statements. John Wiley & Sons.

Qiu, F. and et.al., 2020. A Neural Network Approach to the Measure of Management Accounting

Practices. Available at SSRN 3710331.

Takeshima, and et.al., 2020. The Chicago Group of Four That Changed Accounting

Research. Accounting Historians Journal. 47(2). pp.41-45.

Venturelli, A. and et.al., 2018. The state of art of corporate social disclosure before the

introduction of non-financial reporting directive: A cross country analysis. Social

responsibility journal.

Vicari, A., 2021. 8 Accounting and financial statements. In European Company Law (pp. 195-

212). De Gruyter.

Wei, L. and et.al., 2019. Developing a hierarchical system for energy corporate risk factors based

on textual risk disclosures. Energy Economics.80. pp.452-460.

Books and Journals

Dinçer, H. and Yüksel, S., 2018. Financial sector-based analysis of the G20 economies using the

integrated decision-making approach with DEMATEL and TOPSIS. In Emerging

trends in banking and finance (pp. 210-223). Springer, Cham.

Dong, W., Liao, S. and Zhang, Z., 2018. Leveraging financial social media data for corporate

fraud detection. Journal of Management Information Systems. 35(2). pp.461-487.

Epizitone, A., 2021. INTERNATIONAL CRITIQUE ON THE IAS16 PRESCRIPTION

APPLICATION AND TREATMENT. Academy of Accounting and Financial Studies

Journal. 25(1). pp.1-16.

Ji, Q. and Zhang, D., 2019. How much does financial development contribute to renewable

energy growth and upgrading of energy structure in China?. Energy Policy. 128.

pp.114-124.

Kliestik, and et.al., 2018. Bankruptcy prevention: new effort to reflect on legal and social

changes. Science and Engineering Ethics. 24(2). pp.791-803.

Latan, H., Jabbour, C.J.C. and de Sousa Jabbour, A.B.L., 2019. ‘Whistleblowing triangle’:

Framework and empirical evidence. Journal of Business Ethics. 160(1). pp.189-204

Oussii, A.A. and Taktak, N.B., 2018. Audit report timeliness: does internal audit function

coordination with external auditors matter? Empirical evidence from Tunisia. EuroMed

Journal of Business.

Parker, H. and Burke, K., 2018. Engagement Essentials: Preparation, Compilation, and Review

of Financial Statements. John Wiley & Sons.

Qiu, F. and et.al., 2020. A Neural Network Approach to the Measure of Management Accounting

Practices. Available at SSRN 3710331.

Takeshima, and et.al., 2020. The Chicago Group of Four That Changed Accounting

Research. Accounting Historians Journal. 47(2). pp.41-45.

Venturelli, A. and et.al., 2018. The state of art of corporate social disclosure before the

introduction of non-financial reporting directive: A cross country analysis. Social

responsibility journal.

Vicari, A., 2021. 8 Accounting and financial statements. In European Company Law (pp. 195-

212). De Gruyter.

Wei, L. and et.al., 2019. Developing a hierarchical system for energy corporate risk factors based

on textual risk disclosures. Energy Economics.80. pp.452-460.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.