ATH Technologies Case Study: Performance, Management & Control

VerifiedAdded on 2023/06/15

|13

|2830

|156

Case Study

AI Summary

This document presents a comprehensive analysis of the ATH Technologies case study, focusing on the evolution of the company's performance management and control systems across different phases: founding, growth, push to profitability, refocus on process, and new management. The analysis covers key aspects such as the effectiveness of the earn-out structure, communication and motivation strategies for employees, financial measures for performance assessment, and the role of control systems in both the company's successes and failures. It also addresses critical issues like avoiding FDA investigations, managing company reputation, and scanning the competitive environment. The study further evaluates the decision of Scepter to purchase ATH's technologies, and how the new management can use control systems to implement their agenda and ensure future success. The document provides detailed recommendations for improving performance management, setting goals, and mitigating risks.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. FOUNDING........................................................................................................................1

1. Does the earn out structure focus on the right performance goals.....................................1

a) Should Scepter pharmaceutical put additional controls on this entrepreneurial firm?.......1

2. from the perspective of president of ATH technologies, how would you communicate

and motivate employees to achieve profit and performance goals.........................................2

a) What are the appropriate performance goals for employees to focus on?.........................2

b) How would you communicate and control events and employee actions that could put

business objectives at risk?.....................................................................................................2

3. Explain the best financial measures to assess ATH technologies’ performance and why?

................................................................................................................................................2

2. GROWTH PHASE: 2011-2012.............................................................................................3

1. How would you evaluate the performance of ATH technologies during the growth

period?....................................................................................................................................3

2. What is the strategy of the business?..................................................................................4

3. How should performance be measured and analyzed?.......................................................4

a) Which additional measures would you use to implement the strategy?.............................5

b) What are the characteristics of a good measure?...............................................................5

4. As a president of ATH technologies, what would you do to focus on the attention and

efforts of your employees?.....................................................................................................5

3. Push to Profitability................................................................................................................5

1. How did managers at ATH technologies achieve their profit and performance goals

during 2013?...........................................................................................................................5

a) What role did control systems play in ATH’s success and problems?..............................5

b) How could top management have avoided the actions by employees that led to the FDA

investigation?..........................................................................................................................5

c) What are the possible consequences of these events on the company’s reputation?.........5

2. If you were the president of ATH, what would you do to get the business back on track?

................................................................................................................................................6

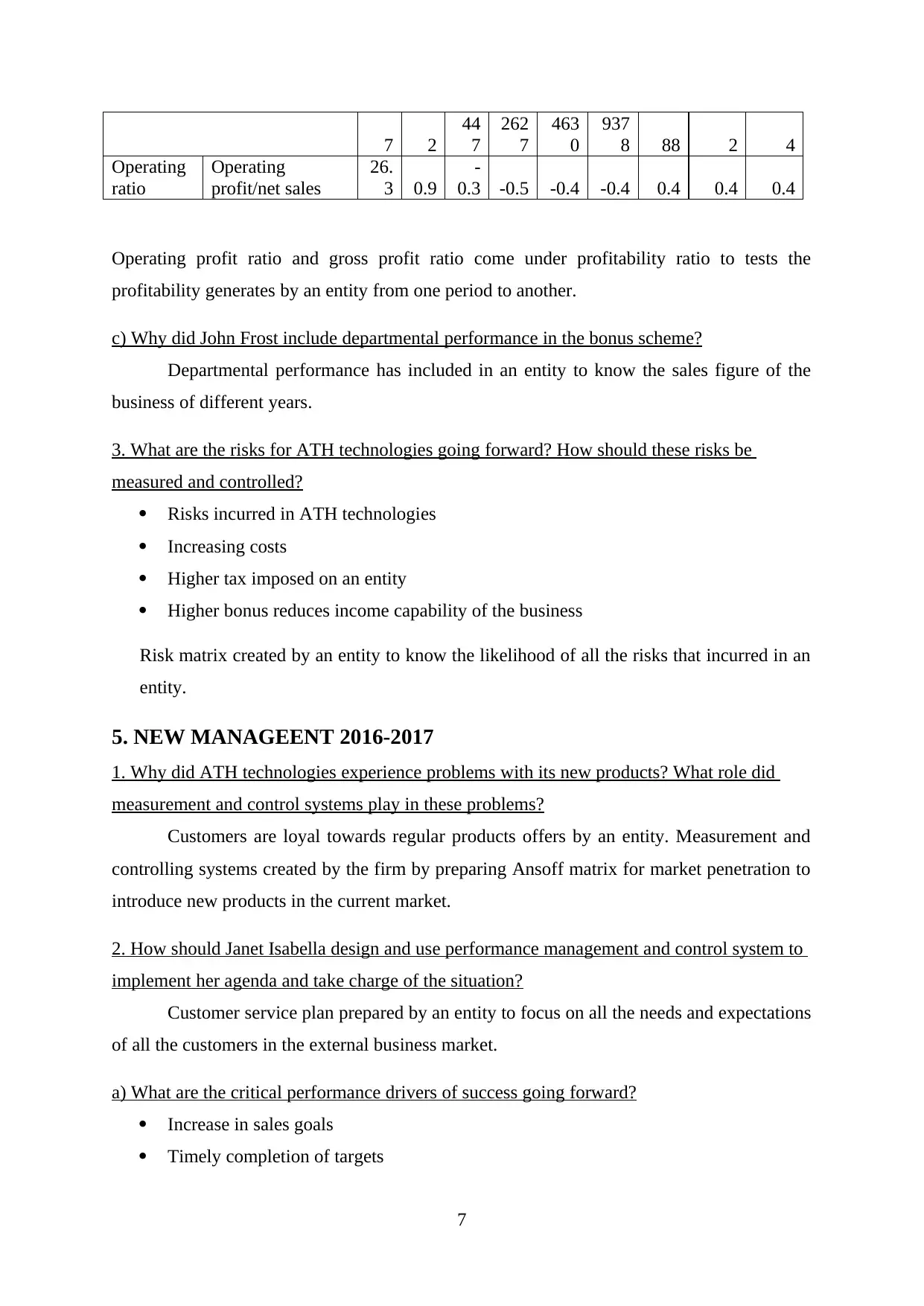

4. REFOCUS ON PROCESS: 2014-2015.................................................................................6

1. Why did senior managers introduce a vision and belief statement?..................................6

2. Why did managers at ATH Technologies change their performance measures?...............6

a) John Frost includes both process and output measures. Why? What is he trying to

accomplish?............................................................................................................................6

1. FOUNDING........................................................................................................................1

1. Does the earn out structure focus on the right performance goals.....................................1

a) Should Scepter pharmaceutical put additional controls on this entrepreneurial firm?.......1

2. from the perspective of president of ATH technologies, how would you communicate

and motivate employees to achieve profit and performance goals.........................................2

a) What are the appropriate performance goals for employees to focus on?.........................2

b) How would you communicate and control events and employee actions that could put

business objectives at risk?.....................................................................................................2

3. Explain the best financial measures to assess ATH technologies’ performance and why?

................................................................................................................................................2

2. GROWTH PHASE: 2011-2012.............................................................................................3

1. How would you evaluate the performance of ATH technologies during the growth

period?....................................................................................................................................3

2. What is the strategy of the business?..................................................................................4

3. How should performance be measured and analyzed?.......................................................4

a) Which additional measures would you use to implement the strategy?.............................5

b) What are the characteristics of a good measure?...............................................................5

4. As a president of ATH technologies, what would you do to focus on the attention and

efforts of your employees?.....................................................................................................5

3. Push to Profitability................................................................................................................5

1. How did managers at ATH technologies achieve their profit and performance goals

during 2013?...........................................................................................................................5

a) What role did control systems play in ATH’s success and problems?..............................5

b) How could top management have avoided the actions by employees that led to the FDA

investigation?..........................................................................................................................5

c) What are the possible consequences of these events on the company’s reputation?.........5

2. If you were the president of ATH, what would you do to get the business back on track?

................................................................................................................................................6

4. REFOCUS ON PROCESS: 2014-2015.................................................................................6

1. Why did senior managers introduce a vision and belief statement?..................................6

2. Why did managers at ATH Technologies change their performance measures?...............6

a) John Frost includes both process and output measures. Why? What is he trying to

accomplish?............................................................................................................................6

b) He also includes ratio and ordinal measures. What are the advantages and issues of each

type?.......................................................................................................................................6

c) Why did John Frost include departmental performance in the bonus scheme?.................7

3. What are the risks for ATH technologies going forward? How should these risks be

measured and controlled?.......................................................................................................7

5. NEW MANAGEENT 2016-2017..........................................................................................7

1. Why did ATH technologies experience problems with its new products? What role did

measurement and control systems play in these problems?...................................................7

2. How should Janet Isabella design and use performance management and control system

to implement her agenda and take charge of the situation?....................................................7

a) What are the critical performance drivers of success going forward?...............................7

b) What variables should be measured?.................................................................................7

c) How easy or difficult should goals be?..............................................................................8

d) How should financial expectations be set and communicated?.........................................8

3. How can Janet Isabella use control systems to scan the competitive environment to

ensure that the business is not again surpassed by new technology?.....................................8

4. What events or employee actions could put business objectives at risk? How would you

ensure that these risks are adequately communicated and controlled?..................................8

5. How would you measure and evaluate Scepter’s decision to purchase ATH’s

technologies in 2011?.............................................................................................................8

REFERENCES...........................................................................................................................9

3

type?.......................................................................................................................................6

c) Why did John Frost include departmental performance in the bonus scheme?.................7

3. What are the risks for ATH technologies going forward? How should these risks be

measured and controlled?.......................................................................................................7

5. NEW MANAGEENT 2016-2017..........................................................................................7

1. Why did ATH technologies experience problems with its new products? What role did

measurement and control systems play in these problems?...................................................7

2. How should Janet Isabella design and use performance management and control system

to implement her agenda and take charge of the situation?....................................................7

a) What are the critical performance drivers of success going forward?...............................7

b) What variables should be measured?.................................................................................7

c) How easy or difficult should goals be?..............................................................................8

d) How should financial expectations be set and communicated?.........................................8

3. How can Janet Isabella use control systems to scan the competitive environment to

ensure that the business is not again surpassed by new technology?.....................................8

4. What events or employee actions could put business objectives at risk? How would you

ensure that these risks are adequately communicated and controlled?..................................8

5. How would you measure and evaluate Scepter’s decision to purchase ATH’s

technologies in 2011?.............................................................................................................8

REFERENCES...........................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

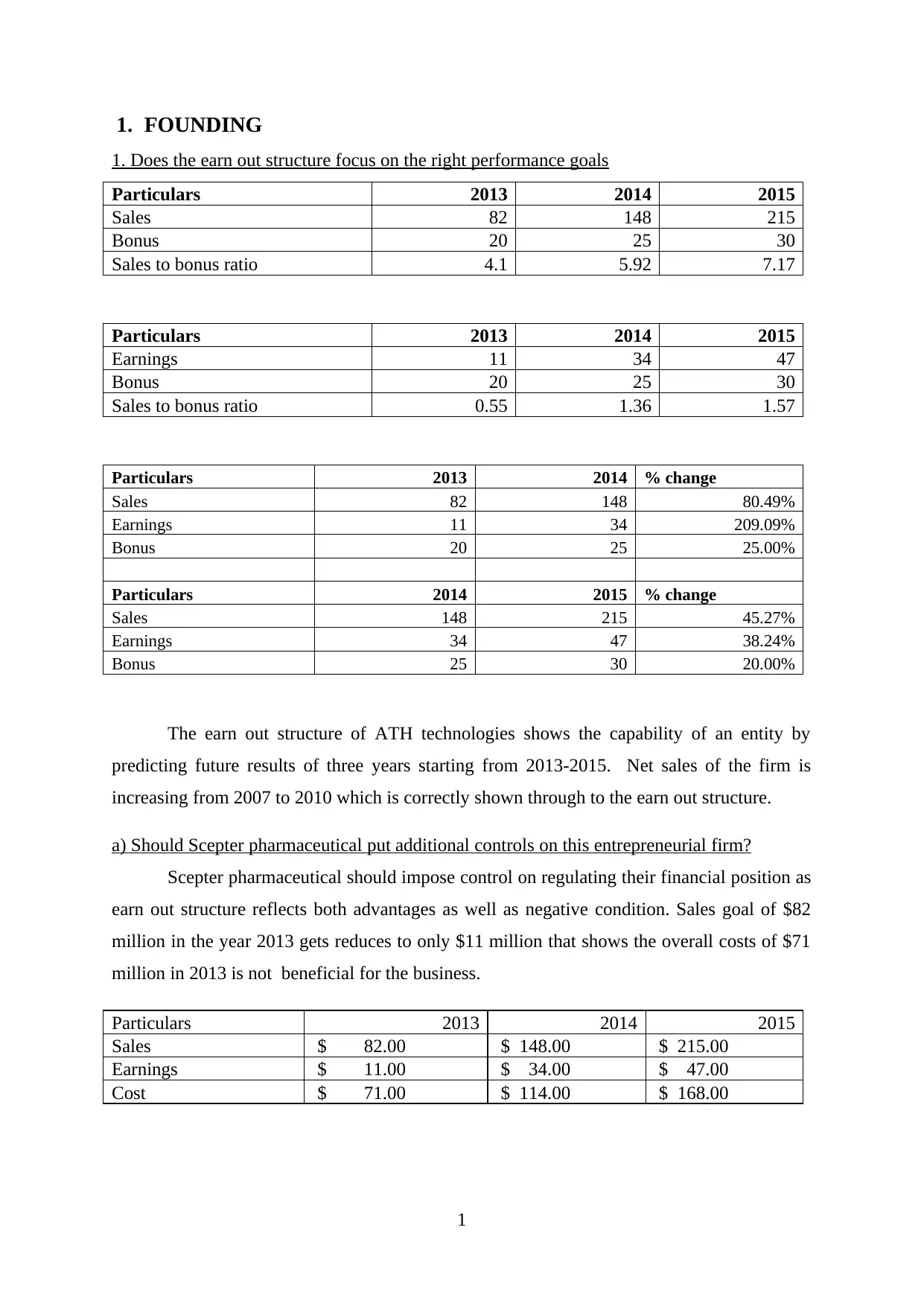

1. FOUNDING

1. Does the earn out structure focus on the right performance goals

Particulars 2013 2014 2015

Sales 82 148 215

Bonus 20 25 30

Sales to bonus ratio 4.1 5.92 7.17

Particulars 2013 2014 2015

Earnings 11 34 47

Bonus 20 25 30

Sales to bonus ratio 0.55 1.36 1.57

Particulars 2013 2014 % change

Sales 82 148 80.49%

Earnings 11 34 209.09%

Bonus 20 25 25.00%

Particulars 2014 2015 % change

Sales 148 215 45.27%

Earnings 34 47 38.24%

Bonus 25 30 20.00%

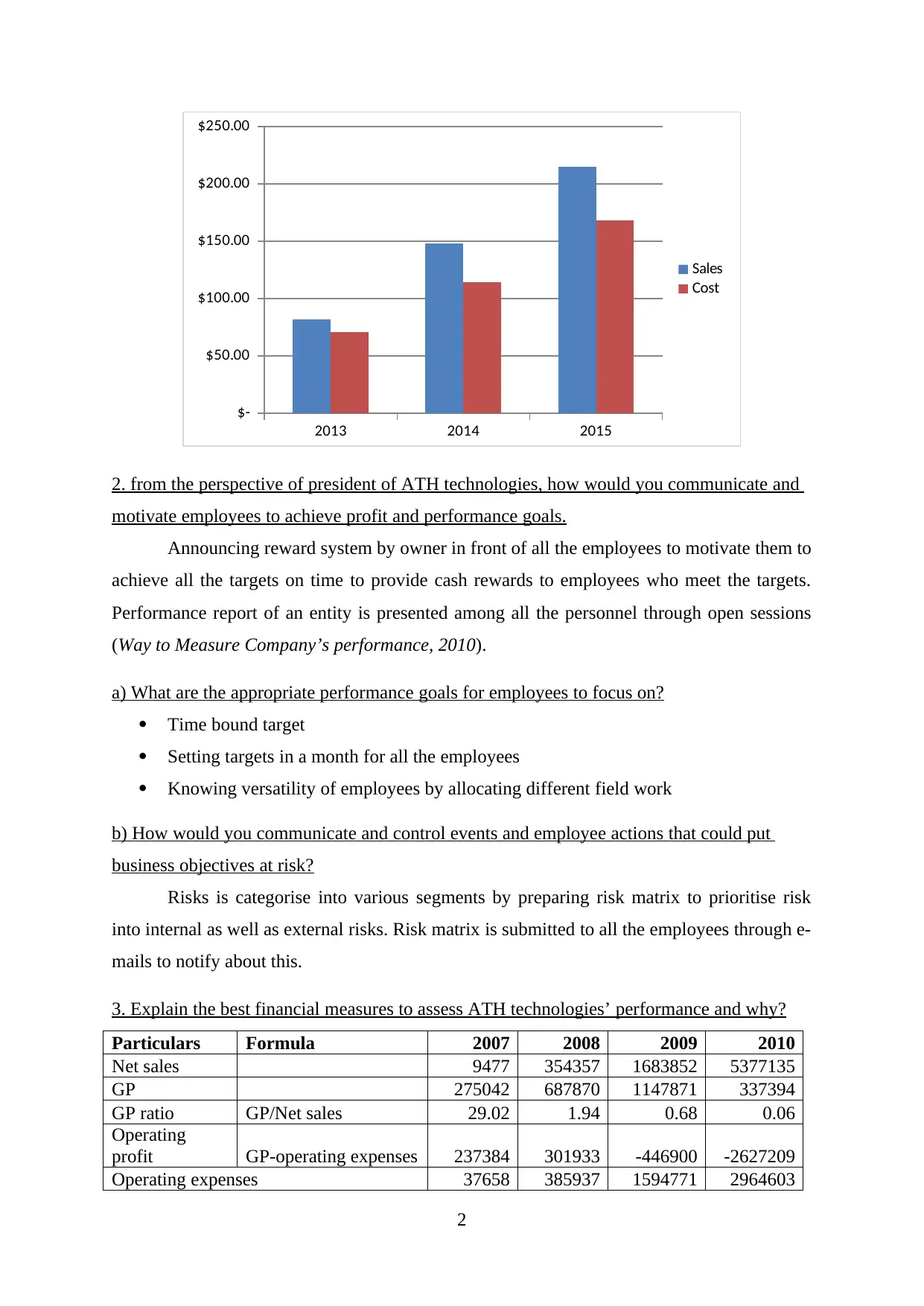

The earn out structure of ATH technologies shows the capability of an entity by

predicting future results of three years starting from 2013-2015. Net sales of the firm is

increasing from 2007 to 2010 which is correctly shown through to the earn out structure.

a) Should Scepter pharmaceutical put additional controls on this entrepreneurial firm?

Scepter pharmaceutical should impose control on regulating their financial position as

earn out structure reflects both advantages as well as negative condition. Sales goal of $82

million in the year 2013 gets reduces to only $11 million that shows the overall costs of $71

million in 2013 is not beneficial for the business.

Particulars 2013 2014 2015

Sales $ 82.00 $ 148.00 $ 215.00

Earnings $ 11.00 $ 34.00 $ 47.00

Cost $ 71.00 $ 114.00 $ 168.00

1

1. Does the earn out structure focus on the right performance goals

Particulars 2013 2014 2015

Sales 82 148 215

Bonus 20 25 30

Sales to bonus ratio 4.1 5.92 7.17

Particulars 2013 2014 2015

Earnings 11 34 47

Bonus 20 25 30

Sales to bonus ratio 0.55 1.36 1.57

Particulars 2013 2014 % change

Sales 82 148 80.49%

Earnings 11 34 209.09%

Bonus 20 25 25.00%

Particulars 2014 2015 % change

Sales 148 215 45.27%

Earnings 34 47 38.24%

Bonus 25 30 20.00%

The earn out structure of ATH technologies shows the capability of an entity by

predicting future results of three years starting from 2013-2015. Net sales of the firm is

increasing from 2007 to 2010 which is correctly shown through to the earn out structure.

a) Should Scepter pharmaceutical put additional controls on this entrepreneurial firm?

Scepter pharmaceutical should impose control on regulating their financial position as

earn out structure reflects both advantages as well as negative condition. Sales goal of $82

million in the year 2013 gets reduces to only $11 million that shows the overall costs of $71

million in 2013 is not beneficial for the business.

Particulars 2013 2014 2015

Sales $ 82.00 $ 148.00 $ 215.00

Earnings $ 11.00 $ 34.00 $ 47.00

Cost $ 71.00 $ 114.00 $ 168.00

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 2014 2015

$-

$50.00

$100.00

$150.00

$200.00

$250.00

Sales

Cost

2. from the perspective of president of ATH technologies, how would you communicate and

motivate employees to achieve profit and performance goals.

Announcing reward system by owner in front of all the employees to motivate them to

achieve all the targets on time to provide cash rewards to employees who meet the targets.

Performance report of an entity is presented among all the personnel through open sessions

(Way to Measure Company’s performance, 2010).

a) What are the appropriate performance goals for employees to focus on?

Time bound target

Setting targets in a month for all the employees

Knowing versatility of employees by allocating different field work

b) How would you communicate and control events and employee actions that could put

business objectives at risk?

Risks is categorise into various segments by preparing risk matrix to prioritise risk

into internal as well as external risks. Risk matrix is submitted to all the employees through e-

mails to notify about this.

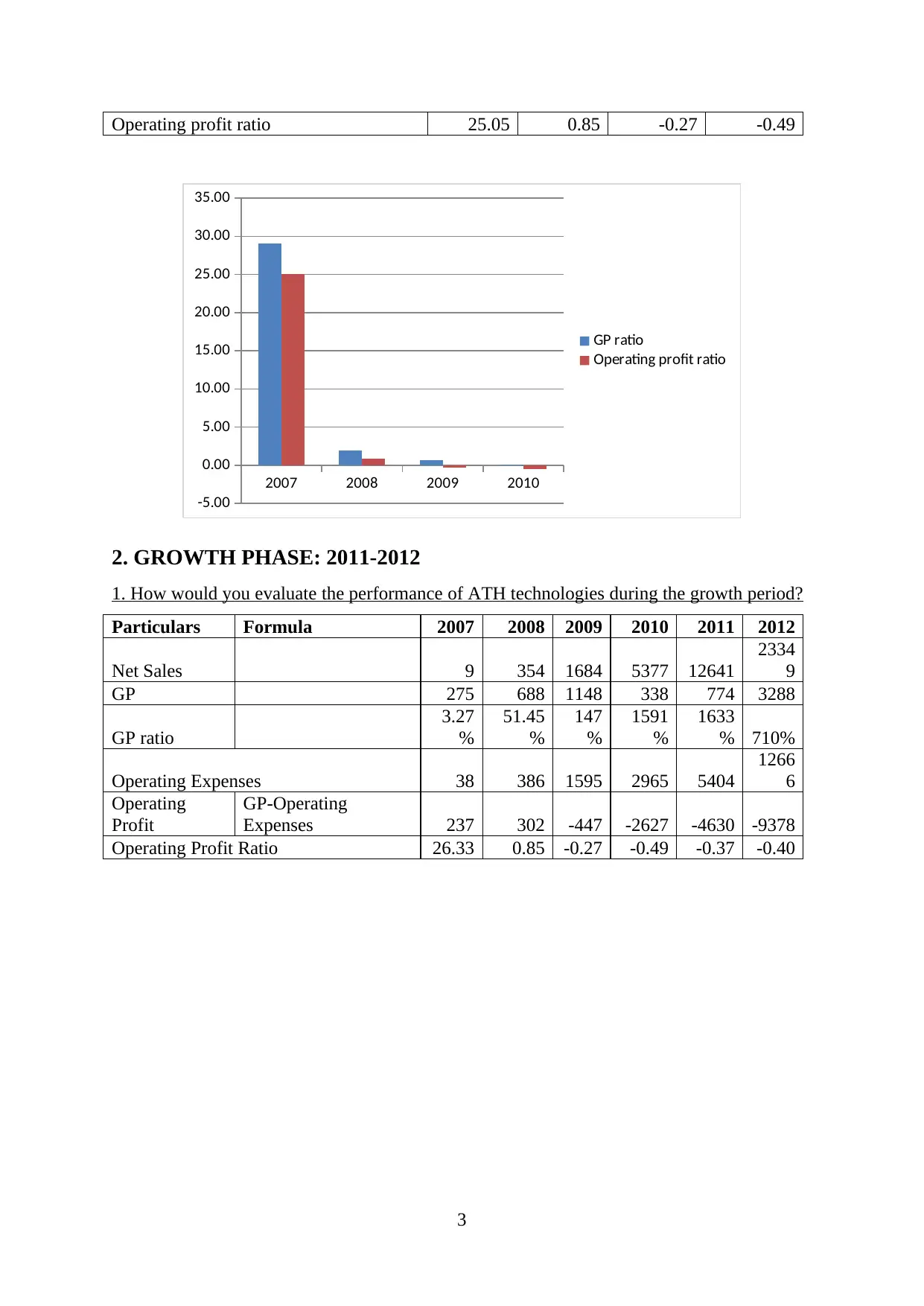

3. Explain the best financial measures to assess ATH technologies’ performance and why?

Particulars Formula 2007 2008 2009 2010

Net sales 9477 354357 1683852 5377135

GP 275042 687870 1147871 337394

GP ratio GP/Net sales 29.02 1.94 0.68 0.06

Operating

profit GP-operating expenses 237384 301933 -446900 -2627209

Operating expenses 37658 385937 1594771 2964603

2

$-

$50.00

$100.00

$150.00

$200.00

$250.00

Sales

Cost

2. from the perspective of president of ATH technologies, how would you communicate and

motivate employees to achieve profit and performance goals.

Announcing reward system by owner in front of all the employees to motivate them to

achieve all the targets on time to provide cash rewards to employees who meet the targets.

Performance report of an entity is presented among all the personnel through open sessions

(Way to Measure Company’s performance, 2010).

a) What are the appropriate performance goals for employees to focus on?

Time bound target

Setting targets in a month for all the employees

Knowing versatility of employees by allocating different field work

b) How would you communicate and control events and employee actions that could put

business objectives at risk?

Risks is categorise into various segments by preparing risk matrix to prioritise risk

into internal as well as external risks. Risk matrix is submitted to all the employees through e-

mails to notify about this.

3. Explain the best financial measures to assess ATH technologies’ performance and why?

Particulars Formula 2007 2008 2009 2010

Net sales 9477 354357 1683852 5377135

GP 275042 687870 1147871 337394

GP ratio GP/Net sales 29.02 1.94 0.68 0.06

Operating

profit GP-operating expenses 237384 301933 -446900 -2627209

Operating expenses 37658 385937 1594771 2964603

2

Operating profit ratio 25.05 0.85 -0.27 -0.49

2007 2008 2009 2010

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

GP ratio

Operating profit ratio

2. GROWTH PHASE: 2011-2012

1. How would you evaluate the performance of ATH technologies during the growth period?

Particulars Formula 2007 2008 2009 2010 2011 2012

Net Sales 9 354 1684 5377 12641

2334

9

GP 275 688 1148 338 774 3288

GP ratio

3.27

%

51.45

%

147

%

1591

%

1633

% 710%

Operating Expenses 38 386 1595 2965 5404

1266

6

Operating

Profit

GP-Operating

Expenses 237 302 -447 -2627 -4630 -9378

Operating Profit Ratio 26.33 0.85 -0.27 -0.49 -0.37 -0.40

3

2007 2008 2009 2010

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

GP ratio

Operating profit ratio

2. GROWTH PHASE: 2011-2012

1. How would you evaluate the performance of ATH technologies during the growth period?

Particulars Formula 2007 2008 2009 2010 2011 2012

Net Sales 9 354 1684 5377 12641

2334

9

GP 275 688 1148 338 774 3288

GP ratio

3.27

%

51.45

%

147

%

1591

%

1633

% 710%

Operating Expenses 38 386 1595 2965 5404

1266

6

Operating

Profit

GP-Operating

Expenses 237 302 -447 -2627 -4630 -9378

Operating Profit Ratio 26.33 0.85 -0.27 -0.49 -0.37 -0.40

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2007 2008 2009 2010 2011 2012

-500.00%

0.00%

500.00%

1000.00%

1500.00%

2000.00%

2500.00%

3000.00%

GP ratio

Operating ratio

2. What is the strategy of the business?

Cost reduction strategy used by an entity whose results reflect in higher sales of the

business of ATH technologies from 2007 to 2012.

3. How should performance be measured and analyzed?

Particulars

20

07

200

8

200

9

201

0

201

1

201

2

Net Sales 9

1

0

0 354

39.

33

168

4

3.

76

537

7

2.1

9

126

41

1.3

5

233

49

0.8

5

GP

27

5

1

0

0 688

2.5

0

114

8

0.

67 338

-

0.7

1 774

1.2

9

328

8

3.2

5

Marketing and sales 38

1

0

0 386

10.

16

159

5

3.

13

296

5

0.8

6

540

4

0.8

2

126

66

1.3

4

R&D

10

09

1

0

0

171

6

1.7

0

282

7

0.

65

428

4

0.5

2

829

9

0.9

4

133

42

0.6

1

Net loss

15

61

1

0

0

400

0

2.5

6

705

7

0.

76

882

9

0.2

5

181

14

1.0

5

305

25

0.6

9

Cash and short term

investments

13

00

1

0

0

764

3

5.8

8

105

60

0.

38

234

1

-

0.7

8

-

545

-

1.2

3 546

-

2.0

0

Other current assets

16

7

1

0

0 839

5.0

2

157

0

0.

87

228

0

0.4

5

912

3

3.0

0

112

91

0.2

4

Net fixed assets

61

3

1

0

0

169

8

2.7

7

214

9

0.

27

252

3

0.1

7

757

6

2.0

0

130

30

0.7

2

4

-500.00%

0.00%

500.00%

1000.00%

1500.00%

2000.00%

2500.00%

3000.00%

GP ratio

Operating ratio

2. What is the strategy of the business?

Cost reduction strategy used by an entity whose results reflect in higher sales of the

business of ATH technologies from 2007 to 2012.

3. How should performance be measured and analyzed?

Particulars

20

07

200

8

200

9

201

0

201

1

201

2

Net Sales 9

1

0

0 354

39.

33

168

4

3.

76

537

7

2.1

9

126

41

1.3

5

233

49

0.8

5

GP

27

5

1

0

0 688

2.5

0

114

8

0.

67 338

-

0.7

1 774

1.2

9

328

8

3.2

5

Marketing and sales 38

1

0

0 386

10.

16

159

5

3.

13

296

5

0.8

6

540

4

0.8

2

126

66

1.3

4

R&D

10

09

1

0

0

171

6

1.7

0

282

7

0.

65

428

4

0.5

2

829

9

0.9

4

133

42

0.6

1

Net loss

15

61

1

0

0

400

0

2.5

6

705

7

0.

76

882

9

0.2

5

181

14

1.0

5

305

25

0.6

9

Cash and short term

investments

13

00

1

0

0

764

3

5.8

8

105

60

0.

38

234

1

-

0.7

8

-

545

-

1.2

3 546

-

2.0

0

Other current assets

16

7

1

0

0 839

5.0

2

157

0

0.

87

228

0

0.4

5

912

3

3.0

0

112

91

0.2

4

Net fixed assets

61

3

1

0

0

169

8

2.7

7

214

9

0.

27

252

3

0.1

7

757

6

2.0

0

130

30

0.7

2

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total assets

24

25

1

0

0

105

57

4.3

5

148

39

0.

41

775

5

-

0.4

8

165

09

1.1

3

252

36

0.5

3

Long term debt 0

1

0

0 0

0.0

0 0

0.

00 0

0.0

0

240

46

0.0

0

617

58

1.5

7

Common stock

47

45

1

0

0

160

81

3.3

9

264

93

0.

65

264

93

0.0

0

264

93

0.0

0

264

93

0.0

0

Retained earnings

25

70

1

0

0

657

0

2.5

6

136

27

1.

07

224

56

0.6

5

405

70

0.8

1

710

96

0.7

5

a) Which additional measures would you use to implement the strategy?

Ratio analysis is used by an entity to compare their current results with the previous

financial figures of an entity.

b) What are the characteristics of a good measure?

A good financial measure is easy to understandable approach by all the candidates in

a firm.

4. As a president of ATH technologies, what would you do to focus on the attention and

efforts of your employees?

Performance report is distributed among all the employees as positive or negative

results of the report will change the perspectives of the business.

3. PUSH TO PROFITABILITY

1. How did managers at ATH technologies achieve their profit and performance goals during

2013?

Balance score card approach used by the firm to develop all the goals according to

four pillars of an entity such as financial, internal control, innovation and customers and

stakeholders.

a) What role did control systems play in ATH’s success and problems?

In controlling system, an entity will keep watch on all the business activities through

dashboards that helps in improving individual’s performance.

5

24

25

1

0

0

105

57

4.3

5

148

39

0.

41

775

5

-

0.4

8

165

09

1.1

3

252

36

0.5

3

Long term debt 0

1

0

0 0

0.0

0 0

0.

00 0

0.0

0

240

46

0.0

0

617

58

1.5

7

Common stock

47

45

1

0

0

160

81

3.3

9

264

93

0.

65

264

93

0.0

0

264

93

0.0

0

264

93

0.0

0

Retained earnings

25

70

1

0

0

657

0

2.5

6

136

27

1.

07

224

56

0.6

5

405

70

0.8

1

710

96

0.7

5

a) Which additional measures would you use to implement the strategy?

Ratio analysis is used by an entity to compare their current results with the previous

financial figures of an entity.

b) What are the characteristics of a good measure?

A good financial measure is easy to understandable approach by all the candidates in

a firm.

4. As a president of ATH technologies, what would you do to focus on the attention and

efforts of your employees?

Performance report is distributed among all the employees as positive or negative

results of the report will change the perspectives of the business.

3. PUSH TO PROFITABILITY

1. How did managers at ATH technologies achieve their profit and performance goals during

2013?

Balance score card approach used by the firm to develop all the goals according to

four pillars of an entity such as financial, internal control, innovation and customers and

stakeholders.

a) What role did control systems play in ATH’s success and problems?

In controlling system, an entity will keep watch on all the business activities through

dashboards that helps in improving individual’s performance.

5

b) How could top management have avoided the actions by employees that led to the FDA

investigation?

Reason behind the frauds takes places in an entity communicated to all the employees

in an entity to overcome all the problems.

c) What are the possible consequences of these events on the company’s reputation?

Increase in sales in return increases the profitability of the firm induces the business

image and its goodwill which helps in attracting large number of customers.

2. If you were the president of ATH, what would you do to get the business back on track?

FDA investigation of the firm is done had spoil the image of the business due to lower

quality of goods. This problem can avoid by the firm by providing high quality services.

4. REFOCUS ON PROCESS: 2014-2015

1. Why did senior managers introduce a vision and belief statement?

To attract customers and potential investors to be part of the business who have

contributed for all their customers.

2. Why did managers at ATH Technologies change their performance measures?

Senior managers have changes their performance measures to overcome all their

problems. They have changed their goals by seeking feedback of all their personnel.

a) John Frost includes both process and output measures. Why? What is he trying to

accomplish?

John Frost includes both processes and end results measures to tests the quality of

generated output by using good method (Assess company’s performance, 2017).

b) He also includes ratio and ordinal measures. What are the advantages and issues of each

type?

Particular

s Formula

20

07

20

08

20

09

201

0

201

1

201

2

201

3 2014 2015

Net Sales 9

35

4

16

84

537

7

126

41

233

49

953

81

1400

80

1964

92

GP

27

5

68

8

11

48 338 774

328

8

578

96

8860

0

1227

95

GP ratio GP/Net sales

30.

6 1.9 0.7 0.1 0.1 0.1 0.6 0.6 0.6

Operating expenses 38

38

6

15

95

296

5

540

4

126

66

213

08

3318

8

3749

1

Operating Profit 23 30 - - - - 365 5541 8530

6

investigation?

Reason behind the frauds takes places in an entity communicated to all the employees

in an entity to overcome all the problems.

c) What are the possible consequences of these events on the company’s reputation?

Increase in sales in return increases the profitability of the firm induces the business

image and its goodwill which helps in attracting large number of customers.

2. If you were the president of ATH, what would you do to get the business back on track?

FDA investigation of the firm is done had spoil the image of the business due to lower

quality of goods. This problem can avoid by the firm by providing high quality services.

4. REFOCUS ON PROCESS: 2014-2015

1. Why did senior managers introduce a vision and belief statement?

To attract customers and potential investors to be part of the business who have

contributed for all their customers.

2. Why did managers at ATH Technologies change their performance measures?

Senior managers have changes their performance measures to overcome all their

problems. They have changed their goals by seeking feedback of all their personnel.

a) John Frost includes both process and output measures. Why? What is he trying to

accomplish?

John Frost includes both processes and end results measures to tests the quality of

generated output by using good method (Assess company’s performance, 2017).

b) He also includes ratio and ordinal measures. What are the advantages and issues of each

type?

Particular

s Formula

20

07

20

08

20

09

201

0

201

1

201

2

201

3 2014 2015

Net Sales 9

35

4

16

84

537

7

126

41

233

49

953

81

1400

80

1964

92

GP

27

5

68

8

11

48 338 774

328

8

578

96

8860

0

1227

95

GP ratio GP/Net sales

30.

6 1.9 0.7 0.1 0.1 0.1 0.6 0.6 0.6

Operating expenses 38

38

6

15

95

296

5

540

4

126

66

213

08

3318

8

3749

1

Operating Profit 23 30 - - - - 365 5541 8530

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 2

44

7

262

7

463

0

937

8 88 2 4

Operating

ratio

Operating

profit/net sales

26.

3 0.9

-

0.3 -0.5 -0.4 -0.4 0.4 0.4 0.4

Operating profit ratio and gross profit ratio come under profitability ratio to tests the

profitability generates by an entity from one period to another.

c) Why did John Frost include departmental performance in the bonus scheme?

Departmental performance has included in an entity to know the sales figure of the

business of different years.

3. What are the risks for ATH technologies going forward? How should these risks be

measured and controlled?

Risks incurred in ATH technologies

Increasing costs

Higher tax imposed on an entity

Higher bonus reduces income capability of the business

Risk matrix created by an entity to know the likelihood of all the risks that incurred in an

entity.

5. NEW MANAGEENT 2016-2017

1. Why did ATH technologies experience problems with its new products? What role did

measurement and control systems play in these problems?

Customers are loyal towards regular products offers by an entity. Measurement and

controlling systems created by the firm by preparing Ansoff matrix for market penetration to

introduce new products in the current market.

2. How should Janet Isabella design and use performance management and control system to

implement her agenda and take charge of the situation?

Customer service plan prepared by an entity to focus on all the needs and expectations

of all the customers in the external business market.

a) What are the critical performance drivers of success going forward?

Increase in sales goals

Timely completion of targets

7

44

7

262

7

463

0

937

8 88 2 4

Operating

ratio

Operating

profit/net sales

26.

3 0.9

-

0.3 -0.5 -0.4 -0.4 0.4 0.4 0.4

Operating profit ratio and gross profit ratio come under profitability ratio to tests the

profitability generates by an entity from one period to another.

c) Why did John Frost include departmental performance in the bonus scheme?

Departmental performance has included in an entity to know the sales figure of the

business of different years.

3. What are the risks for ATH technologies going forward? How should these risks be

measured and controlled?

Risks incurred in ATH technologies

Increasing costs

Higher tax imposed on an entity

Higher bonus reduces income capability of the business

Risk matrix created by an entity to know the likelihood of all the risks that incurred in an

entity.

5. NEW MANAGEENT 2016-2017

1. Why did ATH technologies experience problems with its new products? What role did

measurement and control systems play in these problems?

Customers are loyal towards regular products offers by an entity. Measurement and

controlling systems created by the firm by preparing Ansoff matrix for market penetration to

introduce new products in the current market.

2. How should Janet Isabella design and use performance management and control system to

implement her agenda and take charge of the situation?

Customer service plan prepared by an entity to focus on all the needs and expectations

of all the customers in the external business market.

a) What are the critical performance drivers of success going forward?

Increase in sales goals

Timely completion of targets

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Work allocation according to interests

b) What variables should be measured?

Market segment

New customer base

c) How easy or difficult should goals be?

Identifying new customer base is difficult for an entity as it requires deep knowledge

of the external market.

d) How should financial expectations be set and communicated?

Financial goals is to be set by an entity by including in the annual reports of the business

3. How can Janet Isabella use control systems to scan the competitive environment to ensure

that the business is not again surpassed by new technology?

Environmental scanning is used to scan the events in the atmosphere to consider the

best suitable strategies.

4. What events or employee actions could put business objectives at risk? How would you

ensure that these risks are adequately communicated and controlled?

Increasing number of customers affects the current sales figure of the business

Market segmentation strategies used by an entity to evaluate all the customers in the market.

5. How would you measure and evaluate Scepter’s decision to purchase ATH’s technologies

in 2011?

Business acquisition amount evaluates by an individual to know the prospective worth

of the business of ATH technologies.

8

b) What variables should be measured?

Market segment

New customer base

c) How easy or difficult should goals be?

Identifying new customer base is difficult for an entity as it requires deep knowledge

of the external market.

d) How should financial expectations be set and communicated?

Financial goals is to be set by an entity by including in the annual reports of the business

3. How can Janet Isabella use control systems to scan the competitive environment to ensure

that the business is not again surpassed by new technology?

Environmental scanning is used to scan the events in the atmosphere to consider the

best suitable strategies.

4. What events or employee actions could put business objectives at risk? How would you

ensure that these risks are adequately communicated and controlled?

Increasing number of customers affects the current sales figure of the business

Market segmentation strategies used by an entity to evaluate all the customers in the market.

5. How would you measure and evaluate Scepter’s decision to purchase ATH’s technologies

in 2011?

Business acquisition amount evaluates by an individual to know the prospective worth

of the business of ATH technologies.

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.