Project Report: Analysis of Atlas Iron Limited's Corporate Accounting

VerifiedAdded on 2020/05/28

|8

|1961

|54

Project

AI Summary

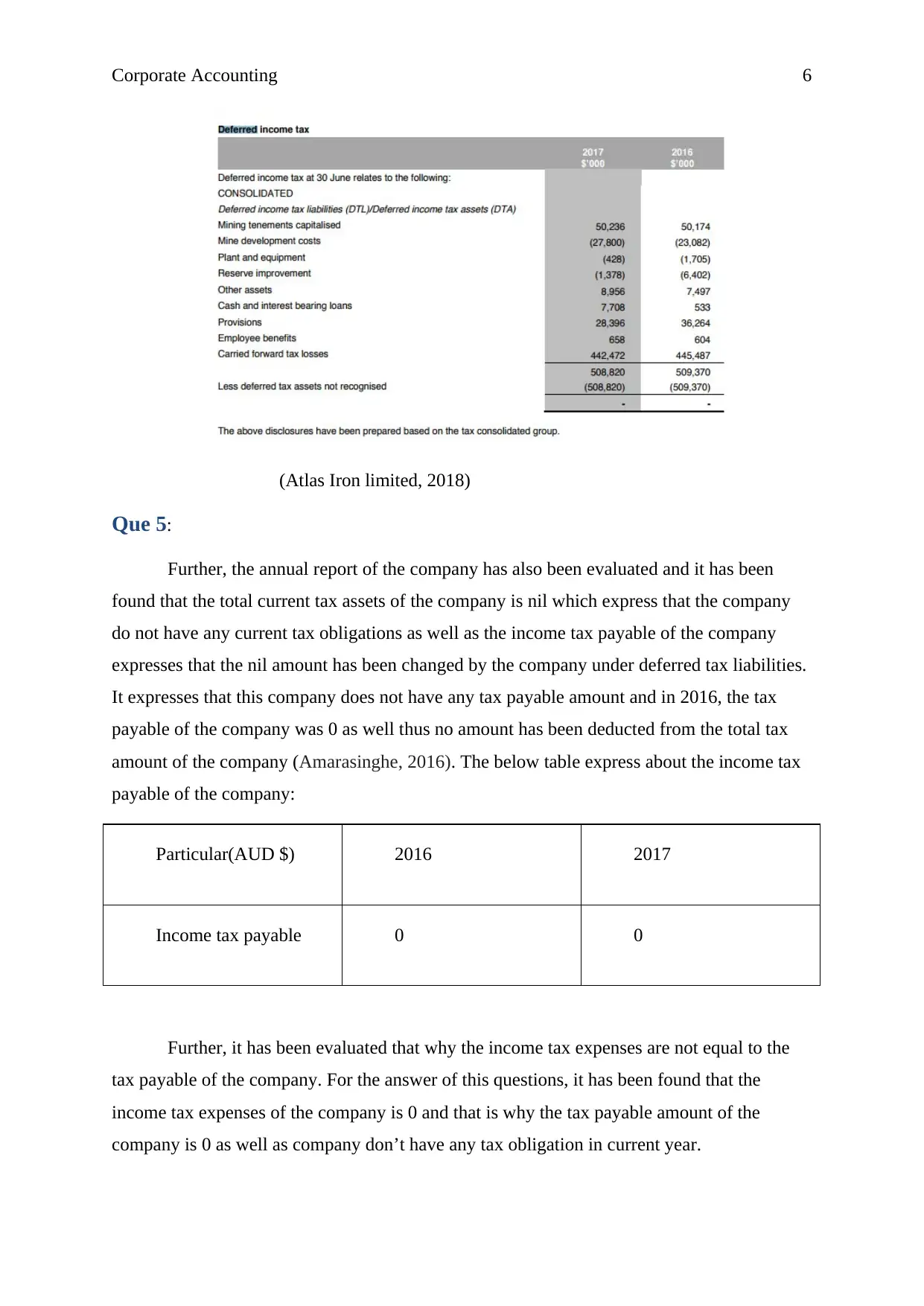

This project report provides a comprehensive analysis of the corporate accounting practices of Atlas Iron Limited. The report examines the company's equity structure, including share capital, reserves, and accumulated losses, and analyzes the company's tax payments to the government. The analysis reveals that Atlas Iron Limited has effectively utilized tax planning strategies, resulting in zero income tax payable. The report delves into the differences between tax expenses and tax payable, exploring the impact of deferred tax liabilities and current tax assets. The study evaluates the company's income tax expenses and paid income tax amounts, comparing the income statement and cash flow statement. The report highlights interesting and surprising aspects of the company's tax recording, along with the difficulties encountered in managing effective tax planning. The report uses the annual report of Atlas Iron limited and relevant accounting rules and regulations to support the analysis. The report concludes with an assessment of the company's corporate governance program and its impact on tax reporting, and the report has references to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.