AstraZeneca Financial Reporting: Ratio Analysis and Performance Review

VerifiedAdded on 2023/01/05

|12

|2974

|91

Report

AI Summary

This report provides a comprehensive financial analysis of AstraZeneca, a major pharmaceutical company. It begins with an introduction to financial reporting and its significance for stakeholders. The main body of the report focuses on calculating various financial ratios, including profitability, liquidity, efficiency, and gearing ratios, using data from AstraZeneca's financial statements from 2018 and 2019. The report analyzes the company's financial performance based on these ratios, highlighting trends and comparing the two years. It also discusses the impact of poor financial strategies, resource deficiencies, communication problems, increased expenses, poor inventory management, and economic crises on the company's financial performance. The report provides recommendations for improving AstraZeneca's financial position, such as reducing expenses, recovering outstanding debts, selling unwanted assets, using key financial indicators, and applying financial governance. Finally, the report describes the application of IAS 12, Income Taxes, in the context of AstraZeneca, explaining the standard's provisions regarding deferred tax and its implications for financial reporting. The report concludes with a summary of the key findings and a list of references.

FINANCIAL REPORTING

FOR BUSINESS

FOR BUSINESS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1 Calculation of financial ratio of AstraZeneca ..........................................................................1

2 Brief description of financial performance of AstraZeneca.....................................................4

3 Description of report of Deferred Tax regarding IAS 12 Income tax of AstraZeneca.........7

CONCLUSION................................................................................................................................8

REFRENCES...................................................................................................................................9

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1 Calculation of financial ratio of AstraZeneca ..........................................................................1

2 Brief description of financial performance of AstraZeneca.....................................................4

3 Description of report of Deferred Tax regarding IAS 12 Income tax of AstraZeneca.........7

CONCLUSION................................................................................................................................8

REFRENCES...................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting is consider as document which show all the relevant information

regarding financial performance of an organization. Manager formulate, financial statement, cash

flow, fund flow document as by analysis financial ratio, could represent statement for

shareholder through which they can able to recognize whether organization is beneficial for them

or not. To understand this concept, AstraZeneca has been taken. Its headquarter is situated at

Cambridge, it is British Swedish organization which pharmaceutical business. This report

describe financial performance of organization by calculating relevant ratio. It also define

revenue of IAS 12 income tax standard and its provision in context with AstraZeneca

MAIN BODY

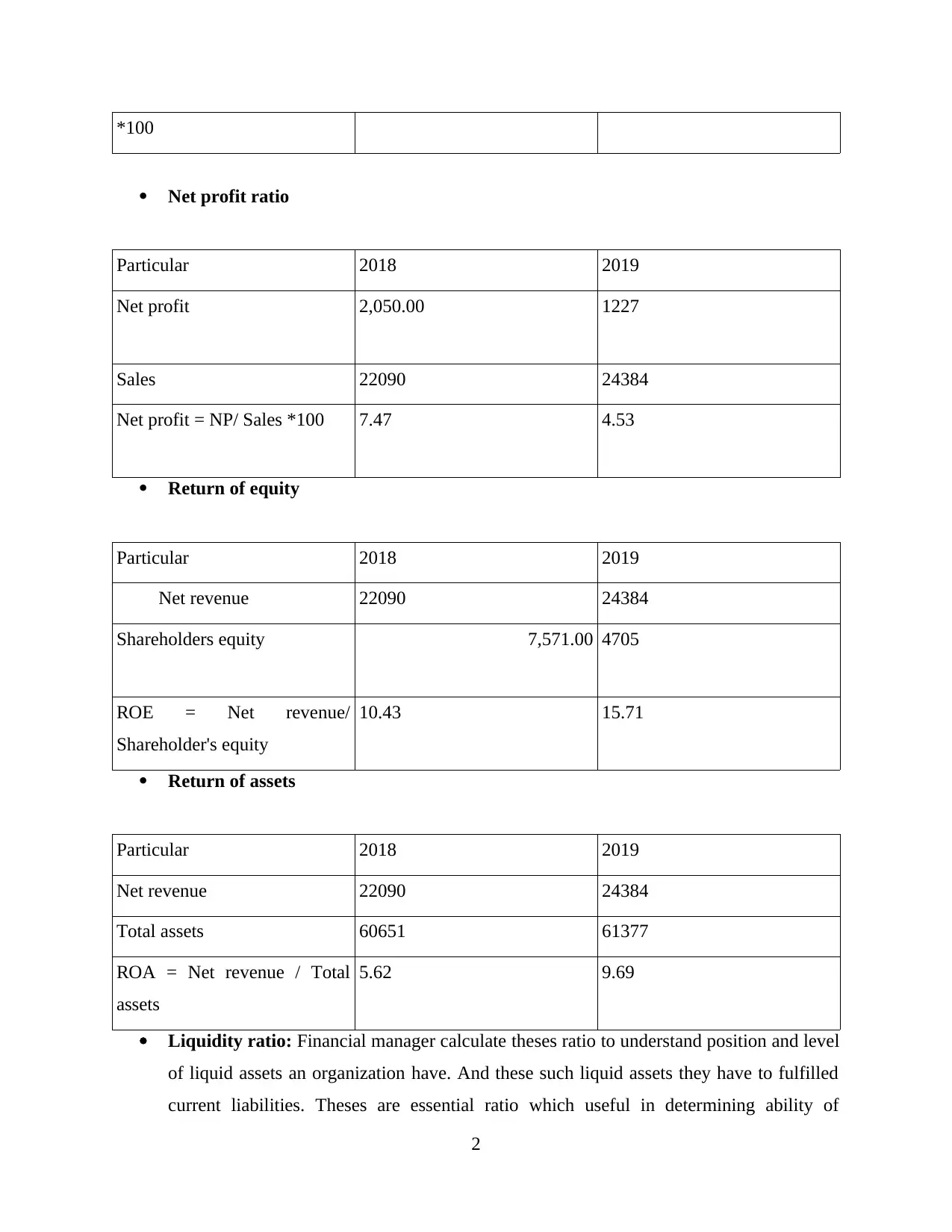

1 Calculation of financial ratio of AstraZeneca

Financial ratio: Theses are the technique of financial management used by managers

for understanding financial performance of an organization on the basis of calculating magnitude

of 2 select financial value of items taken from financial statements. There are various types of

ratio which divide in series according to their relevance. Following are the ratio analysis of

AstraZeneca

Profitability ratio: Theses ratio are calculated for analysing ability of organization to

generate profit and use of these profits to fulfil liability of organization. Organization

use this ratio for measuring as well as compromising its revenue rate from current year to

past year. By profitably ratio , organization easily find out reason and well as difference

arise in revenue rate from any comparative year. It considers, revenue generate from

trading and business activities, and through investment in shares. following are profitably

ratio of AstraZeneca define below AstraZeneca (Pando, San-José, and Sicilia, 2019).

Gross profit ratio

Particular 2018 2019

Gross profit 557.6 728.24

Sales 22,090.00 24384

Gross profit ratio = GP/ Sales 2.9 2.52

1

Financial reporting is consider as document which show all the relevant information

regarding financial performance of an organization. Manager formulate, financial statement, cash

flow, fund flow document as by analysis financial ratio, could represent statement for

shareholder through which they can able to recognize whether organization is beneficial for them

or not. To understand this concept, AstraZeneca has been taken. Its headquarter is situated at

Cambridge, it is British Swedish organization which pharmaceutical business. This report

describe financial performance of organization by calculating relevant ratio. It also define

revenue of IAS 12 income tax standard and its provision in context with AstraZeneca

MAIN BODY

1 Calculation of financial ratio of AstraZeneca

Financial ratio: Theses are the technique of financial management used by managers

for understanding financial performance of an organization on the basis of calculating magnitude

of 2 select financial value of items taken from financial statements. There are various types of

ratio which divide in series according to their relevance. Following are the ratio analysis of

AstraZeneca

Profitability ratio: Theses ratio are calculated for analysing ability of organization to

generate profit and use of these profits to fulfil liability of organization. Organization

use this ratio for measuring as well as compromising its revenue rate from current year to

past year. By profitably ratio , organization easily find out reason and well as difference

arise in revenue rate from any comparative year. It considers, revenue generate from

trading and business activities, and through investment in shares. following are profitably

ratio of AstraZeneca define below AstraZeneca (Pando, San-José, and Sicilia, 2019).

Gross profit ratio

Particular 2018 2019

Gross profit 557.6 728.24

Sales 22,090.00 24384

Gross profit ratio = GP/ Sales 2.9 2.52

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*100

Net profit ratio

Particular 2018 2019

Net profit 2,050.00 1227

Sales 22090 24384

Net profit = NP/ Sales *100 7.47 4.53

Return of equity

Particular 2018 2019

Net revenue 22090 24384

Shareholders equity 7,571.00 4705

ROE = Net revenue/

Shareholder's equity

10.43 15.71

Return of assets

Particular 2018 2019

Net revenue 22090 24384

Total assets 60651 61377

ROA = Net revenue / Total

assets

5.62 9.69

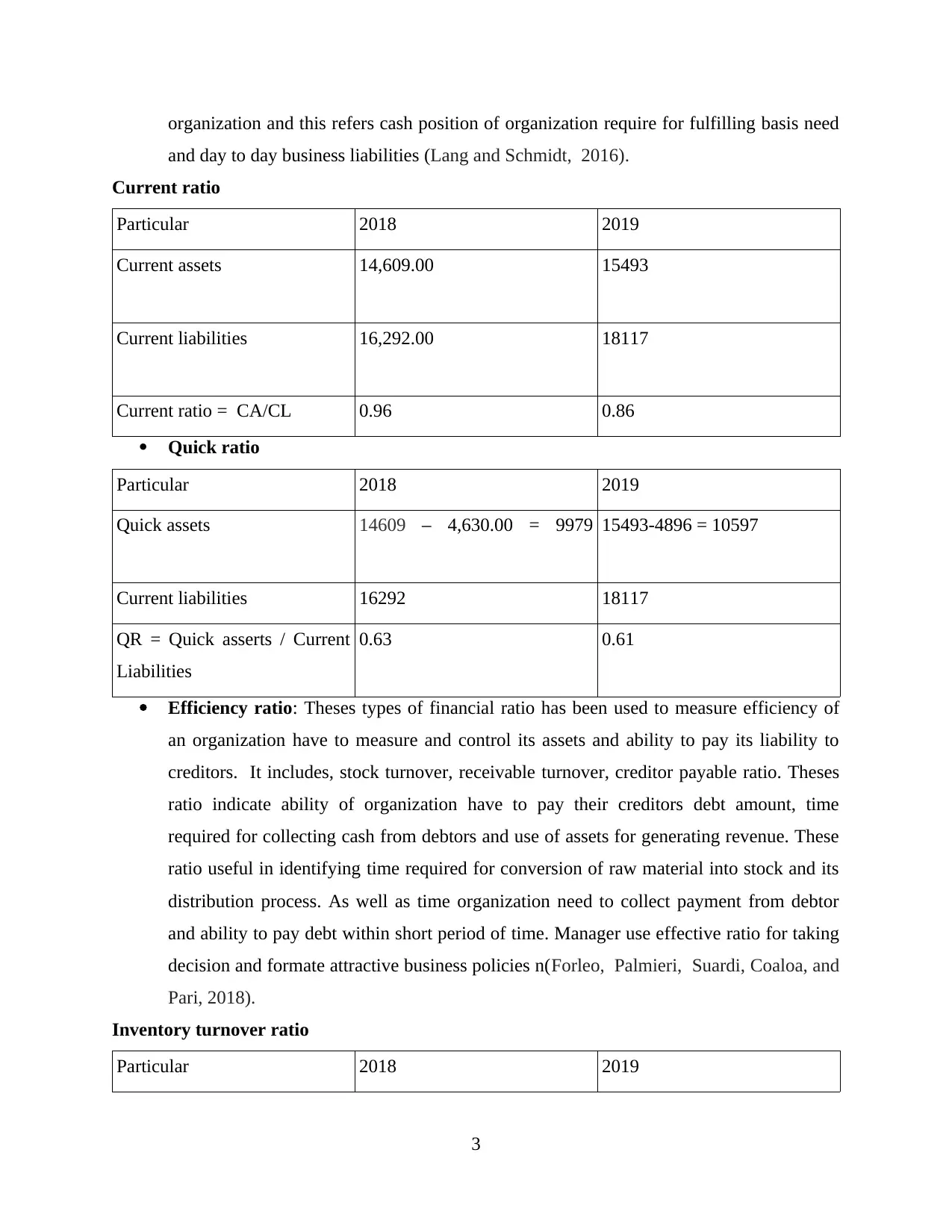

Liquidity ratio: Financial manager calculate theses ratio to understand position and level

of liquid assets an organization have. And these such liquid assets they have to fulfilled

current liabilities. Theses are essential ratio which useful in determining ability of

2

Net profit ratio

Particular 2018 2019

Net profit 2,050.00 1227

Sales 22090 24384

Net profit = NP/ Sales *100 7.47 4.53

Return of equity

Particular 2018 2019

Net revenue 22090 24384

Shareholders equity 7,571.00 4705

ROE = Net revenue/

Shareholder's equity

10.43 15.71

Return of assets

Particular 2018 2019

Net revenue 22090 24384

Total assets 60651 61377

ROA = Net revenue / Total

assets

5.62 9.69

Liquidity ratio: Financial manager calculate theses ratio to understand position and level

of liquid assets an organization have. And these such liquid assets they have to fulfilled

current liabilities. Theses are essential ratio which useful in determining ability of

2

organization and this refers cash position of organization require for fulfilling basis need

and day to day business liabilities (Lang and Schmidt, 2016).

Current ratio

Particular 2018 2019

Current assets 14,609.00 15493

Current liabilities 16,292.00 18117

Current ratio = CA/CL 0.96 0.86

Quick ratio

Particular 2018 2019

Quick assets 14609 – 4,630.00 = 9979 15493-4896 = 10597

Current liabilities 16292 18117

QR = Quick asserts / Current

Liabilities

0.63 0.61

Efficiency ratio: Theses types of financial ratio has been used to measure efficiency of

an organization have to measure and control its assets and ability to pay its liability to

creditors. It includes, stock turnover, receivable turnover, creditor payable ratio. Theses

ratio indicate ability of organization have to pay their creditors debt amount, time

required for collecting cash from debtors and use of assets for generating revenue. These

ratio useful in identifying time required for conversion of raw material into stock and its

distribution process. As well as time organization need to collect payment from debtor

and ability to pay debt within short period of time. Manager use effective ratio for taking

decision and formate attractive business policies n(Forleo, Palmieri, Suardi, Coaloa, and

Pari, 2018).

Inventory turnover ratio

Particular 2018 2019

3

and day to day business liabilities (Lang and Schmidt, 2016).

Current ratio

Particular 2018 2019

Current assets 14,609.00 15493

Current liabilities 16,292.00 18117

Current ratio = CA/CL 0.96 0.86

Quick ratio

Particular 2018 2019

Quick assets 14609 – 4,630.00 = 9979 15493-4896 = 10597

Current liabilities 16292 18117

QR = Quick asserts / Current

Liabilities

0.63 0.61

Efficiency ratio: Theses types of financial ratio has been used to measure efficiency of

an organization have to measure and control its assets and ability to pay its liability to

creditors. It includes, stock turnover, receivable turnover, creditor payable ratio. Theses

ratio indicate ability of organization have to pay their creditors debt amount, time

required for collecting cash from debtors and use of assets for generating revenue. These

ratio useful in identifying time required for conversion of raw material into stock and its

distribution process. As well as time organization need to collect payment from debtor

and ability to pay debt within short period of time. Manager use effective ratio for taking

decision and formate attractive business policies n(Forleo, Palmieri, Suardi, Coaloa, and

Pari, 2018).

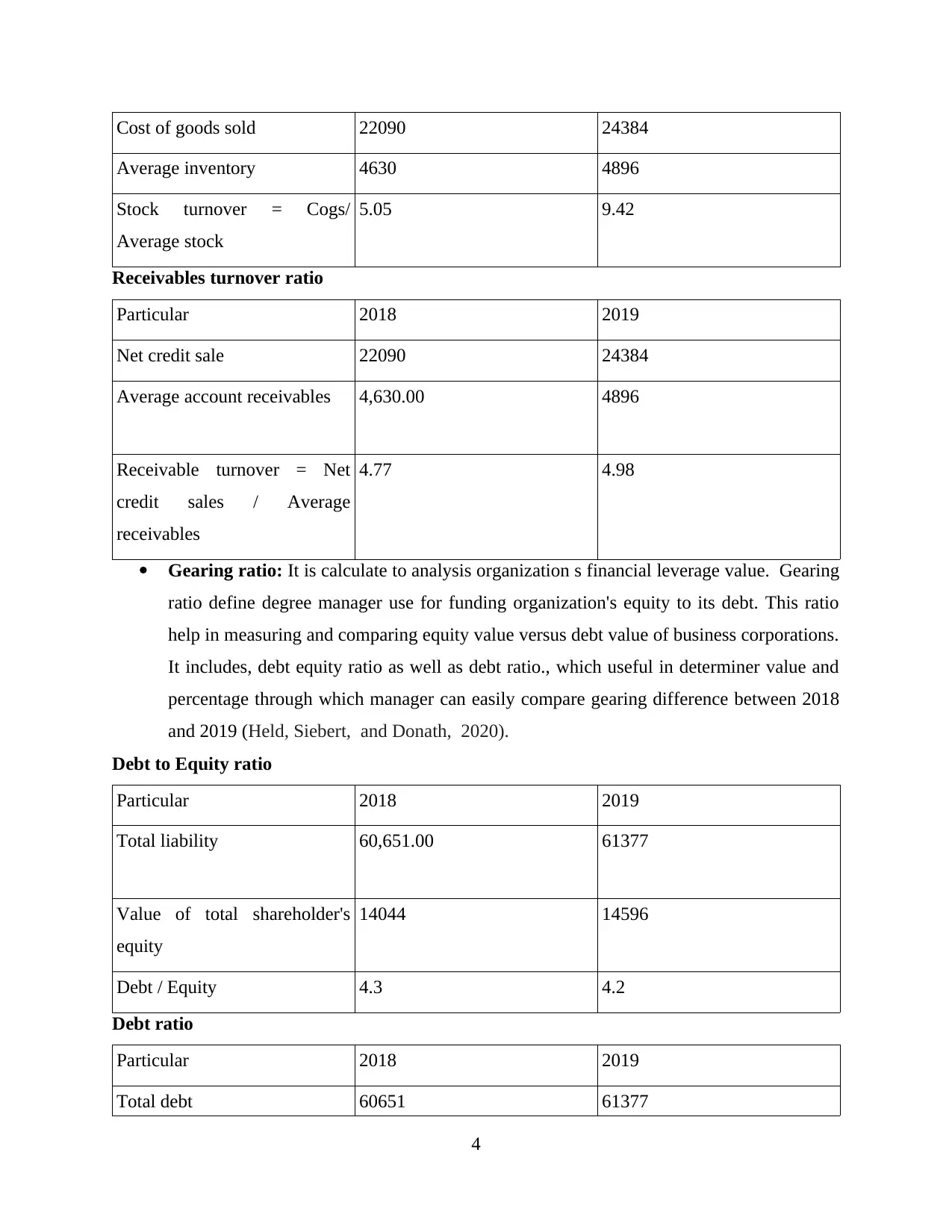

Inventory turnover ratio

Particular 2018 2019

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of goods sold 22090 24384

Average inventory 4630 4896

Stock turnover = Cogs/

Average stock

5.05 9.42

Receivables turnover ratio

Particular 2018 2019

Net credit sale 22090 24384

Average account receivables 4,630.00 4896

Receivable turnover = Net

credit sales / Average

receivables

4.77 4.98

Gearing ratio: It is calculate to analysis organization s financial leverage value. Gearing

ratio define degree manager use for funding organization's equity to its debt. This ratio

help in measuring and comparing equity value versus debt value of business corporations.

It includes, debt equity ratio as well as debt ratio., which useful in determiner value and

percentage through which manager can easily compare gearing difference between 2018

and 2019 (Held, Siebert, and Donath, 2020).

Debt to Equity ratio

Particular 2018 2019

Total liability 60,651.00 61377

Value of total shareholder's

equity

14044 14596

Debt / Equity 4.3 4.2

Debt ratio

Particular 2018 2019

Total debt 60651 61377

4

Average inventory 4630 4896

Stock turnover = Cogs/

Average stock

5.05 9.42

Receivables turnover ratio

Particular 2018 2019

Net credit sale 22090 24384

Average account receivables 4,630.00 4896

Receivable turnover = Net

credit sales / Average

receivables

4.77 4.98

Gearing ratio: It is calculate to analysis organization s financial leverage value. Gearing

ratio define degree manager use for funding organization's equity to its debt. This ratio

help in measuring and comparing equity value versus debt value of business corporations.

It includes, debt equity ratio as well as debt ratio., which useful in determiner value and

percentage through which manager can easily compare gearing difference between 2018

and 2019 (Held, Siebert, and Donath, 2020).

Debt to Equity ratio

Particular 2018 2019

Total liability 60,651.00 61377

Value of total shareholder's

equity

14044 14596

Debt / Equity 4.3 4.2

Debt ratio

Particular 2018 2019

Total debt 60651 61377

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

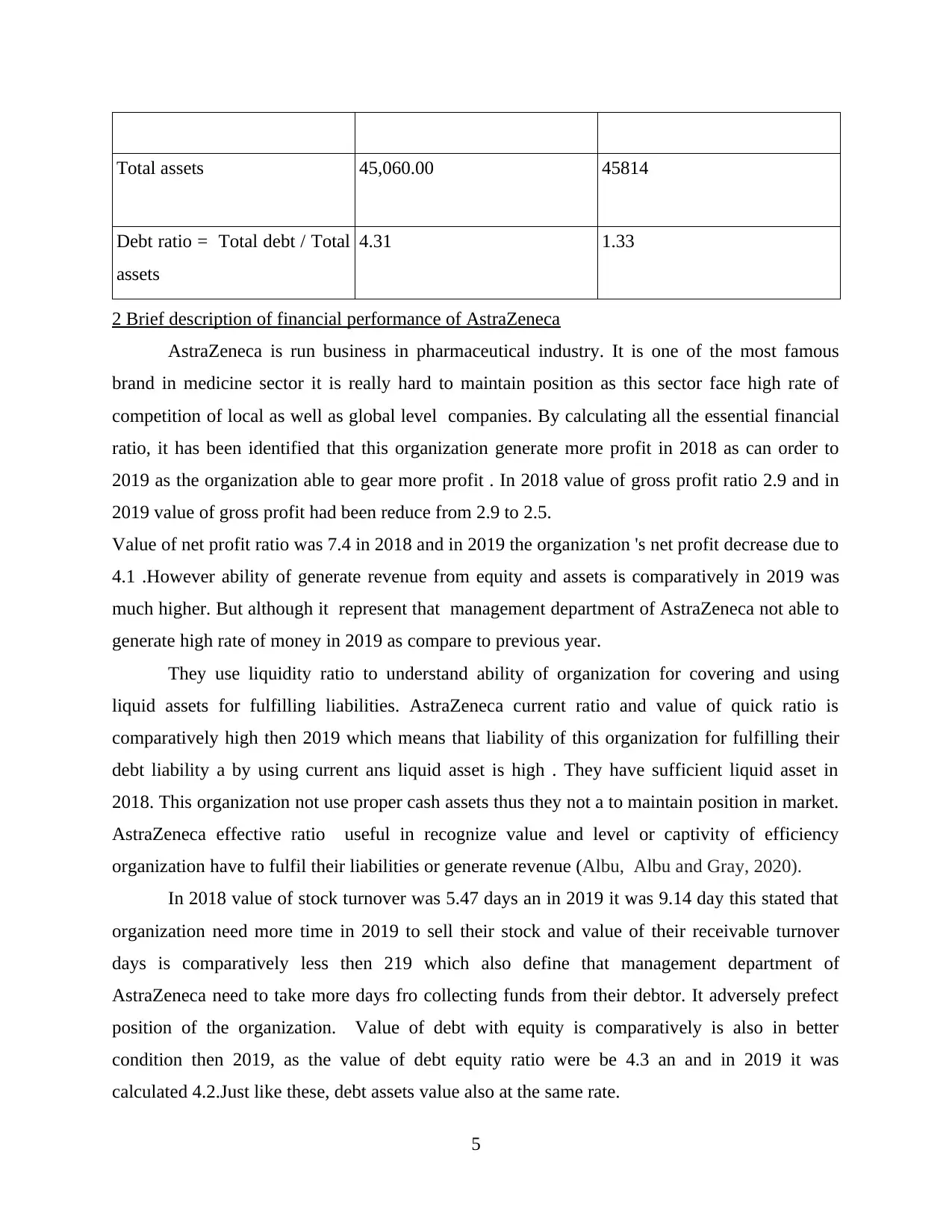

Total assets 45,060.00 45814

Debt ratio = Total debt / Total

assets

4.31 1.33

2 Brief description of financial performance of AstraZeneca

AstraZeneca is run business in pharmaceutical industry. It is one of the most famous

brand in medicine sector it is really hard to maintain position as this sector face high rate of

competition of local as well as global level companies. By calculating all the essential financial

ratio, it has been identified that this organization generate more profit in 2018 as can order to

2019 as the organization able to gear more profit . In 2018 value of gross profit ratio 2.9 and in

2019 value of gross profit had been reduce from 2.9 to 2.5.

Value of net profit ratio was 7.4 in 2018 and in 2019 the organization 's net profit decrease due to

4.1 .However ability of generate revenue from equity and assets is comparatively in 2019 was

much higher. But although it represent that management department of AstraZeneca not able to

generate high rate of money in 2019 as compare to previous year.

They use liquidity ratio to understand ability of organization for covering and using

liquid assets for fulfilling liabilities. AstraZeneca current ratio and value of quick ratio is

comparatively high then 2019 which means that liability of this organization for fulfilling their

debt liability a by using current ans liquid asset is high . They have sufficient liquid asset in

2018. This organization not use proper cash assets thus they not a to maintain position in market.

AstraZeneca effective ratio useful in recognize value and level or captivity of efficiency

organization have to fulfil their liabilities or generate revenue (Albu, Albu and Gray, 2020).

In 2018 value of stock turnover was 5.47 days an in 2019 it was 9.14 day this stated that

organization need more time in 2019 to sell their stock and value of their receivable turnover

days is comparatively less then 219 which also define that management department of

AstraZeneca need to take more days fro collecting funds from their debtor. It adversely prefect

position of the organization. Value of debt with equity is comparatively is also in better

condition then 2019, as the value of debt equity ratio were be 4.3 an and in 2019 it was

calculated 4.2.Just like these, debt assets value also at the same rate.

5

Debt ratio = Total debt / Total

assets

4.31 1.33

2 Brief description of financial performance of AstraZeneca

AstraZeneca is run business in pharmaceutical industry. It is one of the most famous

brand in medicine sector it is really hard to maintain position as this sector face high rate of

competition of local as well as global level companies. By calculating all the essential financial

ratio, it has been identified that this organization generate more profit in 2018 as can order to

2019 as the organization able to gear more profit . In 2018 value of gross profit ratio 2.9 and in

2019 value of gross profit had been reduce from 2.9 to 2.5.

Value of net profit ratio was 7.4 in 2018 and in 2019 the organization 's net profit decrease due to

4.1 .However ability of generate revenue from equity and assets is comparatively in 2019 was

much higher. But although it represent that management department of AstraZeneca not able to

generate high rate of money in 2019 as compare to previous year.

They use liquidity ratio to understand ability of organization for covering and using

liquid assets for fulfilling liabilities. AstraZeneca current ratio and value of quick ratio is

comparatively high then 2019 which means that liability of this organization for fulfilling their

debt liability a by using current ans liquid asset is high . They have sufficient liquid asset in

2018. This organization not use proper cash assets thus they not a to maintain position in market.

AstraZeneca effective ratio useful in recognize value and level or captivity of efficiency

organization have to fulfil their liabilities or generate revenue (Albu, Albu and Gray, 2020).

In 2018 value of stock turnover was 5.47 days an in 2019 it was 9.14 day this stated that

organization need more time in 2019 to sell their stock and value of their receivable turnover

days is comparatively less then 219 which also define that management department of

AstraZeneca need to take more days fro collecting funds from their debtor. It adversely prefect

position of the organization. Value of debt with equity is comparatively is also in better

condition then 2019, as the value of debt equity ratio were be 4.3 an and in 2019 it was

calculated 4.2.Just like these, debt assets value also at the same rate.

5

From analysing all the ratio it has been identified that position of AstraZeneca in market

as compare to 2018 was decrease. Organization not able to maintain its position and revenue

gernatet6in rate. Even they don't have enough time to control and handle efficiency level of the

organization. Thus it is relay hard to maintain effective efficacy and capability of payment to

creditors for the organization. Following are the reason financial performance of AstraZeneca

has been decreases

Poor financial strategy: Decrement in profits may be cause due to not using effective financial

strategies and plan which directivity impact managing assets and liabilities . It become the reason

of reduction in profit rates.

Resource deficiency: By not properly use financial resource and lack of expertise also main

case of decrement of financial performance of AstraZeneca . As due to Brixit agreement rate of

employee turnover goes high thus organization not able skilled personal for their work.

Poor communication problem: Organization not able to effective communicate with their

workforce , they don't able to understand clear goal thus workforce not able to work in effective

manner. They don't use effective marketing tools for communication.

Increment in expenses: To spread target market, AstraZeneca focus on research , it directly

increase cost of organization. Which also reasoning of reduce rate of profits.

Poor management if inventory: Management department of AstraZeneca not properly formate

polices and use tools for manage and control stock thus it will become reason on increasing

maintaining cost of inventory which directly impact on financial performance and increase value

of stock turnover ratio (Grishkina, Sidneva, Shcherbinina and Dubinina, 2018).

Effect of economic crises: After Brixit agreement , all the European countries change and made

strict or rigid polices regarding trade. Before this agreement, AstraZeneca easily get ingredient

require for produce drugs but now due to economic recession period, and high rate of ingredient,

the cost of producing drug is getting to high. Which may become the reason that organization

increase their price and this will adversely impact on reducing profit rates.

For enhancing financial position of AstraZeneca ,its management department needs to implement

following suggestion

Reduce expenses: Management department of AstraZeneca by cut throat activities which

generate high rate of cash outflow can able to increase their profits .

6

as compare to 2018 was decrease. Organization not able to maintain its position and revenue

gernatet6in rate. Even they don't have enough time to control and handle efficiency level of the

organization. Thus it is relay hard to maintain effective efficacy and capability of payment to

creditors for the organization. Following are the reason financial performance of AstraZeneca

has been decreases

Poor financial strategy: Decrement in profits may be cause due to not using effective financial

strategies and plan which directivity impact managing assets and liabilities . It become the reason

of reduction in profit rates.

Resource deficiency: By not properly use financial resource and lack of expertise also main

case of decrement of financial performance of AstraZeneca . As due to Brixit agreement rate of

employee turnover goes high thus organization not able skilled personal for their work.

Poor communication problem: Organization not able to effective communicate with their

workforce , they don't able to understand clear goal thus workforce not able to work in effective

manner. They don't use effective marketing tools for communication.

Increment in expenses: To spread target market, AstraZeneca focus on research , it directly

increase cost of organization. Which also reasoning of reduce rate of profits.

Poor management if inventory: Management department of AstraZeneca not properly formate

polices and use tools for manage and control stock thus it will become reason on increasing

maintaining cost of inventory which directly impact on financial performance and increase value

of stock turnover ratio (Grishkina, Sidneva, Shcherbinina and Dubinina, 2018).

Effect of economic crises: After Brixit agreement , all the European countries change and made

strict or rigid polices regarding trade. Before this agreement, AstraZeneca easily get ingredient

require for produce drugs but now due to economic recession period, and high rate of ingredient,

the cost of producing drug is getting to high. Which may become the reason that organization

increase their price and this will adversely impact on reducing profit rates.

For enhancing financial position of AstraZeneca ,its management department needs to implement

following suggestion

Reduce expenses: Management department of AstraZeneca by cut throat activities which

generate high rate of cash outflow can able to increase their profits .

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recover outstanding debt collection: The main reason of reduction in financial performance of

the organization is that not pay timely their debt payment. Manager need to use effective strategy

to control their non performing asset and proved attract discount offer it will useful in motivate

customer so they pay cash rather then credit payment.

Selling of unwanted assets: AstraZeneca is multinational organization , in the situation of

financial crises, they can cover up cost and manage liquidity by selling unwanted asset and

securities. To increase cash inflow level within the organization .

Uses of key financial indicators: Management department of AstraZeneca need to apply key

performance indicator, benchmarking , theses technique useful in performance measurement .By

using marginal tools they can increase their sales market through motivate employee to cover up

target by offering them incentive.

Apply financial governance : AstraZeneca need to focus on applying this policy, as it will useful

in properly maintain records as well as work in ethical way. Manager for controlling misuse off

financial resources apply financial governance. This help in tracking all the records in effective

way.

3 Description of report of Deferred Tax regarding IAS 12 Income tax of AstraZeneca

IAS 12 , is related with provision regarding Deferred tax and its implementation during

preparing financial statement. During preparation of financial statement it is essential for

managers to focus on provision regarding tax and theses will be implies according to

International Financial Standard terms. IAS 12 standard is related with defiling method of

computation of current as well as deferred tax. It define as use of business assets and essential

liabilities which reflect corporate profit for same type of treatment.

This standard contain 8 section. Which define meaning, definition of deferred tax, how

organization able to calculate it , and requirement of IAS 12. It also define how manager allocate

liability of deferred tax, by adjustment in profit as well as loss, comprehensive income. They

disclose, deferred tax amount of current and future charges. In the their section related with

detail information regarding disclosure of unproved deferred tax, difference arises between asset

& liabilities. Recognition of deferred asset. IAS 12 by using norms of this standard AstraZeneca

could understand how asset and liabilities compensate with tax amounts. Settlement of tax and

how manager will be able to recover rates, They solve problem problem (Mullinova, and

Simonyants, 2016).

7

the organization is that not pay timely their debt payment. Manager need to use effective strategy

to control their non performing asset and proved attract discount offer it will useful in motivate

customer so they pay cash rather then credit payment.

Selling of unwanted assets: AstraZeneca is multinational organization , in the situation of

financial crises, they can cover up cost and manage liquidity by selling unwanted asset and

securities. To increase cash inflow level within the organization .

Uses of key financial indicators: Management department of AstraZeneca need to apply key

performance indicator, benchmarking , theses technique useful in performance measurement .By

using marginal tools they can increase their sales market through motivate employee to cover up

target by offering them incentive.

Apply financial governance : AstraZeneca need to focus on applying this policy, as it will useful

in properly maintain records as well as work in ethical way. Manager for controlling misuse off

financial resources apply financial governance. This help in tracking all the records in effective

way.

3 Description of report of Deferred Tax regarding IAS 12 Income tax of AstraZeneca

IAS 12 , is related with provision regarding Deferred tax and its implementation during

preparing financial statement. During preparation of financial statement it is essential for

managers to focus on provision regarding tax and theses will be implies according to

International Financial Standard terms. IAS 12 standard is related with defiling method of

computation of current as well as deferred tax. It define as use of business assets and essential

liabilities which reflect corporate profit for same type of treatment.

This standard contain 8 section. Which define meaning, definition of deferred tax, how

organization able to calculate it , and requirement of IAS 12. It also define how manager allocate

liability of deferred tax, by adjustment in profit as well as loss, comprehensive income. They

disclose, deferred tax amount of current and future charges. In the their section related with

detail information regarding disclosure of unproved deferred tax, difference arises between asset

& liabilities. Recognition of deferred asset. IAS 12 by using norms of this standard AstraZeneca

could understand how asset and liabilities compensate with tax amounts. Settlement of tax and

how manager will be able to recover rates, They solve problem problem (Mullinova, and

Simonyants, 2016).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AstraZeneca suffers from issue arising due to complexities of deferred tax . Provision of

this tax help manager to avoid or eliminate intra group revenues. IAS 12 help in giving

information regarding how profit has been calculated and equity recognise profits. Provision of

shared payment . This standard define recovery of assets which is related with deferred payment

and is of these assets for analysing financial balance sheet.

IAS 12 's last sections define about summery if all the issues and method of solving all these

issue. It clearly mention that whether tax refine meets and fulfil criteria of deferred tax.

Reason of differences and variation arise between recognizing initial assets value. Base required

for changing theses standard .

Changes in accounting policies on the basis of revaluation in tax base system.

AstraZeneca use this standard norm which help in defining all the process and riles required for

calculation if income tax on the basis of include all the essential taxer. Manager of AstraZeneca

consider all the relevant tax liabilities during preparation of financial statements. It includes

foreign, domestic taxes, and also 2withohlding tax. Theses are playable by organization;s

subsidised. This standard define methods of accounting which is related with accounting grant.

AstraZeneca use this system as it will help in considering all the tax and manager can easily

define and evaluate difference and effective of each tax on calculating profit. AstraZeneca 's

management department can easily evaluate and recognize assets as well as liabilities which is

directly linked with de4ffred tax . It define systems sequences of payment of future tax

(Badenhorst, and Ferreira, 2016).

They calculate amount of deferred tax for success fulling competing all the more which

help in fulfilling responsibilities of financial governance. Managers for understanding effect of

all theses essential element of financial statement use this tax system. AstraZeneca cause

calculating of deferred tax can able to understand all the essential requirement, difference of

asset and liabilities and effect of each item due to effect of theses assets.

CONCLUSION

From the above analysis it has been concluded that every business organization needs,

financial reporting for identify and recognize financial position of their organization. On the

basis of that they formulate reports to represent theses report for their stockholders. By using

financial ratio, managers can easily recognize liquidity position of the organization and its

efficiency as well as ability of organization for fulfilling current and long term debt liabilities.

8

this tax help manager to avoid or eliminate intra group revenues. IAS 12 help in giving

information regarding how profit has been calculated and equity recognise profits. Provision of

shared payment . This standard define recovery of assets which is related with deferred payment

and is of these assets for analysing financial balance sheet.

IAS 12 's last sections define about summery if all the issues and method of solving all these

issue. It clearly mention that whether tax refine meets and fulfil criteria of deferred tax.

Reason of differences and variation arise between recognizing initial assets value. Base required

for changing theses standard .

Changes in accounting policies on the basis of revaluation in tax base system.

AstraZeneca use this standard norm which help in defining all the process and riles required for

calculation if income tax on the basis of include all the essential taxer. Manager of AstraZeneca

consider all the relevant tax liabilities during preparation of financial statements. It includes

foreign, domestic taxes, and also 2withohlding tax. Theses are playable by organization;s

subsidised. This standard define methods of accounting which is related with accounting grant.

AstraZeneca use this system as it will help in considering all the tax and manager can easily

define and evaluate difference and effective of each tax on calculating profit. AstraZeneca 's

management department can easily evaluate and recognize assets as well as liabilities which is

directly linked with de4ffred tax . It define systems sequences of payment of future tax

(Badenhorst, and Ferreira, 2016).

They calculate amount of deferred tax for success fulling competing all the more which

help in fulfilling responsibilities of financial governance. Managers for understanding effect of

all theses essential element of financial statement use this tax system. AstraZeneca cause

calculating of deferred tax can able to understand all the essential requirement, difference of

asset and liabilities and effect of each item due to effect of theses assets.

CONCLUSION

From the above analysis it has been concluded that every business organization needs,

financial reporting for identify and recognize financial position of their organization. On the

basis of that they formulate reports to represent theses report for their stockholders. By using

financial ratio, managers can easily recognize liquidity position of the organization and its

efficiency as well as ability of organization for fulfilling current and long term debt liabilities.

8

With the use of ratio s manage able to take decision regarding formation of effective financial

strategies through which they can able to attain business goals and generate high rate of profits.

For enhancing performance,managers need to apply and work according to IAS 12 standard

these help in work in ethical way and resolve issue arise regarding no payment of tax value .

REFRENCES

From books and journals

Pando, V., San-José, L. A. and Sicilia, J., 2019. Profitability ratio maximization in an inventory

model with stock-dependent demand rate and non-linear holding cost. Applied

Mathematical Modelling, 66. pp.643-661.

Lang, M. and Schmidt, P. G., 2016. The early warnings of banking crises: Interaction of broad

liquidity and demand deposits. Journal of International Money and Finance, 61, pp.1-

29.

Forleo, M. B., Palmieri, N., Suardi, A., Coaloa, D. and Pari, L., 2018. The eco-efficiency of

rapeseed and sunflower cultivation in Italy. Joining environmental and economic

assessment. Journal of Cleaner Production, 172, pp.3138-3153.

Held, S., Siebert, T. and Donath, L., 2020. Changes in mechanical power output in rowing by

varying stroke rate and gearing. European journal of sport science, 20(3), pp.357-365.

Albu, N., Albu, C. N. and Gray, S.J., 2020, February. Institutional factors and the impact of

international financial reporting standards: the Central and Eastern European

experience. In Accounting Forum (pp. 1-31). Routledge.

Grishkina, S., Sidneva, V., Shcherbinina, Y. and Dubinina, G., 2018, October. Comparability of

financial reporting under different tax regimes. In The 2018 International Conference

on Digital Science (pp. 88-93). Springer, Cham.

Mullinova, S. and Simonyants, N., 2016. Reflection of a deferred tax liability in the credit union

reporting according to IFRS (IAS) 12" Income taxes". Modern European Researches,

(1). pp.83-88.

Badenhorst, W. M. and Ferreira, P. H., 2016. The Financial Crisis and the Value‐relevance of

Recognised Deferred Tax Assets. Australian Accounting Review, 26(3). pp.291-300.

9

strategies through which they can able to attain business goals and generate high rate of profits.

For enhancing performance,managers need to apply and work according to IAS 12 standard

these help in work in ethical way and resolve issue arise regarding no payment of tax value .

REFRENCES

From books and journals

Pando, V., San-José, L. A. and Sicilia, J., 2019. Profitability ratio maximization in an inventory

model with stock-dependent demand rate and non-linear holding cost. Applied

Mathematical Modelling, 66. pp.643-661.

Lang, M. and Schmidt, P. G., 2016. The early warnings of banking crises: Interaction of broad

liquidity and demand deposits. Journal of International Money and Finance, 61, pp.1-

29.

Forleo, M. B., Palmieri, N., Suardi, A., Coaloa, D. and Pari, L., 2018. The eco-efficiency of

rapeseed and sunflower cultivation in Italy. Joining environmental and economic

assessment. Journal of Cleaner Production, 172, pp.3138-3153.

Held, S., Siebert, T. and Donath, L., 2020. Changes in mechanical power output in rowing by

varying stroke rate and gearing. European journal of sport science, 20(3), pp.357-365.

Albu, N., Albu, C. N. and Gray, S.J., 2020, February. Institutional factors and the impact of

international financial reporting standards: the Central and Eastern European

experience. In Accounting Forum (pp. 1-31). Routledge.

Grishkina, S., Sidneva, V., Shcherbinina, Y. and Dubinina, G., 2018, October. Comparability of

financial reporting under different tax regimes. In The 2018 International Conference

on Digital Science (pp. 88-93). Springer, Cham.

Mullinova, S. and Simonyants, N., 2016. Reflection of a deferred tax liability in the credit union

reporting according to IFRS (IAS) 12" Income taxes". Modern European Researches,

(1). pp.83-88.

Badenhorst, W. M. and Ferreira, P. H., 2016. The Financial Crisis and the Value‐relevance of

Recognised Deferred Tax Assets. Australian Accounting Review, 26(3). pp.291-300.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.