HI5020 Corporate Accounting: Financial Analysis of ASX Listed Firms

VerifiedAdded on 2023/04/25

|32

|4566

|415

Report

AI Summary

This report analyzes the financial statements of three ASX-listed companies: Domino’s Pizza Enterprise Limited, G8 Education Limited, and Navitas Limited, focusing on equity, liabilities, cash flow statements, other comprehensive income, and corporate income tax. The analysis includes a comparative study of debt and equity positions, cash flow activities, and items reported under other comprehensive income. The report also examines the tax expenses, effective tax rates, deferred tax assets and liabilities, and cash tax rates for each company. The debt-equity structure is evaluated, highlighting leverage positions and solvency. The report concludes with insights into how these companies manage their finances and tax obligations, offering a comprehensive overview of their financial health. Desklib provides access to similar solved assignments and resources for students.

Running head: CORPORATE ACCOUNTING

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Corporate accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive summary

Aim of the report is to analyse the financial report of ASX listed companies Domino’s

Enterprise Limited, G8 Education Limited and Navitas Limited. The report will focus on the

items on equity and liability and changes taken place for those items during the year from

2015 to 2017. The report will further focus on the cash flow statements of the companies and

other comprehensive income statements. Finally the report will highlight the tax treatment of

the companies reported in the financial statements.

CORPORATE ACCOUNTING

Executive summary

Aim of the report is to analyse the financial report of ASX listed companies Domino’s

Enterprise Limited, G8 Education Limited and Navitas Limited. The report will focus on the

items on equity and liability and changes taken place for those items during the year from

2015 to 2017. The report will further focus on the cash flow statements of the companies and

other comprehensive income statements. Finally the report will highlight the tax treatment of

the companies reported in the financial statements.

2

CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Equity and liabilities..................................................................................................................3

(i) Equity items.................................................................................................................3

(ii) Liability items..............................................................................................................6

(iii) Comparative analysis of debt and equity position.......................................................8

Cash flow statement...................................................................................................................9

(iv) Listed items for cash flow...........................................................................................9

(v) Comparative analysis.................................................................................................11

(vi) Comparative analysis selected for explaining insights..............................................13

Other comprehensive income statement..................................................................................13

(vii) Reported items under other comprehensive income (OCI).......................................13

(viii) Why items of OCI are not reported in the profit and loss statement.....................14

(ix) Comparative analysis of items reported under OCI..................................................15

(x) Including comprehensive income to analyse the manager’s performance................15

Accounting for corporate income tax.......................................................................................15

(xi) Reported tax expenses for 2017................................................................................15

(xii) Effective rate of tax...................................................................................................15

(xiii) Deferred tax assets or deferred tax liabilities.........................................................16

(xiv) Increase or decrease in deferred tax assets or liabilities reported by the entities. .16

CORPORATE ACCOUNTING

Table of Contents

Introduction................................................................................................................................3

Equity and liabilities..................................................................................................................3

(i) Equity items.................................................................................................................3

(ii) Liability items..............................................................................................................6

(iii) Comparative analysis of debt and equity position.......................................................8

Cash flow statement...................................................................................................................9

(iv) Listed items for cash flow...........................................................................................9

(v) Comparative analysis.................................................................................................11

(vi) Comparative analysis selected for explaining insights..............................................13

Other comprehensive income statement..................................................................................13

(vii) Reported items under other comprehensive income (OCI).......................................13

(viii) Why items of OCI are not reported in the profit and loss statement.....................14

(ix) Comparative analysis of items reported under OCI..................................................15

(x) Including comprehensive income to analyse the manager’s performance................15

Accounting for corporate income tax.......................................................................................15

(xi) Reported tax expenses for 2017................................................................................15

(xii) Effective rate of tax...................................................................................................15

(xiii) Deferred tax assets or deferred tax liabilities.........................................................16

(xiv) Increase or decrease in deferred tax assets or liabilities reported by the entities. .16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

(xv) Cash tax.....................................................................................................................17

(xvi) Rate of cash tax......................................................................................................17

(xvii) Difference of cash tax rate from the book tax rate................................................18

Conclusion................................................................................................................................18

Reference..................................................................................................................................19

Appendix..................................................................................................................................21

CORPORATE ACCOUNTING

(xv) Cash tax.....................................................................................................................17

(xvi) Rate of cash tax......................................................................................................17

(xvii) Difference of cash tax rate from the book tax rate................................................18

Conclusion................................................................................................................................18

Reference..................................................................................................................................19

Appendix..................................................................................................................................21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Introduction

Domino’s Pizza Enterprise Limited is involved in operation of the retail foods and

franchise services. Different segments of the company include New Zealand, Australia, Japan

and Europe. The entity is the franchise for Domino’s Pizza brand all over the world. Various

menu served by the company are prawn and chicken pizza, pizza mogul, traditional pizza,

crusts, pizza chefs, chef’s best and gluten free pizza. Further, the customers are availed with

the facility of ordering online. It operates in 7 nations from more than 2000 stores

(Dominos.com.au 2019).

G8 Education Limited is largest child care centre that is listed under ASX and

operates in Australia. The company aims to be the leading provider of the high quality

educational and developmental service centre for child care. The company was established in

the year 2006 and it brought together the team with dedicated professionals that drive high

quality educational and developmental child care services in Australia (G8 Educatio 2019).

Navitas Limited offers the educational services for the professional and students of

Australia, Asia, United Kingdom, Asia, Canada, United States and globally. The company

operates its business through the University partnership, industry segments and careers. The

university partnership segment provides pre-university, university courses and managed

campus. Industry and career segment provides wide range of programs related to higher

education in different fields of the study including film, audio, animation, design and gaming

(Navitas.com 2019).

CORPORATE ACCOUNTING

Introduction

Domino’s Pizza Enterprise Limited is involved in operation of the retail foods and

franchise services. Different segments of the company include New Zealand, Australia, Japan

and Europe. The entity is the franchise for Domino’s Pizza brand all over the world. Various

menu served by the company are prawn and chicken pizza, pizza mogul, traditional pizza,

crusts, pizza chefs, chef’s best and gluten free pizza. Further, the customers are availed with

the facility of ordering online. It operates in 7 nations from more than 2000 stores

(Dominos.com.au 2019).

G8 Education Limited is largest child care centre that is listed under ASX and

operates in Australia. The company aims to be the leading provider of the high quality

educational and developmental service centre for child care. The company was established in

the year 2006 and it brought together the team with dedicated professionals that drive high

quality educational and developmental child care services in Australia (G8 Educatio 2019).

Navitas Limited offers the educational services for the professional and students of

Australia, Asia, United Kingdom, Asia, Canada, United States and globally. The company

operates its business through the University partnership, industry segments and careers. The

university partnership segment provides pre-university, university courses and managed

campus. Industry and career segment provides wide range of programs related to higher

education in different fields of the study including film, audio, animation, design and gaming

(Navitas.com 2019).

5

CORPORATE ACCOUNTING

Equity and liabilities

(i) Equity items

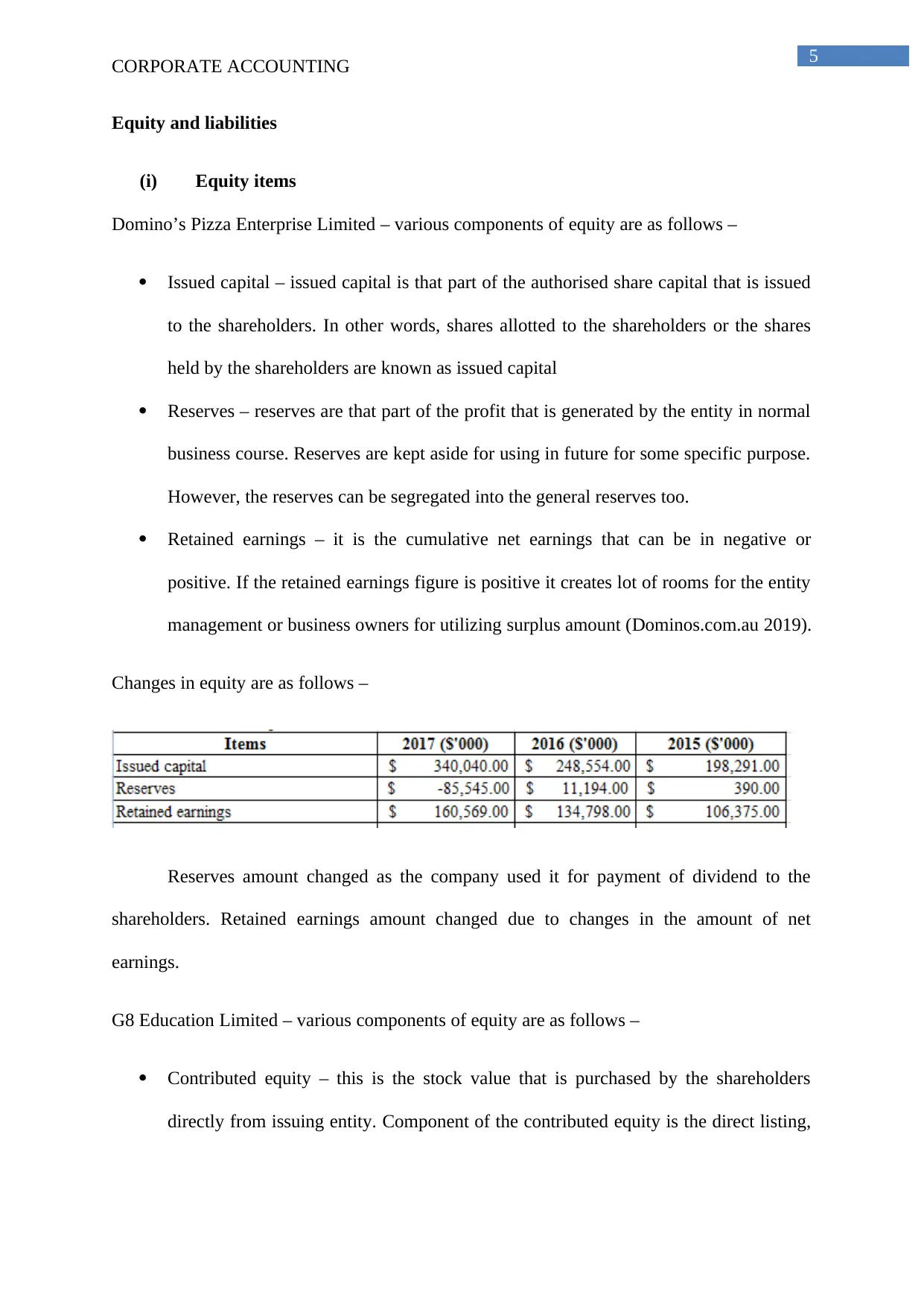

Domino’s Pizza Enterprise Limited – various components of equity are as follows –

Issued capital – issued capital is that part of the authorised share capital that is issued

to the shareholders. In other words, shares allotted to the shareholders or the shares

held by the shareholders are known as issued capital

Reserves – reserves are that part of the profit that is generated by the entity in normal

business course. Reserves are kept aside for using in future for some specific purpose.

However, the reserves can be segregated into the general reserves too.

Retained earnings – it is the cumulative net earnings that can be in negative or

positive. If the retained earnings figure is positive it creates lot of rooms for the entity

management or business owners for utilizing surplus amount (Dominos.com.au 2019).

Changes in equity are as follows –

Reserves amount changed as the company used it for payment of dividend to the

shareholders. Retained earnings amount changed due to changes in the amount of net

earnings.

G8 Education Limited – various components of equity are as follows –

Contributed equity – this is the stock value that is purchased by the shareholders

directly from issuing entity. Component of the contributed equity is the direct listing,

CORPORATE ACCOUNTING

Equity and liabilities

(i) Equity items

Domino’s Pizza Enterprise Limited – various components of equity are as follows –

Issued capital – issued capital is that part of the authorised share capital that is issued

to the shareholders. In other words, shares allotted to the shareholders or the shares

held by the shareholders are known as issued capital

Reserves – reserves are that part of the profit that is generated by the entity in normal

business course. Reserves are kept aside for using in future for some specific purpose.

However, the reserves can be segregated into the general reserves too.

Retained earnings – it is the cumulative net earnings that can be in negative or

positive. If the retained earnings figure is positive it creates lot of rooms for the entity

management or business owners for utilizing surplus amount (Dominos.com.au 2019).

Changes in equity are as follows –

Reserves amount changed as the company used it for payment of dividend to the

shareholders. Retained earnings amount changed due to changes in the amount of net

earnings.

G8 Education Limited – various components of equity are as follows –

Contributed equity – this is the stock value that is purchased by the shareholders

directly from issuing entity. Component of the contributed equity is the direct listing,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

initial public offerings, secondary offerings and direct public offerings and the issues

of the preferred stock (G8 Education 2019).

Reserves – Explained above for Domino’s Pizza Enterprise Limited

Retained earnings – Explained above for Domino’s Pizza Enterprise Limited

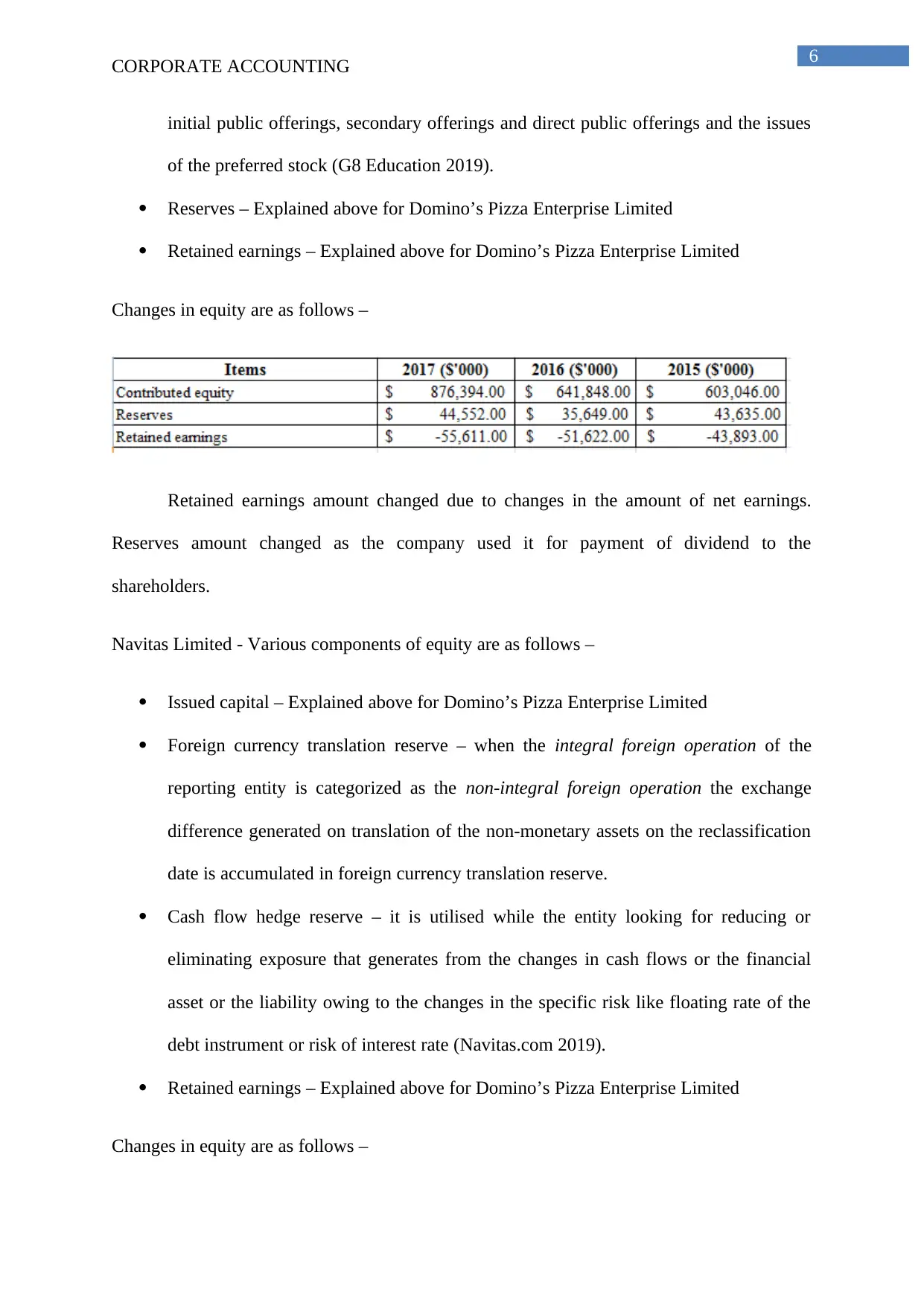

Changes in equity are as follows –

Retained earnings amount changed due to changes in the amount of net earnings.

Reserves amount changed as the company used it for payment of dividend to the

shareholders.

Navitas Limited - Various components of equity are as follows –

Issued capital – Explained above for Domino’s Pizza Enterprise Limited

Foreign currency translation reserve – when the integral foreign operation of the

reporting entity is categorized as the non-integral foreign operation the exchange

difference generated on translation of the non-monetary assets on the reclassification

date is accumulated in foreign currency translation reserve.

Cash flow hedge reserve – it is utilised while the entity looking for reducing or

eliminating exposure that generates from the changes in cash flows or the financial

asset or the liability owing to the changes in the specific risk like floating rate of the

debt instrument or risk of interest rate (Navitas.com 2019).

Retained earnings – Explained above for Domino’s Pizza Enterprise Limited

Changes in equity are as follows –

CORPORATE ACCOUNTING

initial public offerings, secondary offerings and direct public offerings and the issues

of the preferred stock (G8 Education 2019).

Reserves – Explained above for Domino’s Pizza Enterprise Limited

Retained earnings – Explained above for Domino’s Pizza Enterprise Limited

Changes in equity are as follows –

Retained earnings amount changed due to changes in the amount of net earnings.

Reserves amount changed as the company used it for payment of dividend to the

shareholders.

Navitas Limited - Various components of equity are as follows –

Issued capital – Explained above for Domino’s Pizza Enterprise Limited

Foreign currency translation reserve – when the integral foreign operation of the

reporting entity is categorized as the non-integral foreign operation the exchange

difference generated on translation of the non-monetary assets on the reclassification

date is accumulated in foreign currency translation reserve.

Cash flow hedge reserve – it is utilised while the entity looking for reducing or

eliminating exposure that generates from the changes in cash flows or the financial

asset or the liability owing to the changes in the specific risk like floating rate of the

debt instrument or risk of interest rate (Navitas.com 2019).

Retained earnings – Explained above for Domino’s Pizza Enterprise Limited

Changes in equity are as follows –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

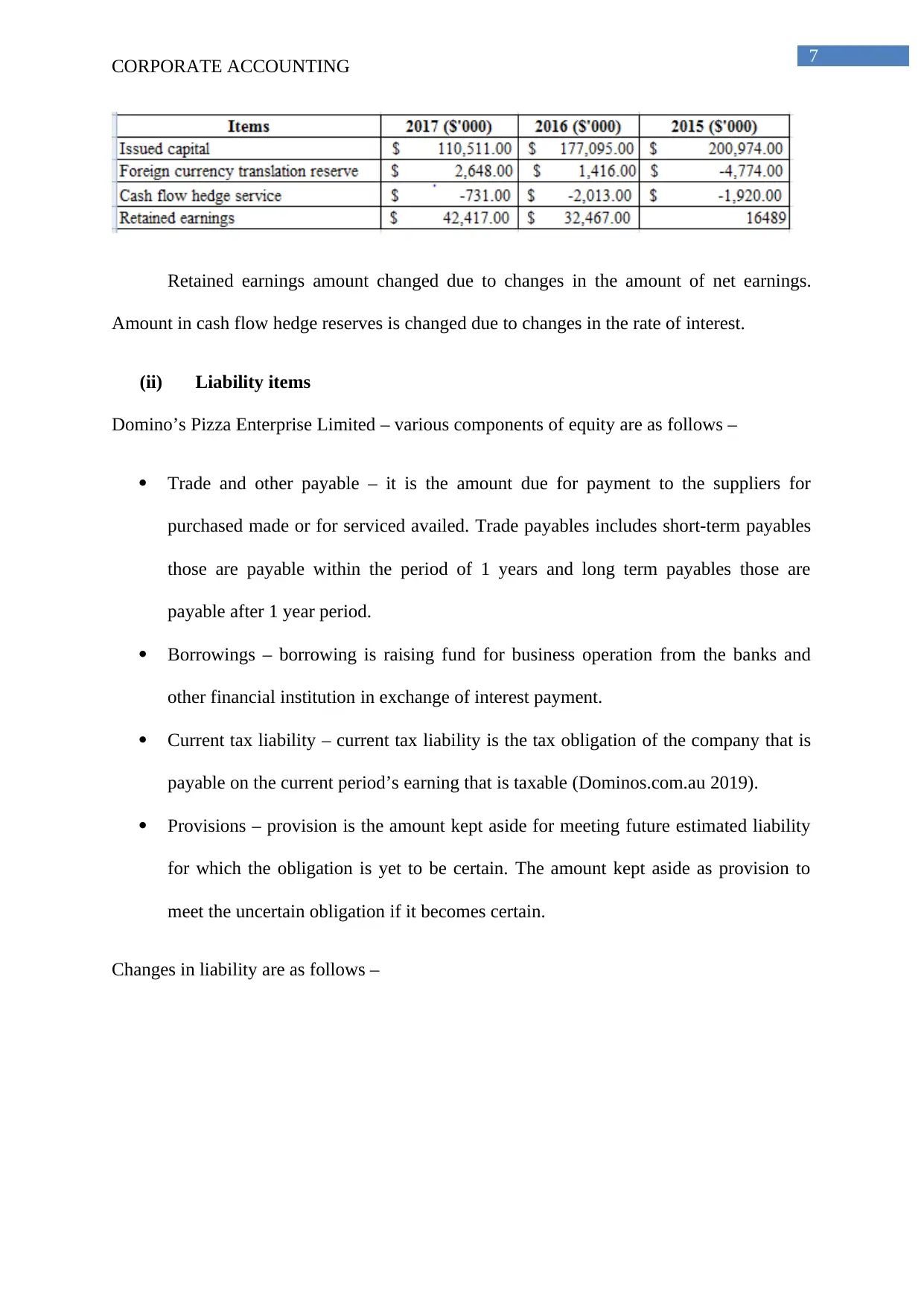

Retained earnings amount changed due to changes in the amount of net earnings.

Amount in cash flow hedge reserves is changed due to changes in the rate of interest.

(ii) Liability items

Domino’s Pizza Enterprise Limited – various components of equity are as follows –

Trade and other payable – it is the amount due for payment to the suppliers for

purchased made or for serviced availed. Trade payables includes short-term payables

those are payable within the period of 1 years and long term payables those are

payable after 1 year period.

Borrowings – borrowing is raising fund for business operation from the banks and

other financial institution in exchange of interest payment.

Current tax liability – current tax liability is the tax obligation of the company that is

payable on the current period’s earning that is taxable (Dominos.com.au 2019).

Provisions – provision is the amount kept aside for meeting future estimated liability

for which the obligation is yet to be certain. The amount kept aside as provision to

meet the uncertain obligation if it becomes certain.

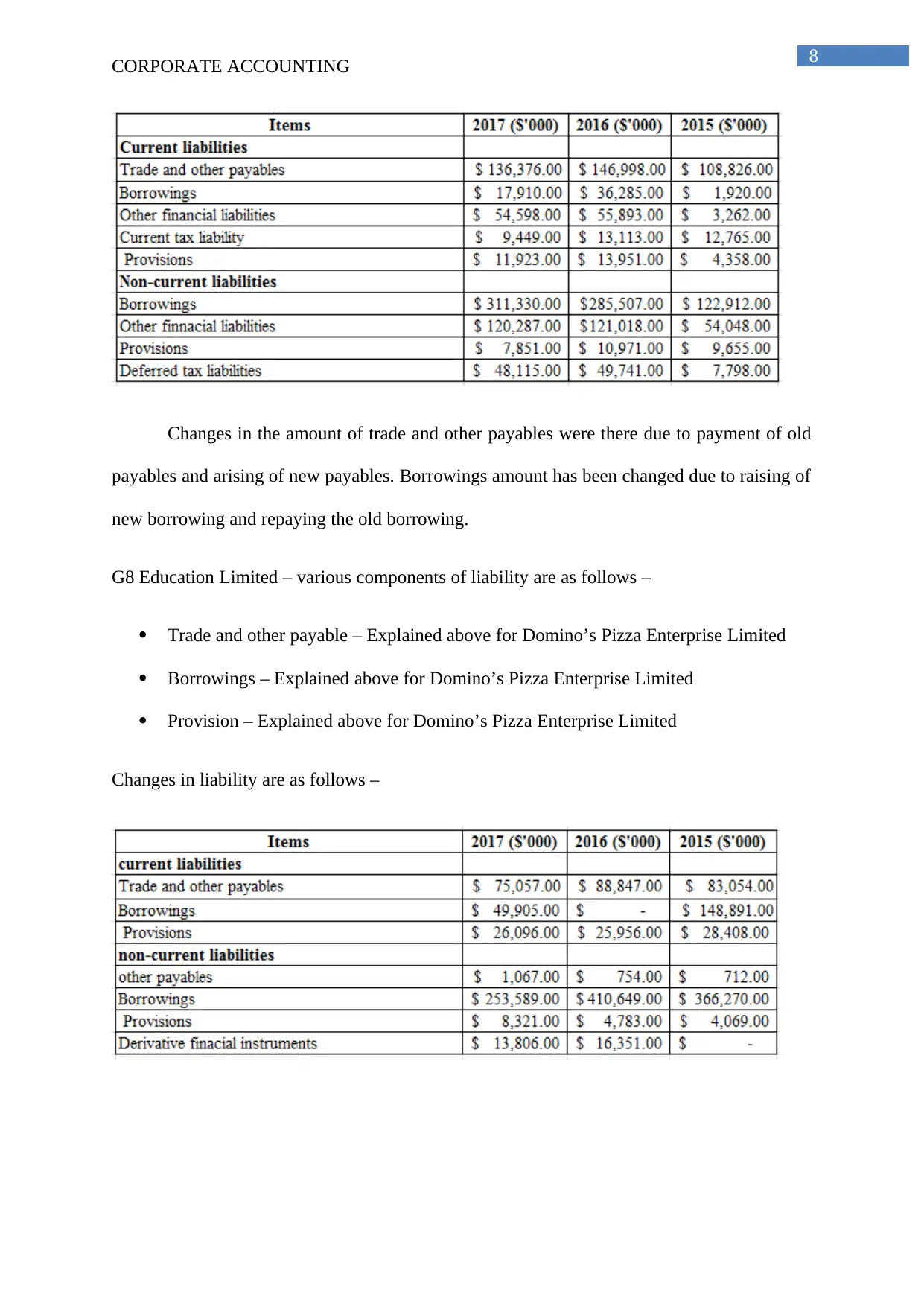

Changes in liability are as follows –

CORPORATE ACCOUNTING

Retained earnings amount changed due to changes in the amount of net earnings.

Amount in cash flow hedge reserves is changed due to changes in the rate of interest.

(ii) Liability items

Domino’s Pizza Enterprise Limited – various components of equity are as follows –

Trade and other payable – it is the amount due for payment to the suppliers for

purchased made or for serviced availed. Trade payables includes short-term payables

those are payable within the period of 1 years and long term payables those are

payable after 1 year period.

Borrowings – borrowing is raising fund for business operation from the banks and

other financial institution in exchange of interest payment.

Current tax liability – current tax liability is the tax obligation of the company that is

payable on the current period’s earning that is taxable (Dominos.com.au 2019).

Provisions – provision is the amount kept aside for meeting future estimated liability

for which the obligation is yet to be certain. The amount kept aside as provision to

meet the uncertain obligation if it becomes certain.

Changes in liability are as follows –

8

CORPORATE ACCOUNTING

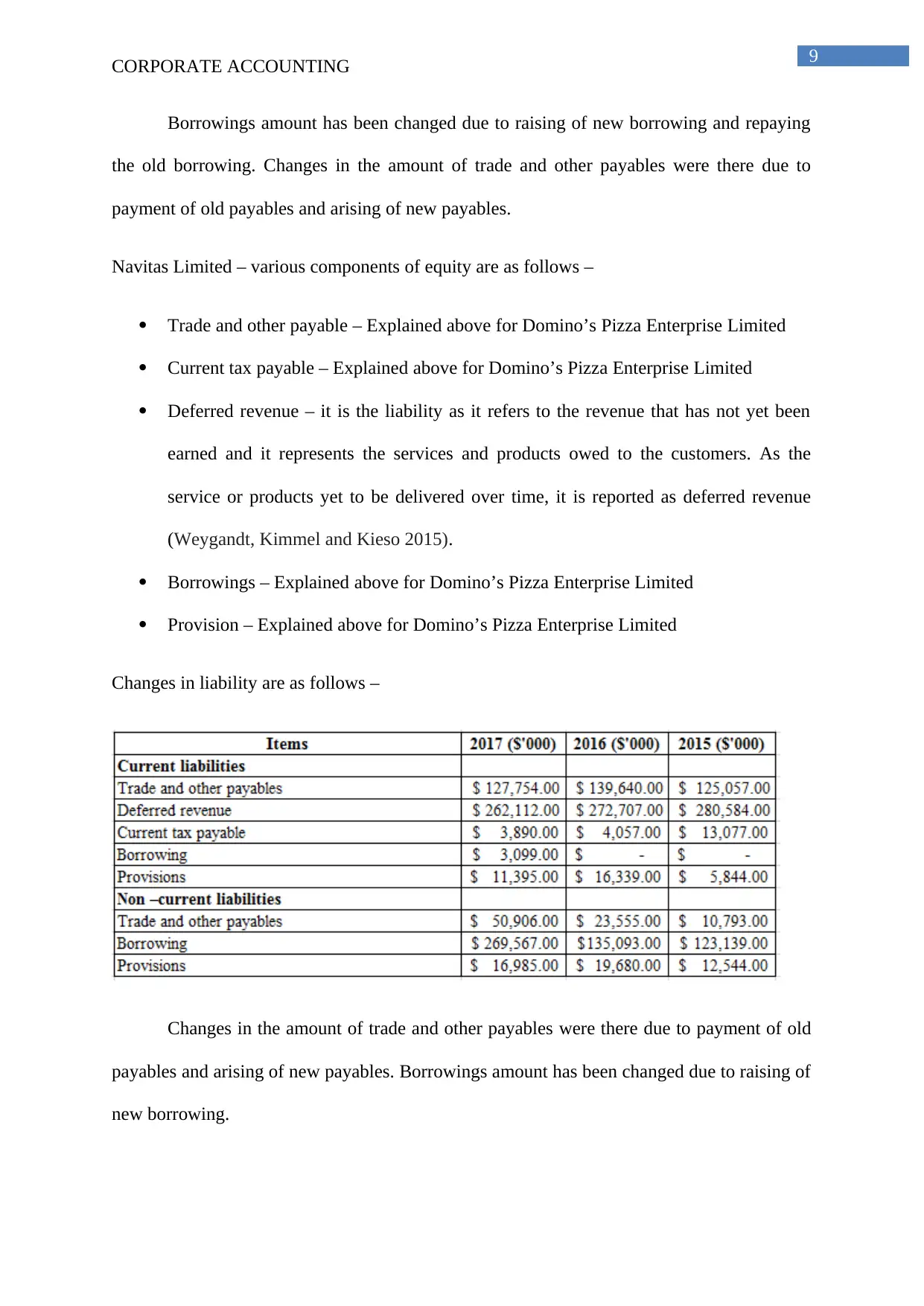

Changes in the amount of trade and other payables were there due to payment of old

payables and arising of new payables. Borrowings amount has been changed due to raising of

new borrowing and repaying the old borrowing.

G8 Education Limited – various components of liability are as follows –

Trade and other payable – Explained above for Domino’s Pizza Enterprise Limited

Borrowings – Explained above for Domino’s Pizza Enterprise Limited

Provision – Explained above for Domino’s Pizza Enterprise Limited

Changes in liability are as follows –

CORPORATE ACCOUNTING

Changes in the amount of trade and other payables were there due to payment of old

payables and arising of new payables. Borrowings amount has been changed due to raising of

new borrowing and repaying the old borrowing.

G8 Education Limited – various components of liability are as follows –

Trade and other payable – Explained above for Domino’s Pizza Enterprise Limited

Borrowings – Explained above for Domino’s Pizza Enterprise Limited

Provision – Explained above for Domino’s Pizza Enterprise Limited

Changes in liability are as follows –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Borrowings amount has been changed due to raising of new borrowing and repaying

the old borrowing. Changes in the amount of trade and other payables were there due to

payment of old payables and arising of new payables.

Navitas Limited – various components of equity are as follows –

Trade and other payable – Explained above for Domino’s Pizza Enterprise Limited

Current tax payable – Explained above for Domino’s Pizza Enterprise Limited

Deferred revenue – it is the liability as it refers to the revenue that has not yet been

earned and it represents the services and products owed to the customers. As the

service or products yet to be delivered over time, it is reported as deferred revenue

(Weygandt, Kimmel and Kieso 2015).

Borrowings – Explained above for Domino’s Pizza Enterprise Limited

Provision – Explained above for Domino’s Pizza Enterprise Limited

Changes in liability are as follows –

Changes in the amount of trade and other payables were there due to payment of old

payables and arising of new payables. Borrowings amount has been changed due to raising of

new borrowing.

CORPORATE ACCOUNTING

Borrowings amount has been changed due to raising of new borrowing and repaying

the old borrowing. Changes in the amount of trade and other payables were there due to

payment of old payables and arising of new payables.

Navitas Limited – various components of equity are as follows –

Trade and other payable – Explained above for Domino’s Pizza Enterprise Limited

Current tax payable – Explained above for Domino’s Pizza Enterprise Limited

Deferred revenue – it is the liability as it refers to the revenue that has not yet been

earned and it represents the services and products owed to the customers. As the

service or products yet to be delivered over time, it is reported as deferred revenue

(Weygandt, Kimmel and Kieso 2015).

Borrowings – Explained above for Domino’s Pizza Enterprise Limited

Provision – Explained above for Domino’s Pizza Enterprise Limited

Changes in liability are as follows –

Changes in the amount of trade and other payables were there due to payment of old

payables and arising of new payables. Borrowings amount has been changed due to raising of

new borrowing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

(iii) Comparative analysis of debt and equity position

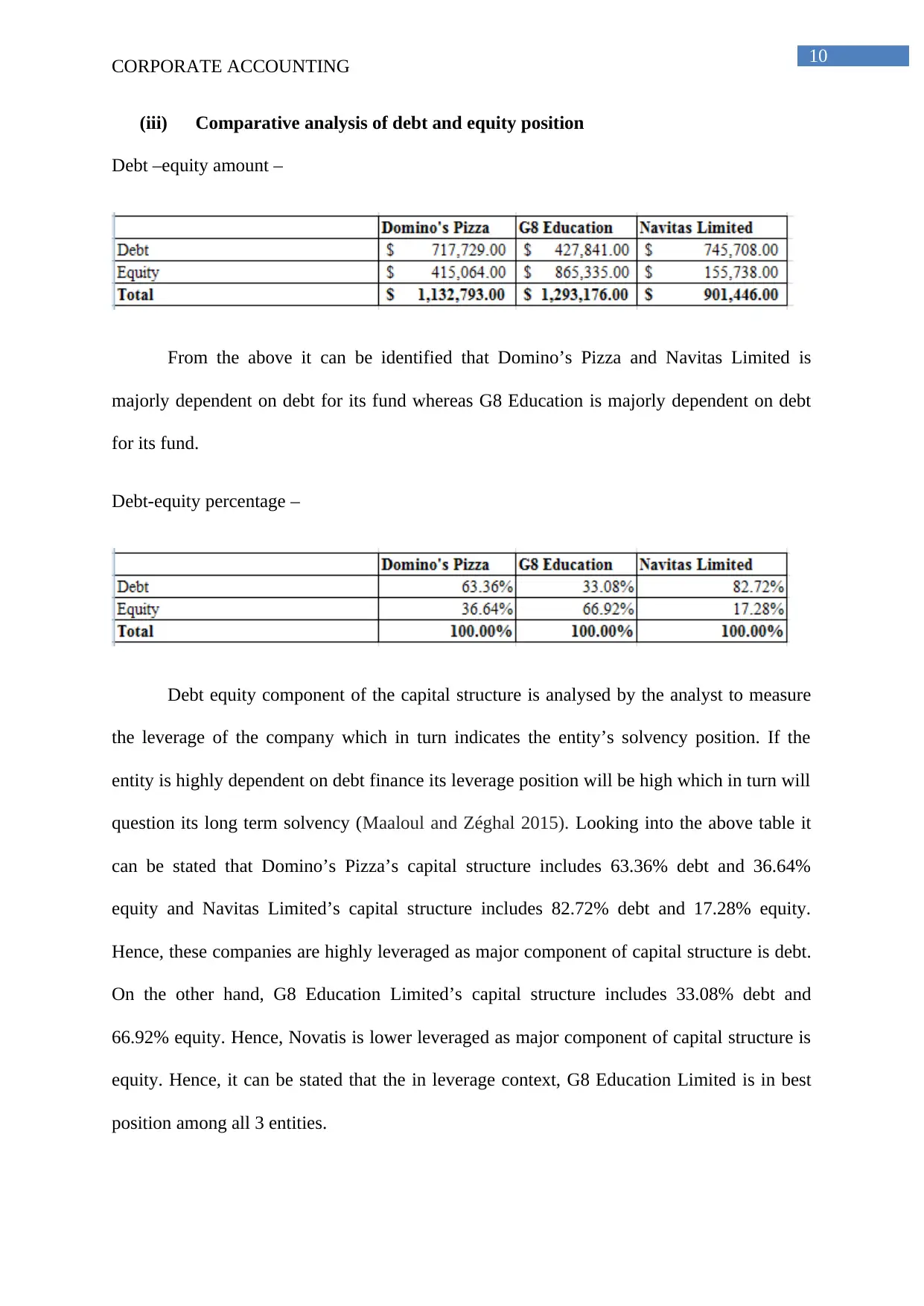

Debt –equity amount –

From the above it can be identified that Domino’s Pizza and Navitas Limited is

majorly dependent on debt for its fund whereas G8 Education is majorly dependent on debt

for its fund.

Debt-equity percentage –

Debt equity component of the capital structure is analysed by the analyst to measure

the leverage of the company which in turn indicates the entity’s solvency position. If the

entity is highly dependent on debt finance its leverage position will be high which in turn will

question its long term solvency (Maaloul and Zéghal 2015). Looking into the above table it

can be stated that Domino’s Pizza’s capital structure includes 63.36% debt and 36.64%

equity and Navitas Limited’s capital structure includes 82.72% debt and 17.28% equity.

Hence, these companies are highly leveraged as major component of capital structure is debt.

On the other hand, G8 Education Limited’s capital structure includes 33.08% debt and

66.92% equity. Hence, Novatis is lower leveraged as major component of capital structure is

equity. Hence, it can be stated that the in leverage context, G8 Education Limited is in best

position among all 3 entities.

CORPORATE ACCOUNTING

(iii) Comparative analysis of debt and equity position

Debt –equity amount –

From the above it can be identified that Domino’s Pizza and Navitas Limited is

majorly dependent on debt for its fund whereas G8 Education is majorly dependent on debt

for its fund.

Debt-equity percentage –

Debt equity component of the capital structure is analysed by the analyst to measure

the leverage of the company which in turn indicates the entity’s solvency position. If the

entity is highly dependent on debt finance its leverage position will be high which in turn will

question its long term solvency (Maaloul and Zéghal 2015). Looking into the above table it

can be stated that Domino’s Pizza’s capital structure includes 63.36% debt and 36.64%

equity and Navitas Limited’s capital structure includes 82.72% debt and 17.28% equity.

Hence, these companies are highly leveraged as major component of capital structure is debt.

On the other hand, G8 Education Limited’s capital structure includes 33.08% debt and

66.92% equity. Hence, Novatis is lower leveraged as major component of capital structure is

equity. Hence, it can be stated that the in leverage context, G8 Education Limited is in best

position among all 3 entities.

11

CORPORATE ACCOUNTING

Cash flow statement

(iv) Listed items for cash flow

Cash flow statement of all the entities selected above are segregated into 3 segments – cash

generated or used for operation, cash generated or used for investing and cash generated or

used for financing. Cash flow statement as a whole represents the cash position of the entity

that is the amount of cash generated and used during the specific period of time (Marshall

2016). Detail explanation of each segment is as follows –

Cash generated or used for operation – it represents the net cash flows reported in the

1st section of the cash flow statement. This section focuses on the cash generated or

used from the core activities of the entity and includes adjustments for the non-cash

expenses like depreciation, adjustments for changes in working capital, money

received from customers and money paid to suppliers.

Cash generated or used for investing - it represents the net cash flows reported in the

2nd section of the cash flow statement. This section focuses on the cash generated or

used for purchasing long term and fixed assets like plant, equipment and property and

the proceeds received from selling of the long term and fixed assets (Watson 2015).

Cash generated or used for financing – it represents the net cash flows reported in the

2nd section of the cash flow statement. This section focuses on the cash generated or

used for repurchasing of company stocks, payment of the dividends, repayment of the

debt, sale of the stocks and issuance of debts like bonds.

Changes for the cash flows statement items –

Domino’s Pizza Enterprise Limited – cash from operation for the entity has been increased

from $ 128,472 thousand. Increase was due to the amount received from the customers.

Amount used for investing activities reduced from $ 263,968 thousand to $ 88,260 thousand.

CORPORATE ACCOUNTING

Cash flow statement

(iv) Listed items for cash flow

Cash flow statement of all the entities selected above are segregated into 3 segments – cash

generated or used for operation, cash generated or used for investing and cash generated or

used for financing. Cash flow statement as a whole represents the cash position of the entity

that is the amount of cash generated and used during the specific period of time (Marshall

2016). Detail explanation of each segment is as follows –

Cash generated or used for operation – it represents the net cash flows reported in the

1st section of the cash flow statement. This section focuses on the cash generated or

used from the core activities of the entity and includes adjustments for the non-cash

expenses like depreciation, adjustments for changes in working capital, money

received from customers and money paid to suppliers.

Cash generated or used for investing - it represents the net cash flows reported in the

2nd section of the cash flow statement. This section focuses on the cash generated or

used for purchasing long term and fixed assets like plant, equipment and property and

the proceeds received from selling of the long term and fixed assets (Watson 2015).

Cash generated or used for financing – it represents the net cash flows reported in the

2nd section of the cash flow statement. This section focuses on the cash generated or

used for repurchasing of company stocks, payment of the dividends, repayment of the

debt, sale of the stocks and issuance of debts like bonds.

Changes for the cash flows statement items –

Domino’s Pizza Enterprise Limited – cash from operation for the entity has been increased

from $ 128,472 thousand. Increase was due to the amount received from the customers.

Amount used for investing activities reduced from $ 263,968 thousand to $ 88,260 thousand.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.