Commerce National Bank: Athletequip Inc. Case Analysis

VerifiedAdded on 2023/06/10

|7

|1506

|403

Case Study

AI Summary

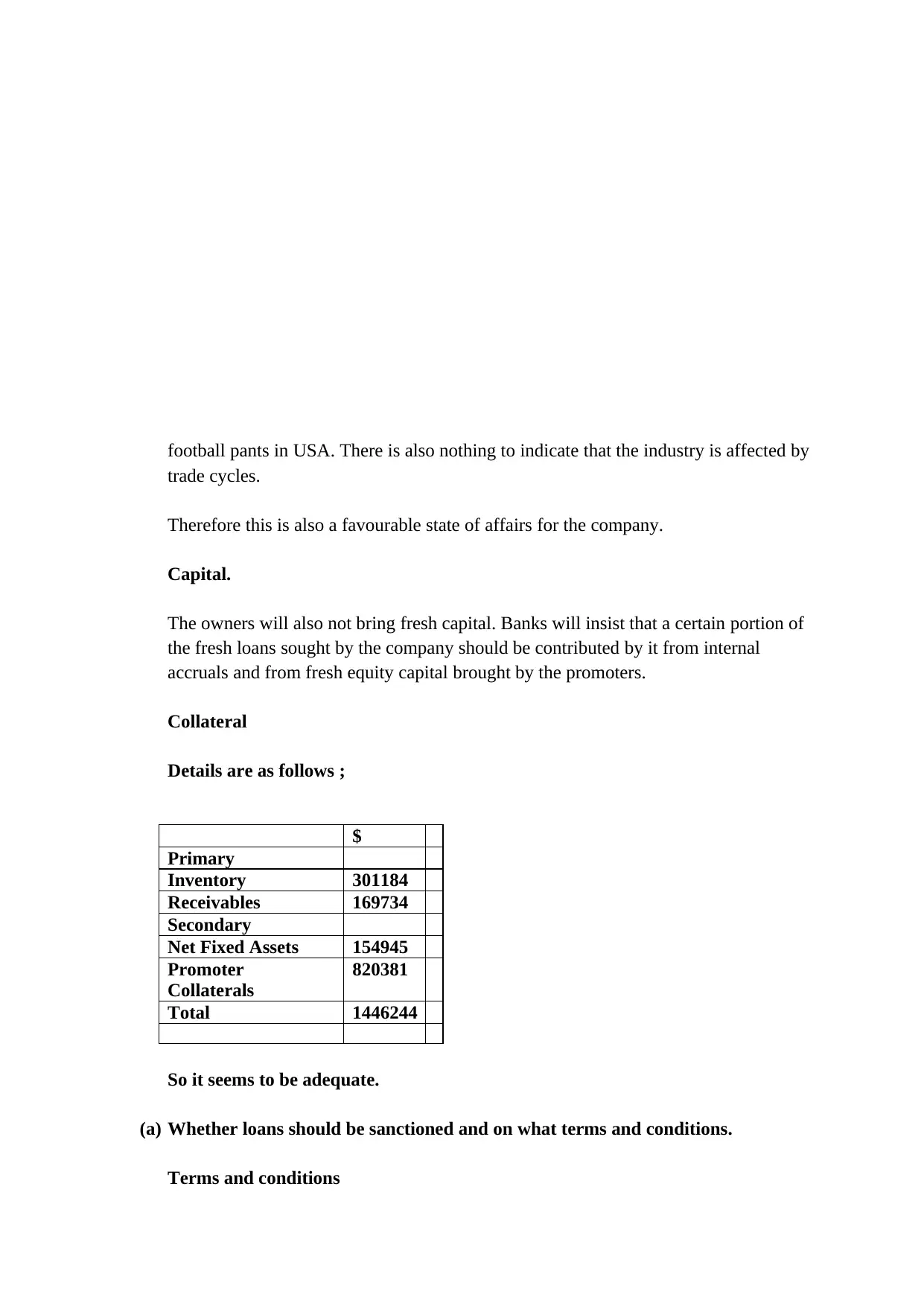

This case study analyzes Athletequip Inc., a company seeking a line of credit from Commerce National Bank. The analysis focuses on the bank's evaluation of the company based on the 5Cs of credit: Character, Capacity, Condition, Capital, and Collateral. The analysis examines the company's financial statements, including balance sheets, income statements, and industry comparisons. The study assesses the company's profitability, liquidity, and debt-equity ratio to determine whether the loan should be sanctioned, the appropriate terms and conditions, and the associated risks for both the bank and the company. The study provides recommendations for loan terms, including requirements for audited financial statements, collateral, and ongoing monitoring. The conclusion emphasizes the need for careful monitoring of the company's performance, particularly its profitability, and highlights the importance of a thorough risk assessment before approving the loan.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.